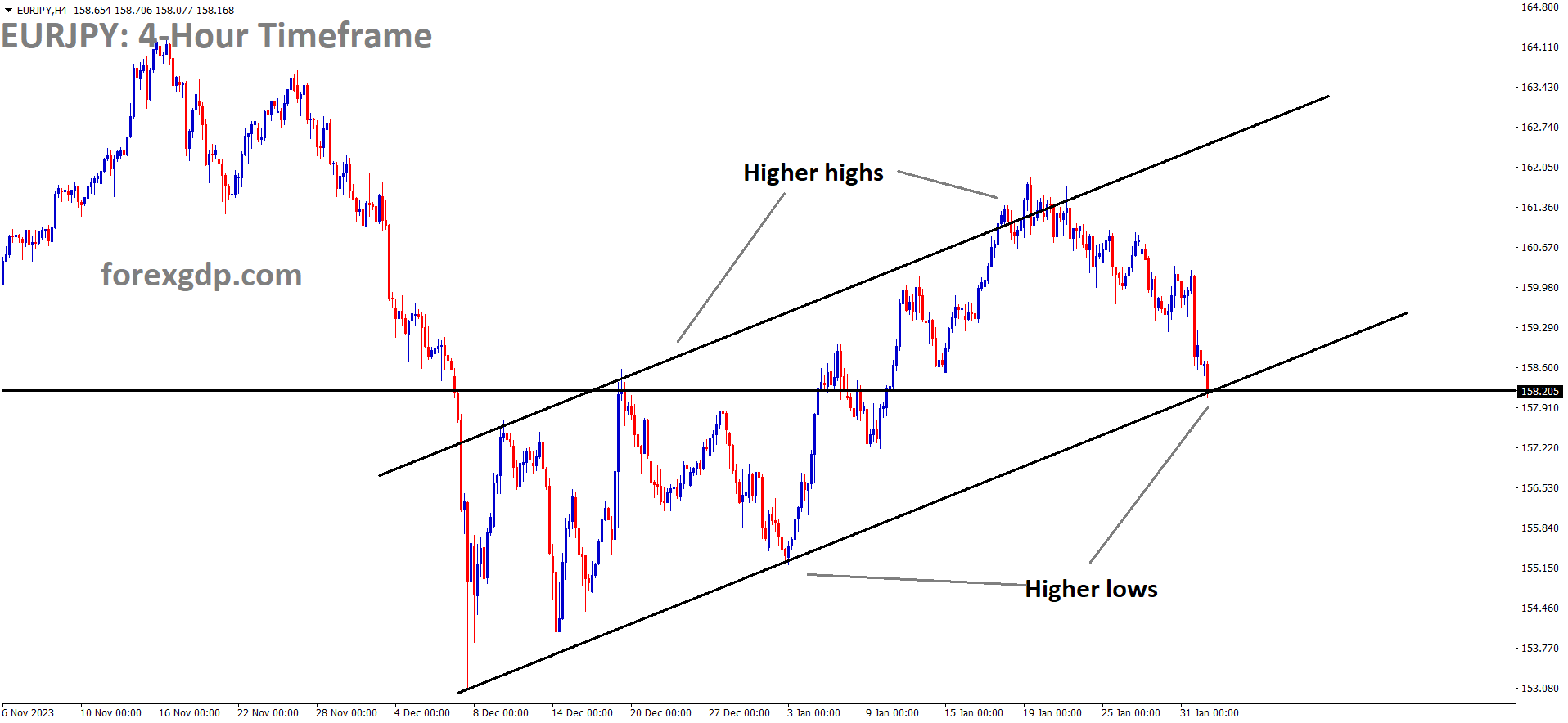

EURJPY Analysis:

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

In the final week of January, foreign bond investment in Japan amounted to Yen 382.9 billion, showing a notable decrease from the Yen 1.689 trillion recorded in the first week of the same month. This data reflects a consistent trend of strengthening the Yen, propelled by the influx of funds from both stock and foreign bond investors into Japan over recent months.

In the week ending January 26, foreign bond investment in Japan experienced a notable inflow of ¥382.9 billion, marking a significant turnaround from the previous week’s outflows of ¥-43.5 billion. However, it remains considerably lower than the peak inflows seen in January, which reached ¥1.689 trillion. During the same period, foreign investment in Japanese stocks also rebounded, with an inflow of ¥720.3 billion compared to the previous week’s ¥287 billion. Despite this rebound, it falls well short of the peak inflows recorded in January at ¥1.202 trillion.

The data on securities investment, as reported by the Ministry of Finance, pertains to bonds issued in the domestic market by foreign entities in the domestic currency. This report provides insights into the financial flows from the public sector, excluding the Bank of Japan. The net data reflects the difference between capital inflows and outflows, with a positive difference indicating net sales of foreign securities by residents and a negative difference indicating net purchases of foreign securities by residents.

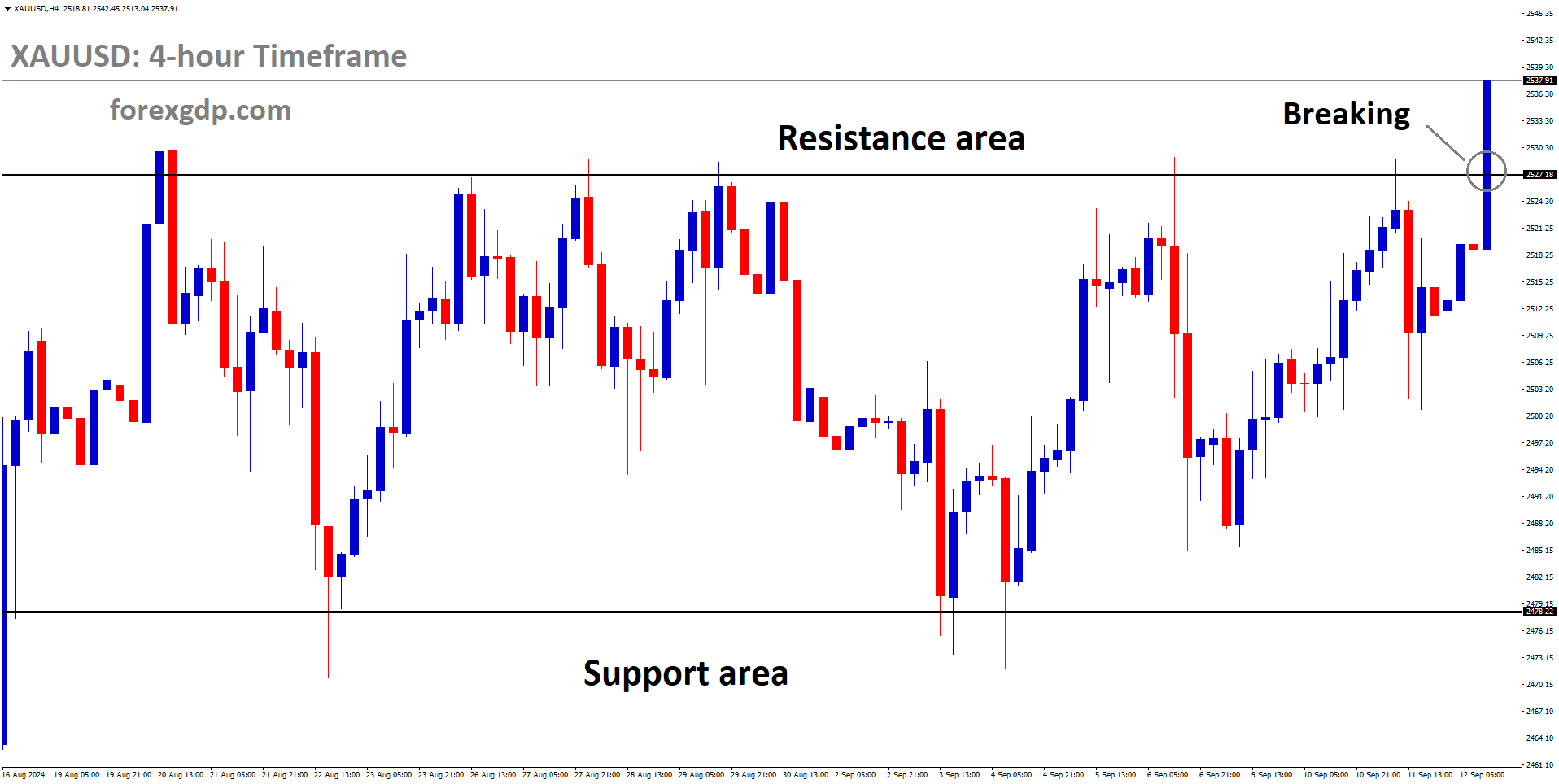

XAUUSD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices exhibited minimal movement in response to the Federal Reserve’s decision to maintain interest rates at their current levels. The possibility of near-term rate cuts seemed to dissipate following Federal Reserve Chairman Powell’s recent speech.

In January, US private employers added 107K jobs, falling short of expectations set at 145K and trailing behind the prior reading of 158K. This slowdown in labor demand is likely to fuel speculations about potential early rate cuts by the Federal Reserve, heightening market volatility as investors anticipate the central bank’s monetary policy decision. The Fed is widely anticipated to maintain the current interest rates, marking the fourth consecutive meeting with a steady rate decision. Attention will be focused on the Fed’s guidance regarding future interest rates, which could significantly influence FX market movements.

Despite diminishing price pressures, further quantitative tightening is not anticipated from the Fed. Consequently, market participants will closely monitor when and at what pace the central bank might initiate interest rate reductions. Some investors are anticipating the onset of rate cuts as early as May. While previous guidance from the Fed suggested a potential 75 basis points reduction in interest rates for 2024, individual policymakers have cautioned against lowering interest rates too soon, emphasizing the need to wait until there is confidence in achieving the Fed’s 2% inflation target. In response to downbeat private employment data, the Gold price surged to $2,050, while the US Dollar Index witnessed a sharp decline. Investors are now eagerly awaiting the Federal Reserve’s monetary policy decision and its potential implications for the interest rate outlook. According to the CME Fedwatch tool, traders are expecting the Fed to maintain interest rates within the 5.25-5.50% range, marking the fourth consecutive instance of interest rate stability.

Persistently diminishing price pressures within the US economy have deterred Fed policymakers from pursuing further interest rate hikes. Thus, the forthcoming statements from Fed policymakers regarding the interest rate outlook are of paramount importance, given the prevailing expectation of a stable monetary policy decision. In the previous monetary policy meeting, both Fed Chair Jerome Powell and the Summary of Economic Projections indicated the potential for a 75-basis point reduction in interest rates for 2024, driving increased demand for riskier assets. This guidance initially sparked expectations of rate cuts starting in March but faced resistance due to resilient US economic data. Investors will be closely monitoring how the Fed adjusts its guidance for three rate cuts in upcoming policy meetings.

The CME Fedwatch tool currently suggests that the Fed may initiate rate cuts in May. The absence of dovish signals during the May meeting could exert downward pressure on Gold prices while boosting the appeal of the US Dollar. Looking ahead, various US economic indicators are slated for release this week, keeping investors occupied. On the global front, geopolitical tensions continue to provide support for gold prices, with US President Joe Biden pledging retaliation for aerial drone attacks on US bases near northeastern Jordan.

XAGUSD Analysis:

XAGUSD Silver price has broken the Ascending channel in downside

FED Governor Jerome Powell addressed the issue of inflation, emphasizing that it is closely monitored, and there is transparency in the records. He clarified that when inflation trends lower, the FED responds with rate cuts, while higher inflation readings lead to rate hikes. In the most recent decision, the FED maintained interest rates at a steady 5.25%-5.50%.

Federal Reserve Chairman Jerome Powell elucidated the rationale behind keeping the policy rate, specifically the federal funds rate, unchanged within the range of 5.25% to 5.5%. During the post-meeting press conference, he addressed questions and elaborated on the central bank’s stance. Powell refrained from specifying a specific timeframe for the duration of low inflation required to instill confidence. The emphasis was on the importance of accurate data and ensuring a sustainable approach in achieving their objectives regarding inflation. He assured that the Federal Reserve would not keep its confidence in inflation a secret.

If there were indications of robust inflationary trends, they would proceed cautiously and possibly delay any actions. Conversely, if inflation data exceeded expectations positively, their approach would be different. Powell emphasized that the concern primarily lies in persistent declines in inflation. The central bank is more focused on this aspect rather than the fear of an overly robust economic growth that could lead to inflation resurgence. The central bank’s primary goal is to manage inflation effectively while considering the broader economic context.

USDCAD Analysis:

USDCAD is moving in the Box pattern and the market has rebounded from the support area of the pattern

Canada’s GDP data for November has been revealed, showing growth of 0.20%, surpassing the expected 0.10%. This positive economic news prompted a rise in the Canadian Dollar following the data release.

The Canadian Dollar made gains on Wednesday following an unexpected positive development in Canadian Gross Domestic Product. This marked the first growth in GDP since May, providing a boost to the currency. Meanwhile, the Federal Reserve’s decision to maintain its primary policy rate, as anticipated by the markets, was accompanied by remarks from Fed Chairman Jerome Powell, emphasizing the need for stronger indications of US inflation remaining at the Fed’s 2% target. Despite the uncertainties highlighted by Powell regarding economic data, risk appetite in the markets waned as the possibility of a March rate cut by the Fed seemed increasingly unlikely.

Canada’s monthly GDP exhibited growth for the first time in seven months, leading to a recovery in the Canadian Dollar against the US Dollar. However, it’s worth noting that the CAD still faces challenges against other major currencies. Traders will closely watch Thursday’s release of the January Canadian Purchasing Managers Index for the manufacturing sector, once the impact of the Fed’s rate decision subsides. The November GDP data for Canada, which surprised with a 0.2% month-on-month increase versus the expected 0.1%, marked the first positive growth in seven months after revisions.

S&P Global’s Canadian Manufacturing PMI for January is set to be unveiled on Thursday, with the previous month’s PMI in contraction territory at 45.4. Powell’s explanation for the policy rate’s maintenance has left investors eager for hints about potential future rate cuts by the Fed. Rate swap bets on a Fed rate cut in March surged earlier on Wednesday, now indicating a 65% chance of at least a 25 basis point rate reduction by the March 20 meeting. According to the CME FedWatch Tool, swap rates are pricing in less than a 5% chance of no rate cuts from the Fed by May.

The US Dollar faced a setback after the release of ADP Employment Change figures, which fell well short of expectations, along with an unexpected decline in the Chicago PMI. January’s ADP Employment Change came in at 107K, compared to the forecast of 145K, and December’s figure of 158K. Additionally, January’s Chicago PMI dropped to 46.0, contrary to the expected uptick to 48.0, as recorded in December at 47.2. It’s worth noting that ADP figures are prone to revisions and have a mixed track record in predicting the US Nonfarm Payrolls data scheduled for release on Friday. Since 2007, ADP Employment Change has seen revisions in all months except one.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

SNB Chairman Thomas Jordan anticipates that inflation expectations in the Swiss zone are poised to rise, driven by the VAT tax and escalating electricity prices. However, Swiss Retail Sales witnessed a decline of 0.80% in the month of December.

Despite a brief dip in the US Dollar against the Swiss Franc on Wednesday, which was primarily triggered by disappointing US employment data, a rebound quickly followed. Federal Reserve Chair Jerome Powell’s announcement that a rate cut in the upcoming March meeting was unlikely further contributed to the Dollar’s recovery. This decision was largely anticipated, given the Fed’s commitment to maintaining existing interest rates. Powell emphasized the persistent presence of elevated inflation levels and highlighted the robust growth in economic activity. Additionally, the Federal Open Market Committee made it clear that they would not consider lowering the target range until they had greater confidence in inflation moving steadily toward the 2.0 percent target. Although inflation has eased over the past year, it still remains elevated, and the statement omitted any mention of additional policy tightening.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower low area of the channel

Swiss National Bank Chairman Thomas Jordan recently spoke at a Business Journalists club, where he discussed the expectations for inflation. He noted that inflation is anticipated to increase due to the Value Added Tax hike and rising electricity prices, but it is expected to stay below the 2.0% mark. This is the baseline scenario, and the projection for this year suggests that inflation will, on average, remain below the 2.0% threshold. Consensus among experts is that the Swiss National Bank will implement its first rate cut in September 2024.

In terms of economic indicators, Swiss Real Retail Sales disappointed by declining 0.8% in December, falling short of the anticipated 0.9% growth. November saw a 1.5% drop in Swiss consumer demand. However, there was a positive development in Gross Domestic Product for November, which rose by 0.2% compared to the previous flat 0.0% figure, surpassing the market consensus of 0.1% growth. Looking ahead, traders will keep a close eye on the S&P Global Manufacturing PMI and SVME – Purchasing Managers’ Index scheduled for release on Thursday.

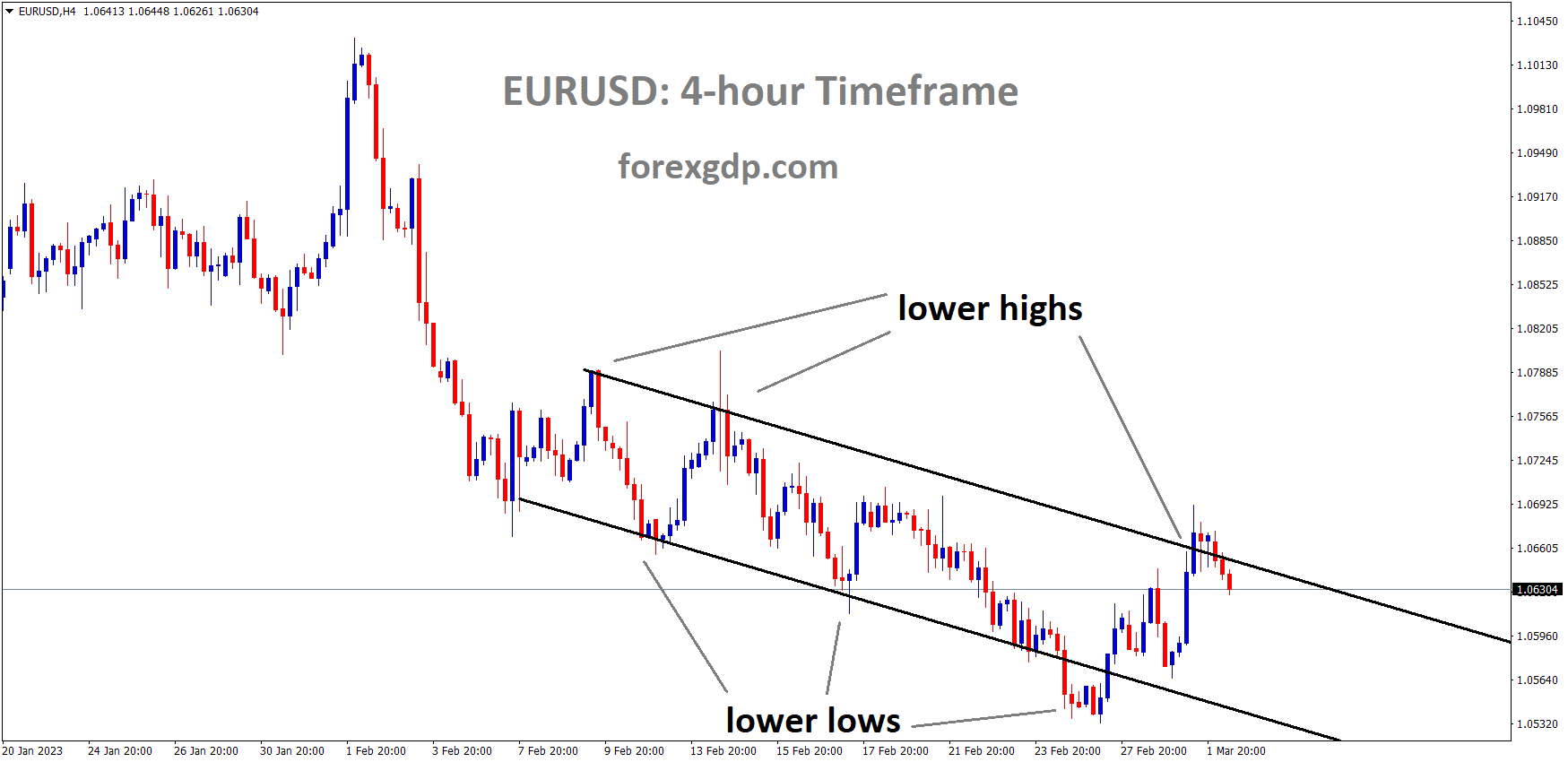

EURUSD Analysis:

EURUSD has broken the Ascending channel in downside

The German Consumer Price Index data for January has been released, revealing a lower-than-expected figure of 2.9% compared to the forecasted 3.2%. This unexpected outcome exerted downward pressure on the Euro against the US Dollar in the market. The European Central Bank now finds itself with increased flexibility and potential options for near-term rate cuts in response to the economic slowdown.

European equities faced a day of modest declines, exemplified by Germany’s DAX index slipping by four-tenths of a percent. The dip was influenced by a mix of factors, notably, Germany’s Consumer Price Index inflation missing expectations. Additionally, concerns arose among investors due to rising expenses linked to the development of AI-based hardware and software products. These increased costs were not necessarily translating into the expected revenue growth, despite the surging demand for AI-powered products.

Germany’s annualized CPI inflation figure for January came in lower than anticipated, registering at 2.9% year-on-year, compared to the forecasted 3.2%. This represented a further drop from the previous period’s 3.8%. This unexpected decrease in inflation within Germany, a key economic powerhouse in the Euro area, has prompted speculation of more significant and swifter rate cuts from the European Central Bank. Market participants are now positioning themselves for the release of the broader EU Harmonized Index of Consumer Prices on Thursday, where pan-EU annualized HICP inflation for January is forecasted to dip from 2.9% to 2.8% year-on-year. Predictions in money markets have increased the anticipated rate cuts by the ECB to 150 basis points by the end of 2024, up from the previous estimate of 140 basis points.

Meanwhile, Europe is grappling with mounting protests in the agriculture sector as farmers unite to demand greater support from European government agencies. Their grievances include seeking a reduction in planned subsidy cuts and calling for stricter tariff controls on imports from Ukraine. The diversion of Ukraine’s agriculture products into European markets following the Russian invasion last year has disrupted traditional export routes. In another sector, the automotive and car parts industry experienced a setback this week due to a European Union Commission raid on tire manufacturers. Major tire producers, including Pirelli, Michelin, and Nokian, were subjected to investigations by EU antitrust regulators on allegations of cartel-like behavior. The EU Commission is expected to provide updates once their initial investigation concludes. The tire manufacturers are accused of price fixing and colluding to the detriment of European consumers.

In the tech realm, major giants such as Microsoft and Alphabet have reported substantial revenue growth in AI-related sectors. However, the burgeoning costs associated with supplying AI-focused chips and software are outpacing income gains, dampening investor sentiment. The semiconductor industry is also grappling with sluggish demand for non-AI chips.

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has reached the lower low area of the channel

In its latest meeting, the Bank of England is anticipated to maintain the current interest rate at 5.25%. This decision comes as a response to a recent uptick in December’s inflation figures, driven in part by escalating geopolitical tensions. Consequently, the GBP is gaining ground against other currencies in the market.

The Bank of England is gearing up for its first policy meeting of 2024, which is poised to have a significant impact on the future trajectory of the Pound Sterling. On this Super Thursday, the central bank is expected to maintain its current policy rate, marking the fourth consecutive meeting without any changes. The benchmark interest rate is anticipated to remain steady at 5.25%. Alongside the rate decision, the BoE will release its Monetary Policy Report , followed by a press conference hosted by Governor Andrew Bailey. Market expectations are currently factoring in approximately 100 basis points of rate cuts throughout the year, starting in the second quarter. Despite these expectations, the BoE is likely to maintain a firm stance, emphasizing the prospect of higher interest rates persisting for an extended period. Several factors support this view, including a surprising increase in December’s annual inflation rate, growing tensions in the Middle East, and the impending impact of rising borrowing costs. These factors could deter policymakers from embracing an earlier shift towards a dovish policy stance. BoE Governor Andrew Bailey, during his testimony before the UK Treasury Select Committee in January, highlighted disruptions in shipping traffic, leading to increased shipping prices and costs. Initially, this could pose challenges in the realm of monetary policy and potentially spill over into financial stability concerns. Deputy Governor Sarah Breeden echoed the sentiment after the December policy meeting, stressing the importance of a prolonged period of restrictive monetary policy. As of now, UK annual inflation stands at 4.0%, rebounding from a low of 3.9% in November. Additionally, the UK’s Gross Domestic Product showed growth of 0.3% in November, following a 0.3% decline in October. The S&P Global UK Preliminary Services PMI also surged to an eight-month high of 53.80 in January, up from 53.40 in December, indicating ongoing economic recovery. These positive indicators provide the BoE with the rationale to keep interest rates elevated for an extended duration.

In addition to the rate decision, the focus will be on the central bank’s updated forecasts for inflation and economic growth. Governor Bailey’s press conference will offer valuable insights into the BoE’s timing for any potential policy shift. In the November MPR, the BoE Monetary Policy Committee projected flat GDP growth in the fourth quarter of 2023 and the subsequent quarters, with a likelihood of CPI inflation returning to the 2% target by 2025. Analysts from Goldman Sachs anticipate upward revisions to growth projections for 2025 and 2026. They predict a downward revision in near-term inflation forecasts due to softer consumption data and lower energy prices. This could pave the way for rate cuts by spring, with the first 25 basis point cut expected in May, followed by similar cuts in subsequent meetings until the Bank Rate reaches 3.0% in May 2025. An earlier rate cut in March is not entirely ruled out, especially if disinflation coincides with deteriorating economic conditions.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

China’s Vice Finance Minister, Wang Dongwei, has announced plans to introduce additional stimulus measures in the upcoming Government Budget for the current year. Notably, the tax cuts implemented in 2023 had a financial impact of approximately 2.2 trillion yuan. As a result of these measures, there is an optimistic outlook for fiscal revenues in 2024. Wang Dongwei has also highlighted the potential benefits of considering structural tax cuts in 2024, specifically targeting the technology and manufacturing sectors. This statement underscores China’s commitment to supporting key sectors of its economy and fostering growth, indicating a proactive approach to fiscal policies that adapt to the evolving needs of its industries.

China’s Vice Finance Minister, Wang Dongwei, made a noteworthy announcement on Thursday, highlighting the government’s plans to strategically boost investments within the central government budget. Notably, the tax and fee cuts in 2023 amounted to a substantial 2.2 trillion yuan, providing a substantial financial relief. Looking ahead to the financial landscape of 2024, there’s an optimistic outlook for fiscal revenue, with expectations of continued recovery. The commitment to maintaining a certain level of fiscal spending throughout the year underscores the government’s efforts to bolster domestic demand through fiscal policy.

In parallel, another official from the finance ministry echoed the government’s commitment to economic growth. They mentioned the upcoming implementation of structural tax cuts in 2024, with a particular focus on supporting technological innovation and the manufacturing sector. This strategic move aligns with China’s broader economic agenda and its aspiration to drive growth in these vital sectors.

In January, the Australian Judo Bank Manufacturing Purchasing Managers’ Index revealed that business growth persisted at a modest pace, registering a reading of 50.1 on a month-on-month basis. This represented an improvement from December’s 47.6 figure, a reflection of Australia’s ongoing transition toward a soft landing economic scenario. While there was a slight adjustment from the preliminary 50.3 reading, the seasonally-adjusted Manufacturing PMI still hovers above the critical 50.0 level, indicating a positive territory. However, Australia’s overall economic conditions have been trending softer, leading to a slowdown in various aspects of business activity, including new orders and exports.

According to Warren Hogan, Chief Economic Advisor at Judo Bank, the recent uptick in output and new orders during January has alleviated concerns about a looming manufacturing sector recession. Moreover, business confidence among manufacturers improved in January, with the future output index reaching its highest point since August of the previous year. The Manufacturing Purchasing Managers Index is a valuable leading indicator that assesses business activity within Australia’s manufacturing sector. Published monthly by Judo Bank and S&P Global, this data is derived from surveys of senior executives at private-sector companies. The responses collected provide insights into any changes occurring in the current month compared to the previous month, offering a glimpse into evolving trends in key economic indicators such as Gross Domestic Product, industrial production, employment, and inflation. The index’s range extends from 0 to 100, where a level of 50.0 signifies no change compared to the previous month. A reading above 50 indicates overall expansion in the manufacturing sector, which is typically viewed as a positive sign for the Australian Dollar. Conversely, a reading below 50 suggests a decline in activity among goods producers, often regarded as bearish for the AUD.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The New Zealand Dollar saw an upward surge following the release of China’s Caixin Manufacturing PMI data for January, which came in at 50.8, surpassing the anticipated 50.6 figure.

The recently unveiled data for China’s Caixin Manufacturing Purchasing Managers’ Index for January provides an insightful view into the state of the country’s manufacturing sector. In this latest release, the PMI is reported at 50.8, marking a noteworthy figure that reflects the sector’s performance. To put this into context, it’s essential to compare it with the previous month’s data. In December, the Caixin Manufacturing PMI was also recorded at 50.8, indicating that the level of expansion has remained consistent between these two months. This consistency in PMI figures suggests a certain level of stability or continuity in China’s manufacturing activities during this period.

A PMI reading above 50 generally signifies expansion in the manufacturing sector, whereas a reading below 50 indicates contraction. Therefore, with a January PMI of 50.8, it is evident that the Chinese manufacturing sector maintained its growth momentum, albeit at a similar level as seen in December.

This data can have far-reaching implications for financial markets, trade dynamics, and the broader global economy, as China is a major player in the world of manufacturing and international trade. The PMI serves as a crucial barometer of economic health, offering insights into production levels, employment, new orders, and overall business sentiment within the manufacturing sector. Market participants and analysts closely monitor these PMI figures, as they can provide early signals of potential shifts in economic trends. In this case, the January PMI reading suggests that the manufacturing sector in China is holding its ground, which can have implications for various stakeholders, from investors and policymakers to businesses engaged in international trade with China.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/