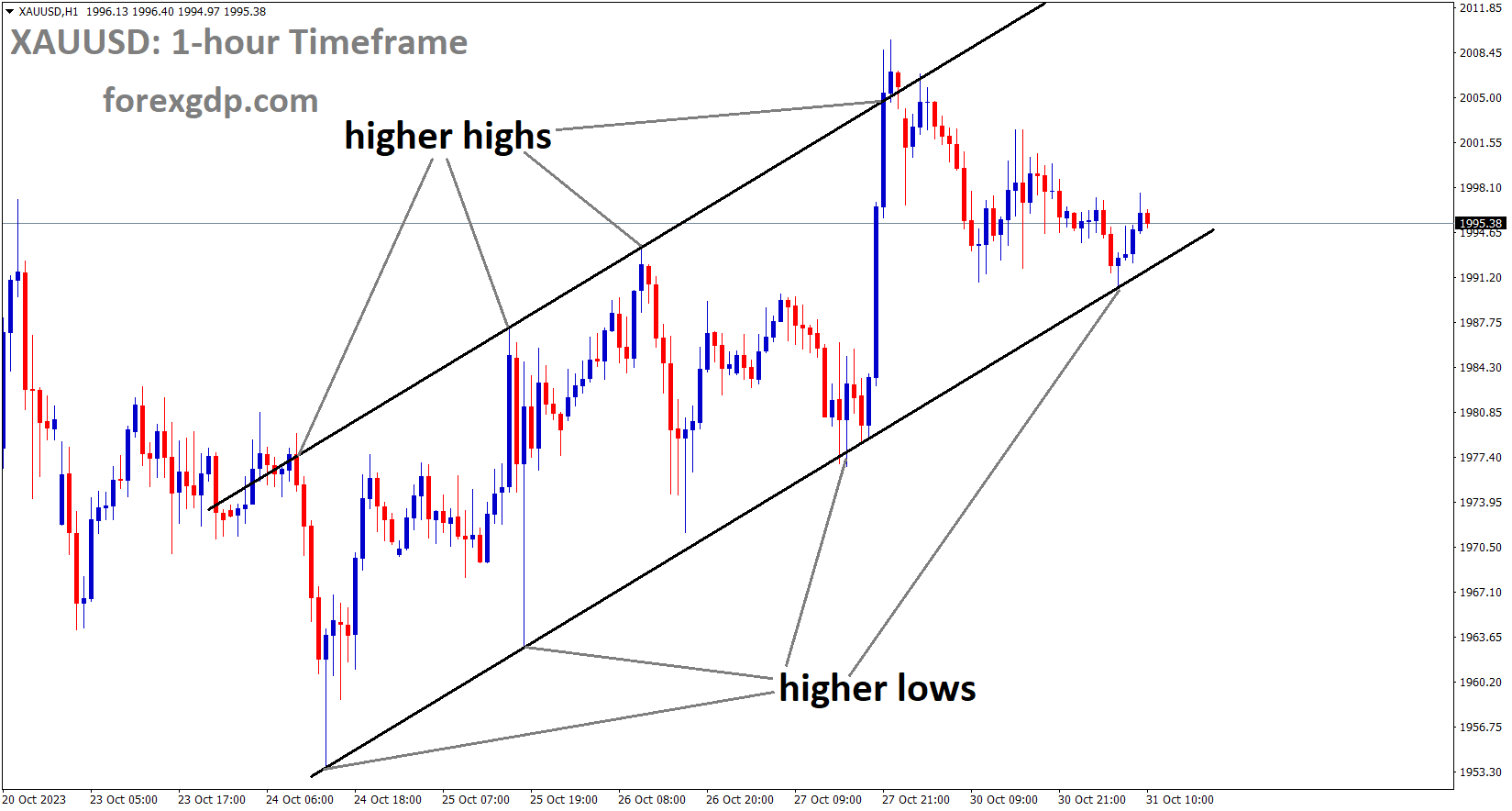

Gold Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices continue to stay in the green, supported by ongoing Middle East tensions that persist in the market. With the Federal Reserve’s interest rate decision looming tomorrow, there is still significant demand for gold compared to the US Dollar.

The ongoing escalation of military activity in Gaza continues to drive up the price of gold, pushing the precious metal to a fresh five-month high on Friday. The persistent demand for safe-haven assets is expected to persist, and we may see a re-test of resistance around the $2,009 per ounce mark in the days ahead. While the primary catalyst for gold’s price surge is geopolitical tensions, this week’s economic calendar includes several high-impact data releases and events that could also influence the precious metal’s value.

This week, we are anticipating policy decisions from the Federal Reserve, the Bank of Japan, and the Bank of England, all of which have the potential to surprise the market and introduce increased volatility. On the economic front, important releases such as US consumer confidence, ISM manufacturing data, and the monthly US Jobs Report are scheduled, with particular focus on the Non-Farm Payrolls (NFP) release, which is closely watched.

Gold is expected to consolidate within the $2,000 per ounce range before making a push towards higher price levels. The chart shows a positive outlook, with support levels at approximately $1,987 per ounce and $1,971 per ounce (representing a 23.6% Fibonacci retracement). Additionally, the 20-day simple moving average crossing above the 50-day simple moving average underscores the recent strength of the precious metal. If we witness a confirmed breakthrough above $2,009 per ounce, the next significant resistance level to watch for would be around $2,050 per ounce.

Silver Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The US Dollar is exhibiting increased strength against its counterpart currencies, with the eagerly anticipated Federal Reserve interest rate decision scheduled for tomorrow. This surge in the US Dollar’s value is attributed to robust economic data from the United States.

On Monday, the US Dollar (USD) faced a decline, falling to a level below 106.10 as measured by the DXY Index, which assesses the USD’s value against a basket of global currencies. This weakening of the USD was primarily driven by an influx of risk-on sentiment, which made it challenging for the currency to attract demand. With a relatively uneventful economic calendar on Monday, investor attention now turns to key events scheduled for the remainder of the week, notably the Federal Reserve (Fed) Interest Rate Decision on Wednesday and Nonfarm Payrolls data due on Friday. Both of these events hold the potential to influence the dynamics of the USD’s price.

The US economy continues to display strength, providing some support to the USD in recent sessions. However, the likelihood of a 25 basis point interest rate hike in December, as indicated by data from the CME Group FedWatch tool, remains low. This factor hinders any substantial strengthening of the USD. A pause in rate hikes is largely anticipated before Wednesday’s Fed meeting, but investors will closely scrutinize Fed Chair Jerome Powell’s stance and outlook to gain insights into the Fed’s future decisions.

The USD DXY Index dropped to around 106.10, marking a 0.40% decline for the day and reaching its lowest level since the previous Tuesday. The USD faces challenges in maintaining the momentum it had gained in the preceding week, as profit-taking by buyers takes place. Investors are also reviewing high-impact economic reports released last week in anticipation of the Fed’s decision on Wednesday.

On Friday, the US Bureau of Economic Analysis reported that the Personal Consumption Expenditures (PCE) Price Index for September matched expectations, coming in at 3.4% year-on-year, in line with the consensus and consistent with its previous reading of 3.4%. The Core PCE decreased to 3.7% year-on-year. Furthermore, last Thursday’s data from the US Bureau of Economic Analysis revealed that preliminary estimates for Gross Domestic Product (GDP) in the third quarter exceeded expectations. The headline figure indicated an annualized growth rate of 4.9%, surpassing the consensus of 4.2% and accelerating from the 2.1% growth observed in the second quarter.

Simultaneously, US Treasury yields have been on the rise, with the 2-year rate reaching 5.05%, and the longer-term 5-year and 10-year rates advancing towards 4.83% and 4.91%, respectively. This upward movement in yields may mitigate the losses of the Greenback.

As investors prepare for the Fed’s decision on Wednesday, the CME Group FedWatch Tool indicates that the probability of a 25 basis point rate hike in December remains low, standing at approximately

USDJPY Analysis:

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Today, the Bank of Japan has decided to keep its interest rate unchanged. During the BoJ press conference, it was announced that they are raising the inflation target to a higher level. Furthermore, they intend to maintain their accommodative monetary policy stance, and there is no possibility of a rate hike in 2023.

And In September, Japan’s unemployment rate improved to 2.6%, down from the previous reading of 2.7%. However, retail sales experienced a year-on-year decline of 5.8% in September, slightly below the expected 5.9% and down from the previous month’s figure of 7.0%.

Bank of Japan (BOJ) Governor Kazuo Ueda addressed the press conference following the October policy meeting on Tuesday. During this meeting, the focus will be on analyzing the impact of the government’s policies once they are announced. Up until now, we have not witnessed a significant upgrade in the inflation outlook driven by what we refer to as the ‘2nd force,’ which encompasses demand-driven factors. It is crucial for currencies to exhibit stability that aligns with their underlying fundamentals. We anticipate that the likelihood of our monetary policy falling behind the curve will remain low. A substantial portion of the revision in the CPI forecast is attributed to the longer-than-expected increase in commodity prices. Notably, considerable volatility in the foreign exchange market could have adverse effects on the overall economy.

We maintain a close working relationship with the government and diligently monitor the forex situation. Through flexible market operations, we aim to contain speculative movements in the market. Furthermore, we are inclined to allow greater flexibility in response to non-speculative market shifts based on fundamental factors. As we did in July, the decision to introduce flexibility in Yield Curve Control (YCC) today partly serves to prevent financial market turbulence, including fluctuations in foreign exchange rates. From a practical standpoint, it would be challenging for BOJ staff to ascertain whether the day-to-day rise in long-term yields is driven by speculative factors. In practice, we may need to repeatedly assess and take action to curb rising yields by analyzing the pace of change and making subsequent judgments. Until we achieve our inflation target, both YCC and the negative interest rate policy will remain in effect.

According to official data released by the Japan Statistics Bureau on Tuesday, Japan’s Unemployment Rate for September improved to 2.6%, down from the previous figure of 2.7%. This aligns with the market’s consensus expectation of a 2.6% reading for the reported period. In addition, Japan’s Retail Trade recorded a year-on-year decrease, falling to 5.8% in September from the previous reading of 7.0%. This figure fell short of the market’s anticipated 5.9%, as reported by the Ministry of Economy, Trade, and Industry on Tuesday.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

In the third quarter of 2023, the Swiss National Bank (SNB) reported a loss of 12.04 billion francs. This loss was attributed to various factors, including 9.00 billion francs from foreign exchange (FX), 132 million francs from gold investments, and the remainder primarily stemming from interest payments to commercial banks.

The Swiss National Bank (SNB) reported a loss of 12.04 billion Swiss francs ($13.36 billion) for the third quarter. This loss was attributed to a combination of factors, including losses on gold holdings, foreign currency investments, and Swiss franc positions. Specifically:

- The SNB incurred a loss of 9.16 billion Swiss francs from its foreign currency positions during the three-month period ending in September. This decline was due to falling bond and equity prices, driven by concerns that global interest rates would remain elevated for an extended period.

- The central bank also recorded a valuation loss of 132 million Swiss francs on its holdings of 1,040 metric tons of gold, primarily due to a decrease in global gold prices.

- Additionally, there was a loss of 2.66 billion Swiss francs from Swiss franc positions, primarily attributable to interest payments made to commercial banks.

During the first nine months of the year, the SNB paid 5.4 billion Swiss francs in interest to commercial banks for overnight deposits. The SNB mentioned that it was reducing this interest rate after costs surged when negative rates turned positive in September 2022.

As a result of these losses across all three categories, the SNB’s profit for the first nine months of the year decreased to 1.7 billion Swiss francs, down from the 13.7 billion Swiss francs reported in the first half of the year. The SNB’s financial results have been notably volatile in recent years, primarily due to its substantial foreign currency investments, which it had built up during an extended campaign to weaken the Swiss franc.

The SNB acknowledged the inherent volatility in its financial results, as they are closely tied to developments in the gold, foreign exchange, and capital markets. The central bank emphasized that strong fluctuations should be anticipated, and definitive conclusions regarding the annual result can only be drawn at a later date. It’s worth noting that in 2022, the SNB recorded a historic loss of 132.5 billion Swiss francs, marking the largest loss in the central bank’s 115-year history.

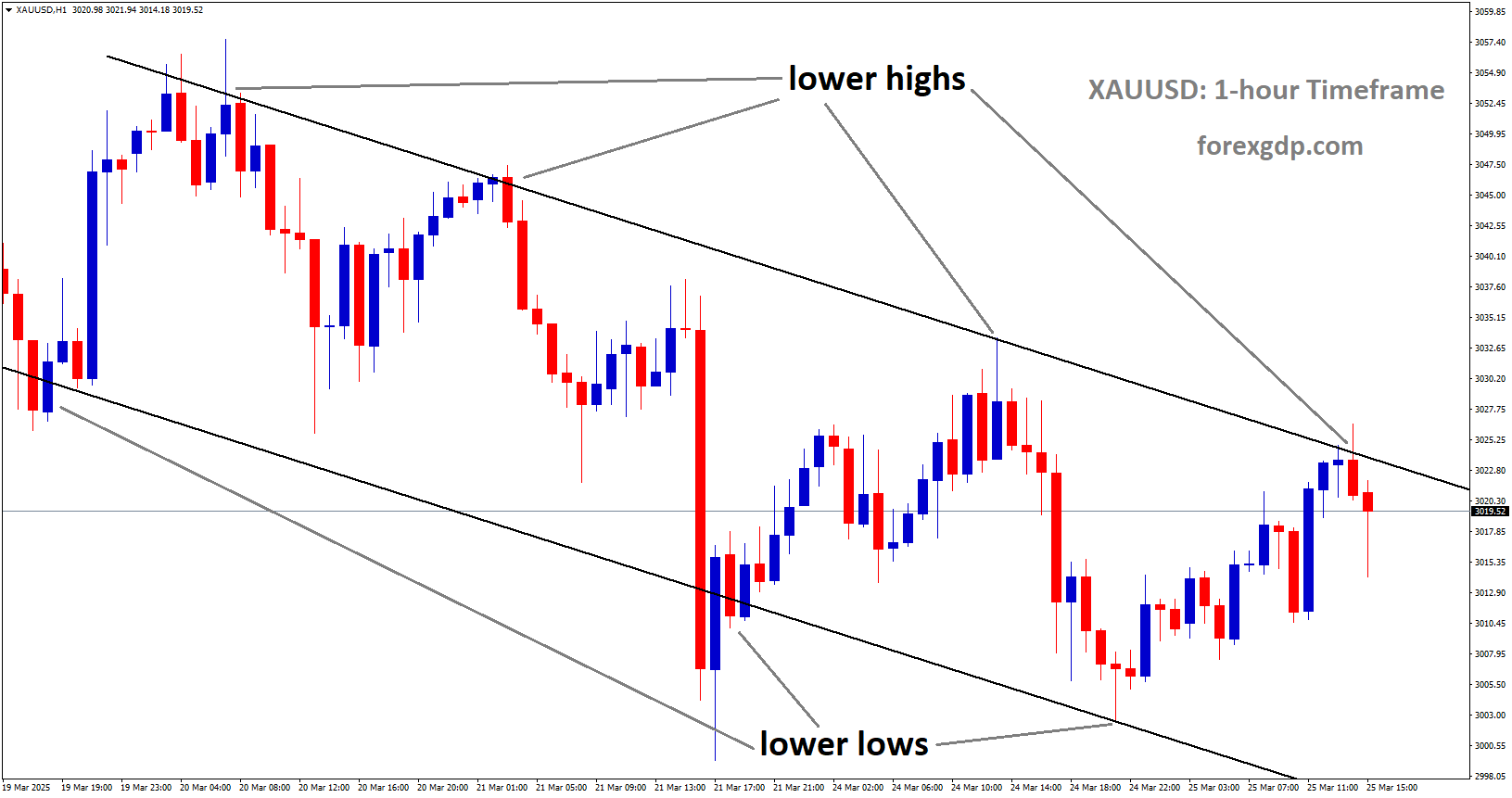

EURUSD Analysis:

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In September, German retail sales unexpectedly dipped by -0.80%, in contrast to the anticipated 0.50% increase and following a -1.2% decline in August. This marginally improved data compared to the previous month has bolstered the Euro against the USD.

decline")

According to the most recent official data from Destatis released on Tuesday, Germany’s Retail Sales experienced a 0.8% month-on-month (MoM) decline in September, which was unexpectedly lower than the anticipated 0.5% increase. This decline follows a -1.2% drop observed in August. On an annual basis, Retail Sales in the Eurozone’s leading economy contracted by 4.3% in September, a more substantial decline compared to the 2.3% decrease recorded in August.

The Retail Sales data, provided by the Statistisches Bundesamt Deutschland, measures the changes in sales within the German retail sector, offering insights into its short-term performance. Percentage changes in this data reflect the rate of sales fluctuations, and these changes are closely monitored as an indicator of consumer spending trends. Typically, a positive economic growth outlook is considered bullish for the EUR currency, while a lower reading is viewed as “bearish” or negative for the EUR.

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The British Pound is undergoing a period of market consolidation, primarily driven by concerns stemming from heightened tensions in the Middle East. As the Bank of England prepares to announce its interest rate decision this week, the performance of the GBP is poised to fluctuate, hinging on the anticipated outcome. Depending on the expected results, the GBP may either weaken or strengthen.

The British pound closed the previous week with a downward trend, primarily due to a softening of inflationary pressures in the UK labor market and the release of weak PMI preliminary data.

The ongoing conflict between Israel and Hamas continues to create volatility, favoring safe-haven currencies like the USD over the British pound. Additionally, cracks in global stock markets have added to the decline in risk sentiment, fueled by disappointing corporate earnings.

This week, all eyes are on the upcoming interest rate decisions from the Bank of England (BoE) and the Federal Reserve. Neither central bank is expected to raise interest rates, but the focus will be on any revised forecasts and guidance regarding potential policy changes.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

Bank of Canada Governor Tiff Mackhlem has stated that inflation is currently well-managed, and if there is any uptick in inflation, they will not hesitate to implement rate hikes. Increasing interest rates are aimed at constraining economic activity and government spending.

")

Weaker Chinese Purchasing Managers’ Index (PMI) data has the potential to exert downward pressure on oil pricesBank of Canada Governor Tiff Macklem addressed lawmakers in the House of Commons on Monday, highlighting the intersection of elevated interest rates and subdued growth and its potential impact on government spending. While acknowledging the country’s sustainable fiscal position, Macklem emphasized the importance of exercising restraint in expenditure to protect social programs in the face of these economic dynamics.

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has reached the resistance area of the pattern

At the time of writing, Western Texas Intermediate (WTI) is trading below $82.50 per barrel. Traders are adopting a cautious stance in anticipation of the upcoming US Fed policy meeting, overshadowing previous support from Middle East tensions. The unexpected contraction of China’s NBS Manufacturing Purchasing Managers’ Index in September, dropping to 49.5 from the expected 50.2 expansion seen in July, has raised concerns. This shift below the critical 50 mark signals contraction and adds to worries about China’s economic conditions. Moreover, the NBS Services PMI echoed this trend, falling to 50.6, below the anticipated 51.8 and the previous reading of 51.7, further heightening concerns about the sluggish state of the Chinese economy.

AUDUSD Analysis:

AUDUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

Analysts are anticipating favorable Q3 CPI and retail sales data, which could pave the way for an interest rate increase at the upcoming RBA meeting next week.

The Australian Dollar put an end to its three-day winning streak on Tuesday, primarily due to the resurgence of the US Dollar, which weighed down the AUDUSD pair. Nonetheless, positive news came from Australian Retail Sales, lending support to the Aussie pair as investors looked ahead to the US Federal Reserve’s (Fed) policy decision scheduled for Wednesday. Additionally, the Reserve Bank of Australia is set to announce its policy decision on November 7, with expectations of a 25 basis point interest rate hike driven by elevated inflation. The preceding week saw Australia’s Consumer Price Index (CPI) expand in the third quarter of 2023, surpassing the growth seen in the second quarter. Furthermore, the seasonally adjusted Retail Sales (Month-on-Month) pleasantly surprised the market with a notably higher reading in September.

Adding to the mix, a Tuesday report from China revealed declines in both the manufacturing and non-manufacturing Manufacturing Purchasing Managers’ Index (PMI) for September, raising concerns about the sluggish economic conditions in the world’s second-largest economy. This development raises the potential for an impact on the Australian Dollar, given Australia’s status as China’s largest trading partner.

Meanwhile, the US Dollar Index (DXY) retraced recent losses ahead of the US Fed policy decision. The moderate economic data from the United States (US) released on Friday failed to provide support for the Greenback, as market participants anticipate the Fed maintaining its interest rates at 5.5% in the upcoming meeting. However, the December meeting is expected to be data-driven, with the CME Fedwatch tool indicating a 23% probability of a 25 basis point hike by the Fed in December.

saw a significant increase to 0.9%")

Australia’s Retail Sales (Month-on-Month) saw a significant increase to 0.9% in September, surpassing market expectations of 0.3% and the previous figure of 0.2%. Meanwhile, Australia’s Producer Price Index (PPI) exhibited a modest easing, dropping to 3.8% on a yearly basis in Q3 compared to the previous quarter’s 3.9%. On a quarterly basis, the nation’s PPI saw a notable rise to 1.8%, up from the previous reading of 0.5%. The Australian Consumer Price Index (CPI) for the third quarter of 2023 reached 1.2%, exceeding both the 0.8% uptick in the previous quarter and the market consensus of 1.1% for the same period.

Governor of the Reserve Bank of Australia, Michele Bullock, expressed heightened concern about the inflation impact stemming from supply shocks. Bullock stated that if inflation persists above projections, the RBA will take responsive policy measures. Additionally, there is an observable deceleration in demand, with per capita consumption on the decline.

China’s NBS Manufacturing Purchasing Managers’ Index (PMI) took an unexpected turn in September, contracting to 49.5 from the 50.2 expansion observed in July and falling short of the market consensus of 50.2. Similarly, the NBS Services PMI experienced a decline, dropping to 50.6 in September, compared to the anticipated figure of 51.8 and the previous reading of 51.7. Reports suggest that there is a tentative agreement between the US and China for a meeting between Presidents Joe Biden and Xi Jinping in November, following months of diplomatic efforts to mend relations.

The US Core Personal Consumption Expenditures Price Index (YoY) showed a slight decline to 3.7% from the previous reading of 3.8%. However, the monthly index showed an increase to 0.3%, in line with expectations and up from 0.1% previously. The University of Michigan Consumer Index surpassed expectations in October, reporting a figure of 63.8, which was expected to remain consistent at 63.0.

As the market awaits the Fed Interest Rate Decision on Wednesday, with expectations of interest rates remaining at 5.5%, investor attention will be directed towards key indicators such as the US ADP Employment Change and ISM Manufacturing PMI for October.

AUDNZD Analysis:

AUDNZD is moving in an Ascending triangle pattern and the market has rebounded from the higher low area of the pattern

In October, China’s PMI stood at 49.5, down from 50.2 the previous month, and the Services PMI recorded 50.6, a decrease from the previous month’s 51.7. This news prompted a decline in the strength of the New Zealand Dollar in the market.

The disappointing release of Chinese PMI data. China’s official Manufacturing PMI unexpectedly slipped into contraction territory for October, registering at 49.5 compared to the previous month’s 50.2. In addition, the services sector gauge also fell below consensus estimates, dropping to 50.6 from September’s 51.7. These data points have raised uncertainties about China’s economic recovery, which in turn has put pressure on antipodean currencies, including the New Zealand Dollar.

Conversely, the US Dollar has attracted some buying interest, supported by higher US Treasury bond yields driven by hawkish expectations regarding the Federal Reserve (Fed). However, downside movements remain limited as traders appear hesitant to make aggressive bets, with their focus now turning to the outcome of the highly anticipated two-day FOMC monetary policy meeting, which is set to be announced by the US central bank on Wednesday.

The Fed is widely expected to maintain the current status quo in its decision. Nevertheless, the continued strength of the US economy and persistent inflation levels leave the door open for another rate hike by the end of the year. As a result, investors will closely analyze the accompanying policy statement and listen to Fed Chair Jerome Powell’s remarks during the post-meeting press conference for insights into the potential future rate hike trajectory. Ahead of this key central bank event, the US economic calendar for Tuesday includes the release of the Chicago PMI and the Conference Board’s Consumer Confidence Index. These data releases will be closely monitored by traders for any short-term trading opportunities.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/