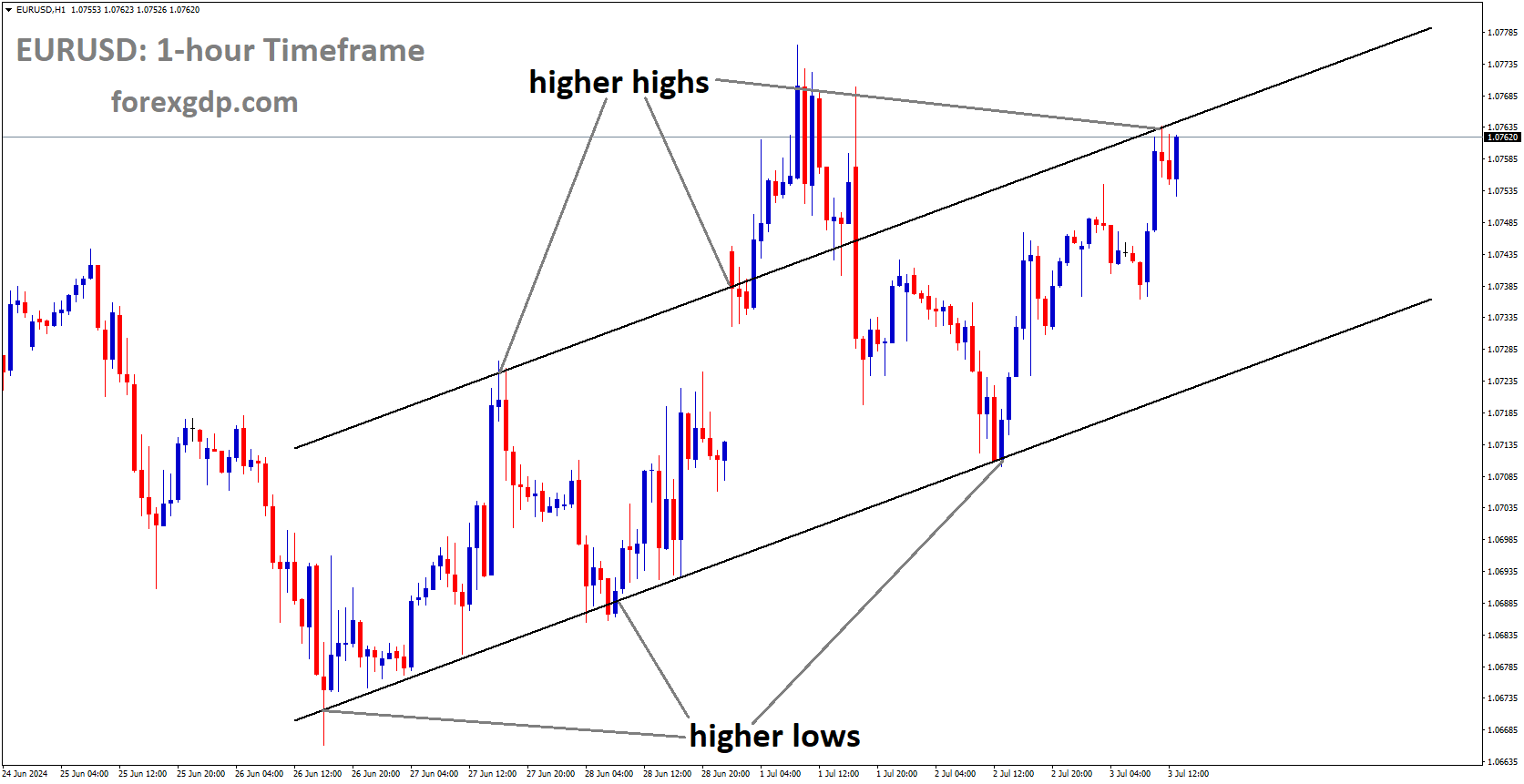

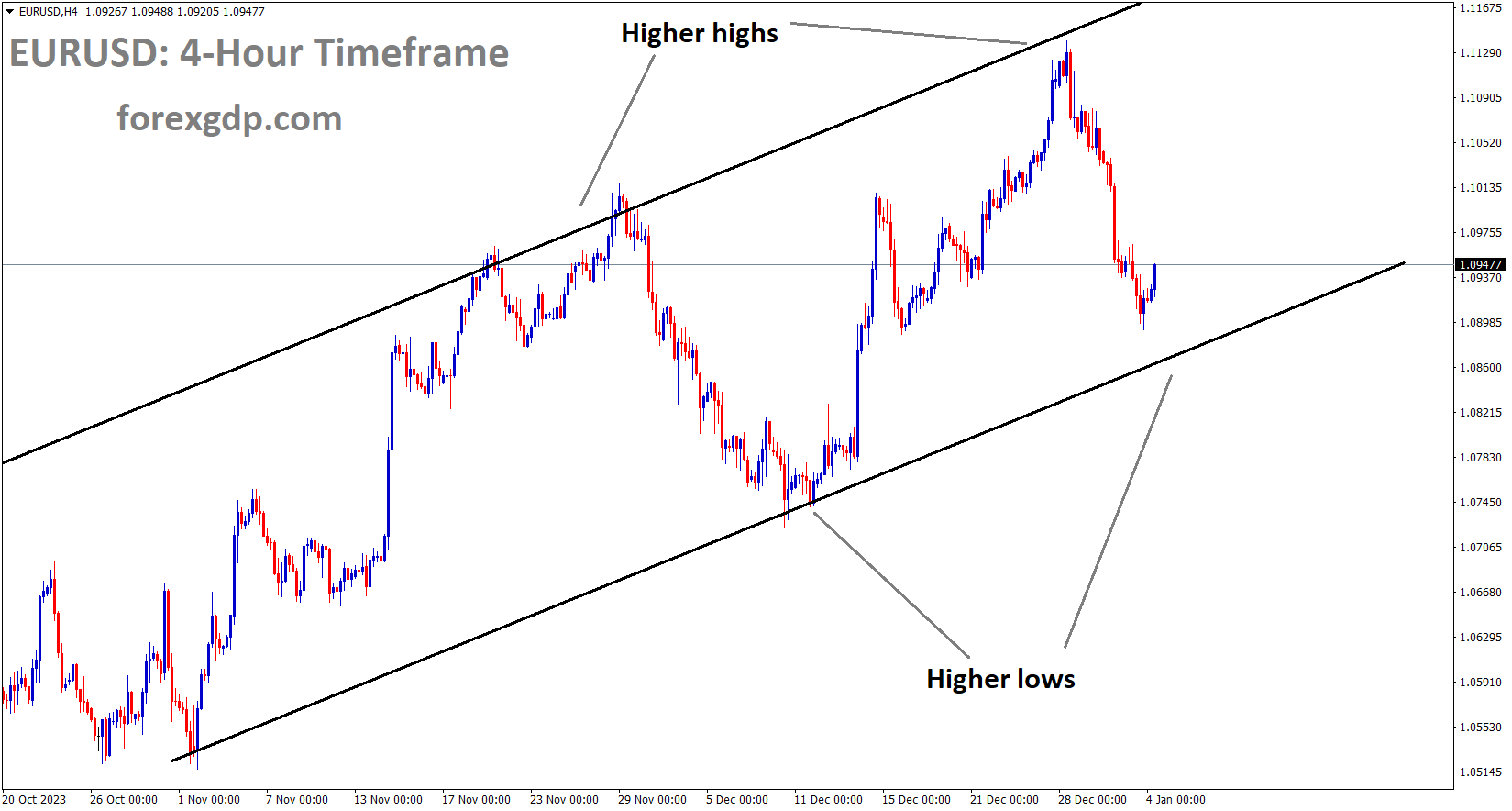

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

In December, Germany reported an unemployment rate of 5.9%, and there was a modest increase of 5,000 in unemployment, which was lower than the expected 20,000. Today, the Eurozone Consumer Price Index (CPI) is on the schedule, with an anticipated reading of 3.0%, up from the previous month’s 2.4%.

The German Unemployment Rate held steady at 5.9%, in line with expectations. The Unemployment Change data revealed an increase of 5,000 unemployed individuals, which was below the market consensus of 20,000 and the previous figure of 21,000.

Investors are now looking ahead to the Eurozone inflation report scheduled for Friday, hoping for fresh market momentum. The Annualized Harmonized Index of Consumer Prices for December is expected to bounce back to 3.0% from the previous reading of 2.4%.

On the other side of the Atlantic, the Federal Open Market Committee (FOMC) decided to maintain its benchmark rate within a range of 5.25% to 5.5% at its December 2023 meeting. FOMC members anticipate three quarter-point rate cuts by the end of 2024. However, the minutes from the meeting highlighted that the actual path of policy will depend on how the economy evolves, despite participants’ belief that the policy rate is likely at or near its peak in this tightening cycle.

In a somewhat hawkish tone, Richmond Fed President Thomas Barkin commented on Wednesday that interest rate hikes should not be ruled out despite progress in controlling inflation. These remarks bolstered the US Dollar across the board while putting pressure on the Euro.

Market participants will closely monitor the release of December’s HCOB Composite PMI and Services PMI data from France, Germany, and the Eurozone. Additionally, the German Consumer Price Index is due on Thursday. In the United States, attention will focus on the US ADP Employment Change report and the weekly Initial Jobless Claims.

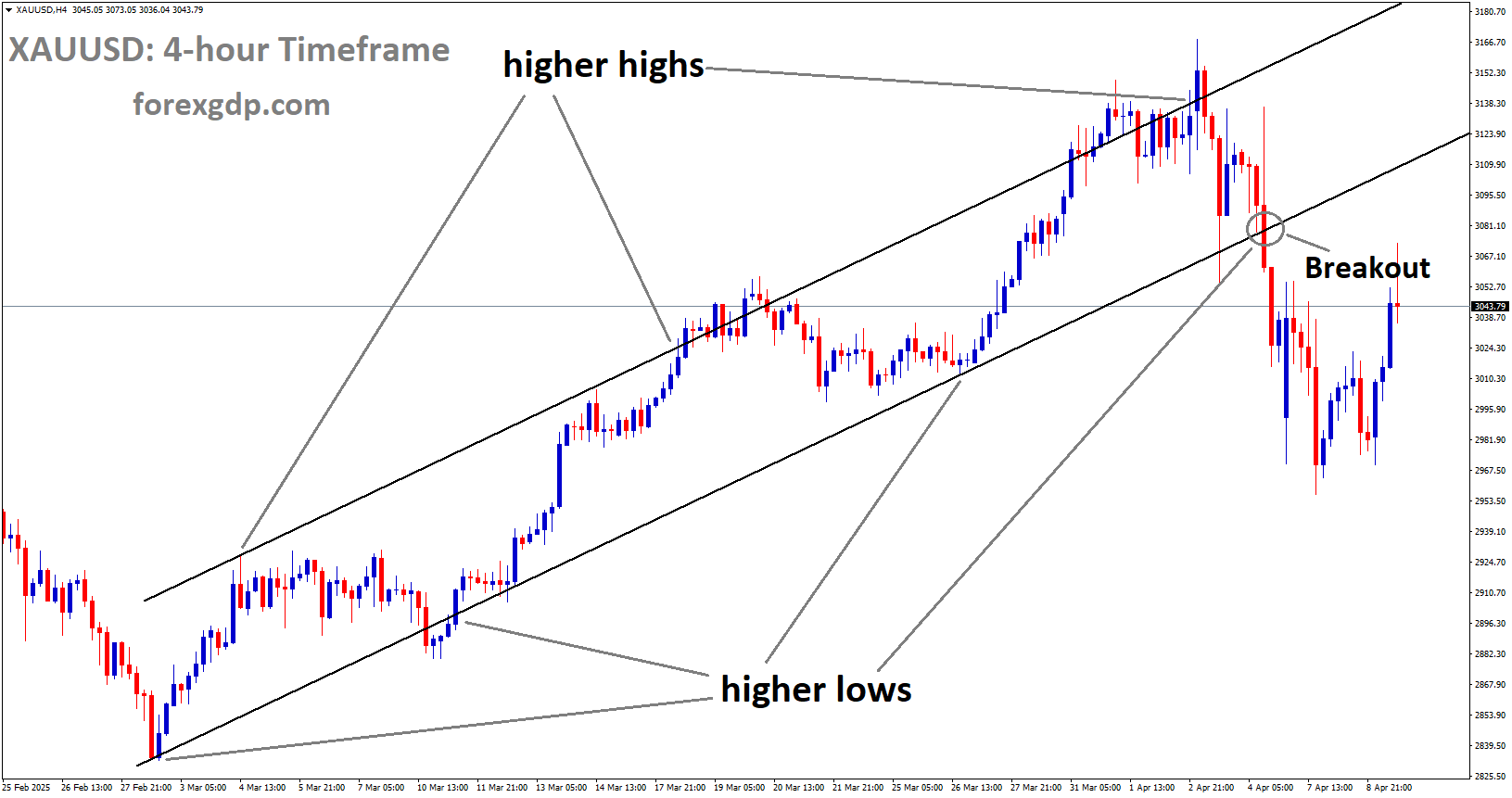

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Gold prices, which had risen significantly in the past week, are now stabilizing following the release of positive US Federal Reserve meeting minutes that have bolstered the US Dollar. The future trajectory of Gold will be heavily influenced by the upcoming US jobs data.

The price of gold experienced a decline, primarily due to the increasing Treasury rates and the strength of the U.S. dollar. To provide context, bond yields have surged significantly in recent trading sessions, with the 10-year Treasury note approaching the psychologically significant 4.0% level after trading below 3.80% just last month. Considering the day’s developments, the value of gold has retreated by more than 2.7% from its late December peak. Investors are becoming more cautious, speculating that the overbought conditions and exuberant sentiment following the Federal Reserve’s policy shift could potentially lead to a reversal in early 2024.

Although gold maintains a positive outlook, its upward trajectory is not expected to be a straightforward ascent, allowing for minor corrections within the broader upward trend. Regardless, we will gain more insight into its future direction later this week when the Bureau of Labor Statistics releases the latest employment report. Traders should closely monitor the nonfarm payrolls survey for indications of the labor market’s health. In this regard, if hiring continues to be strong, it may lead to increased expectations of higher interest rates, reinforcing the rise in yields and the strength of the U.S. dollar. This would be a bearish scenario for gold. Conversely, if job growth falls significantly short of market expectations, it would validate predictions of monetary easing in 2024. This outcome would exert downward pressure on yields and the U.S. currency, creating favorable conditions for gold to resume its upward trend.

SILVER Analysis:

XAGUSD Silver price is moving in the Up-trend line and the market has reached the higher low area of the channel

The outcome of the Federal Reserve’s minutes had a positive impact on the US Dollar in the market. Federal Reserve Chairman Jerome Powell stated that short-term interest rates would remain unchanged in the near term, with potential rate cuts depending on incoming economic data. Powell’s hawkish tone during his speech bolstered the US Dollar’s strength against other currencies in yesterday’s trading session.

U.S. dollar, as gauged by the DXY index, continued its recovery but retreated significantly from its peak during the day due to a pullback in yields following the release of the Fed minutes. To provide context, the summary of the latest Federal Open Market Committee meeting indicated that interest rates might remain elevated for an extended period. However, it also highlighted that policymakers were observing inflation risks becoming more balanced, which is typically the initial phase before considering a reduction in rates. Given the uncertain state of the Fed’s policy direction, it is crucial to closely monitor macroeconomic data, as this will be the primary factor guiding the U.S. central bank’s future decisions and the timing of potential interest rate cuts. In this regard, the next significant report to watch for is the December nonfarm payrolls survey, scheduled for release on Friday morning.

According to consensus estimates, it is anticipated that U.S. employers added 150,000 jobs in the previous month, following the hiring of 199,000 individuals in November. The unemployment rate is expected to inch up from 3.7% to 3.8%, indicating a healthier equilibrium between labor supply and demand. This situation should help alleviate potential future wage pressures. For the U.S. dollar to sustain its recovery in the upcoming weeks, labor market data must demonstrate continued robust and dynamic hiring. This scenario would drive yields upward, signaling that the economy remains resilient and can progress without immediate central bank intervention. In this context, any nonfarm payrolls figure exceeding 200,000 would be considered positive for the U.S. dollar. Conversely, if job growth falls short of expectations by a significant margin, it could lead to the opposite outcome: a weaker U.S. dollar. Such a result would support the notion of substantial rate cuts, confirming a slowdown in economic growth and the need for timely intervention by the Fed to prevent a severe economic downturn.

USDJPY Analysis:

USDJPY has broken the Descending channel in upside

Factory production in Japan has experienced a continuous decline for ten consecutive months, with even earthquakes further dampening the country’s industrial activity. As a result, the Japanese Yen depreciated against other currencies.

Earlier today, data revealed that manufacturing activity in Japan contracted at its most severe rate in 10 months in December. This contraction follows a devastating 7.6 magnitude earthquake on New Year’s Day and is a significant factor weighing on the JPY. Simultaneously, doubts surrounding early interest rate cuts by the Federal Reserve are bolstering US Treasury bond yields, which, in turn, are providing support for the Greenback and the USDJPY pair.

Despite this, USD bulls appear hesitant to make aggressive bets. Concerns are mounting that the US central bank may initiate interest rate cuts as early as March, particularly in anticipation of the crucial US monthly employment data set to be released on Friday, known as the Nonfarm Payrolls report. This report will heavily influence the Fed’s future policy decisions and drive demand for the USD in the short term, potentially offering momentum to the USDJPY pair. In the interim, traders on Thursday may seek guidance from the US economic calendar, which includes the release of the ADP report on private-sector employment and the customary Initial Jobless Claims data.

Furthermore, as expectations solidify regarding an impending shift in the Bank of Japan’s stance, coupled with a subdued risk appetite, the safe-haven JPY’s losses should be contained. This could, in turn, prevent any significant appreciation of the USDJPY pair and warrant caution for bullish traders.

The Japanese Yen has relinquished its modest gains from the Asian session due to weaker domestic data. However, various factors are poised to limit more substantial losses. The au Jibun Bank Japan Manufacturing PMI has remained in contraction territory for seven consecutive months, plummeting to 47.9 in December, its lowest reading since February. The expectation of policy divergence between the Bank of Japan and the Federal Reserve in 2024 is likely to continue supporting the JPY.

The minutes from the December 12-13 FOMC meeting indicated a consensus that inflation is under control and expressed concerns about the potential risks of overly restrictive policies on the economy. Nonetheless, these minutes did not offer direct hints about the timing of rate cuts, which is boosting US bond yields and the US Dollar.

In related news, the Institute for Supply Management reported that the pace of decline in the US manufacturing sector has slowed, marked by a modest increase in production and an improvement in factory employment. The US ISM Manufacturing PMI rose to 47.4 last month, breaking the trend of remaining unchanged at 46.7 for two consecutive months, although it still indicates contraction for the 14th straight month. Separately, the Labor Department’s Job Openings and Labor Turnover Survey indicated that employment listings dropped to 8.79 million in November, the lowest figure since March 2021.

Investors are now turning their attention to the US ADP report, expected to show that private sector employers added 115K jobs in December compared to 103K in the previous month. Nevertheless, the primary focus will remain on Friday’s official monthly employment data release, the Nonfarm Payrolls report.

And On Thursday, Bank of Japan Governor Kazuo Ueda expressed his hope for Japan’s economy to achieve a harmonious equilibrium between wage increases and inflation. The aspiration is that a well-balanced rise in both wages and inflation will encourage companies to invest in equipment and research and development.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

The Swiss SVME Manufacturing Purchasing Managers’ Index increased to 43 from its previous reading of 42.1. This positive outcome provided a boost to the Swiss Franc.

Despite the US Dollar showing signs of improvement, the USDCHF pair is facing downward pressure, possibly due to interventions by the Swiss National Bank in the foreign exchange market. Furthermore, the release of the SVME Manufacturing Purchasing Managers Index for December on Wednesday showed an improved figure of 43, up from 42.1 previously. This improvement in business conditions within the manufacturing sector may have influenced buyers of the Swiss Franc.

On the other hand, concerns about sluggish global economic growth at the end of 2024 have prompted a risk-off sentiment among investors, leading them to seek safety in the US Dollar. Additionally, the strengthening of US bond yields has contributed to the USD’s strength, with the US Dollar Index hovering around 102.40 after recent gains. By the current press time, 2-year and 10-year yields on US Treasury bonds stand at 4.33% and 3.93%, respectively.

The positive momentum of the USD is further supported by the favorable ISM Manufacturing PMI report released on Wednesday, which showed an increase to 47.4 in December, surpassing the market consensus of 47.1 and up from the previous reading of 46.7. However, there is a contrasting trend as JOLTS Job Openings declined to 8.79 million, falling short of the expected figure of 8.85 million for November.

Looking ahead, market attention will focus on Thursday’s labor market data releases, including ADP Employment Change and Initial Jobless Claims, which will provide additional insights into the current economic landscape.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

UK business leaders have grown increasingly pessimistic about the state of the UK economy due to the prospect of higher interest rate hikes, decreased consumer spending, and elevated house prices. Analysts expect that the Bank of England may reduce interest rates by 140 basis points in 2024 in response to these concerns.

The British Pound is facing pressure due to increased pessimism among UK business leaders regarding the economic outlook. They are urging the Bank of England to initiate rate cuts early in the year. Money market indicators suggest that traders are anticipating approximately 140 basis points of rate cuts in 2024.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The GBPUSD pair is encountering headwinds from a modest show of strength in the US Dollar. The minutes from the December 12-13 FOMC meeting, released on Wednesday, did not provide any clear indications of when the Federal Reserve might commence a series of rate cuts. This uncertainty has led to an increase in US Treasury bond yields, offering some support to the US Dollar. Additionally, a generally subdued sentiment in equity markets has boosted demand for the safe-haven Greenback, thereby restraining the GBPUSD pair.

Market expectations currently include a higher likelihood of a 25-basis point Fed rate cut in March, which could limit the recent rally in US Treasury bond yields that has lasted for a week. This scenario might discourage aggressive bullish positions on the US Dollar and help minimize downward pressure on the GBPUSD pair.

Investors appear hesitant and are opting to stay on the sidelines ahead of the release of the US monthly jobs report on Friday. In the meantime, Thursday’s economic calendar will include the final Services PMIs from both the UK and the US, along with the US ADP report on private-sector employment. These releases will be closely watched for potential short-term trading opportunities.

UK business leaders have grown increasingly pessimistic about the state of the UK economy due to the prospect of higher interest rate hikes, decreased consumer spending, and elevated house prices. Analysts expect that the Bank of England may reduce interest rates by 140 basis points in 2024 in response to these concerns.

The British Pound is facing pressure due to increased pessimism among UK business leaders regarding the economic outlook. They are urging the Bank of England to initiate rate cuts early in the year. Money market indicators suggest that traders are anticipating approximately 140 basis points of rate cuts in 2024.

Furthermore, the GBPUSD pair is encountering headwinds from a modest show of strength in the US Dollar. The minutes from the December 12-13 FOMC meeting, released on Wednesday, did not provide any clear indications of when the Federal Reserve might commence a series of rate cuts. This uncertainty has led to an increase in US Treasury bond yields, offering some support to the US Dollar. Additionally, a generally subdued sentiment in equity markets has boosted demand for the safe-haven Greenback, thereby restraining the GBPUSD pair.

Market expectations currently include a higher likelihood of a 25-basis point Fed rate cut in March, which could limit the recent rally in US Treasury bond yields that has lasted for a week. This scenario might discourage aggressive bullish positions on the US Dollar and help minimize downward pressure on the GBPUSD pair.

Investors appear hesitant and are opting to stay on the sidelines ahead of the release of the US monthly jobs report on Friday. In the meantime, Thursday’s economic calendar will include the final Services PMIs from both the UK and the US, along with the US ADP report on private-sector employment. These releases will be closely watched for potential short-term trading opportunities.

EURCAD Analysis:

EURCAD is moving in the Box pattern and the market has reached the support area of the pattern

Oil prices surged to $73 per barrel following attacks by Houthi rebels on container ships in the Southern Red Sea and disruptions in Libya’s oil fields. This conflict provided support for the Canadian Dollar.

The West Texas Intermediate crude oil price is currently trading higher, hovering around $73.10 per barrel. The increase in crude oil prices is driven by several factors, including heightened tensions in the Israel-Gaza conflict and disruptions at a crucial oilfield in Libya.

In the Middle East, the Iran-backed Houthis targeted a container ship in the southern Red Sea en route to Israel, raising concerns about maritime security in the Red Sea region. These geopolitical concerns are contributing to the upward pressure on crude oil prices.

Additionally, in Libya, disruptions at a key oilfield are further boosting crude oil prices. This combination of factors is influencing the current rise in oil prices.

Looking ahead, Canada is set to release labor market data for December on Friday, including the Unemployment Rate and Net Change in Employment figures.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Australian Dollar experienced a decline as a result of the Judo Bank Services sector falling to 47.1, which was below the expected reading of 47.6. Additionally, the Composite PMI dropped from 47.4 to 46.9.

The Aussie Dollar faced additional pressure as the Judo Bank Purchasing Managers Index data indicated weakness. On a positive note, improved Chinese services data could help limit the losses of the AUD. The Caixin Services PMI for December rose to 52.9, surpassing expectations of 51.6 and the previous 51.5.

Contrastingly, Australia’s Services sector experienced a contraction in December, according to the latest Judo Bank Services PMI, which reported a reading of 47.1. This fell short of market expectations that it would remain at 47.6. Additionally, the Composite PMI decreased to 46.9 from the previous figure of 47.4, marking the sharpest pace of Services contraction since Q3 2021. Economist Matthew De Pasquale of Judo Bank suggests that recent readings over the past two months indicate a slowdown in the Australian economy, but one that is not accelerating. Despite households grappling with challenges posed by elevated interest rates, both the output and new order indexes remain at levels consistent with the Reserve Bank of Australia’s anticipated soft landing scenario.

Meanwhile, the US Dollar Index maintains a positive trajectory, bolstered by improved United States Treasury yields. This momentum may receive additional support from the enhanced ISM Manufacturing PMI report, which reported an increase to 47.4 in December, surpassing the market consensus of 47.1. However, JOLTS Job Openings contracted to 8.79 million in November, falling short of the expected 8.85 million figure. Traders are eagerly awaiting US labor market data releases, including ADP Employment Change and Initial Jobless Claims. The December minutes from the Federal Open Market Committee indicate that the policy rate has likely reached or is close to its peak in the current tightening cycle. However, the trajectory of policy will continue to depend on evolving economic conditions.

In Australia, the Judo Bank Manufacturing PMI revealed a modest contraction in manufacturing activity, declining to 47.6 in December from the previous reading of 47.8. RBA’s internal documents show a decline in domestic tourism demand, with consumers opting for more affordable products or reducing overall purchases due to cost-of-living pressures. Nevertheless, the documents suggest that private sector wage growth has stabilized at around 4.0%. Australian Prime Minister Anthony Albanese has directed Treasury and Finance to explore measures to ease the financial burden on families in terms of the cost of living without exacerbating inflation pressures.

Geopolitically, China characterizing the January 13 presidential and parliamentary elections as a choice between war and peace has heightened tensions in the region. A senior Chinese official has urged Taiwan’s people to make a “correct choice,” implying potential consequences based on election outcomes. In economic news, China’s NBS Manufacturing PMI for December decreased to 49.0 from the previous 49.4 figure, falling short of the expected increase to 49.5. Meanwhile, NBS Non-Manufacturing PMI improved to 50.4 from the 50.2 prior but missed the expected 50.5. In the US, the ISM Manufacturing Employment Index improved to 48.1 in December from 45.8 in November. However, the US S&P Global Manufacturing PMI posted a lower-than-expected figure of 47.9, deviating from the anticipated 48.2.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

China’s Caixin Services PMI data for December showed an increase to 52.9, up from the November reading of 51.5. As a result, the New Zealand Dollar received a boost following the release of this data.

The decline in the pair is being reinforced by the robust performance of the US Dollar. With no economic data being released from the New Zealand side, the NZDUSD pair remains subject to the fluctuations in the USD’s value. New Zealand’s economic calendar is relatively quiet for the week.

On Thursday, there was a noteworthy development as China’s Caixin Services Purchasing Managers’ Index surged to 52.9 in December, up from November’s 51.5, surpassing market expectations of 51.6. Despite expectations among market participants that the policy rate may have reached or is close to its peak in the current tightening cycle, the FOMC minutes emphasized that monetary policy direction hinges on the performance of the economy. In light of these less dovish remarks, the US Dollar gained strength, creating a headwind for the NZDUSD pair.

Later on Thursday, attention will shift to the release of the US ADP Employment Change and the weekly Initial Jobless Claims data. Traders will closely monitor these figures for insights and potential trading opportunities involving the NZDUSD pair. Additionally, the highly anticipated US Nonfarm Payrolls report, along with the Unemployment Rate and Average Hourly Earnings, is scheduled for release on Friday, further shaping market sentiment and trading dynamics for the pair.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/