XAUUSD Gold price has broken the Box pattern in upside

XAUUSD – Gold Price Primed to Rise on Increasing June Fed Rate Cut Expectations

Gold prices are moving higher after the expected hopes of FED side June rate cuts is possible from investors side. US CPI data is scheduled for tomorrow. May be higher inflation data will support USD against Gold.

Gold (XAU/USD) maintains a consolidative stance as the European session begins, staying below the recent peak achieved on Friday. Bullish activity appears hesitant amid overbought conditions on the daily chart and in anticipation of the upcoming release of US consumer inflation figures on Tuesday. The critical CPI report will significantly influence expectations regarding the Federal Reserve’s (Fed) rate-cut trajectory, impacting US Dollar (USD) demand and providing a new directional push for the non-yielding precious metal.

Growing consensus that the Fed will initiate rate cuts in June, supported by a rise in the US jobless rate to a two-year high in February, keeps USD bulls on the defensive and supports the Gold price. Additionally, a softer risk tone, geopolitical tensions, and concerns about a global economic slowdown contribute to limiting downside risks for the safe-haven metal. Consequently, the XAU/USD appears inclined to move upward, and any substantial corrective decline may be viewed as an opportunity for bullish traders.

Market Summary: Gold Price Supported by Fed Rate Cut Expectations and Risk Aversion

Friday’s data revealed a two-year high in the US unemployment rate, fueling expectations of a June rate cut by the Federal Reserve and propelling Gold to a new record high. The non-farm payroll (NFP) data indicated an addition of 275K jobs in February, surpassing the estimated 200K, though the previous month’s figure was revised down to 229K from the initially reported 353K.

Wage inflation, as measured by Average Hourly Earnings, increased by 4.3% on a yearly basis, falling short of market expectations and January’s growth of 4.4%. The likelihood of a May interest rate cut by the Fed rose to around 30% after the crucial jobs report, but the June policy meeting remains the most anticipated timing for such a move.

The yield on the 10-year US government bond declined to a more than one-month low, pulling the US Dollar to its lowest level since mid-January and benefiting the non-yielding metal. While a slight USD uptick led to intraday selling during the Asian session on Monday, expectations of an imminent shift in the Fed’s policy stance may help limit losses.

Geopolitical tensions, coupled with concerns about a global economic slowdown in 2024, are expected to drive flows toward the safe-haven XAU/USD, acting as a supportive factor. Investors are now awaiting the release of the latest US consumer inflation figures on Tuesday for fresh insights into the Fed’s rate-cut trajectory before positioning for the next directional move.

EURUSD – Strengthens in Mid-1.0900s, Focus on US and German CPI Data

ECB President Lagarde said rate cuts in the market only when inflation reading seen 2% target in the market. Euro zone Q4 GDP printed at 0.10% inline with expected rate. German CPI is waiting for schedule this week.

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

EUR/USD Maintains Positive Stance in Mid-1.0900s, Focus on US and German CPI Data

During early Asian trading hours on Monday, the EUR/USD pair remains in positive territory around the mid-1.0900s. The US February Nonfarm Payrolls data released on Friday indicated continued strength in the US labor market. The anticipation of the Federal Reserve (Fed) initiating the first rate cut in June has led to a decline in the US Dollar (USD) against the Euro (EUR). The pair is currently trading near 1.0942, marking a 0.06% gain on the day.

The US Bureau of Labor Statistics (BLS) reported an addition of 275,000 jobs in February, surpassing the previous month’s figure of 229,000 and exceeding the consensus estimate of 200,000. However, the Unemployment Rate in the US increased to a two-year high of 3.9% in February from 3.7% in January. Average Hourly Earnings, measuring wage growth, rose by 4.3% YoY in February, slightly below the previous reading of 4.4%. Fed Chair Powell, in remarks to the Senate Banking Committee, expressed the need for more confidence before considering a rate cut, indicating they are not far from that point.

On the Euro front, the European Central Bank (ECB) maintained record-high borrowing costs as expected. ECB President Lagarde adopted a cautious tone, highlighting the requirement for additional evidence before considering rate cuts. Eurostat’s report on Friday revealed that the Eurozone Gross Domestic Product (GDP) for Q4 2023 remained flat MoM and grew by 0.1% YoY.

Looking ahead, Tuesday will see the release of US and German CPI inflation data, while Thursday will bring attention to US Retail Sales. These events will likely influence Fed officials’ considerations regarding the timing of potential interest rate cuts. Traders will closely analyze the data for trading opportunities in the EUR/USD pair.

USDJPY – Japan Escapes Recession as Quarterly Economic Growth Revised Up

The Japan Q4 GDP data grew by 0.10% versus 0.30% expected and -0.70% decline in Q3. Japan economy avoided recession in 2024, due to companies spend more in Plants and Manufacturing equipment’s. This data makes Positive for BoJ to end negative rates in the March Month meeting is expected.

USDJPY has broken the Ascending channel in downside

Japan’s economy defies contraction as Q4 annualized growth reaches 0.4%, surpassing the initial estimate of a 0.4% decline, according to Monday’s government data. The revised gross domestic product (GDP) figure contrasts with economists’ median forecast of a 1.1% increase in a Reuters poll. This positive data prevents Japan, now the world’s fourth-largest economy behind Germany, from entering a technical recession, attributed to stronger-than-expected corporate spending on plants and equipment.

On a quarter-on-quarter basis, GDP shows a 0.1% growth, in contrast to the initial 0.1% drop and a median forecast of a 0.3% rise. Capital expenditure outperformed expectations with a 2.0% increase, surpassing the government’s preliminary announcement of a 0.1% decrease but falling short of the median market forecast of a 2.5% rise.

This upward revision coincides with market speculation that the Bank of Japan may abandon negative interest rates this month, fueled by recent hawkish comments from board members indicating progress toward the central bank’s 2% inflation target. The BOJ is set to conduct a two-day policy-setting meeting on March 18 and 19.

Despite the positive economic growth, private consumption, constituting about 60% of Japan’s economy, decreased by 0.3% in October to December, slightly worse than the initial estimate of a 0.2% drop. Additionally, real wages shrank for the 22nd consecutive month in January, and year-on-year household spending in the same month recorded the most significant decline in 35 months.

External demand maintained its contribution of 0.2 percentage points to real GDP, consistent with the preliminary reading.

AUDJPY – BoJ mulls ending yield control, shifting focus to JGB buying size — Jiji

The Bank of Japan will be end the Negative rates in near month and alternatively the JGB Bonds purchases have to increase in the Market. March 18-19 meeting may be BoJ said its announcement of ending negative rates.

AUDJPY is moving in an Ascending triangle pattern and the market has reaching the higher low area of the pattern

BoJ mulls ending yield curve control, shifting to pre-announced government bond purchases, according to Jiji Press. The new approach aims to normalize monetary policy, focusing on purchase volume rather than yield. Decisions expected after the March 19 policy meeting.

USD INDEX – US Dollar Struggles in Week’s Start

US Dollar struggling to rebound from lows after the mixed reading of Labor data last week, Unemployment rate rose to 3.9%, Wage inflation reading lower to 4.3%. Ahead of US CPI Data tomorrow, US Dollar will decide its direction based on inputs.

USD Index is moving in the Descending channel and the market has reached the lower low area of the channel

US Dollar (USD) Maintains Calm Start After Previous Week’s Significant Losses

The US Dollar (USD) starts the week on a subdued note following substantial losses against major counterparts last week. The USD Index, having experienced a decline of over 1% in the previous week, hovers just below 103.00, while the 10-year US Treasury bond yield remains above 4%. The economic calendar lacks high-tier data releases to kick off the week.

In Friday’s report, the US Bureau of Labor Statistics (BLS) revealed that Nonfarm Payrolls (NFP) increased by 275,000 in February, surpassing the market’s anticipated 200,000. However, this positive data failed to bolster the USD as the BLS also revised the January figure down from 353,000 to 229,000. Additional insights from the jobs report indicated a slight dip in annual wage inflation to 4.3%, an increase in the Unemployment Rate to 3.9% from 3.7%, and a steady Labor Force Participation rate at 62.5%.

USDCHF – Gains Modestly Below 0.8800, Eyes on US PPI Data

The Hamas Leader said Israel did not accepting to hold the war on Gaza, many bloodshed happening in Gaza. Russia is expected to war on Neighboring countries beyond Ukraine makes fears on the market. This two news may be lift the Swiss Franc against counter pairs.

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

Federal Reserve (Fed) Chair Jerome Powell conveyed in his semi-annual testimony last week that the US economy is robust. Powell mentioned that the Fed is nearing a point of having sufficient confidence in the downward trajectory of inflation to consider initiating interest rate cuts.

According to the CME FedWatch Tools, futures markets indicate a likelihood of around 70% that the Fed will commence cutting interest rates by mid-June. Additionally, market expectations suggest a potential full percentage point of rate reductions by the end of the year.

In the latest report from the US Labor Department on Friday, it was revealed that the US economy added 275,000 jobs in February, surpassing the January figure of 229,000 and exceeding the estimated 200,000. However, the Unemployment Rate in the US rose to 3.9% in February from 3.7% in January, marking its highest level in two years. The US wage growth, measured by Average Hourly Earnings, increased by 4.3% YoY in February, slightly below the previous reading of 4.4% and falling short of the market consensus of 4.4%.

On the Swiss front, ongoing geopolitical tensions in the Middle East and economic uncertainties in major countries may contribute to increased safe-haven demand, benefiting the Swiss Franc (CHF). In the Middle East, Hamas leader Ismail Haniyeh accused Israel on Sunday of hindering cease-fire talks and rejecting Hamas’ efforts to halt the violence in Gaza. Meanwhile, tensions are escalating in Russia and neighboring territories, leading to concerns about a potential escalation of conflict beyond Ukraine.

Traders are anticipated to closely monitor the US February Consumer Price Index (CPI) and Retail Sales, scheduled for release on Tuesday and Thursday, respectively. The headline CPI figure is expected to remain steady at 3.1% YoY in February, while Retail Sales are projected to improve to 0.7%. Market participants will use this data to inform their trading decisions, particularly around the USD/CHF pair.

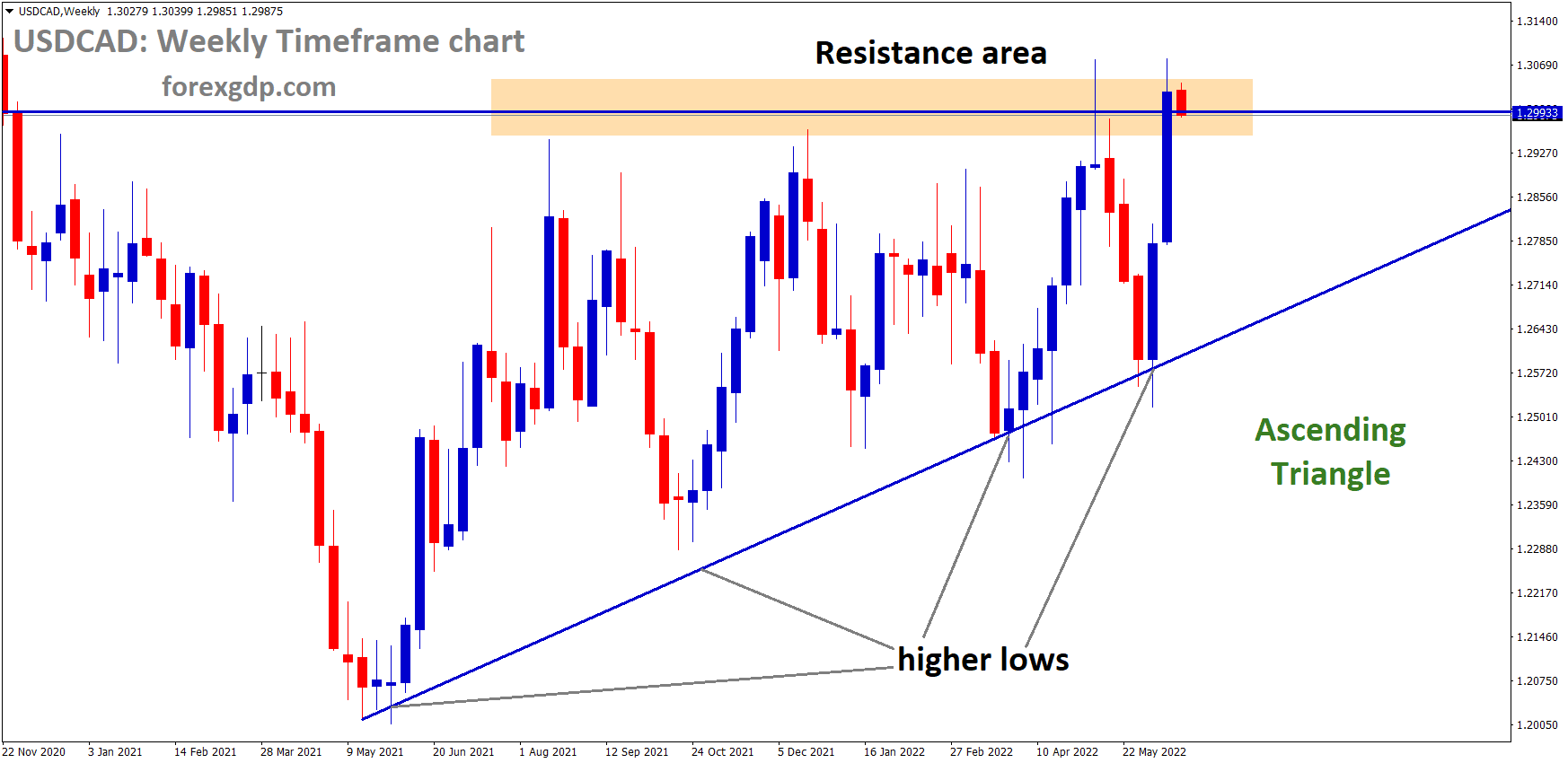

USDCAD – Steady Below 1.3500 Amid Lower Oil Prices and Weak USD Demand

The Canadian Dollar moved lowered after the Canadian Wage data slowdown and unemployment rate ticked up last week. Crudeoil Prices dropped due to slow demand of China in the last 2 months of 2024.

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

The currency pair faces conflicting influences, as lower crude oil prices weigh on the Canadian Dollar (CAD), while mixed economic data from both countries contribute to the overall uncertainty.

The decline in crude oil prices for the second consecutive day, driven by concerns over slowing demand in China and underwhelming import data, puts pressure on the commodity-linked Loonie. Simultaneously, mixed Chinese inflation data adds to market worries and dampens the outlook for oil supply, supporting the USD/CAD pair.

The Canadian Dollar experiences additional strain due to slowing domestic wage growth in February, reaching its lowest level since June, along with an increase in the unemployment rate. In contrast, the US jobs report reveals a spike in the jobless rate to a two-year high, reinforcing expectations that the Federal Reserve (Fed) might initiate interest rate cuts in June. However, this doesn’t contribute to the US Dollar’s (USD) recovery from its recent low, limiting the upside for the USD/CAD pair.

The complex fundamental landscape urges caution among bullish traders, emphasizing the need to carefully assess potential appreciating moves for the currency pair. With market participants awaiting the release of the latest US consumer inflation figures on Tuesday, the near-term trajectory of USD demand remains uncertain. The interplay of these factors, combined with ongoing dynamics in oil prices, will play a crucial role in shaping the USD/CAD pair’s next directional move.

GBPUSD – Holds Firm Around 1.2850, Anticipates UK Jobs Data

The UK Chancellor Jeremy Hunt presented Spring Budget in last week. The Outcome of Budget said UK Economy growth is stronger in 2024. This hint gives boost for GBP Pairs in the market.

GBPUSD has broken the Box pattern in upside

UK Labor data is scheduled this week for further movements in the market.

The US Dollar (USD) rebounded from intraday losses on Friday, gaining strength after the release of optimistic US Nonfarm Payrolls data. In February, Nonfarm Payrolls increased by 275K, surpassing January’s figure of 229K and exceeding expectations of 200K. However, the YoY growth in US Average Hourly Earnings was 4.3%, slightly below the estimated and previous reading of 4.4%. On a monthly basis, there was a 0.1% increase, lower than the anticipated 0.3% and the previous month’s 0.5%.

The GBP/USD pair maintains a positive outlook as the market widely anticipates the Federal Reserve (Fed) to cut interest rates before the Bank of England (BoE), potentially narrowing the policy gap between the two central banks. Federal Reserve Chair Jerome Powell, in his testimony before the US Congress last week, reiterated the central bank’s stance, hinting at potential cuts in borrowing costs later this year, contingent upon the inflation trajectory aligning with the Fed’s 2% target.

Last week, UK Chancellor of the Exchequer Jeremy Hunt presented the Spring Budget to Parliament, boosting positive sentiment surrounding the UK’s budget, especially with the Office for Budget Responsibility (OBR) forecasting stronger economic growth.

Market participants eagerly await UK employment data, including the ILO Unemployment Rate (3M) and Employment Change figures, scheduled for release on Tuesday. Additionally, Consumer Price Index data for February is on the radar for investors and analysts alike.

AUDUSD – Australian Dollar’s Winning Streak May Halt Before US CPI

The Australian Treasurer Jim Chalmers said Australia Government is going to Abolish 500 import goods tariffs from July 01, 2024. This removing tariffs helps the cost of Compliance goods to A$30 million and A$ 8.5 billion worth of Business will be increased in 2024.

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Australian Dollar (AUD) Ends Three-Day Winning Streak Amid Weaker US Dollar (USD)

The Australian Dollar (AUD) saw a decline on Monday, putting an end to its three-day winning streak, influenced by a weakened US Dollar (USD). The benchmark S&P/ASX 200 Index experienced a retreat from all-time highs at the beginning of the week, particularly in the materials and healthcare sectors, as investors opted to book profits. This drop followed a decline in technology stocks on Wall Street on Friday, contributing to the moderation of strength in the AUD/USD pair.

Last week, the Australian Dollar recorded a gain of 1.60% against the US Dollar, primarily driven by mounting expectations of earlier interest rate cuts by the US Federal Reserve (Fed) compared to other major central banks. However, the Australian economy’s fourth-quarter expansion fell below expectations, and the Trade Balance surplus also missed projections, providing a basis for the Reserve Bank of Australia (RBA) to potentially contemplate rate cuts in the near future.

Traders are approaching the US Consumer Price Index (CPI) data for February, scheduled for Tuesday, with caution as they await insights from a panel discussion at the AFR Business Summit in Sydney. During the discussion, Sarah Hunter, Assistant Governor (Economics) at the Reserve Bank of Australia, may offer valuable perspectives on domestic inflation trends. Additionally, market attention will focus on the release of the Australian Westpac Consumer Confidence for March.

Market Overview: Australian Dollar Weakens on Equity Market Decline

The Australian Trade Balance (MoM) for February showed an increased surplus of 11,027M, surpassing the prior figure of 10,743M. However, it fell short of market expectations, which anticipated a rise to 11,500M. The Australian Gross Domestic Product (GDP) grew by 0.2% QoQ in the fourth quarter of 2023, slightly below the market forecast of no change at 0.3%. Despite this, GDP (YoY) expanded by 1.5%, exceeding the expected 1.4% but falling short of the previous growth of 2.1%.

Australia’s Treasurer, Jim Chalmers, announced the government’s decision to eliminate nearly 500 import tariffs on various goods starting July 1, 2024. This move aims to reduce compliance costs for businesses, streamlining approximately A$8.5 billion worth of annual trade and saving over A$30 million in compliance costs annually.

In February, China’s Consumer Price Index (CPI) increased by 0.7% YoY, rebounding from a 0.8% decline in January and surpassing market expectations of a 0.3% rise. The month-on-month (MoM) CPI inflation also rose by 1.0%, up from a 0.3% increase in January and surpassing the market consensus of 0.7%. On the other hand, Chinese Producer Price Index (PPI) declined by 2.7% YoY in February, weaker than January’s 2.5% decline and below market expectations.

Federal Reserve (Fed) Chair Jerome Powell, in recent testimony before the US Congress, reaffirmed the central bank’s position. While hinting at potential rate cuts later this year, Powell emphasized that such actions would depend on the inflation trajectory aligning with the Fed’s 2% target. Cleveland Fed President Loretta Mester expressed concerns about potential inflation persistence throughout the year but suggested rate cuts later in the year if the economy aligns with forecasts.

According to the CME FedWatch Tool, the probability of a rate cut in March and May slightly decreased to 3.0% and 24.5%, respectively, while the likelihood of a 25 basis points rate cut increased to 57.2% for June.

In the US, Nonfarm Payrolls increased by 275K in February, surpassing both January’s figure of 229K and market expectations of 200K. Average Hourly Earnings (YoY) grew by 4.3%, slightly below the estimated and previous reading of 4.4%. On a monthly basis, there was a 0.1% increase, lower than the anticipated 0.3% and the previous month’s 0.5%.

US Initial Jobless Claims remained unchanged at 217K for the week ending on March 1, against the expected 215K. Nonfarm Productivity remained consistent at the growth of 3.2% in the fourth quarter of 2023, exceeding the market expectation of 3.1%. February’s US ADP Employment Change came in at 140K, slightly below the expected 150K but an improvement from 111K prior.

NZDUSD – Held Below 0.6200, Investors Anticipate US CPI Data

China CPI data for the month of February came at 0.70% it is higher than 0.30% expected and -0.80% fall in January data. This data boosted NZ Dollar against counter pairs in the markets.

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

NZD/USD Holds Below 0.6200 Amid Dovish USD Sentiment, Eyes on US CPI Data

During the Asian session on Monday, the NZD/USD pair remains constrained below the 0.6200 barrier. The downtick in the pair is expected to be limited as the US Dollar (USD) continues to face pressure following dovish comments from Federal Reserve (Fed) Chair Jerome Powell and mixed job data last week. At the current press time, NZD/USD is trading at 0.6172, reflecting a 0.03% decline on the day.

Powell’s recent indications of a potential easing of monetary policy in the near future, along with the market’s anticipation of rate cuts in June, have led to a 100 basis points (bps) pricing for total easing this year. This dovish sentiment exerts selling pressure on the Greenback, providing support to the NZD/USD pair.

Conversely, the signal of an upward trend in China’s main inflation gauge supports the New Zealand Dollar (NZD) as a China-proxy currency. The Chinese Consumer Price Index (CPI) rose by 0.7% YoY in February, rebounding from a 0.8% decline in January and surpassing the estimated 0.3% increase.

Looking ahead, the US February Consumer Price Index (CPI) is scheduled for release on Tuesday. The headline CPI figure is expected to maintain stability at 3.1% YoY, while the Core CPI is projected to ease to 3.7% YoY. Additionally, US Retail Sales data on Thursday is anticipated to improve to 0.7%. Better-than-expected data may strengthen the USD and limit the upside potential for the NZD/USD pair.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/