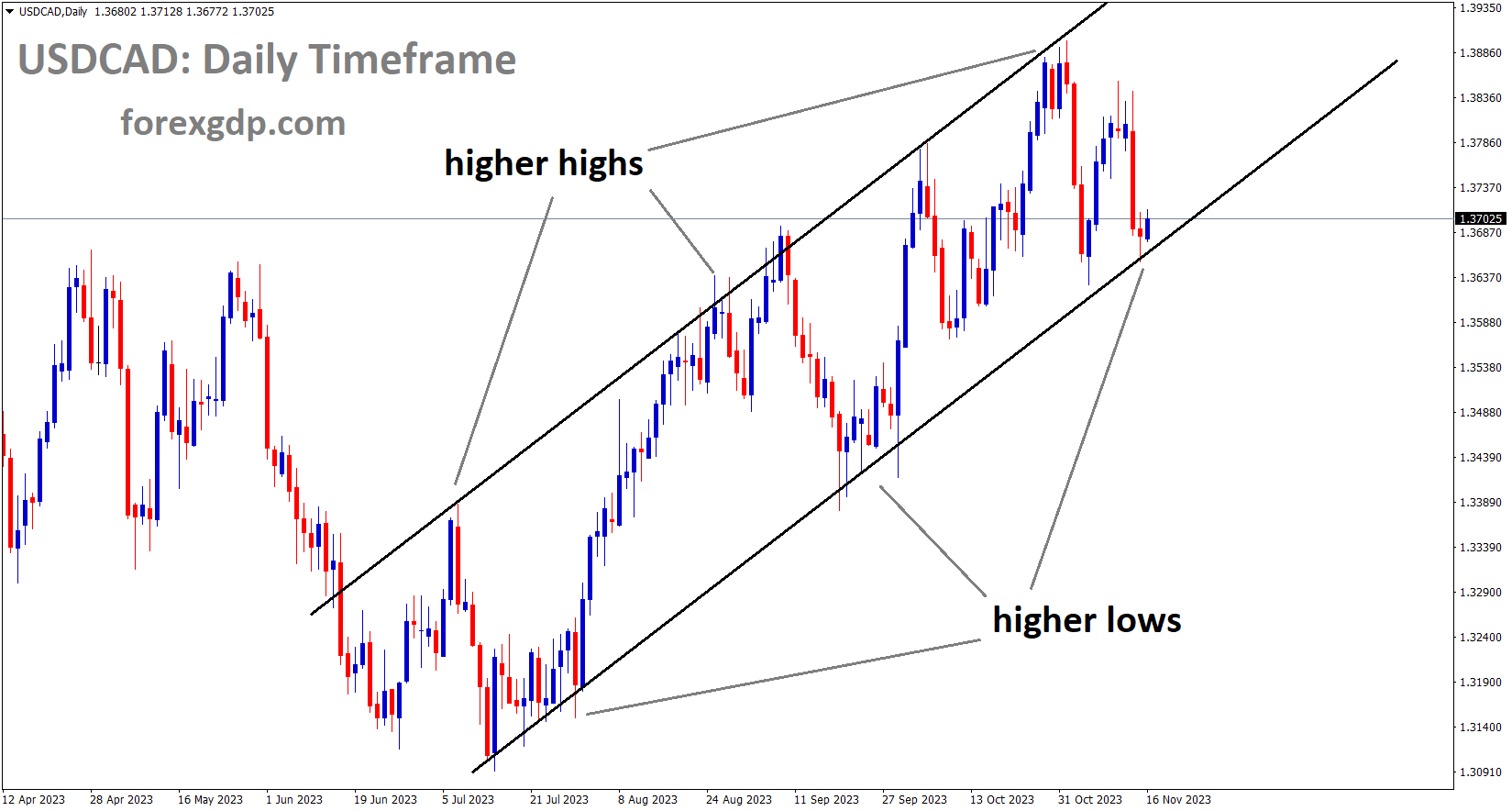

USDCAD Analysis:

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

Following the release of September’s Manufacturing Sales data, the Canadian Dollar strengthened as it showed a positive movement of 0.40%, surpassing the anticipated 0.10% decline. However, this figure is lower than the 1.0% recorded in August. Additionally, Wholesale Sales data for September indicated a decline of 0.40%, contrasting with the 1.8% reported in August.

The Canadian Dollar is experiencing further gains on Wednesday, extending its positive momentum as global markets digest recent risk-on sentiment. Canada’s wholesale and business sales figures exceeded expectations, providing support to the Loonie. However, the Canadian Dollar’s upward movement is constrained by declines in Crude Oil prices. The Loonie is marking its second consecutive day of gains against the US Dollar.

In September, Canadian Manufacturing Sales surpassed forecasts, registering a growth of 0.4% compared to the anticipated -0.1%. Despite this positive outcome, it retreated from August’s revised figure of 1.0%, which was upwardly revised from 0.7%. Wholesale sales for September softened, but still outperformed the flat forecast, printing at 0.4%, down from the previous month’s 1.8% revised down from 2.3%.

On the US front, data fell short of expectations, with Retail Sales for October declining from a revised 0.9% in September to -0.1%. Although contracting, it remained above the forecasted -0.3%. The annualized US Core Producer Price Index Ex Food & Energy for the year up to October also came in below expectations, printing at 2.4% against the forecast of 2.7%. The decline in Crude Oil prices on Wednesday is limiting the Canadian Dollar’s gains and Canadian Housing Starts and changes in employment insurance benefits recipients, providing additional data points for market participants to assess.

GOLD Analysis:

XAUUSD Gold price has broken the Descending channel in upside

Gold prices experienced an upward movement following the release of lower-than-expected Consumer Price Index (CPI) data in major global economies such as the United States and the United Kingdom. This outcome suggests a prospective scenario of no imminent interest rate hikes in the coming months.

Gold prices continued their ascent, although gains were trimmed as the United Kingdom joined the group of developed economies witnessing a potential easing of inflationary pressures. Official data revealed a two-year low in the annual headline consumer price rise for October, registering at 4.6%, a significant deceleration from the previous month’s 6.7%. This downturn was attributed, in part, to lower fuel prices. Even the core inflation measure, excluding fuel, decreased to 5.7% from 6.1%. The trend aligns with recent data from the US, where a reduction in price pressures was also observed, contributing to a positive environment for gold.

The hope of victory against inflation is gaining ground among investors, particularly as many central banks have raised interest rates. Anticipation is growing for potential interest rate cuts in the first half of the coming year. Despite gold’s reputation as an inflation hedge, it has faced challenges amid rising borrowing costs.

Investors have shifted towards more lucrative returns in bond markets, impacting both non-yielding assets like gold and riskier investments like equities. The recent boost in gold prices can be attributed, in part, to the softer inflation figures and geopolitical tensions in Ukraine and the Middle East.

However, caution is warranted as markets might be overly optimistic. Inflation, while showing recent weakness, remains above central bank targets in various regions globally. Interest rates are likely to remain stable as long as inflation persists. Historical lessons from the inflationary era of the 1970s underscore the difficulty of eradicating entrenched inflation, which may not follow the linear decline anticipated by current market expectations. Nevertheless, the current momentum favors gold bulls, with geopolitical uncertainties providing additional support.

Looking ahead, Friday brings heavyweight price data with the Eurozone’s final core CPI rate taking center stage. Expectations are for a slight easing to 4.2% from 4.5%. A print in line with expectations is likely to be well received by the gold market.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

In October, US retail sales witnessed a decline of 0.10%, marking a notable contrast to the 0.90% increase recorded in September. The US Dollar experienced devaluation following the release of this data on the last day.

US retail sales interrupted a streak of six consecutive positive performances, registering a 0.1% decline compared to September. Furthermore, September’s initially reported increase of +0.7% was revised upward to +0.9%. Retail sales have been a significant contributor to the robust performance of the US economy, playing a pivotal role in the impressive Q3 GDP outperformance driven by American consumers. However, leading indicators such as softened labor data, including NFP and average weekly earnings, along with a recent decrease in the Consumer Price Index (CPI), set a cautious tone ahead of the retail sales data release.

Interestingly, the market’s response appears to be influenced more by the actual retail sales figures rather than the consensus, with both the dollar and the 2-year treasury yield experiencing increases despite the month-on-month contraction in retail sales. As the holiday season approaches, markets are now turning their attention to the possibility of a “Santa rally,” assessing the potential market dynamics leading up to Christmas.

USDCHF Analysis:

USDCHF is moving in the Descending triangle pattern and the market has reached the support area of the pattern

The SNB is inclined to raise rates in the upcoming December meeting, a decision influenced by the industrial production figures set to be released this Friday. The Swiss Franc is gaining strength in the market due to global threats of war.

The US Dollar Index exhibited improvement following the release of economic data from the United States on Wednesday. October’s US Retail Sales showed a modest easing at 0.1%, contrary to expectations of a more pronounced decline of 0.3%. However, the unexpected decrease in the US Producer Price Index by 0.5%, compared to the anticipated 0.1% increase, and the decline in the annual PPI from 2.2% to 1.3%, raised concerns about potential challenges to progress on inflation.

This uncertainty justified the Federal Reserve’s cautious stance, even in the face of recent data showing a decline in inflation, introducing an element of unpredictability. The impending Fed policy decision for the December meeting has, in turn, garnered support for the USDCHF pair. Additionally, the USDCHF pair has experienced a rebound, driven by an increase in US Treasury yields, with the 2-year rate at 4.90% and 10-year rates at 4.50%, as of the current writing.

GBPCHF Analysis:

GBPCHF is moving in the Box pattern and the market has reached the support area of the pattern

Swiss National Bank Chairman Thomas Jordan, in an interview with a local television station, did not rule out the possibility of more interest rate hikes in the future. This statement may have contributed to upward support, shoring up the Swiss Franc in recent sessions. The focus on Friday will be on Swiss Industrial Production for the third quarter, providing insights into whether the Swiss National Bank (SNB) will consider an interest rate increase in the December meeting. However, attention will also be on the weekly US Jobless Claims to be released later in the North American session, offering further insights into the condition of the US labor market.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The UK Consumer Price Index for the third quarter showed a decrease to 4.6%, down from 6.7% in the preceding quarter. The primary contributors to this decline in inflation were the Food, Energy, and Services sectors.

UK inflation surpassed expectations with declines in both core and headline measures. The notable drop in food and energy prices played a significant role, contributing to a substantial decrease in goods inflation from 6.2% to 2.9% when comparing October 2023 to the same period last year. Services inflation, closely monitored, also experienced a modest decline from 6.9% to 6.6%. The significant 12-month decline in headline inflation is evident on the chart below and is likely to be praised by the UK government in anticipation of next week’s Autumn Statement.

Rishi Sunak had pledged to halve inflation by the end of 2023, and this latest development reinforces the belief that the Bank of England has concluded its interest rate hikes. However, inflation, average earnings, and services inflation continue to remain elevated, areas previously highlighted by the BoE as focal points. While average earnings have received less recent attention, the immediate market reaction following the release was relatively subdued. The impact on the gains propelled by yesterday’s lower US CPI has been minimal so far, despite the better-than-expected movement in UK inflation this morning.

GBPJPY Analysis:

GBPJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The third-quarter GDP for Japan was reported at -0.50%, a decline from the 1.1% growth in the previous quarter. The Bank of Japan’s recent actions on intervention and rate hikes have diminished compared to previous meetings. As a result, the weakness of the Japanese Yen (JPY) continues to persist in the market.

Strong Retail Sales figures in the US and disappointing Q3 Gross Domestic Product (GDP) figures from Japan have fueled dovish expectations regarding the Bank of Japan. In October, the US Producer Price Index reported a 1.3% increase, falling short of the expected 1.9% rise. Additionally, a monthly decline of 0.5% was observed, contrasting with the projected 0.1% growth. On the contrary, Retail Sales experienced a marginal decrease of 0.1%, surpassing the anticipated 0.3% contraction. Year-on-year, sales rose by 2.5%, indicating a slower growth rate compared to September’s 4.1% increase.

In response, the US Dollar garnered some demand as markets expressed concerns that robust data might prompt Federal Reserve officials to consider further tightening, leading to a rise in US Treasuries after the release. However, given the reports of cooling inflation and job creation figures, the prevailing sentiment suggests that the Federal Reserve is unlikely to hike in the upcoming December meeting.

On the Japanese Yen’s side, Japan’s Q3 GDP contracted by -0.5% QoQ, below expectations of -0.1% and significantly lower than the corresponding 1.2% growth recorded in Q2. This marks its weakest reading since Q1 2022. Consequently, Japanese Government Bond Yields experienced a sharp decline, reflecting the anticipation that the Bank of Japan won’t rush to hike rates due to the weakening economy. In alignment with this sentiment, the World Interest Rate Probabilities tool indicates a postponement in liftoff expectations until June.

AUDUSD Analysis:

AUDUSD is moving in the Box pattern and the market has fallen from resistance area of the pattern

The employment landscape experienced a significant shift, with the addition of 55,000 jobs, surpassing the anticipated 20,000 and surpassing the previous month’s figure of 6,700. The unemployment rate also saw a change, standing at 3.7% as opposed to the expected 3.6%.

The Australian Dollar faced a negative bias on Thursday following the release of Australian employment data. The seasonally adjusted Employment Change exceeded expectations, showing a rise of 55K in October compared to the anticipated 20K and the previous month’s 6.7K. However, the positive impact of this headline figure was somewhat diminished as the majority of the added jobs were part-time positions. Australia’s Unemployment Rate for October matched expectations at 3.7%, compared to the previous figure of 3.6%. Despite this, the AUDUSD pair experienced volatility in the prior session due to economic data released from the United States (US) on Wednesday.

Australia’s Wage Price Index met expectations, growing by 1.3% compared to the previous reading of 0.8%, with a year-over-year increase of 4.0%, exceeding the anticipated 3.9%. On the sentiment front, Australia’s Westpac Consumer Confidence declined by 2.6% in November, reversing the previous growth of 2.9%.

AUDCHF Analysis:

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

RBA Assistant Governor Marion Kohler remarked that the slowdown in inflation is expected to be slower than initially anticipated. This is attributed to the sustained high level of domestic demand and robust pressures from labor and other costs. Kohler emphasized the necessity for a tighter policy to address the challenges posed by elevated inflation. The National Australia Bank (NAB) economists foresee another 25 basis points hike in February following Q4 inflation data, with rate cuts unlikely until November 2024.

Turning to China, Industrial Production (YoY) in October showed growth at 4.6%, a slight increase from the previous 4.5%, contrary to expectations of consistency. Retail Sales year-over-year experienced an uptick to 7.6%, surpassing the anticipated 7.0%. Meanwhile, in the US, the Consumer Price Index for October reported lower readings than expected, with the annual rate slowing from 3.7% to 3.2%, below the consensus forecast of 3.3%. The monthly CPI reduced to 0.0% from 0.4%, while the US Core CPI rose by 0.2%, falling short of expectations at 0.3%, and the annual rate decreased to 4.0% from the previous 4.1%. Lastly, the US Monthly Budget Statement reported a deficit of $67B in October, compared to the expected deficit of $65B.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The Chinese government’s announcement of injecting 1 trillion Yuan into the property sector to address concerns served as a catalyst for the New Zealand Dollar (NZD), leading to an upward movement in its value.

The New Zealand Dollar experienced an upward boost thanks to positive economic data from China, enhancing the trade outlook for the country. China’s injection of 1 trillion Yuan in low-cost financing for its property sector, aimed at alleviating concerns about a credit crunch, is a strategic move with potential ripple effects on global economies, including New Zealand. The Kiwi Dollar benefitted from the favorable impact of this positive news flow from China, particularly given New Zealand’s status as a major exporter of dairy products to the Chinese market. The improved economic prospects and increased demand for the NZD are closely tied to these developments.

However, on Thursday, data revealed a 0.38% decline in China’s House Price Index for October, signaling a deteriorating condition in China’s property sector. Concurrently, the US Dollar Index strengthened following Wednesday’s release of economic data from the United States, marking a second consecutive day of gains. At the time of writing, the spot price hovers around 104.50.

In the US, October’s Retail Sales showed a modest easing at 0.1%, below the expected decline of 0.3%, potentially posing challenges to progress on US inflation. The Federal Reserve’s cautious stance, despite recent soft inflation data, introduces an element of uncertainty into the market. Additionally, the unexpected 0.5% decline in the US Producer Price Index (PPI), compared to the anticipated 0.1% increase, and the drop in the annual PPI from 2.2% to 1.3%, may moderate market sentiment regarding further rate hikes by the Fed. Market participants are likely anticipating insights from the upcoming release of the weekly US Jobless Claims later in the North American session, especially considering the US labor market’s potential role as a catalyst for higher inflation, which could influence overall market dynamics.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/