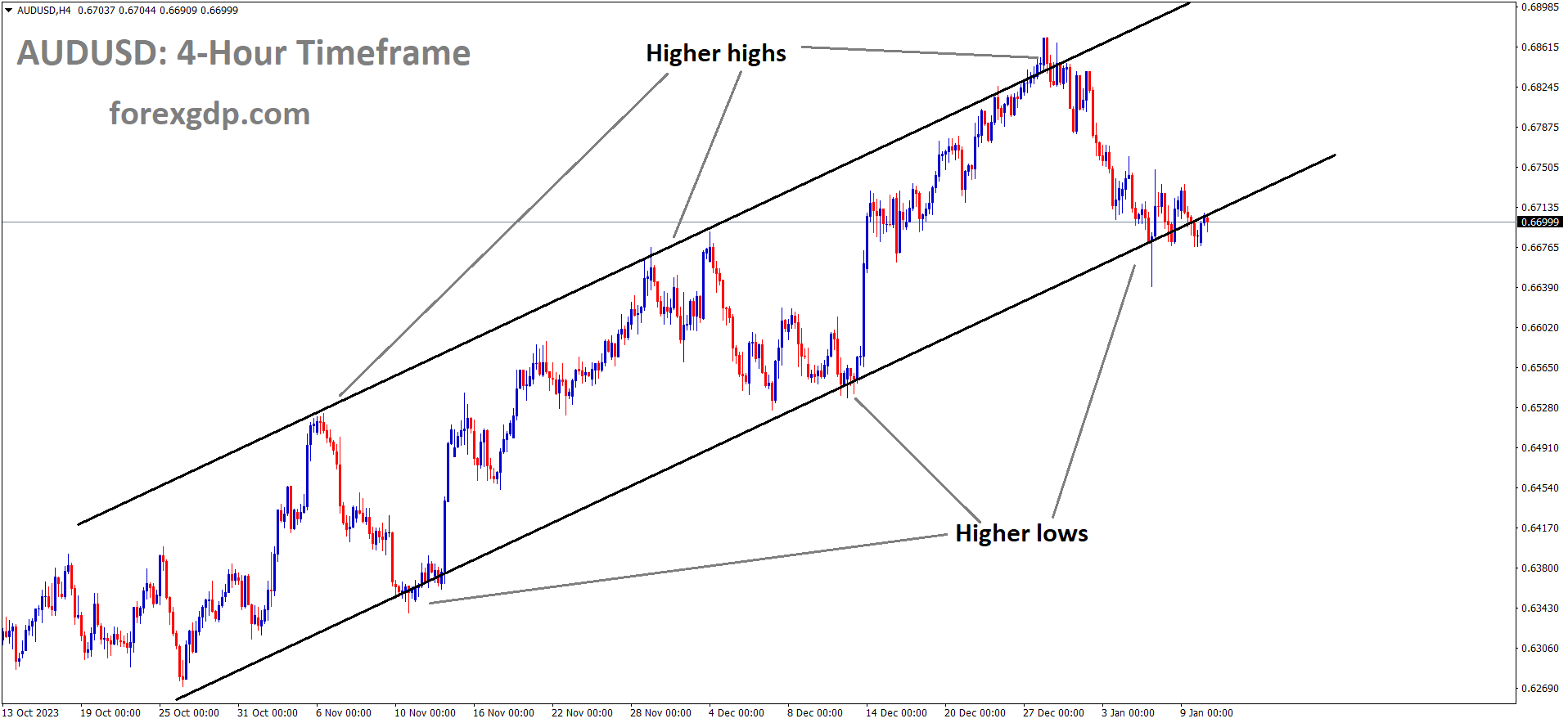

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

In November, Australian CPI data registered at 4.3%, slightly below the expected 4.4% and a decrease from the 4.9% recorded in October. However, there were positive developments in retail sales and building permit data. Additionally, the trade balance for December is anticipated to expand by 7500 million AUD.

Australia’s economic data is sending mixed signals, as the November Monthly Consumer Price Index shows a slight decrease to 4.3%, slightly below the market’s expectation of 4.4% and down from the previous 4.9%. This suggests a modest easing of year-on-year inflationary pressures. On a more positive note, Australian Retail Sales saw an increase on Tuesday, indicating higher consumer spending. Additionally, the monthly Building Permits data showed growth, defying expectations of a decline. These favorable trends in retail sales and building permits suggest some resilience in the domestic economy. The release of Australian Trade Balance data for December on Thursday is expected to show an increase from 7,129 million to 7,500 million, potentially indicating improved export performance and contributing positively to the overall economic outlook.

The US Dollar Index is currently moving sideways after experiencing gains, despite weaker US Treasury yields on Tuesday. However, the risk-on sentiment sparked by remarks from Federal Reserve members speculating about interest rate cuts by the end of 2024 may have limited the US Dollar’s profits. Traders are eagerly awaiting the release of December’s Consumer Price Index (CPI) data from the United States on Thursday. This economic indicator is crucial for assessing inflationary pressures and can significantly influence market expectations regarding the Fed’s monetary policy stance.

Australia’s Bureau of Statistics reported seasonally adjusted Retail Sales for November, which increased by 2.0%, surpassing the expected 1.2% and reversing the previous 0.2% decline. Building Permits in Australia also grew by 1.6%, instead of the anticipated 2.0% decline, contrasting with the previous 7.5% figure.

In other news, Chinese wealth manager Zhongzhi Enterprise Group has filed for bankruptcy liquidation, facing a substantial $64 billion in liabilities. Atlanta Fed President Raphael W. Bostic mentioned on Monday that inflation has declined more than initially anticipated and expressed the expectation of two quarter-point cuts by the end of 2024. Bostic expressed comfort with the current rate level and emphasized the importance of allowing the Fed’s tight policy time to address inflation.

US Fed Governor Michelle W. Bowman suggested that inflation could decrease further with the policy rate held steady for some time. Bowman stated that the current policy stance appears sufficiently restrictive, but it may become appropriate to lower the Fed’s policy rate if inflation approaches the 2% target.

In terms of US economic data, Nonfarm Payrolls rose to 216K in December, an improvement from the 173K reported in November and exceeding the market’s expectation of a 170K rise. US Average Hourly Earnings (YoY) also improved to 4.1% from the previous 4.0%. The monthly index remained unchanged at 0.4%, defying the expected 0.3% decline. However, the US ISM Services Purchasing Managers Index (PMI) came in at 50.6, below the expected 52.6 and the previous 52.7, with the Services Employment Index dropping to 43.3 from the previous reading of 50.7.

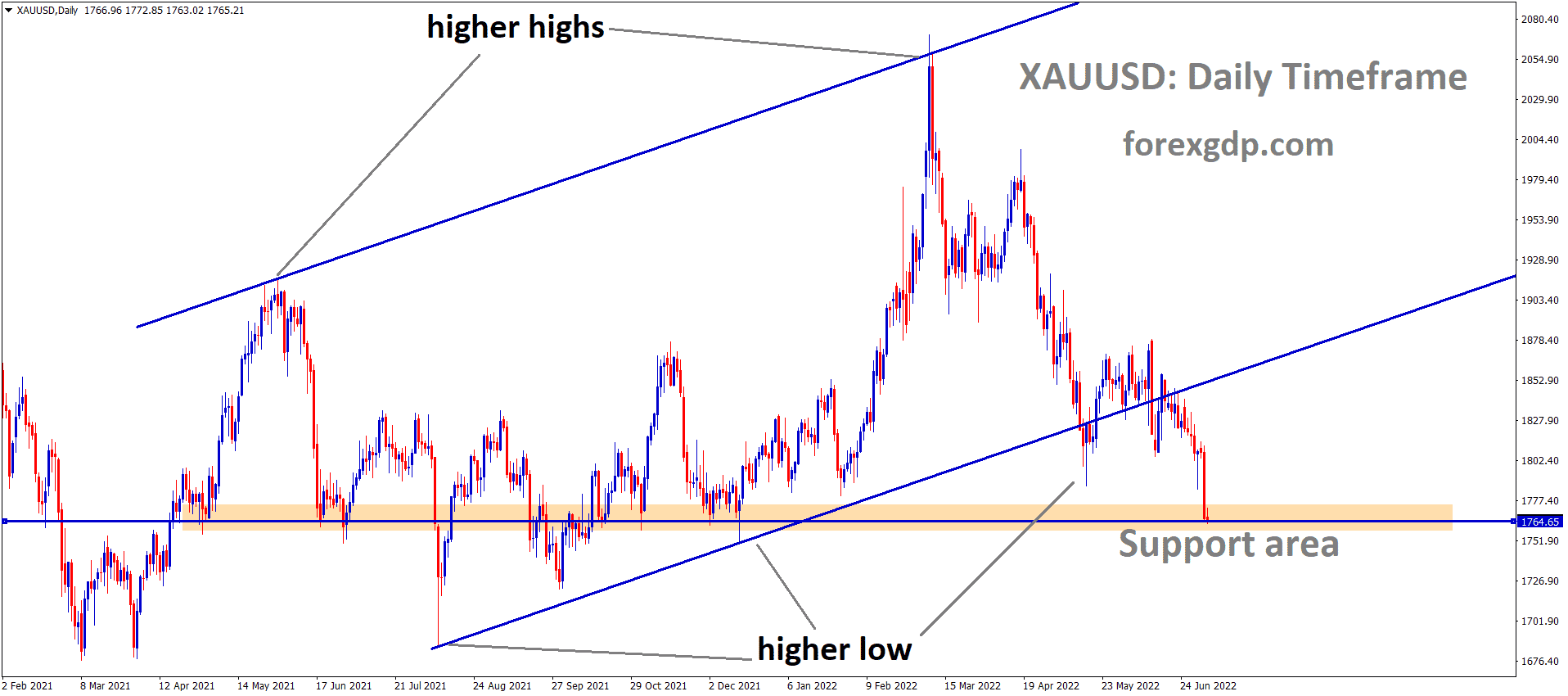

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending triangle pattern and the market has reached the higher low area of the pattern

Gold markets experienced a decline as anticipation of a December increase in the US Consumer Price Index strengthened the US Dollar, aided by ongoing geopolitical tensions.

The precious metal continues its decline as we enter the European session on Wednesday, sliding even further towards a nearly three-week low observed on Monday. The decreasing likelihood of a more aggressive policy easing by the Federal Reserve (Fed) in 2024 is bolstering US Treasury bond yields. Consequently, this provides support to the US Dollar and diverts investment away from the non-yielding gold.

Nevertheless, geopolitical tensions arising from the Israel conflict and persistent concerns regarding a sluggish economic recovery in China, the world’s second-largest economy, should offer some backing to the safe-haven gold price. Traders may exercise caution, refraining from making substantial directional bets and opting to await the release of the latest Consumer Price Index (CPI) data from the United States on Thursday. The pivotal US CPI report will shape expectations regarding the Fed’s future policy actions, thereby influencing USD demand and determining the short-term trajectory of the precious metal.

Uncertainty surrounding when the Federal Reserve will commence interest rate cuts is holding back traders from committing to new positions in gold. The New York Fed revealed on Monday that consumer inflation expectations in the US dipped to their lowest point in nearly three years in December, heightening speculations of an imminent shift in the Fed’s policy stance. In contrast, the resilient US economy, marked by above-target inflation, affords the US central bank more leeway to maintain higher interest rates for a longer duration. This situation helps keep the yield on the benchmark 10-year US government bond above the 4.0% threshold, bolstering the US Dollar and capping gold’s performance. Despite these factors, bearish traders appear hesitant and opt to wait on the sidelines in anticipation of the forthcoming US consumer inflation figures, set to be unveiled on Thursday.

In recent developments, CNBC reported late on Tuesday that Iran-backed Houthi militants executed their largest attack to date on commercial merchant vessels, according to a senior US Defense Department official. Meanwhile, a senior official from the People’s Bank of China stated on Wednesday that the central bank might employ monetary policy tools to support reasonable credit growth. The official further mentioned that the PBoC intends to strengthen its counter-cyclical and cross-cycle policy adjustments to foster favorable conditions for the country’s economic growth. As for scheduled market-moving macroeconomic data from the US on Wednesday, there is none, leaving the XAUUSD pair susceptible to the dynamics of the USD price.

SILVER Analysis:

XAGUSD Silver price is moving in an Up-trend line and the market has reached the higher low area of the trend line

The US Dollar gained strength against other currencies in anticipation of higher US Consumer Price Index data for the month of December.

The US Dollar surged against other currencies as market participants adopted a cautious stance in anticipation of the eagerly awaited inflation data set to be released on Thursday. As we move into Wednesday, the major currency pairs appear to be relatively stable. The potential influence on currency valuations looms with forthcoming comments from central bankers and the scheduled 10-year US Treasury note auction later in the day. The benchmark 10-year US Treasury bond yield remains firmly above the 4% mark, while the USD Index maintains its position above 102.50. Notably, New York Federal Reserve (Fed) President John Williams, who had previously stated in December that rate cuts were not under discussion, is scheduled to deliver a speech.

USDCAD Analysis:

USDCAD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

In November, Canada’s trade balance shifted to 1.57 billion CAD from a previous surplus of 3.2 billion CAD. Additionally, building permits experienced a 3.9% decline, in contrast to the prior -1.7% figure. Following the release of this data, the Canadian Dollar depreciated.

The Canadian Dollar continued to weaken as Canada’s International Merchandise Trade in November retreated from the 14-month high reached in October. Additionally, Canadian Building Permits for November registered a nearly 4% decline. While Crude Oil attempted to recover from Monday’s downturn, it struggled to gain significant upward momentum, resulting in Crude Oil remaining relatively flat for the week as buyers found it challenging to push prices higher. Canada’s trade balance is moving back towards the average as November’s International Merchandise Trade Balance decreased from October’s 14-month peak of CAD 3.2 billion to CAD 1.57 billion, with October receiving an upward revision from CAD 2.97 billion.

Moreover, Canada’s Building Permits for November fell more than anticipated, dropping by 3.9% compared to the forecast of -1.7%. October’s Building Permits, on the other hand, increased by 3% following a positive revision from 2.3%.

In the United States, the trade deficit decreased by a smaller margin than expected, with the Goods Trade Balance for November improving slightly from a slightly-revised -90.3 billion to -89.4 billion. November’s US Goods and Services Trade Balance also saw a smaller decline than anticipated, reaching $-63.2 billion compared to the forecast of $-65.0 billion. October’s figure was mildly revised from $-64.3 billion to $-64.5 billion. The market’s primary focus will be on Thursday’s US Consumer Price Index inflation report, where headline CPI inflation is expected to rise to 3.2% YoY in December.

And American authorities have informed that Iran-backed Houthi rebels carried out missile and drone attacks on 50 merchant vessels in the Red Sea, marking the most substantial assault on this sea route by the rebels. The ship crews have reported these rebel attacks on the sea routes to maritime security offices, with the incidents occurring on Tuesday.

According to a senior official from the US Defense Department, CNBC News late on Tuesday reported that Iran-backed Houthi militants executed their most extensive assault to date on commercial merchant ships. Incidents occurred in at least two locations: Southwest of Mokha, Yemen, and Hodeidah, Yemen. American officials stated that around 50 merchant vessels were present in the vicinity when the attack took place. Crews reported being targeted by rocket fire and armed drones.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

In December, the Swiss Consumer Price Index saw an increase from 1.4% to 1.7%. Retail sales also exceeded expectations, rising to 0.70% compared to the anticipated 0.0%. However, the unemployment rate climbed to 2.2% from its previous reading of 2.1%. The Swiss National Bank is bracing for an annual loss of 3 billion Swiss Francs due to the appreciating Swiss Franc in the market, impacting both equities and foreign portfolios of FX reserves investments.

The US Dollar Index is holding firm above the 102.50 level, supported by stable US bond yields, with the 2-year and 10-year yields at 4.35% and 4.02%, respectively. The recent risk-on sentiment was ignited by remarks made earlier in the week by Atlanta Federal Reserve President Raphael W. Bostic, speculating on potential interest rate cuts by the end of 2024. This has placed downward pressure on the US Dollar, as Bostic cited a greater-than-expected decline in inflation and expressed the expectation of two quarter-point rate cuts by the close of 2024. Additionally, market attention will be focused on Thursday’s release of December’s Consumer Price Index data for the United States.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

On a contrasting note, Switzerland saw positive economic data on Monday, bolstering the Swiss Franc’s gains. The December Consumer Price Index (YoY) exhibited an increase from 1.4% to 1.7%, while Real Retail Sales improved to 0.7%, surpassing the anticipated flat reading of 0.0%. Tuesday brought further good news as the seasonally adjusted Unemployment Rate improved to 2.2%, up from the previous rate of 2.1%. It’s worth noting that the Swiss National Bank is anticipating an annual loss of approximately 3 billion CHF for the previous year, primarily due to the robust strength of the Swiss Franc, which has offset capital gains derived from the bank’s equity and bond portfolios denominated in foreign currencies.

GBPUSD Analysis:

GBPUSD is moving in an Up-trend line and the market has reached the higher low area of the trend line

The British Pound saw a modest increase as the Bank of England diverged from economists’ expectations by refraining from hinting at rate cuts in 2024. This comes against a backdrop of rising inflation and elevated interest rates, which has cast a shadow over the outlook for the UK economy. Today, there is anticipation surrounding the scheduled speech by Bank of England Governor Bailey.

An improved market risk appetite, fueled by comments from Federal Reserve (Fed) members speculating about potential rate cuts by the end of 2024, has contributed to a weaker US Dollar. However, a sudden shift towards risk aversion has added pressure, impacting the GBPUSD pair. The US Dollar Index is currently consolidating near 102.50 after recent gains, attempting to extend its profits due to improved US Treasury yields. As of the latest data, the 2-year and 10-year yields on US bond coupons stand at 4.36% and 4.02%, respectively. Nevertheless, the risk-on sentiment triggered by the Federal Reserve’s members’ remarks speculating on interest rate cuts by the end of 2024 has exerted downward pressure on the US Dollar. Atlanta Fed President Raphael W. Bostic mentioned that inflation has declined more than initially anticipated and expressed an expectation of two quarter-point cuts by the end of 2024. Additionally, US Fed Governor Michelle W. Bowman expressed that the current policy stance appears sufficiently restrictive, but it might eventually become appropriate to lower the Fed’s policy rate if inflation falls closer to the 2% target.

The GBPUSD pair has recently exhibited strength, largely influenced by monetary policy differences between the Bank of England and the US Federal Reserve (Fed). The BoE has maintained its stance on further rate hikes, even as indicators like inflation and wage growth show signs of easing. In contrast, expectations are growing that the Fed may initiate an easing cycle as early as March. DeAnne Julius, a former member of the Bank of England’s monetary policy committee, holds a different view regarding interest rates. She believes that the Bank of England won’t be in a position to start cutting interest rates in 2024. Additionally, she mentioned that escalating tensions in the Middle East could potentially lead to a new round of energy price increases, triggering a fresh inflation shock. BoE’s Governor Andrew Bailey is scheduled to deliver a speech on Wednesday. Furthermore, UK Manufacturing Production data will be released on Friday, with expectations of growth in November. On the US calendar, December’s Consumer Price Index (CPI) data from the United States will be released on Thursday.

GBPJPY Analysis:

GBPJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

After the release of lower CPI data in Japan, the Ministry of Labor department announced a decrease in real wages in the country. As a result, the Bank of Japan is expected to maintain an extremely accommodative policy during this month’s meeting, leading to weakness in the Japanese Yen against the US Dollar.

Data released on Tuesday indicated a decline in inflation rates in Tokyo. Furthermore, the Labour Ministry’s report today revealed that real wages in Japan contracted for the 20th consecutive month in November, reinforcing expectations that the Bank of Japan (BoJ) will maintain its highly accommodative policy stance at the January 22-23 meeting. This, combined with government stimulus measures following a destructive earthquake, is likely to postpone the BoJ’s plan to move away from negative interest rates. Additionally, the stable performance of equity markets undermines the safe-haven status of the Japanese Yen.

The Japanese Yen continues to weaken following the Labour Ministry’s report on Wednesday, which disclosed that inflation-adjusted real wages had decreased by 3.0% in November compared to the previous year. Furthermore, nominal pay for Japanese workers only grew by a modest 0.2% in November, marking the slowest increase in nearly two years, in contrast to a 1.5% rise in the preceding month. This follows Tuesday’s data, which revealed that Tokyo’s core Consumer Price Index had decelerated to a 2.1% year-on-year rate in December, matching a low recorded in June 2022. These developments further diminish hopes of a hawkish shift by the Bank of Japan, which considers wage trends and inflation projections as pivotal factors in its deliberations on reversing its negative interest rate policy. The Asahi newspaper reported that the Japanese government is contemplating doubling budget reserves to 1 trillion Yen for the upcoming fiscal year starting in April to cover the expenses associated with earthquake reconstruction. Japanese Prime Minister Fumio Kishida’s cabinet also approved 4.74 billion Yen in spending from fiscal 2023/24 reserves for items such as water, food, diapers, and heaters.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

ECB Vice President Francois De Villeroy stated that the ECB would refrain from reducing rates until inflation solidly returns to the 2% target. This announcement gave a boost to the Euro currency.

Banque de France Governor and European Central Bank policymaker François Villeroy de Galhau reiterated his expectation of rate cuts in 2024 during his New Year’s address to the European financial sector on Tuesday. Villeroy, who plays a significant role in shaping European central bank and monetary policy as a member of the ECB’s Governing Council, emphasized that the ECB is poised to lower rates in 2024 as long as unforeseen surprises do not alter the underlying economic fundamentals.

He stressed that the ECB will not make any rate adjustments until inflation expectations are firmly anchored at the 2% target. Villeroy also highlighted the ECB’s commitment to data-driven decisions, indicating that central policy planners will not rush but will remain flexible in their approach. He underscored the importance of continued vigilance regarding inflation data.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

Both business and consumer confidence in the New Zealand economy experienced growth, with building permits surging by more than 8.7% in October. This strong performance contributed to the New Zealand Dollar strengthening against its counterparts.

The New Zealand Dollar faced losses against the US Dollar, and traders are now anticipating the release of November’s Building Permits data from New Zealand, following an 8.7% increase reported in October. Positive Kiwi Consumer Confidence and Business Confidence figures for November have strengthened the belief that the Reserve Bank of New Zealand will maintain a hawkish stance by refraining from policy easing in the upcoming meeting, contributing to a favorable outlook for the New Zealand Dollar. Furthermore, attention is likely to turn to Friday’s Chinese Consumer Price Index and Producer Price Index figures, given the close economic ties between China and New Zealand.

The US Dollar Index is holding steady near 102.50 following recent gains, as it seeks to extend its upward momentum despite uncertain US Treasury yields. Currently, the 2-year and 10-year yields on US bonds stand at 4.35% and 4.01%, respectively. The Greenback may find support if the risk aversion sentiment strengthens ahead of the release of December’s Consumer Price Index (CPI) data from the United States, scheduled for Thursday. Investors are keenly observing signals from the Federal Reserve regarding the trajectory of interest rates. While higher interest rates could potentially weigh on overall demand, leading to subdued economic growth and a softer job market, the consensus suggests that the Fed is unlikely to implement any rate cuts in its upcoming January policy meeting.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/