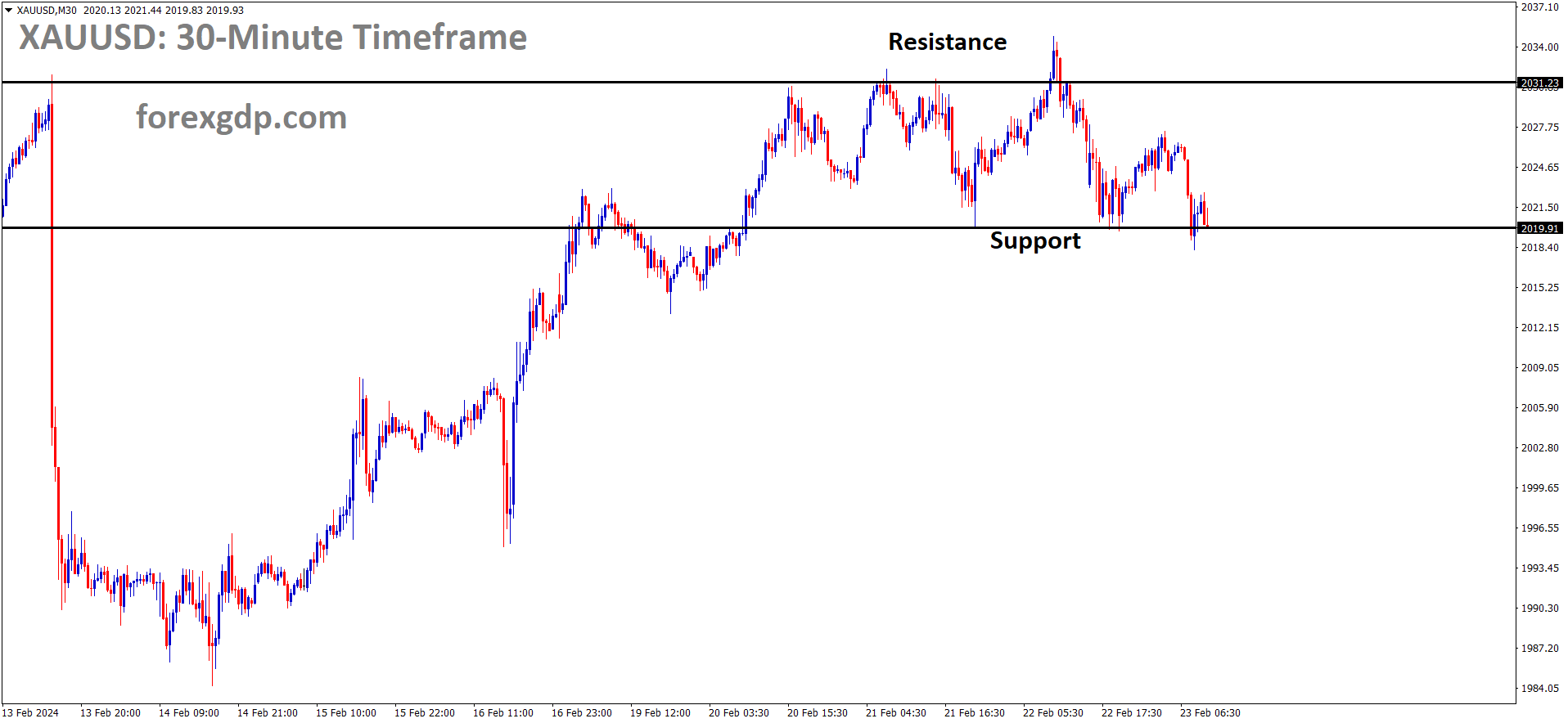

XAUUSD Gold price is moving in the Box pattern and the market has reached the support area of the pattern

GOLD – Retreats from Two-Week High Amid Hawkish Fed Signals

Gold prices traded higher due to Geopolitical tensions surrounding the Red Sea. Israel doing more conflicts with Gaza for retaliation purposes.

The US Dollar moved flat after the FED Hawkish meeting minutes this week.

Gold Slips from Two-Week High Amid Hawkish Fed Signals and Risk-On Sentiment

On Friday, gold faces renewed selling pressure in the European session, retracting from its nearly two-week peak reached the day before. Investor sentiment leans towards a belief that the Federal Reserve (Fed) will maintain higher interest rates for an extended period, given persistent inflation and a resilient economy. Hawkish comments from influential Fed officials reinforce this stance, supporting elevated US Treasury bond yields and undermining the non-yielding gold.

Additionally, the ongoing risk-on rally in global equity markets diverts capital away from the safe-haven appeal of gold. However, the potential for heightened geopolitical tensions in the Middle East poses a counterbalance. Despite the US Dollar’s struggles to attract significant buying, it may help limit the downside for gold. Overall, while facing headwinds, XAU/USD appears poised for modest weekly gains.

Market Recap: Gold Price Slips Amid Delayed Fed Rate Cut Expectations and Elevated US Bond Yields

In the aftermath of intensified conflict in the Middle East and continued pressure on the safe-haven appeal of gold, the yellow metal faces a decline. Despite the US Dollar’s struggle to capitalize on recent gains, the Federal Reserve’s hawkish outlook remains a potential limitation on gold’s upward trajectory.

The latest FOMC meeting minutes reveal uncertainty about the duration of current borrowing costs to combat inflation. Fed Vice Chair Philip Jefferson suggests a possible rate cut later this year, contingent on a thorough evaluation of economic indicators. Philadelphia Fed President Patrick Harker acknowledges the proximity to rate cuts but deems an imminent move unlikely to avoid reigniting inflation.

Fed Governor Lisa Cook advocates against rate reductions, citing a potentially bumpy path to the 2% inflation goal. Christopher Waller recommends delaying rate cuts to assess whether January’s inflation surge is a temporary hurdle.

Market sentiment, reflected in the CME Group’s FedWatch Tool, indicates a 30% chance of rate cuts in May and a 66% probability for the June FOMC policy meeting. Positive labor market data and steady yields on the 10-year US government bond provide support for the US Dollar, curbing gold’s gains amid prevailing risk-on sentiment.

Additionally, encouraging flash Eurozone PMI prints in February contribute to investor confidence, further restraining the upside for XAU/USD.

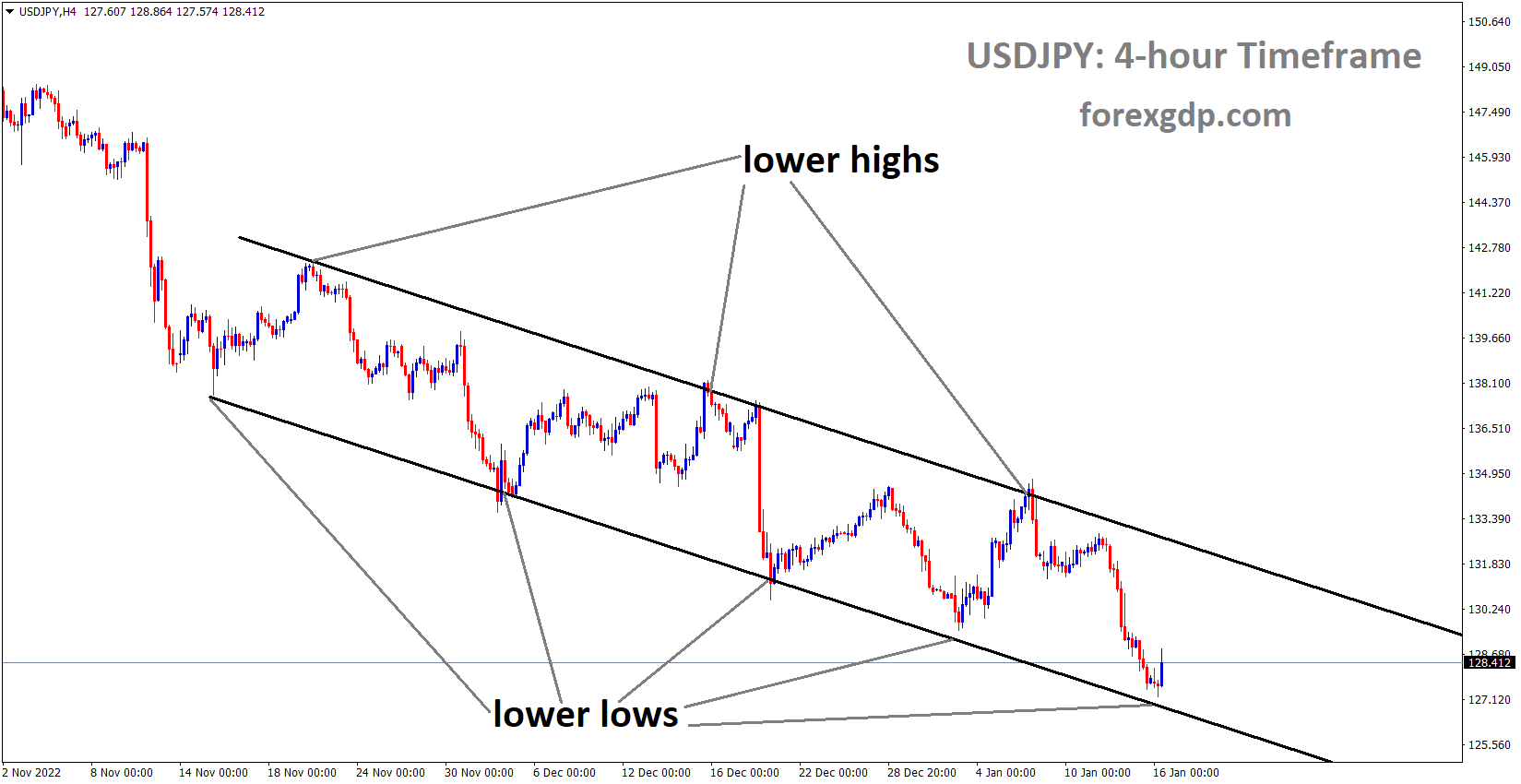

USDJPY – JPY Eyes Multi-Month Low on Diminished BoJ Pivot Bets

The investor’s expectations of the Bank of Japan’s rising interest rates faded after the recession in the Japanese economy published last week. So JPY weakness persists in the market against counter pairs.

USDJPY is moving in an Uptrend line and the market has rebounded from the higher low area of the trend line

JPY Continues Defensive Stance Amid Reduced BoJ Pivot Expectations

For the third consecutive day, the Japanese Yen (JPY) hovers near its weekly low against the US Dollar. Investors have tempered their anticipation of the Bank of Japan (BoJ) ending negative interest rates in the wake of unexpected recession data in Japan last week. The prevailing risk-on sentiment and the Japanese government’s warnings of potential market intervention in the face of JPY weakness contribute to the Yen’s vulnerability.

Despite a recent rebound from a nearly three-week low, the US Dollar (USD) struggles to gain significant momentum. In the absence of relevant macro data, this adds to the challenges of any substantial upward movement in the USD/JPY pair.

Market Digest: Japanese Yen Faces Pressure from Multiple Sources

Last week’s data revealing an unexpected recession in Japan’s economy dashes hopes of a Bank of Japan exit from ultra-easy policies, weighing down the Japanese Yen. Additionally, positive Eurozone flash PMI prints boost investor sentiment and add to the downward pressure on the safe-haven JPY.

Ongoing attacks on commercial vessels in the Red Sea by Yemen’s Houthi rebels, despite US and UK strikes, raise the risk of military action, providing some support to the JPY.

Warnings from Japan’s Ministry of Finance and the BoJ about closely monitoring the exchange rate and intervening if necessary contribute to cautious trading in the face of potential weakness in the Yen.

Federal Reserve signals, including FOMC meeting minutes and comments from influential officials like Vice Chair Philip Jefferson, President Patrick Harker, Governor Lisa Cook, and Governor Christopher Waller, reinforce the commitment to keeping interest rates higher for a longer duration. The CME FedWatch Tool reflects a reduced market expectation, with about a 30% chance of rate cuts in May.

Furthermore, positive indicators from the US labor market contribute to the support of elevated US Treasury bond yields, favoring USD bulls and potentially propelling the USD/JPY pair higher. The US Department of Labor’s report on a decline in unemployment insurance benefit applications to 201K adds to signs of strength in the labor market.

GBPUSD – Gains Modestly Above Mid-1.2600s on Mixed US Data

UK Preliminary Manufacturing PMI came at 47.1 in February month versus 47.0 in the previous reading. Services PMI data came at 54.3 with no change from the previous reading. Composite PMI reading at 53.3 versus 52.9 previous reading.

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

US Jobless Claims Drop, Manufacturing PMI Improves; Investors Delay Rate Cut Expectations

US Initial Jobless Claims for the week ending February 17 decrease to 201K, suggesting a robust labor market and potentially influencing the Fed to postpone rate cuts. Continuing Claims also fall to 1.862M, below expectations.

Investor expectations for the first Fed rate cut shift from May to June, driven by a strong job market and higher-than-expected inflation in January.

US Manufacturing PMI rises to 51.5 in February, the highest in 16 months, beating estimates. However, Services PMI eases to 51.3, below the expected 52.00.

In the UK, preliminary Manufacturing PMI for February is at 47.1 (missing expectations), Services PMI remains at 54, and Composite PMI is at 53.3 (beating expectations).

Investors await Fed Christopher J. Waller’s speech for further guidance, with the US GDP Annualized for Q4 scheduled for release next week.

USD INDEX – Fed’s Waller: No Urgency for US Interest Rate Cuts

Fed Governor Christopher Waller said there is no rush to do rate cuts in the monetary policy. If rate cuts are done then inflation prices will shoot up in the economy. Inflation has to cool down in the market, rate cuts will be seen in the second half of 2024.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

Federal Reserve Governor Christopher Waller, speaking on Thursday, emphasized the lack of urgency in initiating interest rate cuts. He stressed the importance of further evidence supporting the cooling of inflation before considering support for rate reductions. Key points from his statements include:

– Policy decisions and the frequency of rate cuts hinge on incoming data.

– The Committee can afford to wait longer before implementing monetary policy easing.

– Waller expressed puzzlement at the narrative suggesting that delaying cuts could risk causing a recession.

– He debunked the supposed asymmetry of lagged effects between rate hikes and cuts, asserting it lacks support from any model.

– Unless a major economic shock occurs, delaying cuts by a few months is not expected to significantly impact the economy in the near term.

– Waller cautioned against cutting rates too soon, as it could jeopardize progress on inflation and pose considerable harm to the economy.

– Recent data since his last speech on January 16 reinforced the need to verify sustained inflation progress from the latter half of 2023.

– He reiterated that there is no rush to initiate interest rate cuts.

– Waller pointed out the uncertainty surrounding the recent Consumer Price Index (CPI) report, questioning whether it was driven by seasonal factors or signals a stickier inflation that is harder to bring down to the target.

– He emphasized the need for more data to determine if the January CPI was more noise than signal.

– The strength in output and employment growth lessens the urgency for policy easing.

– Waller expects policy easing later in the year, acknowledging recent data validating Chair Powell’s careful risk management approach.

– He highlighted the lower risk of waiting a little longer to ease compared to the risk of acting too soon.

– Several indicators suggest a slowdown in growth, with the latest data on job openings and quits indicating potential labor market moderation.

– Waller presented estimates for January core Personal Consumption Expenditures (PCE) based on CPI and PPI data.

– He expressed comfort in knowing that the progress made in inflation was real and not a mirage.

– Waller still sees wage growth as somewhat elevated to achieve the 2% inflation goal.

– He is monitoring housing costs to see if they continue to run higher than expected.

– Considering all inflation aspects, Waller sees predominantly upside risks to the expectation that inflation will move toward the 2% goal.

– He emphasized the need for a couple more months of inflation data to ascertain if January was a fluke and to confirm the trajectory toward price stability.

– Waller stated that there are currently no indications of an imminent recession.

EURCHF – Swiss Inflation Slows, Paving Way for Earlier SNB Cuts

The Swiss CPI data for January came at 1.3% from 1.7% forecasted. SNB said inflation rates are within in range of 0-2%. Rate cuts more probably happen in the September 2024 meeting if the inflation range is sustained at this level.

EURCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Swiss Inflation Eases, Paving the Way for Possible Earlier SNB Rate Cuts

In January, Swiss inflation unexpectedly slowed, suggesting the potential for earlier rate cuts by the Swiss National Bank (SNB). Consumer prices rose 1.3%, falling short of the economists’ prediction of 1.7%. The core gauge, excluding volatile elements, also decelerated to 1.2%. The surprise drop is notable, given the regulated nature of many Swiss prices and recent increases in electricity costs and value-added tax.

SNB President Thomas Jordan, while expecting inflation to approach the upper limit of the target range (0-2%), has maintained the possibility of rate cuts. Economists initially anticipated rate cuts in September, but the weaker-than-expected reading raises the likelihood of an earlier move, with some analysts considering June. The Swiss central bank convenes quarterly, unlike its major counterparts.

The strong franc acts as a buffer against higher imported price growth, with the currency dipping after the inflation data. The potential for a rate cut in March is now higher, although uncertainties persist, considering the resilience of growth in the US and Switzerland.

In contrast, euro area prices rose 2.8% annually in January, while Swiss inflation, based on the EU’s harmonized measure, stood at 1.5%.

EURJPY Surges Above 163.00 on German GDP Data

German GDP for the fourth quarter came at -0.30% QoQ and -0.20% in YoY in line with expected readings. ECB Meeting minutes for the January month outcome is Rate cuts will be delayed until at least the first quarter of 2024. Due to slower wage growth and rate cuts, the possibility comes only after the inflation has slowed down.

EURJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

EUR/JPY Climbs Above 163.00 on In-Line German GDP Data

The pair sees a 0.12% daily gain, trading near 163.07, following Germany’s Q4 GDP contraction that matched market expectations. Eurozone Composite PMI for February outperformed consensus forecasts, with services improving, but manufacturing remained in deep contraction.

ECB’s January meeting minutes indicate a cautious shift in inflation assessment, making spring rate cuts unlikely. Japanese authorities’ verbal intervention aims to limit JPY downside, and Middle East tensions may act as a headwind for EUR/JPY.

Upcoming focus on German IFO survey and ECB’s Schnabel speech, with Japanese National CPI scheduled for next week.

AUDUSD – AUD Extends Winning Streak on Higher ASX 200; USD Stable

The Australian Dollar moved higher after the Domestic data from the private sector was boosted in the last 5 months. Mainly Services sector expansion in the Australian Economy is support for the Aussie Dollar. RBA rate cut hopes vanished after the RBA meeting minutes outcome this week.

AUDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

AUD Gets Boost from Growing Private Sector Activity in February, Driven by Services Sector Expansion; Market Sentiment Favors No Immediate Rate Cuts after RBA Meeting Minutes

USD Strengthens on Positive US Employment Data, Mixed PMI Indicators, and Hawkish Fed Comments

Daily Digest Market Movers: Australian Dollar Gains on Improved PMI and Wage Index

– Judo Bank Australia Composite PMI rises to 51.8 in February, marking the first month of expansion in the private sector after five months of contraction.

– Judo Bank Australia Services PMI increases to 52.8, while Manufacturing PMI falls to 47.7 due to a significant drop in new orders.

– Australian Wage Price Index grows by 0.9% QoQ in Q4, below the previous rise of 1.3%, but rises by 4.2% YoY, surpassing market expectations.

– Westpac Leading Index declines by 0.1% in January.

– RBA’s Meeting Minutes reveal deliberation on the possibility of a 25 bps rate hike or keeping rates unchanged, with a cautious approach to another rate hike.

– S&P’s analysis suggests that inflation is expected to continue cooling, with no anticipated changes to monetary policy in 2024, predicting a 25 bps rate reduction in June.

– Richmond Federal Reserve Bank President Thomas Barkin notes the US still has “ways to go” for a soft landing, emphasizing positive trends in inflation and employment data.

– Federal Reserve Governor Christopher J. Waller states that policy easing and rate cuts will depend on incoming data, with a willingness to wait before considering monetary policy easing.

– Philadelphia Fed President Patrick T. Harker sees no urgency for rate cuts and emphasizes data-driven future Fed actions, with no forecast for a rate cut in May.

– Federal Reserve Governor Lisa D. Cook acknowledges risks in better balance, preferring confidence in inflation convergence before initiating rate cuts.

– S&P Global US Services PMI records 51.3 in February, below expectations, while US Manufacturing PMI improves to 51.5, exceeding expectations.

– US Composite PMI declines to 51.4 in February.

– US Initial Jobless Claims drop to 201K, beating market expectations.

– Existing Home Sales Change (MoM) rises by 3.1% in January, rebounding from the previous decline.

NZDUSD – Set to Rise in Q2 – ING

ING Analysts said RBNZ soon do rate cuts in the near-term meeting. NZ Dollar may be going slower than the Australian Dollar’s performance if rate cuts are done from RBNZ. NZ Dollar may be rebound in the Second quarter of 2024.

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

NZD/USD Moves with Policy Expectations, ING Analyzes Kiwi’s Outlook

RBNZ to Ease Hawkish Stance

Amid the global central bank landscape, the credibility of RBNZ’s tightening bias diminishes, prompting an expected softening in the hawkish narrative during the February meeting.

NZD Might Lag Behind AUD Due to Priced-in RBNZ Cuts

Despite expectations of RBNZ cuts affecting the New Zealand Dollar’s performance relative to the Australian Dollar, NZD/USD appears poised for an upward trend from Q2 onwards.

USDCAD – Falters on US PMIs; Canadian Retail Sales Complicate Picture

Canadian retail sales rose to 0.90% in December month versus the 0.80% forecasted. The Canadian Dollar moved higher after the data came. Excluding the Auto sector, retail sales show 0.60% missing 0.70% but came above the previous reading of -0.40%.

USDCAD is moving in ascending triangle pattern and the market has reached the higher low area of the pattern

Canada’s Retail Sales Show Mixed Results; Focus Shifts to Friday’s Fed Monetary Policy Report

Retail sales volumes in Canada, excluding automobiles, fall below expectations. Attention turns to the Federal Reserve’s Monetary Policy Report on Friday, with minimal expectations for significant content after the recent release of the Fed’s meeting minutes on Wednesday.

Daily Digest Market Movers: USD/CAD Reacts to Varied Data Prints

– Canadian Retail Sales in December rise 0.9%, exceeding the forecast of 0.8% and rebounding from the previous month’s 0.0%.

– Canadian Retail Sales excluding Autos increase by 0.6%, missing the 0.7% forecast but recovering from the previous -0.4%.

– US Initial Jobless Claims for the week ended February 16 decline to 201K, well below the 4-week average of 215.25K and the forecast of 218K.

– S&P Global PMIs for February in the US show mixed results, with Services underperforming (51.3 MoM) and Manufacturing gaining ground (51.5).

– US Existing Home Sales in January rise, with Existing Home Sales Change climbing 3.1% MoM, recovering from the previous -0.8% (revised up from -1.0%).

XTIUSD – WTI Holds at $78.00 Amid Geopolitical Risks and EIA Inventory Buildup

Israel attacked Hezbollah targets on Lebanon’s side and Yemen Houthi rebels attacked in Redsea areas. This conflict causes oil prices to move higher due to disruptions of Oil supply fears in the economy.

XTIUSD Oil price is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern.

WTI Prices Rise on EIA Report and Middle East Tensions, but Face Possible Cap from Fed’s Interest Rate Narrative

Crude oil inventory increased by 3.514 million barrels, below forecasts, according to the Energy Information Administration. Geopolitical tensions in the Middle East, including Israeli attacks in Lebanon and Houthi actions in the Red Sea, raise concerns about crude supply disruptions, supporting WTI prices.

However, the prospect of the Fed and major central banks maintaining a ‘higher for longer’ interest rate stance may limit WTI’s upside. The FOMC Minutes highlighted the need for more evidence before considering rate cuts, with warnings about the risks of moving too quickly. Higher interest rates could dampen WTI prices due to reduced demand with increased costs.

Upcoming events, including German GDP for Q4 and Fed Christopher J. Waller’s speech, will be monitored by oil traders. The release of US GDP for Q4 next week could significantly impact USD-denominated WTI prices, offering trading opportunities for oil traders.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/