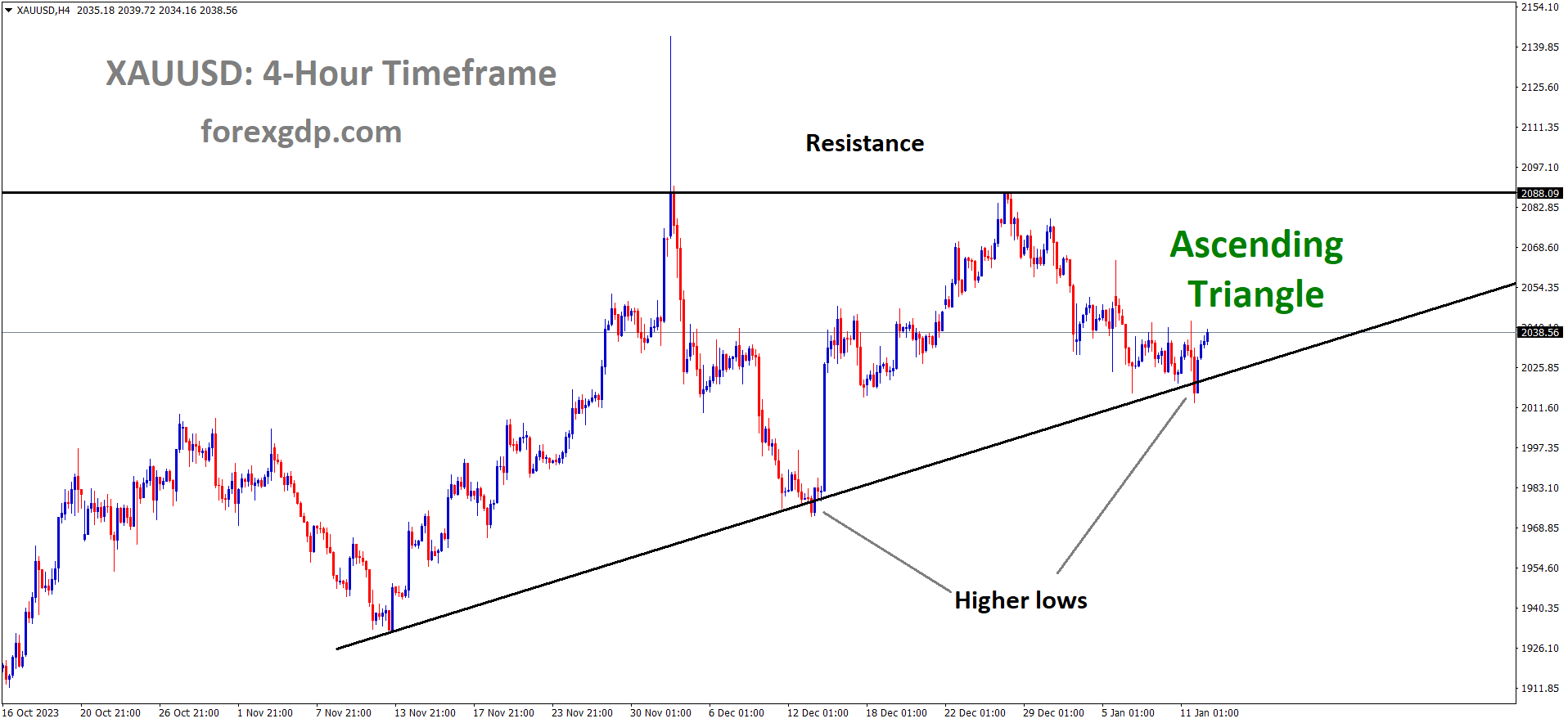

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending triangle pattern and the market has rebounded from the support area of the pattern

Gold prices dipped following the release of higher US CPI data yesterday. Additionally, the sluggish pace of China’s economic recovery contributed to a decline in gold prices against the USD in the market.

During the early European session, the precious metal continues its steady upward climb for the day, benefiting from renewed demand for safe-haven assets amid concerns about a potential escalation of geopolitical tensions in the Middle East. However, the metal is still trading below the key resistance zone of $2,040-2,042, which suggests caution among bullish traders due to uncertainty surrounding the Federal Reserve’s stance on interest rate cuts.

The recent release of slightly higher US consumer inflation figures on Thursday, coupled with hawkish comments from Fed officials, has led investors to trim their expectations of aggressive policy easing. This has provided support to US Treasury bond yields and the US Dollar (USD), potentially limiting gains for gold, which doesn’t yield interest. Nevertheless, the market still anticipates a higher likelihood of a Fed rate cut in March, which should provide a floor for the non-yielding yellow metal. In the short term, traders are closely monitoring the US Producer Price Index (PPI) and a speech by Minneapolis Fed President Neel Kashkari for market direction.

The mixed US consumer inflation figures have raised the possibility that the Federal Reserve may delay an anticipated rate cut in March, causing gold prices to fall to a one-month low on Thursday. In December, the headline US Consumer Price Index (CPI) increased from a year-on-year rate of 3.1% to 3.4%, while the core CPI recorded its smallest yearly increase since May 2021. Cleveland Fed President Loretta Mester commented on the CPI data, suggesting that it might be too early for the central bank to lower interest rates at the March policy meeting.

Richmond Fed Chief Tom Barkin also stated that the central bank needs to be confident that inflation is moving toward the target before considering rate cuts, indicating a potential shift in policy once inflation reaches 2%. Chicago Fed President Austan Goolsbee added that the central bank remains comfortable with its approach to inflation and will assess policy restrictiveness as inflation continues to decline. Market sentiment, as reflected in the CME Group’s FedWatch Tool, still indicates a more than 65% probability of a rate cut in March, providing support for gold. Additionally, the yield on the 10-year US government bond remains below the 4.0% threshold, keeping pressure on the US Dollar and benefiting gold.

Furthermore, recent military actions by US and UK forces against Houthi targets in response to attacks on ships in the Red Sea have heightened geopolitical tensions, potentially adding further support to gold. US President Joe Biden has expressed willingness to take further measures following airstrikes on Houthi targets in Yemen, and UK Prime Minister Rishi Sunak has emphasized their commitment to safeguarding freedom of navigation and trade flow. Chinese inflation data released on Friday has raised deflationary concerns, and a 0.3% drop in imports for 2023 indicates sluggish domestic demand, contributing to worries about a slow economic recovery.

In summary, gold appears on track to end the week with losses for the second consecutive week, with traders keeping a close eye on the US Producer Price Index and Minneapolis Fed President Neel Kashkari’s speech for potential market catalysts.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern

The December US inflation data exceeded expectations, coming in at 3.4% instead of the anticipated 3.2%. These unexpectedly positive figures led to a strengthening of the US Dollar against other currencies.

Following the release of December inflation figures on Thursday, the US Dollar initially performed well against other currencies but couldn’t maintain its strength as US Treasury bond yields declined during the later part of the American session. While the markets remained relatively calm early on Friday, the upcoming Producer Price Index data for December from the US has the potential to increase volatility as the weekend approaches.

According to the US Bureau of Labor Statistics, the Consumer Price Index rose by 3.4% on a yearly basis in December, following a 3.1% increase in November. This figure exceeded market expectations of a 3.2% rise. The Core CPI, which excludes the volatile components of food and energy prices, increased by 0.3% on a monthly basis, in line with forecasts.

After the release of the inflation report, the USD Index surged to a five-day high of 102.76. However, it ended the day with little change below 102.50, as the yield on the benchmark 10-year US Treasury bond failed to hold above 4%.

In China, data showed that the Consumer Price Index in December increased by 0.1% on a monthly basis, rebounding from a 0.5% decrease observed in November. Additionally, China’s trade surplus widened to $75.34 billion in December from $68.39 billion, surpassing market expectations of a surplus of $74.75 billion. Despite these positive economic indicators, both the Shanghai Composite and the Hang Seng indexes were trading flat at the time of reporting.

USDJPY Analysis:

USDJPY is moving in the Up-trend line and the market has reached the higher low area of the trend line

The Bank of Japan occasionally implements negative interest rates in response to earthquake disasters and wage hike challenges within Japan’s economy. As a result, the Japanese yen (JPY) tends to weaken against the US dollar.

On Friday, the Japanese Yen continued its upward momentum for the second consecutive day against the US Dollar, recovering further from a one-month low it had reached following the release of US consumer inflation figures. This rise in the Yen’s value can be attributed to several factors. Firstly, amid China’s economic challenges, the Japanese Yen is benefiting from its relative safe-haven status, especially with the potential for increased geopolitical tensions in the Middle East looming in the background. Secondly, the US Dollar remained subdued in terms of price action, which put downward pressure on the USDJPY currency pair. The recent headlines regarding a slightly higher US Consumer Price Index and comments from Federal Reserve officials have led to speculation that US interest rates may remain elevated for a longer period. However, the market still anticipates a possible shift in the Fed’s policy stance in March. This, in turn, has had an impact on US Treasury bond yields and has weighed on the US Dollar. Despite these factors, the downside for the USDJPY pair is somewhat cushioned by the growing consensus that the Bank of Japan (BoJ) is unlikely to deviate from its ultra-dovish monetary policy stance.

Given this mixed fundamental backdrop, it is advisable to wait for more pronounced selling pressure before considering fresh bearish positions, confirming that the recent recovery of the USDJPY pair from multi-month lows has reached its limits. Traders are now closely watching the US Producer Price Index and a speech by Minneapolis Fed President Neel Kashkari, as these events could influence the US Dollar and provide further market direction. Nevertheless, it appears that the currency pair is set to end the week with gains for the second consecutive week. It is expected that the Bank of Japan will maintain its ultra-loose monetary policy settings at its upcoming meeting on January 22-23, which continues to weigh on the Japanese Yen. Additionally, the US consumer inflation figures released on Thursday have cast doubt on the likelihood of a rate cut by the Federal Reserve in March, offering some support to the USDJPY pair. The US Labor Department reported that the headline US CPI increased by 0.3%, with a year-on-year rise from 3.1% to 3.4% in December. Excluding the volatile food and energy prices, the core CPI increased by 0.3% last month and rose 3.9% year-on-year in December, marking its smallest gain since May 2021.

Comments from Cleveland Fed President Loretta Mester and Richmond Fed Chief Tom Barkin suggested that the central bank is not in a rush to lower interest rates in March. However, they indicated that the Fed would consider rate cuts once inflation is on track to reach its 2% target. In a separate development, reports emerged of attacks by US and UK forces against multiple Houthi targets in response to repeated drone and missile attacks on ships in the Red Sea. This geopolitical situation adds another layer of complexity to the market. Traders will be closely monitoring the US Producer Price Index for fresh insights, with expectations of a 1.3% year-on-year increase in December, up from the previous 0.9%. The core PPI is expected to tick down to 1.9% from November’s 2.0%.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc depreciated against other currencies following the release of higher US CPI data. Additionally, tensions in the Red Sea involving the US and UK against Yemen rebels have led to cautious market movements in both the Swiss Franc and US Dollar.

While the firmer US Dollar, driven by positive US inflation data, may offer some support to the USD, its potential upside against the Swiss Franc (USDCHF) could be constrained by increasing tensions in the Middle East. Inflation in the United States showed an upward trend in December, with the Bureau of Labor Statistics reporting an annual Consumer Price Index (CPI) increase of 3.4%, up from 3.1% in the previous month, surpassing expectations of 3.2%. On a monthly basis, the CPI rose by 0.3%, compared to a 0.1% increase in November. It’s worth noting that this robust US inflation data, along with positive labor market indicators, might delay the anticipated Federal Reserve rate cut in March.

On the flip side, the escalating tensions in the Middle East could drive safe-haven flows into currencies like the Swiss Franc. Recent events have seen the US and UK forces conducting strikes against multiple Houthi targets in areas of Yemen controlled by the Houthi rebels. US President Joe Biden has stated that these actions are a direct response to Houthi attacks on international maritime vessels in the Red Sea.

Earlier this week, Switzerland’s Consumer Price Index for December outperformed expectations, rising to 1.7% year-on-year from the previous reading of 1.4%. Additionally, Real Retail Sales for November came in at 0.7%, surpassing the previous figure of -0.3%. Looking ahead, the release of the December US Producer Price Index (PPI) is expected later on Friday, with forecasts indicating a 0.1% month-on-month increase and a 1.3% year-on-year rise. Traders will closely monitor these data releases for potential trading opportunities within the USDCHF pair.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The ECB Economy Bulletin indicates that the Eurozone experienced a slowdown in the third quarter of 2023, and any potential rate cuts will be contingent on data-driven decisions. Inflation is expected to continue weakening in the coming days, while employment maintains a steady growth trajectory.

During the US market session, the Euro experienced a decline against the US Dollar, primarily due to US Consumer Price Index inflation figures surpassing market expectations. This development offset the Euro’s earlier positive performance for the day. While the Euro exhibited strength against most major currencies on Thursday, it remained flat against the safe-haven currencies, the US Dollar and the Japanese Yen, during the first half of the US session. However, it rebounded before the close of the Thursday trading session.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The European Central Bank released its latest Economic Bulletin earlier on Thursday, largely maintaining its stance. The ECB emphasized its data-driven approach, with a continued focus on inflation expectations for the European economy. The Euro initially made notable gains on Thursday but experienced a slight setback following the release of US CPI data.

The US CPI inflation data for December exceeded expectations, with headline inflation increasing by 0.3% month-on-month (MoM), surpassing the forecasted 0.2% and November’s 0.1%. The annualized core US CPI saw a slight decline from 4.0% to 3.9%, which was less than the market’s anticipated drop to 3.8%. Year-on-year (YoY) December headline CPI rose to 3.4% from 3.1%, exceeding the forecast of 3.2%. The higher inflation figures may complicate the Federal Reserve’s ability to justify rate cuts as quickly as some market participants had hoped.

The European Economic Bulletin noted that the ECB continues to prioritize data releases and that potential rate cuts hinge on forward-looking inflation expectations. The bulletin also highlighted a slight contraction in the euro area economy in the third quarter of 2023, attributing it to a decline in inventories. Despite expectations of weakening growth, the ECB acknowledged the resilience of employment in the euro area. Overall, the Euro experienced fluctuations during the trading session, with its performance influenced by the US CPI data and the ECB’s commitment to data-driven decision-making.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

In November, the UK’s GDP data showed a growth of 0.30%, contrasting with a 0.30% contraction in October. This unexpected boost in GDP had a positive impact on the GBP, causing it to strengthen against other currencies.

According to the latest data released by the Office for National Statistics (ONS) on Friday, the UK economy rebounded in November, growing by 0.3% following a 0.3% contraction in October. Market analysts had anticipated a 0.2% expansion during the same period. In addition, the Index of Services for November recorded a 3-month growth rate of 0%, surpassing the -0.1% reading in October and exceeding expectations of a 0.2% increase.

The Canadian Dollar strengthened in response to the Red Sea conflicts, which involved US and UK airstrikes against Yemen rebels. US President Joe Biden stated that these actions were taken to ensure the safety of commercial vessels and counteract the activities of the rebels in the Red Sea.

The Canadian Dollar has gained strength in response to the rise in crude oil prices, a surge that can be attributed to heightened tensions in the Middle East. The military forces of the United States (US) and United Kingdom, supported by Australia, Bahrain, Canada, and the Netherlands, conducted airstrikes on Houthi targets in Yemen, which is backed by Iran. This action was taken to protect maritime vessels in the Red Sea. The West Texas Intermediate oil price is currently trading near $73.40 per barrel. With no economic data from Canada available for the entire week, traders are eagerly anticipating next week’s release of Canada’s Consumer Price Index data for December and Retail Sales figures for November, scheduled for Tuesday and Friday, respectively.

GBPNZD Analysis:

GBPNZD is moving in the Descending channel and the market has reached the lower high area of the channel

China’s trade balance has surged to $75.34 billion, surpassing the expected $68.39 billion and the previous reading of $74.75 billion. This development provided a boost to the New Zealand Dollar against the US Dollar in the market. Export data outperformed expectations, showing a 2.3% increase compared to the anticipated 1.7%, while import data also exceeded expectations with a 1.6% rise compared to the previous reading of 0.60%.

NZDUSD Analysis:

NZDUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The NZDUSD pair is experiencing upward momentum as improved risk appetite prevails in the market, driven by trader speculation regarding potential rate cuts by the Federal Reserve in March and May. This optimism persists despite the release of upbeat inflation data from the United States. Moreover, the New Zealand Dollar is finding support from moderate Chinese inflation figures, considering the close trade relationship between the two countries. In December, the Chinese Consumer Price Index unexpectedly decreased by 0.3%, diverging from the anticipated 0.4% decline. The monthly Consumer Price Index exhibited a more modest easing of 0.1%, compared to the market’s expected 0.2%. Meanwhile, the annual Producer Price Index recorded a 2.7% decline, slightly surpassing the anticipated decrease of 2.6%. Additionally, the Chinese Trade Balance for December surged to $75.34 billion from the previous $68.39 billion, exceeding the expected figure of $74.75 billion. Export figures showed a growth of 2.3%, surpassing the expected 1.7%, while the annual Imports in CNY increased by 1.6% compared to the previous 0.6%. Traders are now awaiting the release of the US Producer Price Index data for December, seeking further insights into the economic landscape of the United States.

In contrast, the US Dollar Index has been relatively stable, consolidating recent gains during the early Asian trading hours on Friday, following the release of positive US inflation data. However, the DXY is trading slightly lower, hovering near 102.20, despite improved US Treasury yields. As of the latest available data, the 2-year and 10-year yields on US bonds are at 4.26% and 3.97%, respectively. Furthermore, the robust US inflation data has provided some support to the US Dollar, enabling it to gain slight upward traction. The US Consumer Price Index (CPI) for December reported a year-on-year increase of 3.4%, surpassing both November’s 3.1% and the market’s expected figure of 3.2%. The monthly CPI growth for December showed a 0.3% increase, exceeding the market’s projection of 0.2%. The annual Core CPI, which excludes volatile items, eased slightly to 3.9% from the previous reading of 4.0%, while the monthly figure remained steady at 0.3%, in line with expectations.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

China’s December inflation data revealed a decrease of 0.30%, which was slightly better than the expected 0.40% decline. The Australian Dollar showed minimal movement in response to this data release.

The National Bureau of Statistics in China has reported that the Consumer Price Index (CPI) continued its decline for the third consecutive month, showing a 0.3% year-on-year decrease in December. Additionally, the Producer Price Index (PPI), which measures the costs of goods at the factory gate, fell by 2.7% year-on-year in December, marking the 15th consecutive month of decline. These data releases have sparked speculation that the Chinese government may introduce further stimulus measures to address deflationary risks.

Furthermore, China’s Customs department reported that the country’s exports and imports of goods for 2023 exceeded expectations. This development has boosted the Australian Dollar, which is often seen as a proxy for China’s economic performance. China’s Yuan-denominated exports for 2023 increased by 0.6% year-on-year, indicating signs of recovery in global trade. However, imports for the same period declined by 0.3% year-on-year, suggesting weak domestic demand and raising concerns about a sluggish economic recovery.

And TDS Analysts had foreseen China adopting a cautious approach to bolster its economy through fiscal measures last year. However, they are eagerly awaiting the economic outcomes until the first quarter of 2024. China’s government maintained its proactive stance on economic stimulus until the GDP reached its 5% target by the year 2024.

The economic prospects for China continue to appear uncertain. TD Securities’ economists have provided their projections for fiscal and monetary policies in the upcoming year. Despite the stimulus measures introduced in the fourth quarter of 2023, China’s economic momentum as it enters 2024 remains modest. As the fiscal resources allocated in the latter part of last year are injected into the economy, policymakers will closely monitor the economic data for the first quarter of 2024 before revising their assessment of the economic path ahead. It is our expectation that the authorities will maintain an active stance, utilizing both fiscal and monetary tools to ensure that China’s GDP growth reaches approximately 5% for the year.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/