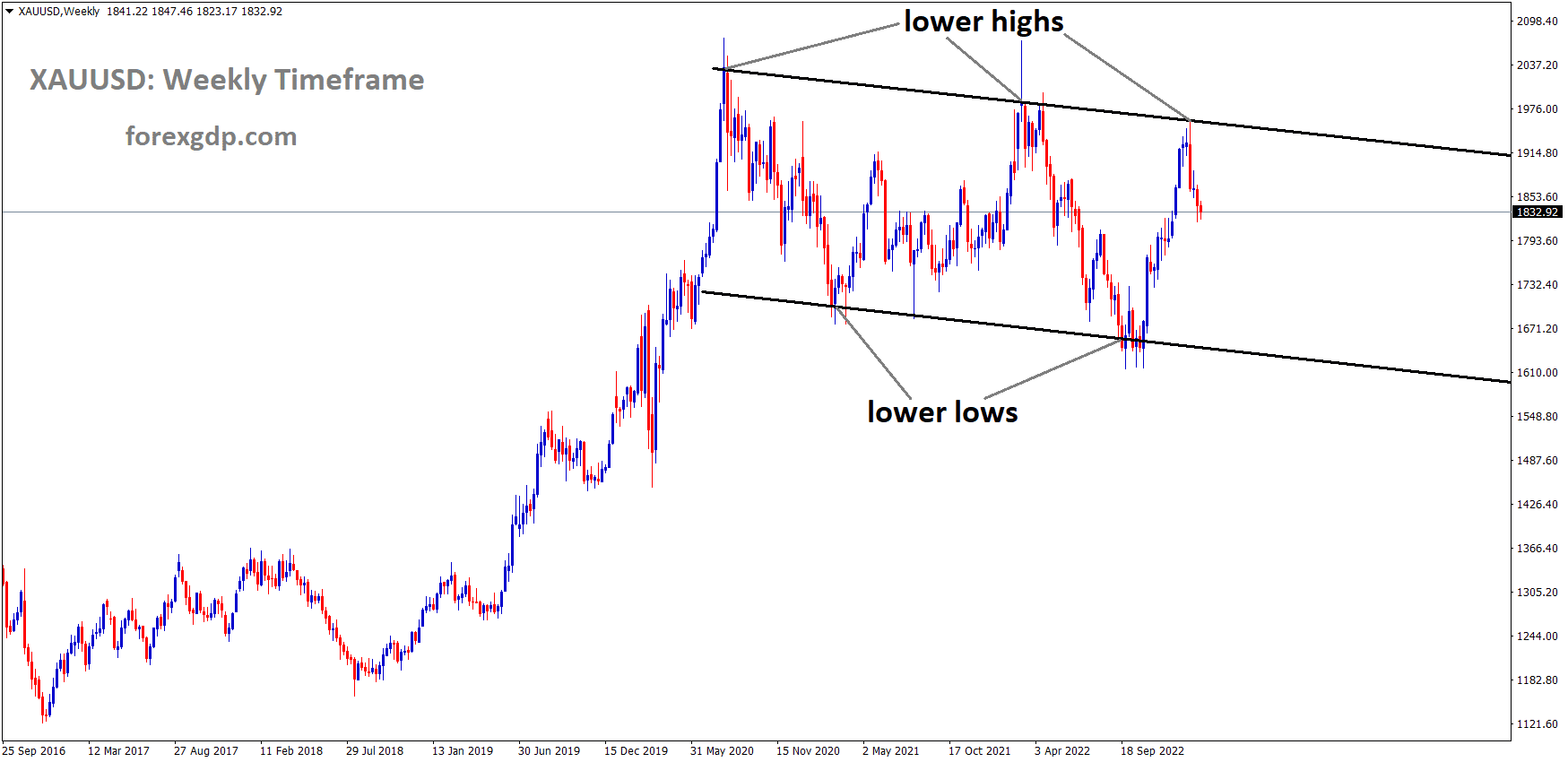

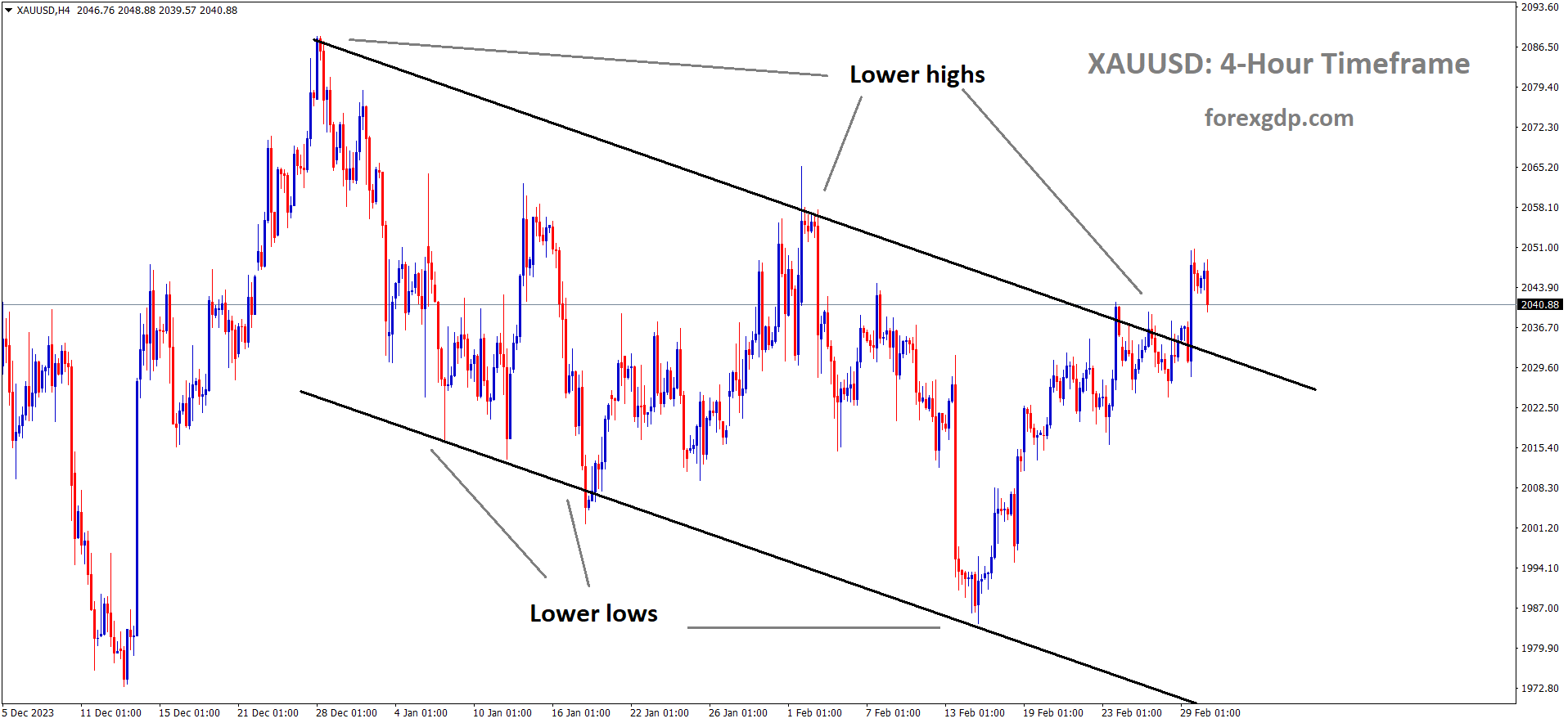

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

XAUUSD – Gold Price Near One-Month Peak, Poised for Further Climb

Gold prices moved higher after the US PCE Index data came at lower than expected last day. US Dollar weakness positively moved Gold. Today US ISM Manufacturing PMI is scheduled.

Gold Price Rises for Third Day, Nears One-Month Peak Amid Easing US Inflation. Market Awaits Fed Rate Cut Signals, US Macro Data. Fed Officials Reaffirm Potential Rate Cuts, US Treasury Yields Near Highs.

GBPUSD – GBP Seeks Clarity on BoE Rate Cut Timing

The UK Economy will grow in 2024 from foreign investments if interest rates are maintained at the same rate. The economists expected rate cuts from BoE in the August month until the Economy grows further with the neutral rates.

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

Pound Sterling Temporarily Supported Amid US Inflation Concerns:

The Pound Sterling sees a brief respite in Friday’s European session, recovering from Thursday’s negative close. However, the GBP/USD pair faces potential pressure as higher monthly US core Personal Consumption Expenditure Price Index (PCE) data for January reduces expectations of Federal Reserve (Fed) rate cuts in the June policy meeting.

In January, US monthly core inflation data increased by 0.4%, surpassing December’s revised down 0.1%. Despite expectations for a more significant growth in price pressures, the momentum does not align with the Fed’s objective of achieving a 2% inflation target.

The Pound Sterling remains on edge due to a slightly uncertain market mood. In the broader context, GBP may benefit from expectations that the Bank of England (BoE) will initiate interest rate reductions after the Fed.

Investors anticipate rate cuts from both the BoE and the Fed in August and June, respectively. This alignment in policy easing is expected to temporarily reduce the divergence between the central banks, potentially attracting higher foreign inflows to the Pound Sterling.

In today’s session, focus is on the UK’s S&P Global/CIPS Manufacturing PMI and the US ISM Manufacturing PMI for February. The UK Manufacturing PMI is expected to remain unchanged at 47.1, while the US Manufacturing PMI is anticipated to rise to 49.5 from 49.1 in January.

Market Movers in the Daily Digest:

– Pound Sterling finds interim support near 1.2600 after a sharp sell-off, but the downside remains favored in a cautious market.

– The US Dollar Index remains firm above 104.00 against six major currencies.

– The market sentiment is uncertain as US core PCE Price Index data for January aligns with expectations.

– The annual core PCE Price Index is at the lowest in three years at 2.8%, meeting market expectations.

– The probability of a rate cut in June remains at 52%, according to the CME FedWatch tool.

Regarding the Bank of England (BoE), investors are seeking clarity on the timing of interest rate reductions. A Reuters poll indicates expectations for a rate cut in the third quarter of this year, with a slim majority favoring August. BoE policymakers are cautious, considering rate cuts only after gaining confidence in inflation reaching the 2% target. Concerns persist about the pace of wage growth and service inflation, which currently exceed the necessary levels for sustainable inflation return to the 2% target.

USDJPY – BoJ’s Ueda: Recent Recession a Rebound from Strong Prior Quarters

The Bank of Japan Governor Kazhao Ueda said Japan is in a Recession mode after the strong quarters pick up, Wage growth must increase in the near term, and Companies showing interest in hiking wages. Once wages increase then Inflation will pick up. Inflation can sustain at the 2.0% target level and we need a soft landing of interest rates with inflation to Wage growth.

USDJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

BoJ’s Ueda: Skepticism on 2% Inflation, Sees Recent Recession as Rebound

BoJ Governor Kazuo Ueda shared insights, expressing skepticism about Japanese inflation sustaining 2% growth. Highlights include noting the recent recession as a rebound from robust quarters, observing faster-paced inflation easing, and anticipating a tailwind from wage negotiations. He believes Japan’s economy will gradually recover, maintaining the view that sustained 2% inflation is not foreseeable yet.

Ueda emphasizes the importance of considering wage talks and firm hearings collectively for a comprehensive assessment. Despite Q4 negative GDP, he expects a consumption recovery post-COVID reopening and sees a soft landing in the global economy, aligning with January projections.

USDCAD – Dips to Around 1.3560 on Elevated Crude Oil Prices, Focus on US Manufacturing PMI

The Canadian GDP for Q4 2023 came at 1.0% versus 0.80% expected and a -0.50% decline in Q3. So the Canadian Dollar appreciated against counter pairs yesterday.

USDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

Furthermore, the positive performance of Canada’s Gross Domestic Product (GDP) Annualized may have lent support to the Canadian Dollar (CAD). The data revealed a growth of 1.0% in the fourth quarter of 2023, surpassing market expectations of a 0.8% increase and reversing the previous decline of 0.5%. Additionally, the GDP (QoQ) rose by 0.2%, contrasting with the earlier decrease of 0.1%.

The West Texas Intermediate (WTI) oil price has exhibited improvement, reaching close to $78.10. Speculation about a potential extension of supply cuts by the Organization of the Petroleum Exporting Countries and its allies (OPEC+) and ongoing tensions in the Middle East contribute to this positive trend.

Recent economic data, including GDP figures and the US Personal Consumption Expenditures – Price Index from the United States (US), has caused a delay in market expectations for the Federal Reserve’s (Fed) initial rate cut. This delay has provided support for the US Dollar (USD). Investors are now eagerly awaiting the final US S&P Global Manufacturing PMI for February, scheduled for release on Friday.

As per the CME FedWatch Tool, the probability of rate cuts in March stands at 3.0%, with expectations decreasing to 23.1% in May and rising to 52.2% in June. Atlanta Fed President Raphael W. Bostic remarked that recent inflation data suggests a challenging path toward achieving the central bank’s 2% inflation target. Furthermore, Chicago Fed President Austan Dean Goolsbee anticipates the first-rate cuts later this year but refrains from specifying the exact timeline.

USD INDEX – Today’s Forex: USD Gains Consolidate, PMI and Euro Inflation Data Awaited

US Core PCE Index data for January is 2.4% which is lowered from 2.6% printed in December month. Personal consumption and Expenditure declines make the FED make rate cuts in the near term. So the US Dollar moved down against counter pairs yesterday.

USD Index is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Friday Focus: DXY Consolidation, Eyes on ISM PMI and Eurostat HICP. Fed Speeches, US PCE Data, and Core PCE Index in Review.

US Treasury Yield Retreats Below 4.3% on PCE Data, USD Rebounds; AUD/USD Rebounds on Improved PMI Data. USD/JPY Climbs Above 150.00 After BoJ Comments; EUR/USD Stabilizes Above 1.0800. Gold Gains Momentum, Hits $2,050 Amid Retreating US Yields.

EURCHF – Swiss Economy Expanded at the Conclusion of 2023 Amid Tourism Recovery

The Swiss Economy grew by 0.30% which is supported by Tourism and Household spending. But 2023 has 1.3% growth which is a slowdown from 2.5% in 2022. The data is supportive for SNB to rate cuts in the near term rather than the long-term expected, So the Swiss Franc moved down after the data was published.

EURCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Switzerland’s economy expanded at a modest pace in the final quarter of 2023, driven by a rebounding tourism sector and increased household spending, despite ongoing challenges in the industrial sector.

According to data released by the State Secretariat for Economic Affairs (Seco) on Thursday, the country’s gross domestic product (GDP) grew by 0.3% for the second consecutive quarter in the October to December period. However, the overall annual growth for the year slowed to 1.3%, down from 2.5% in 2022.

Household consumption saw a 0.3% increase on a quarterly basis, aided by a decrease in inflation. However, overall domestic demand dipped by 0.3%, primarily impacted by a 2.5% decline in equipment and software investment.

Swiss manufacturing faced challenges, with output decreasing by 0.1% on a quarterly basis. The decline was driven by the nation’s vital chemical and pharmaceutical industry, where output fell by 2.3% due to declining exports.

On a positive note, the services sector played a supportive role in the economy. The recovery in tourism continued, with the accommodation and food services sector growing by 3.5%, especially as the ski season commenced. Financial services also saw growth, expanding by 1.0%.

Looking ahead, economic growth is expected to pick up in the coming quarters, particularly with the prospect of lower central-bank interest rates. Adrian Prettejohn, Europe economist at Capital Economics, anticipates that the Swiss National Bank will ease monetary policy in March, providing support for investment and potentially lowering the franc, which could boost exports further.

EURGBP – Gains Above Mid-0.8500s, Watches Eurozone HICP Data

The Euro currency moved higher against Counter pairs after ECB president Lagarde said near-term rate cuts may not happen easily. So March month Rate cut has faded, and now expectations going to the June month meeting for further rate cuts. Eurozone CPI data is scheduled today.

EURGBP is moving in the Box pattern and the market has rebounded from the support area of the pattern

During the early European trading hours on Friday, the EUR/GBP pair maintained a positive stance above the mid-0.8500s. Investors are eagerly anticipating the release of the Eurozone Harmonized Index of Consumer Prices (HICP) for potential market-moving cues. As of now, the cross is trading near 0.8560, showing a marginal decline of 0.01% for the day.

The European Central Bank (ECB) is expected to continue its policy normalization process. ECB President Christine Lagarde is likely to dismiss the possibility of rate cuts during the March meeting. However, financial markets speculate that the first rate cuts may occur in the June meeting. In February, market expectations for policy easing underwent a repricing, shifting from around 150 basis points (bps) of anticipated rate cuts to 87 bps. The consensus now points towards a 25 bps cut in June, with a total of 75 bps expected for the year.

On the other hand, Bank of England (BoE) Deputy Governor Dave Ramsden expressed his intention to observe how long inflation will remain elevated before contemplating a shift in monetary policy. BoE policymakers have resisted market expectations for early interest rate cuts, providing support to the Pound Sterling (GBP) and limiting the downside for the EUR/GBP cross.

Looking forward, market participants are keenly observing the Eurozone Harmonized Index of Consumer Prices (HICP) scheduled for release on Friday. Additionally, attention is directed towards the HCOB Manufacturing PMI reports from Italy, France, and Germany. Later in the day, BoE’s Huw Pill is scheduled to speak, adding to the potential market impact. The focus is set to shift to the ECB interest rate decision in the upcoming week, with expectations that this event could induce volatility in the market. Traders are on the lookout for potential trading opportunities around the EUR/GBP cross.

GBPAUD – General: China’s Commerce Ministry Pledges Import Expansion for Domestic Demand

China Commerce Ministry said China is facing severe, complex Domestic demand from the External Environment. So We need to support import companies to increase the import products in 2024

GBPAUD is moving in an Ascending trend line and the market has rebounded from the higher low area of the trend line

China’s Commerce Ministry Addresses Post-Conference:

China’s trade confronts a complex, severe, and uncertain external environment.

The Ministry pledges to assist companies in exploring markets for orders and is committed to expanding imports to ensure domestic demand.

AUDUSD – AUD Consolidates, Eyes on US Manufacturing PMI amid Stable USD

The Australian Retail sales data for January came at 1.1% versus the 1.5% expected and it is an increased reading from the decline of 2.7%.

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Private expenditure improved and Judo Manufacturing’s PMI reading improved in January month.

On Friday, the Australian Dollar (AUD) maintained its positive momentum, driven by the S&P/ASX 200 Index reaching new record highs and gains in Wall Street overnight. Despite this upward trend, the AUD/USD pair experienced a retracement on Thursday, attributed to the strengthening of the US Dollar following the release of the Federal Reserve’s preferred inflation gauge, the US Personal Consumption Expenditures – Price Index, which met expectations.

The AUD received a boost following the release of Australia’s Retail Sales and Private Capital Expenditure data on Thursday. Additionally, the Judo Bank Manufacturing PMI indicated a slight improvement in Australia’s manufacturing sector, with the February reading rising to 47.8 from 47.7 in the previous period.

In contrast, the US Dollar Index showed a slight decline despite the increase in US Treasury yields. The delay in expectations for the Federal Reserve’s first rate cut, influenced by recent Gross Domestic Product data from the United States, provided support to the Greenback. Investors are now focusing on the final US S&P Global Manufacturing PMI for February, scheduled for release on Friday.

The Daily Digest highlighted key movements in the market, noting that Australian Retail Sales (MoM) grew by 1.1% in January, slightly below the expected 1.5%, but recovering from the previous decline of 2.7%. Australian Private Capital Expenditure improved by 0.8% in the fourth quarter of 2023, exceeding the expected 0.5% and the previous 0.6%. The Australian Monthly Consumer Price Index remained unchanged at 3.4% for January, falling below market expectations of 3.5%.

Concerns about Australia’s manufacturing sector were expressed by Warren Hogan, Chief Economist Advisor at Judo Bank, who noted a lack of growth, challenging the notion of a post-pandemic manufacturing revival. In China, the Manufacturing PMI met expectations at 49.1 in February, slightly lower than the previous reading of 49.2. The Non-manufacturing PMI improved to 51.4 from the prior 50.7, surpassing the expected reading of 50.8.

Statements from US Federal Reserve officials revealed varying perspectives. Atlanta Fed President Raphael W. Bostic highlighted challenges in achieving the central bank’s 2% inflation target. Chicago Fed President Austan Dean Goolsbee anticipated the possibility of the first rate cuts later this year. New York Federal Reserve (Fed) President John Williams acknowledged the need to cover some ground to reach the 2% inflation target and expressed the potential for interest rate cuts this year, contingent upon incoming data.

According to the CME FedWatch Tool, the probability of rate cuts in March stands at 3.0%, while the likelihood of cuts in May and June is estimated at 23.1% and 52.2%, respectively.

In terms of economic data, the US Personal Consumption Expenditure (PCE) Price Index grew by 2.4% YoY in January, meeting market expectations. The Core PCE (YoY), the Fed’s preferred inflation gauge, rose by 2.8%, aligning with the consensus. The preliminary US Gross Domestic Product Annualized grew by 3.2% in the fourth quarter of 2023, slightly below market expectations of remaining steady at 3.3%.

The preliminary US Gross Domestic Product Price Index (Q4) increased by 1.7%, exceeding the expected and previous rise of 1.5%. However, the US Housing Price Index (MoM) increased by 0.1% in December, falling short of the expected 0.3% and the previous 0.4%.

NZDUSD – Rises to Around 0.6090 as RBNZ Orr Emphasizes Need for Restrictive Policy

RBNZ Governor ORR spoke today showing a hawkish policy stance. Inflation remains elevated in the near term, So Policy standing at the current term. Policy gets Normal in 2025. But growth seen in 2024.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

NZD/USD Ends Four-Day Decline on RBNZ’s Orr Outlook:

NZD/USD halted its four-day downtrend after remarks from Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr on Friday. Orr indicated the central bank’s intention to initiate policy normalization in 2025, prompting the pair to rise, reaching nearly 0.6090 during the Asian session.

Governor Orr highlighted the economy’s progress as expected, noting a decline in inflation expectations. While inflation remains elevated, it shows a downward trajectory. Emphasizing the necessity for sustained restrictive monetary policy, Orr also expressed optimism for economic growth in 2024.

The US Dollar Index (DXY) is marginally lower, hovering around 104.10, despite improved US Treasury bond yields (4.63% for the 2-year and 4.25% for the 10-year bonds at the time of writing). However, the Federal Reserve’s delay in the first-rate cut, influenced by recent US Gross Domestic Product (GDP) data, has supported the US Dollar (USD).

The USD strengthened following the release of the Federal Reserve’s preferred inflation indicator, the US Personal Consumption Expenditures – Price Index, meeting expectations. Attention now turns to the final US S&P Global Manufacturing PMI for February, scheduled for release on Friday.

In January, the US Personal Consumption Expenditure (PCE) Price Index expanded by 2.4% YoY, slightly down from the previous 2.6%, aligning with market forecasts. On a monthly basis, the index rose by 0.3%, exceeding the prior 0.1% increase.

Simultaneously, the US Core PCE, the Federal Reserve’s preferred inflation measure, grew by 2.8% YoY, slightly lower than December’s 2.9%, meeting consensus expectations. On a monthly basis, the core PCE increased by 0.4%, surpassing the previous 0.1% rise.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/