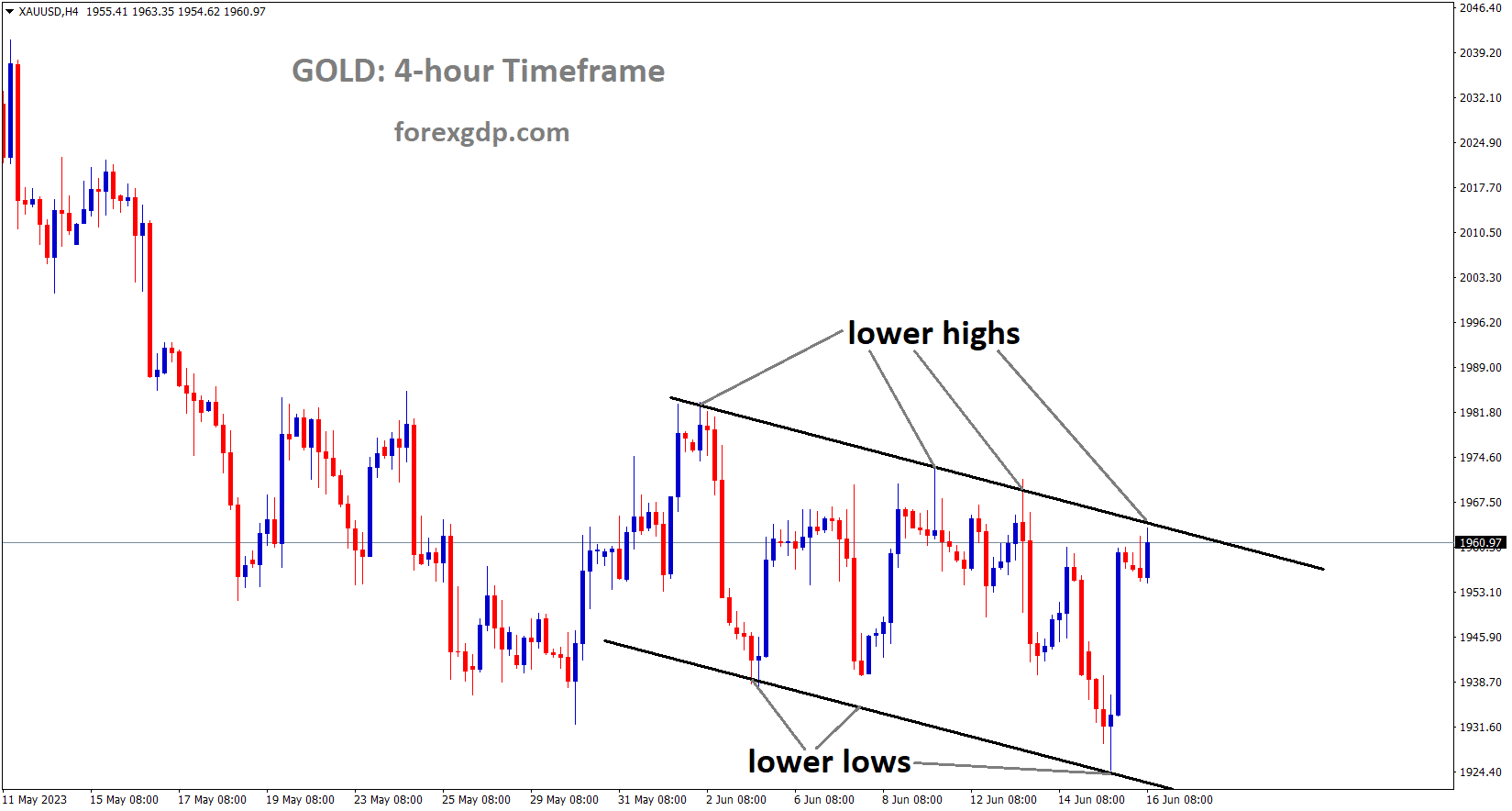

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Today, gold prices have surged significantly against the USD following an incident on Sunday where Yemen Houthi rebels targeted three commercial ships in the Red Sea. In response, a US Warship intercepted and shot down three drones deployed by the rebels. Iran has aligned itself with the rebels, taking a stand against Israel in this event.

The price of gold reached a new record high, nearing $2,150 at the start of the week, driven by heightened geopolitical tensions in the Middle East. The US economic docket for Monday features October Factory Orders as the sole highlighted data. Investors will closely monitor updates on the Israel-Hamas conflict and statements from central bankers.On Sunday, Yemen’s Houthi rebels targeted three commercial ships in the Red Sea, prompting a response from a US warship, which successfully intercepted three drones. The US military’s Central Command stated that there is a strong belief that these attacks, attributed to the Houthis in Yemen, are facilitated by Iran. In acknowledgment, the Houthi movement in Yemen confirmed targeting two Israeli ships, citing their response to calls from Islamic nations to support the Palestinian cause.

SILVER Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

Last week, Federal Reserve Chair Jerome Powell stated that the current interest rates are now at their peak to help mitigate inflation and bring it closer to our goals. Powell also emphasized the readiness to implement rate hikes if inflation shows signs of resurgence. Following these remarks, the USD experienced a decline.

The US Dollar Index has exhibited a modest decline, currently trading at 103.15, despite Federal Reserve Chair Jerome Powell adopting a hawkish stance. Although the November ISM Manufacturing PMI came in below expectations, it did not trigger significant downward movements in the Greenback. The apparent weakness in the currency is attributed to the market’s skepticism towards Powell’s hawkishness. Despite a cooling inflation and a mixed trend in the US labor market, the Fed surprisingly maintained a less dovish stance, keeping the door open for further policy tightening.

Key inflation indicators, such as the Consumer Price Index and Personal Consumption Expenditures , have shown a downward trend. However, the Fed has emphasized the need for more evidence of inflation cooling before considering any change in policy, indicating a potential for further tightening.

Chair Powell, in a speech at Spelman College, stated that it is premature to consider monetary policy restrictive enough, and the bank is prepared to raise rates again if necessary to address inflation. The recent ISM Manufacturing PMI reported by the Institute for Supply Management for November was 46.7, matching the previous figure but falling short of the expected 47.6. Looking ahead, the release of November’s Nonfarm Payrolls report on Friday is anticipated to show an increase in job creation, although wages are expected to decelerate.

US bond yields are on a downward trajectory, with the 2-year, 5-year, and 10-year yields standing at 4.57%, 4.16%, and 4.25%, respectively. This trend appears to be limiting the upside for the USD. According to the CME FedWatch Tool, market expectations for the December meeting suggest that investors do not anticipate a rate hike. Furthermore, swap markets are pricing in rate cuts midway through 2024.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

In the previous week, the Swiss Q3 GDP was reported at 0.30%, falling short of the anticipated 0.50%. Despite this, the Swiss Franc appreciated against its counterparts.

The Swiss Franc exhibited weakness on Friday following the release of mixed GDP data for the third quarter. On a year-on-year (YoY) basis, the Swiss economy grew by 0.3% in Q3, falling short of the anticipated 0.5%, as reported by the State Secretariat of Economic Affairs. However, the quarter-on-quarter (QoQ) GDP exceeded expectations, providing some balance to the disappointing YoY result. Despite fierce sell-offs, most major pairs involving the Swiss Franc found support on Friday.

The marginal weakening of the Swiss Franc was a response to the lower-than-expected Swiss GDP growth in Q3 on a YoY basis, registering 0.3% compared to the forecasted 0.5%. In contrast, the QoQ figure revealed an unexpected 0.3% gain, surpassing the anticipated 0.1% and reversing the previous 0.1% decline. The US Dollar rebounded, recovering from earlier losses driven by lower-than-expected PCE inflation data and unexpected dovish remarks from Federal Reserve Board Member Christopher J. Waller.

As global data shows signs of decline and inflation cools in major economies worldwide, investors are now concerned about the potential for interest rates to decrease globally, not just in the US. Market attention is focused on comments from Federal Reserve Chair Jerome Powell on Friday for additional guidance before the blackout period preceding the next Fed meeting begins.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower low area of the channel

According to analysts at Commerzbank, German electricity prices have moderated, although they remain comparatively elevated on the global scale. The upcoming integration of green energy is expected to offset electricity consumption in Germany. Despite the recent decline in electricity prices, it has not provided substantial support to the German economy.

Analysts at Commerzbank are examining the extended forecast for German power prices. Despite the recent dip in electricity rates, they persist at elevated levels when compared to both historical and global benchmarks. The substantial expenses associated with the energy transition pose a potential threat, indicating the possibility of further price increases in the years ahead. However, post-transition, the significantly lower expenses related to producing green electricity offer optimism for cost reductions, although this advantage may be partially offset by higher system costs, such as those for reserve capacities. Consequently, while electricity prices are expected to experience a decline, they are likely to remain a competitive disadvantage for the German economy.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The European Central Bank might have the opportunity to implement rate cuts next year, potentially reducing rates by at least 125 basis points. Inflation in the Euro area has considerably eased, aligning with expectations.

Sluggish growth and declining inflation are paving the way for multiple interest rate cuts by the ECB next year, with the market already factoring in a total reduction of over 125 basis points. Among major central banks, the ECB might be the first to implement rate cuts, as current market expectations anticipate a 25 basis points reduction at the meeting on April 11th. The recent catalyst for this trend was the Euro Area inflation report, revealing a significant and sudden decrease in price pressures across the region.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Last week, the British Pound strengthened against the USD, and the rate hikes implemented by the Bank of England contributed to a stabilization of inflation in the market. Anticipations suggest that rate cuts from the Bank of England can be expected in the second half of 2024.

The British Pound has demonstrated consistent strength against the United States Dollar since late September, primarily attributed to Dollar weakness rather than a robust vote of confidence in Sterling. The upcoming week lacks significant scheduled data from the United Kingdom, and while there’s limited data from the US, it is likely to steer GBPUSD trading. Currently, the crucial interest-rate differentials favor Sterling bulls. Although the Bank of England’s decision to raise rates remains uncertain, it appears less likely to cut them than the Federal Reserve. Forex markets anticipate a potential decline in US borrowing costs in the first half of the next year, with the possibility of a substantial decrease once initiated. In contrast, Bank of England Governor Andrew Bailey has cautioned that the UK’s battle against inflation might keep rates elevated well into 2024, contributing to the Pound’s recent gains. The UK’s domestic economy has also outperformed initial forecasts, partly due to the initial gloominess of those predictions.

However, there might be an element of wishful thinking in the market sentiment. Recent Federal Reserve commentary suggests a cautious approach in Washington, with no overt indications of an imminent rate reduction. New York branch President John Williams, in a conference on November 30, emphasized the need for restrictive monetary policy for a considerable duration, signaling a lack of urgency in lowering rates.

The key question for the upcoming week revolves around whether any significant developments are expected to alter the market’s current perspectives. While it seems unlikely, events later in the month, including policy decisions from various central banks such as the Fed and BoE, could bring changes. The release of US payrolls figures for November on December 8, projecting 175,000 new non-farm jobs and a stable 3.9% unemployment rate, is anticipated to offer the most significant short-term trading opportunity. A stronger-than-expected number could provide the Dollar with support, potentially causing a reassessment of rate-cut expectations.

GBPJPY Analysis:

GBPJPY is moving in the Descending channel and the market has reached the lower high area of the channel

The Bank of Japan anticipates wage hikes in tandem with the inflation rate in the economy. Currently, cost-push inflation in the market is influenced by the increased import prices in the domestic market.

Bank of Japan monetary policy board member Seiji Adachi, who emphatically stated that Japan’s economy has not yet reached a stage where a departure from the current policy setting is under consideration. The Bank of Japan has not provided any significant indications that a change is imminent. I have consistently emphasized that a shift will occur, given that Governor Ueda was appointed for this purpose.

Adachi’s comments, however, correctly highlight one of the crucial factors the BoJ is monitoring the prospect of wage growth surpassing inflation. Given the current tight labor market conditions in Japan, this scenario could materialize in the coming months, assuming conditions remain unchanged. I strongly believe this will be the juncture at which the BoJ revises its stance on monetary policy, making it the most pivotal data point to watch in the future.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Canadian employment data revealed an increase of 25,000 jobs, surpassing the expected 15,000 and showing significant growth from the 17,500 reading in October. The unemployment rate in Canada remained steady at 5.8%, aligning with expectations. Following the release of this data last week, the Canadian Dollar strengthened.

In Friday’s trading, the Canadian Dollar is testing higher levels once again against its major counterpart, the US Dollar, buoyed by robust Canadian employment figures that surpassed market expectations. The Canadian Dollar stands out as one of the top-performing currencies for the week, having appreciated by a full percentage point against the US Dollar since Monday’s opening bids.

In November, Canada exceeded predictions by adding nearly 25,000 jobs, significantly outperforming the forecast of 15,000 and surpassing October’s new job additions of 17,500. Although the Canadian Unemployment Rate inched slightly higher to 5.8%, aligning with investor expectations, the Average Hourly Wages for the year remained stable at 5%, alleviating concerns about inflation driven by demand, as Canadian wage growth is capped below 6%.

Despite the positive job data, Canadian hiring remains below the peak observed in February 2023 when 150,000 jobs were added. The Canadian Dollar’s strength is tempered by a modest decline in the Canadian S&P Global Manufacturing Purchasing Managers Index (PMI), slipping from 48.6 to 47.7. While the Unemployment Rate in Canada increased marginally from 5.7% to 5.8%, this was broadly anticipated by the markets. Investors are overlooking Thursday’s downturn in Gross Domestic Product as attention shifts to the substantial upward revision of 2Q’s GDP growth from -0.2% to 1.4%.

In the energy markets, Crude Oil is experiencing volatility as investor sentiment grapples with concerns about declining global demand and the ongoing OPEC Crude Oil production cuts expected to persist through Q1 2024.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

Before the upcoming RBA meeting this week, the Australian Dollar experienced an uptick against the USD. However, the resurgence of COVID-19 cases in China last week has introduced volatility, impacting the Australian Dollar against the USD.

Amid a heightened escalation of tensions in the Middle East and concerns regarding a potential resurgence of a respiratory illness in China akin to COVID-19, investors are adopting a cautious stance, thereby restraining the recent upswing in global equity markets. This cautious sentiment is contributing to a bolstering of the safe-haven US Dollar while simultaneously undermining the risk-sensitive Australian Dollar. Additionally, anticipatory repositioning trades ahead of the Reserve Bank of Australia’s policy meeting on Tuesday are exerting downward pressure on the AUDUSD pair.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

In Q3, the New Zealand trade index recorded a decrease of -0.60%, contrasting with the 0.30% decline in the previous quarter. Export prices witnessed a notable drop from 6.8% to 1.5%, while import prices declined to 0.80% QoQ compared to a 1.0% decrease in the preceding reading. The recent hawkish comments from the Reserve Bank of New Zealand during the last meeting have contributed to the strengthening of the New Zealand Dollar against the USD.

The third quarter Terms of Trade Index for New Zealand dropped 0.6% QoQ on Monday morning after rising by 0.3% the previous week. Goods import prices decreased 0.8% QoQ from a 1.0 decline in the previous reading, while good export prices fell 1.5% QoQ from the previous reading of a 6.8% increase. The Reserve Bank of New Zealand kept the cash rate at 5.5% last week, but they also pointed out that inflation was still too high and that if price pressures did not subside, more policy tightening might be required. Nevertheless, the RBNZ’s hawkish stance strengthens the New Zealand Dollar and provides support for the NZDUSD pair.

However, this stands in stark contrast to the Fed’s dovish tone, as the market now prices in the US central bank ending the cycle of tightening and starting rate cuts as early as March of next year. Fed Chair Jerome Powell said on Friday that it was too soon to rule out further rate increases or to begin talking about reductions. Aside from this, the Institute for Supply Management revealed on Friday that the US ISM Manufacturing PMI for November was lower than anticipated and stayed at 46.7. The US Factory Orders for October will be watched by market participants. Tuesday’s US ISM Services PMI and New Zealand’s ANZ Commodity Price are due later this week. On Friday, focus will turn to US nonfarm payrolls, which are predicted to increase by 180K jobs in November.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/