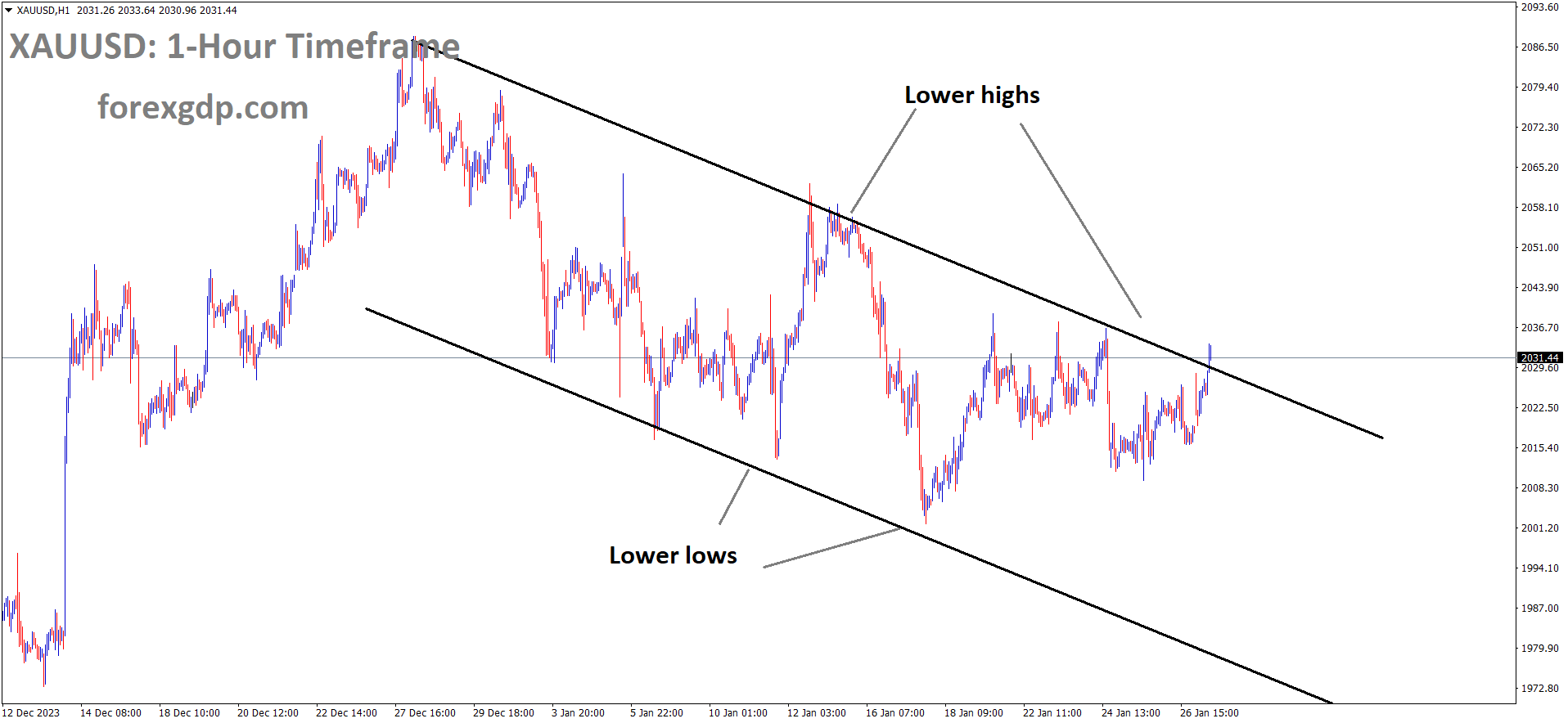

GOLD Analysis:

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Gold prices declined following the release of stronger-than-expected US Q4 GDP figures last week, accompanied by Core PCE index data that was lower than anticipated.

Additionally, tensions in the Middle East escalated during a Sunday event, resulting in gold prices remaining lower in comparison to the US dollar.

Bullish investors should exercise patience and await a breakout above the $2,040-2,042 supply zone before considering further potential gains, especially in anticipation of the FOMC decision. As we approach the significant central bank event, the escalating tensions in the Middle East serve as a noteworthy catalyst bolstering the safe-haven appeal of Gold. Concurrently, the flight to safety exerts downward pressure on US Treasury bond yields, lending additional support to XAUUSD.

While the US Dollar remains below its one-month high reached last week, it currently offers minimal directional influence. Nevertheless, the diminishing likelihood of a more aggressive Federal Reserve policy easing in 2024 may continue to provide tailwinds for the USD, potentially capping the upside for Gold, a non-yielding asset. This warrants caution among bullish traders, prompting them to await substantial follow-through buying before confirming a potential bottom for Gold, particularly near the psychologically significant $2,000 level.

At the start of the new week, the ongoing risk of further escalation in Middle East geopolitical tensions weighs on investor sentiment, bolstering the safe-haven appeal of Gold.

A drone attack on a US base in Jordan resulted in the tragic loss of three US soldiers, marking the first such incident since the outbreak of the Israel war on October 7. President Joe Biden reaffirmed his commitment to respond and hold those responsible accountable at a time and in a manner chosen by the United States.

Meanwhile, the US Dollar remains relatively steady, just below a one-month peak, as investors recalibrate their expectations regarding the Federal Reserve’s monetary policy. Recent data released on Friday indicated a modest uptick in December’s inflation, reaffirming expectations that the Fed may begin cutting interest rates by mid-2024.

The US Bureau of Economic Analysis reported that the Personal Consumption Expenditures (PCE) Price Index maintained a steady yearly rate of 2.6% in December. Conversely, the annual Core PCE Price Index, considered the Fed’s preferred inflation gauge, showed a more significant deceleration than anticipated, dropping to 2.9% from November’s 3.2%. Additionally, other aspects of the report highlighted a 0.7% rise in Personal Spending in December, coupled with a 0.3% increase in Personal Income, indicating robust demand from US consumers. This data, along with a strong Q4 GDP print from the previous week, suggests that the US economy remains in good health, further fueling optimism regarding a smooth economic trajectory.

A slight decrease in US Treasury bond yields is capping the Greenback’s potential for further gains and may continue to provide tailwinds for Gold, which is not yield-producing. Traders might opt to wait for the upcoming FOMC meeting commencing on Tuesday, as well as this week’s pivotal US economic data releases, including the Nonfarm Payrolls report scheduled for Friday.

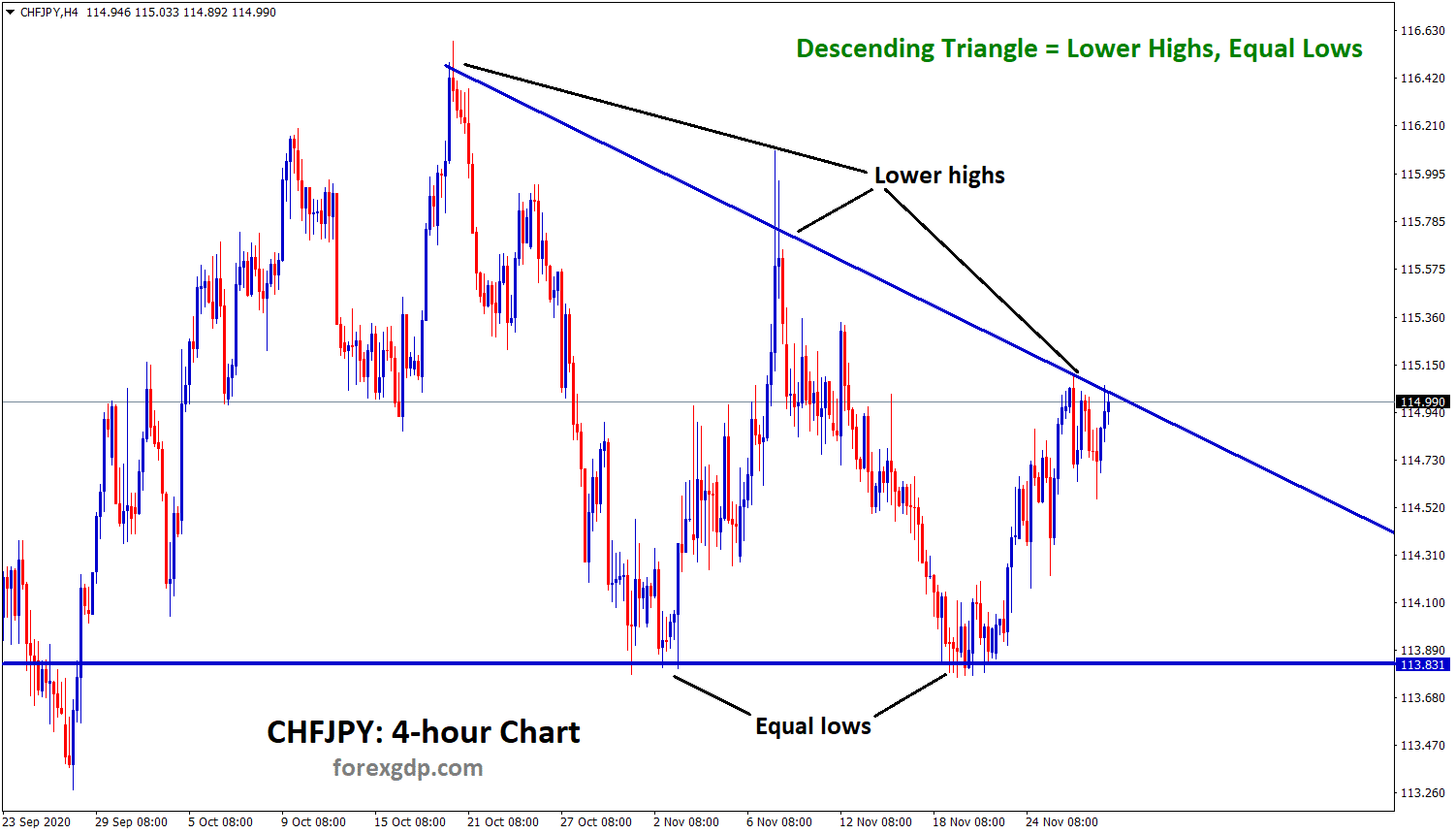

SILVER Analysis:

XAGUSD Silver price is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern

The US Dollar gained strength against its counterparts in anticipation of the upcoming US Federal Reserve meeting and the release of US Non-Farm Payroll (NFP) data scheduled for this week. Federal Reserve officials have suggested that some individuals may have overly optimistic expectations regarding potential rate cuts by the Fed. However, this perspective does not align with the Fed’s actual outlook.

In the lead-up to the upcoming FOMC meeting next week, prominent members of the Federal Reserve have been cautioning against overly optimistic expectations regarding future rate cuts. They emphasize that the Fed does not intend to reduce the benchmark interest rate as rapidly as the market has anticipated. As illustrated in the chart below, future rate expectations for all 2024 Fed funds futures contracts have been scaled back recently. The colored lines have trended higher, indicating a decreased likelihood of rate cuts across the board since the end of the previous year. While reduced expectations for rate cuts are supportive of the US dollar, it’s important to note that the threshold for a sustained bullish move remains quite high.

Furthermore, accompanying data has reinforced the Fed’s message. December’s Consumer Price Index (CPI) came in hotter than expected, revealing lingering price pressures. However, a significant portion of this increase was influenced by base effects that are now largely behind us.

came in hotter than expected, revealing lingering price pressures")

In addition to this, January’s preliminary Purchasing Managers’ Index (PMI) data showed strength, and the fourth-quarter GDP print, although lower than the 4.9% growth in the third quarter, remained solid. Equity markets have been performing well, and the unemployment rate is comfortably below 4%, favoring the idea of a “soft landing” or a stable economic path once again.

If the Fed identifies upside risks to services inflation due to the robust data, it will likely proceed cautiously. Nonetheless, the central bank’s statement is expected to shift towards a more neutral tone, possibly as early as next week. Transitioning from rate hikes to rate cuts is akin to steering a massive freight ship; it requires slowing down first, making the turn, and then proceeding in the opposite direction. Next week, we can anticipate a slowing down of the process.

A noteworthy observation is the duration between the last rate hike and the first rate cut since the 1970s, as shown in the chart below. Interestingly, the average time frame for these transitions rounds up to approximately 6 months. Today marks exactly 6 months since the Fed last raised the Fed funds rate.

And President Joe Biden has stated that three US soldiers tragically lost their lives, with an additional 34 soldiers sustaining injuries in a drone attack carried out by rebels with ties to Iran, targeting a US military camp in the Jordan area. The United States is committed to responding to this attack against our soldiers.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

The Swiss Franc strengthened against other currencies as tensions in the Middle East escalated on Sunday. The attack on US troops in the Red Sea by Iran-backed rebels has heightened concerns about the possibility of further military escalation.

The Swiss Franc is exhibiting strength against the US Dollar (USD), driven by a surge in risk aversion sentiment. This increased demand for the CHF can be attributed to the escalating tensions in the Middle East, a situation where geopolitical uncertainties tend to drive investors toward safe-haven currencies such as the Swiss Franc. Currently, there is uncertainty surrounding the stance of the Swiss National Bank regarding the persistent strength of the Swiss Franc. Despite concerns regarding the CHF’s strength, it is not expected that the SNB will take action to intervene in the foreign exchange market by purchasing foreign currency in order to curb the appreciation of the CHF.

The US Dollar Index is maintaining stability around the 103.50 mark, while 2-year and 10-year US Treasury yields remain subdued at 4.34% and 4.13%, respectively, as of the current moment. Despite the release of moderate US Core Personal Consumption Expenditures Price Index (PCE) data on Friday, the US Dollar failed to garner support. In December, the Core PCE reported a 0.2% monthly increase, in line with expectations and surpassing the previous reading of 0.1%. However, the annual Core PCE increased by 2.9%, falling short of the anticipated 3.0% and the previous reading of 3.2%.

As signs of inflation cooling off emerge, investors are contemplating the possibility of the Federal Reserve implementing a policy of easing. According to the CME FedWatch Tool, futures traders have priced in a 53% probability of the Fed implementing its first interest rate cut in this cycle during the March meeting. Nevertheless, the forthcoming Federal Open Market Committee statement on January 31 is expected to maintain the Fed Funds rate at its current level. Traders are likely to closely monitor key economic indicators, including the releases of the US Housing Price Index and Consumer Confidence figures scheduled for Tuesday, to gain additional insights into the market. On the Swiss economic calendar, Wednesday’s Real Retail Sales and the ZEW Survey will be closely watched to assess the overall health of the Swiss economy.

USDJPY Analysis:

USDJPY is moving in an Uptrend line and the market has reached the higher low area of the trend line

Following the release of Tokyo CPI data, which showed a downward trend on Friday, economists now anticipate a potential shift in monetary policy settings by the Bank of Japan in the near future. As a result, the Japanese yen has experienced a modest strengthening against other currencies.

An escalation of conflicts in the Middle East has dampened investors’ appetite for riskier assets, leading to a generally subdued sentiment in equity markets. This cautious tone, coupled with the Bank of Japan’s recent hawkish stance, indicating a potential phase-out of substantial stimulus measures and lifting short-term interest rates from negative territory, provides some support for the safe-haven Japanese Yen . Meanwhile, the US Dollar continues its consolidation in a familiar range, a pattern it has maintained for the past two weeks. This consolidation puts pressure on the USDJPY pair, especially in the presence of a slight decline in US Treasury bond yields. However, market participants may remain on the sidelines as they await the highly-anticipated two-day FOMC meeting, scheduled to begin on Tuesday.

Throughout the week, investors will also confront significant US economic releases, including the Nonfarm Payrolls (NFP) report set for Friday. Meanwhile, as the odds diminish for a more aggressive policy easing by the Federal Reserve, and uncertainty persists regarding the timing of the first interest rate cut, the USD is unlikely to experience a substantial decline in the absence of significant macroeconomic data. Additionally, the weaker Tokyo Core CPI released on Friday could contribute to limiting any further appreciation of the JPY.

The Tokyo CPI’s continued decline raises doubts about the Bank of Japan’s readiness to withdraw negative interest rates in the near future, potentially weakening the Japanese Yen. The US Dollar remains strong, near its highest level since December 13, reached last week, providing additional support to the USD/JPY pair. Nevertheless, traders may exercise caution and prefer to stay on the sidelines ahead of the crucial two-day FOMC monetary policy meeting that commences on Tuesday. Recent data showed a modest uptick in December’s inflation, reinforcing expectations that the Federal Reserve will reduce interest rates by mid-2024.

According to the US Bureau of Economic Analysis, the Personal Consumption Expenditures (PCE) Price Index held steady at 2.6% on a yearly basis in December. Conversely, the annual Core PCE Price Index, the Fed’s favored inflation measure, decelerated more than anticipated, dropping from 3.2% in November to 2.9%. Additional details revealed a 0.7% increase in Personal Spending in December, coupled with a 0.3% growth in Personal Income, signaling robust consumer demand.

These data points, combined with a positive Q4 GDP print, suggest that the US economy remains robust despite tightening financial conditions. However, the emergence of disinflationary pressures and progress towards the Fed’s 2% target have shifted expectations away from further tightening, leaving USD bulls somewhat defensive. Current market pricing indicates an even likelihood of easing at the March FOMC meeting and approximately a 90% probability of an interest rate cut in May. Alongside these developments, investors will grapple with the release of key US macroeconomic data at the beginning of the new month, with the Nonfarm Payrolls report taking center stage on Friday.

EURJPY Analysis:

EURJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel

On Sunday, Klaas Knot, a member of the ECB Governing Council, emphasized the importance of observing concrete evidence of decelerating wage growth in the economy before considering any rate cuts.

The decline in the major currency pair is being driven by renewed demand for the US Dollar (USD), a trend spurred by escalating geopolitical tensions in the Middle East. Investors are keeping a close eye on the upcoming Federal Open Market Committee (FOMC) meeting.

In the previous week, the European Central Bank (ECB) opted to keep key interest rates unchanged, citing a decrease in underlying inflation for December of the previous year. ECB President Christine Lagarde expressed concerns that the Eurozone likely experienced stagflation in the last quarter of 2023 and highlighted the risks of further economic slowdown. Lagarde emphasized the ECB’s commitment to a data-dependent approach, making decisions on a meeting-by-meeting basis.

Additionally, ECB governing council member Klaas Knot stated on Sunday that evidence of slowing wage growth in the Eurozone is necessary before considering interest rate cuts. Despite this, the market has increased its expectations for rate cuts, with projections of a 50 basis point (bps) reduction by June and a 140 bps cut by December 2024. On Tuesday, the German Gross Domestic Product (GDP) for the fourth quarter is expected to show a contraction of 0.3% on a quarterly basis and 0.2% on a yearly basis.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

In October, UK public inflation expectations decreased to 3.9%, and they further dropped to 3.5% in both November and December in this year’s projections. This revised outlook represents a decline from the previous poll, which recorded inflation expectations at 4.2%, as reported by the survey conducted by US Citibank and polling firm YouGov.

According to the most recent survey conducted by US bank Citi and polling firm YouGov, the expectations of the UK public regarding inflation in the upcoming year decreased during November and December. In October, these expectations were at 4.2%, but they dropped to 3.9% in November and further down to 3.5% in December. Additionally, the long-term UK inflation expectations also saw a decline, reaching 3.4%.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

Bank of Canada Governor Tiff Mackhelm has emphasized that interest rates will remain unchanged until inflation aligns with their target. The Canadian Dollar continues to benefit from ongoing support in the market due to stable oil prices.

The Canadian Dollar has encountered challenges following the Bank of Canada’s decision to maintain its benchmark interest rate at 5.0% on Wednesday, marking the fourth consecutive instance of the central bank keeping rates at this level. BoC Governor Tiff Macklem indicated a shift in focus, moving from discussing whether interest rates are sufficiently high to considering the possibility of lowering them in the future. According to the Bank of Canada’s Monetary Policy Report (MPR), the central bank anticipates that inflation will reach its 2.0% target by 2025.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Canadian Dollar’s losses may be mitigated by the positive performance of crude oil prices. West Texas Intermediate (WTI) oil prices extended their gains to nearly $78.20 per barrel during the Asian session on Monday. WTI prices reached a peak of $79.19 during the early Asian hours but later retraced some of their intraday gains. The surge in crude oil prices was primarily driven by concerns about potential supply disruptions following a missile attack on a fuel tanker in the Red Sea.

Additionally, a drone attack targeted a United States (US) outpost in Jordan on Sunday, resulting in the tragic deaths of three US service members. In response, the Biden administration and the US military are actively devising specific plans, including the possibility of conducting strikes into Iran. The heightened tension in the Red Sea region could provide support for WTI oil prices, which in turn act as a supporting factor for the Canadian Dollar.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Australian Dollar surged following optimistic news of additional stimulus injections by the Chinese government to boost their economy. However, the recent RBA bulletin indicates that the Australian economy has witnessed lackluster business performance over the past six months.

Despite this, the Australian Dollar is expected to receive a boost in the near term, thanks to favorable commodity prices.

The AUDUSD pair is making gains despite a stronger US Dollar, driven by escalating geopolitical tensions. In a drone attack on a US outpost in Jordan near the Syrian border, three United States service members were tragically killed, and at least 24 others were injured. Reports indicate that the US administration under President Joe Biden and the US military are actively devising specific plans for responding to this attack, including the possibility of launching strikes into Iran—a significant escalation if carried out.

Australia’s money market has maintained stability, partly influenced by the positive performance of Crude oil prices. Additionally, the Australian Dollar (AUD) may have received a boost from recent news indicating the potential implementation of additional stimulus measures by the People’s Bank of China. According to the Reserve Bank of Australia’s Bulletin, businesses have generally expected a moderation in price growth over the past six months, with prices projected to remain above the RBA’s inflation target range of 2.0–3.0%. However, the RBA is expected to reduce borrowing costs later this year. Market participants are eagerly awaiting Tuesday’s release of Australian Retail Sales data, with expectations of a 0.7% decline following a previous increase of 2.0%. Furthermore, the Consumer Price Index data scheduled for Wednesday will be closely monitored.

The US Dollar Index is benefitting from improved US Treasury bond yields, which could potentially limit the AUDUSD pair’s upward movement. On Friday, the US Core Personal Consumption Expenditures Price Index for December reported a 0.2% monthly increase, in line with expectations and surpassing the previous reading of 0.1%. However, the yearly Core PCE rose by 2.9%, falling short of the anticipated 3.0% and the prior reading of 3.2%. The Federal Open Market Committee (FOMC) statement is scheduled for Wednesday, January 31, with consensus expectations of no change to the Fed Funds rate at 5.25-5.50%. Nonetheless, the market’s leaning towards a potential rate cut in March may exert downward pressure on the USD. Additionally, Tuesday’s Housing Price Index and Consumer Confidence figures will be closely observed for further market insights.

Australia’s economic data shows signs of improvement, with Manufacturing PMI increasing from 47.6 to 50.3, and Services PMI experiencing an uptick from 47.1 to 47.9. The Composite PMI has also risen to 48.1 from December’s 46.9.

In other developments, Chinese financial media have reported that the People’s Bank of China may reduce the Medium-term Lending Facility (MLF) rate in the current quarter. This comes after PBoC Governor Pan Gongsheng recently announced a 50-basis-point reduction in the Required Reserve Ratio (RRR), effective from February 5th.

US Treasury Secretary Janet Louise Yellen has commented that the strong performance of the US economy in the fourth quarter is viewed as a positive development and is unlikely to pose challenges in terms of inflation. Furthermore, the US Gross Domestic Product Annualized reported a reading of 3.3%, surpassing the previous figure of 4.9% and exceeding the market consensus of 2.0%. Additionally, US Initial Jobless Claims for the week ending on January 19 unexpectedly declined to 214K, contrary to the expected increase from 189K to 200K.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In December, New Zealand’s trade balance improved to -$13.57 billion, compared to -$13.90 billion in the previous month. The primary factor contributing to this improvement is the decrease in imports, which fell from $7.20 billion in November to $6.26 billion in December.

Despite the prevailing strength of the US Dollar Index, the currency pair is making incremental gains. Investors are eagerly awaiting the Federal Open Market Committee meeting and the release of January’s US Nonfarm Payrolls data later in the week, in search of fresh market catalysts. Currently, NZDUSD is trading at 0.6107, marking a 0.26% increase for the day.

Market participants anticipate that the Federal Reserve will maintain interest rates within the range of 5.25–5.50% during its January meeting, scheduled for Wednesday. Notably, traders had been pricing in a 48.2% probability of the Fed implementing its first rate cut in March, a significant decline from the 88% probability estimated a month earlier.

On Monday, Statistics New Zealand reported that the nation’s Trade Balance for December stood at $-13.57 billion YoY, compared to the previous reading of $-13.90 billion. Additionally, exports decreased to $5.94 billion in December, down from the previous figure of $5.99 billion. Imports also witnessed a decline, amounting to $6.26 billion in the same month, in contrast to the $7.20 billion recorded in November.

Looking ahead, traders will closely monitor a speech by Reserve Bank of New Zealand (RBNZ) Chief Economist Conway, scheduled for Tuesday. Subsequently, the focus will shift to the FOMC meeting on Wednesday, an event that could potentially introduce volatility into the market. Market participants will pay close attention to any statements made by Fed Chairman Jerome Powell during the press conference following the meeting.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/