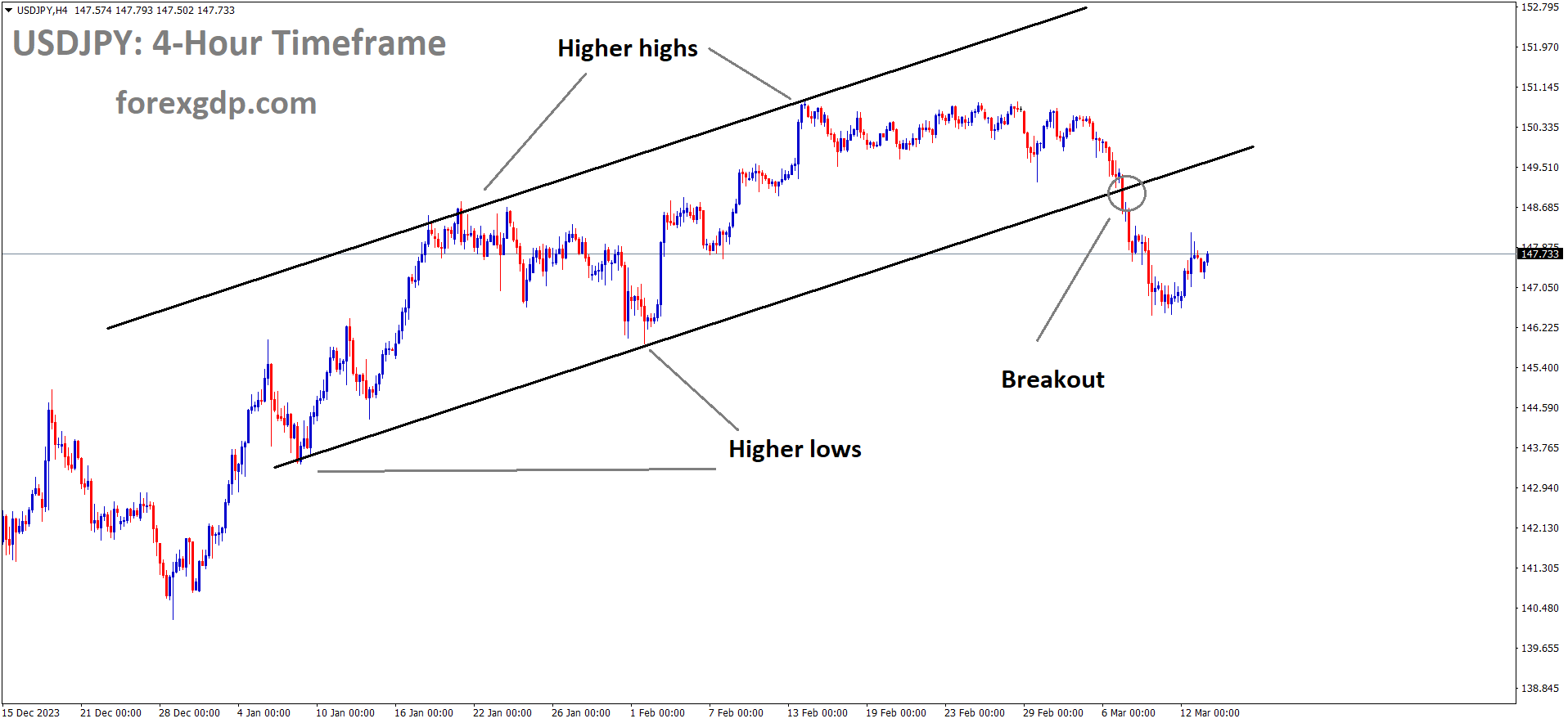

USDJPY has broken the Ascending channel in downside

USDJPY – BoJ’s Ueda to Analyze Wage Talk Outcome for Policy

The BoJ Governor Ueda said we will see whether Wage inflation driven cycle in the economy or not after the companies agreed the Employees pay hike today. We will carefully exit from Stimulus and Negative rates once the real wage to inflation higher in the economy is seen.

After the Japanese wage negotiations, Bank of Japan (BoJ) Governor Kazuo Ueda stated, “We will analyze the wage talk results and other relevant data to inform our policy decisions.”

Additional remarks:

– We will consider adjustments to negative rates, Yield Curve Control (YCC), and other easing measures if we approach our inflation target.

– We need to assess whether a positive wage-inflation cycle is forming to determine if the conditions for ending stimulus are aligning.

– This year’s wage negotiations are crucial for determining the timing of stimulus exit.

– With unions seeking higher pay, we are observing many corporate offers coming in today and beyond.

XAUUSD – Gold Dips, Stabilizes Near $2,150.00

The Gold prices dipped to $2150 in the market after the Stronger US CPI Data reading printed at the February month. US CPI data came at 3.2% from 3.1%, Core CPI Data came at 3.8% YoY versus 3.9% previous reading.

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

Gold prices plummeted in the late North American session on Tuesday following a US inflation report that surpassed expectations, leading to a surge in US Treasury bond yields. The yellow metal dropped over 1%, with XAU/USD trading at $2,157.00 per troy ounce after peaking at $2,184.76.

February’s US Consumer Price Index exceeded estimates with a year-on-year inflation rate of 3.2%, up from January’s 3.1%. Monthly data rose from 0.3% to 0.4%, meeting expectations. Core CPI, which excludes volatile items, stood at 3.8% year-on-year, missing the consensus of 3.7%, while monthly readings remained steady at 0.4%.

Following the release, US Treasury yields increased, with the 10-year benchmark note rate rising five basis points to reach 4.151%. The US Dollar Index (DXY), tracking the Greenback against six major currencies, gained 0.18% to 102.92.

Gold’s decline on the US inflation data suggests decreasing expectations for a Fed rate cut. Despite a perceived dovish tone from Fed Chair Jerome Powell during his congressional testimony last week, the central bank remains data-dependent and cautious about rate adjustments. Despite solid job gains in February, downward revisions to January’s figures cooled the US labor market. Consequently, interest rate futures traders reacted, with expectations for a May rate cut dropping to 11% from 22%, while odds for June decreased to 69% from 72%.

February’s US CPI is expected to rise from 0.3% to 0.4% month-on-month and remain unchanged at 3.1% year-on-year. Core CPI is forecasted to drop from 0.4% to 0.3% month-on-month and from 3.9% to 3.7% year-on-year. Federal Reserve officials emphasize the need for sustainable inflation trends toward the 2% goal, making Tuesday’s inflation report crucial as a sharp increase in prices could prompt a reversal in XAU/USD prices.

EURUSD – Holds Near 1.0920, Awaits US Retail Sales

ECB Governing Council member Francois V illeroy De Halhau said ECB has to do rate cuts in the spring months to tackle inflation in the market. The Bank of Franc Governor Robert Holzmann said interest rate cuts in June month than April month. Pierre Wunsch Governor of Belgium said interest rate cuts from ECB can be soon due to Wage and inflation for services sector is really high.

EURUSD is moving in the Ascending channel and the market has fallen from the higher high area of the channel

Tuesday’s Market Volatility Driven by German and US Inflation Data

The pair experienced fluctuations on Tuesday, largely influenced by the release of February’s inflation figures from Germany and the United States (US). While German data met expectations, US inflation surpassed them.

Germany’s “Destatis” reported the Harmonized Index of Consumer Prices (HICP) with a consistent year-on-year figure of 2.7% in February, in line with expectations. The monthly index remained unchanged at 0.6%.

ECB Governing Council member Francois Villeroy de Galhau noted a consensus within the European Central Bank to begin lowering interest rates in spring, given progress in addressing inflation. He emphasized the ECB’s ability to adjust rates independently, highlighting its pragmatic approach to rate policy.

Bank of France Governor Robert Holzmann, in an interview with news outlet MNI, suggested the ECB is more likely to cut rates in June than April, pending confirmed projections amid high uncertainty. Pierre Wunsch, Governor of the National Bank of Belgium, stated at a news conference that the ECB may soon need to consider an interest rate cut despite uncomfortably high wage inflation and service price rises.

The US Dollar Index (DXY) maintained recent gains, supported by improved US Treasury yields. It received a boost from a stronger-than-expected CPI report, reducing expectations of a near-term Fed rate cut and strengthening the Greenback. This posed a challenge for the EUR/USD pair.

In February, US CPI (YoY) rose by 3.2%, surpassing estimates of 3.1%. The monthly index met expectations at 0.4%, higher than the previous 0.3%. US Core CPI rose by 3.8% year-on-year, above the anticipated 3.7% but below the previous 3.9%. The month-on-month figure remained steady at 0.4%, compared to the expected 0.3%. Traders are anticipated to shift focus to the upcoming US Core Producer Price Index (PPI) and Retail Sales data scheduled for release on Thursday.

USDCAD – Holds Steady Near 1.3490 Amid Stable Dollar

OPEC+ Organisation meeting said Global Oil demand looks robust in 2024 and 2025. This news makes positive for Canadian Dollar in the market. Yesterday US CPI little impressed on US Dollar against Canadian Dollar.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

USD Receives Support Despite Potential Fed Rate Cut, CAD Boosted by Oil Prices

Despite the possibility of a Fed rate cut in June and upbeat CPI data, the US dollar (USD) remains buoyant. The likelihood of a rate cut in March has dwindled to 1.0%, with probabilities at 15.6% for May and 66.6% for June.

February’s US CPI exceeded expectations at 3.2% YoY, with monthly inflation meeting forecasts at 0.4%. Core CPI rose to 3.8% YoY, slightly surpassing estimates. The USD/CAD pair’s upside may be capped by rising crude oil prices, which approached $77.90 per barrel.

Crude prices are expected to climb further due to strong global demand forecasts by OPEC. Canadian economic data this week is light, with focus shifting to US Core PPI and Retail Sales figures on Thursday.

USDCHF – Stalls Below 0.8800, Eyes on US Retail Sales

The Swiss zone import and export data is scheduled this week, Rising middle east tensions may be lift the Swiss franc against counter pairs. Yesterday US CPI Data rose more than expected makes US Dollar stronger against Swiss Franc.

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

US Inflation Remains Elevated, Fed Rate Cut Expectations Shift to Summer

In February, the Consumer Price Index (CPI) in the United States rose by 3.2% year-on-year and 0.4% month-on-month, surpassing January’s figures. The Core CPI, excluding volatile food and energy prices, also increased by 0.4% month-on-month, higher than market expectations.

The hotter CPI report may delay Federal Reserve (Fed) interest rate cuts until summer, lending support to the US dollar. Fed Chair Jerome Powell mentioned the likelihood of rate cuts this year but emphasized the need for more evidence of inflation reaching the 2% target.

Investors are currently pricing in a 70% chance of rate cuts in June, according to the CME FedWatch tool.

Meanwhile, escalating geopolitical tensions in the Middle East and a risk-averse environment could bolster safe-haven assets like the Swiss franc (CHF), potentially hindering the USD/CHF pair.

With no major economic data releases from the US and Switzerland on Wednesday, the pair’s movements depend on USD dynamics and broader market sentiment. Thursday will see the release of Swiss Producer and Import Prices along with US Retail Sales data for February.

USD INDEX – Continues Rally with Elevated US Treasury Yields Post CPI Surge

The US Dollar moved higher in the market after the Stronger US CPI Data reading printed at the February month. US CPI data came at 3.2% from 3.1%, Core CPI Data came at 3.8% YoY versus 3.9% previous reading last day. This CPI rate higher gives the hopes of Rates to be hold in the near term across economists view.

USD Index is moving in the Descending channel and the market has rebounded from the lower low area of the channel

After mixed labor market data in February, hot CPI figures don’t alter expectations much. The Fed is still anticipated to cut rates by 75 bps in 2024, starting from June.

Market Digest: DXY strengthens following CPI surge

February’s US CPI jumped to 3.2% YoY from January’s 3.1%. Core CPI also increased to 3.8% YoY, albeit slightly lower than January’s 3.9%. US Treasury bond yields rise, with 2-year at 4.60%, 5-year at 4.14%, and 10-year at 4.15%.

GBPUSD – UK GDP Grows 0.2% MoM in January, Meeting Expectations

The UK GDP data for the month of January is came at 0.20% expansion versus 0.10% contraction in December month. UK Trade Balance data came at -14.515B in January month versus -13.989B printed in Previous month reading. GBP pairs moved positive after the mixed bags of Data.

GBPUSD has broken the Box pattern in upside

According to the latest data from the Office for National Statistics (ONS), the UK economy rebounded in January, growing by 0.2% following a 0.1% contraction in December. Market forecasts had anticipated this 0.2% expansion.

In January, the Index of Services showed no growth on a 3-month over 3-month basis, compared to December’s 0.8% reading and market expectations of 0% growth.

In other economic indicators, Industrial Production and Manufacturing Production both saw monthly declines of -0.2% and 0% respectively in December.

Additionally, the UK Goods Trade Balance for January stood at GBP-14.515 billion, slightly better than the expected GBP-15 billion and the previous GBP-13.989 billion.

AUDUSD – Falls on US Inflation Data, Fed Rate Cut Expectations Adjust

The Australian Dollar dipped in the market after the Stronger US CPI Data reading printed at the February month. US CPI data came at 3.2% from 3.1%, Core CPI Data came at 3.8% YoY versus 3.9% previous reading

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

AUD/USD Declines Amid US Inflation Report, Fed Rate Cut Expectations Adjust

The Australian Dollar saw consecutive losses against the US Dollar this week, influenced by higher-than-expected inflation in the US, reinforcing the Federal Reserve’s cautious stance on rate cuts. On Tuesday, AUD/USD fell by 0.11%, and at the start of the Wednesday Asian session, it remained relatively steady at 0.6606.

After the US Bureau of Labor Statistics reported February’s inflation, exceeding forecasts, the Consumer Price Index (CPI) rose to 3.2% year-on-year, surpassing January’s 3.1%. Core CPI, excluding volatile items, was at 3.8% year-on-year, slightly missing the consensus of 3.7%.

The AUD/USD extended its decline following the data release as US Treasury bond yields increased, bolstering the US Dollar. The US Dollar Index (DXY) rose by 0.18% to 102.92.

In response to the US data, traders adjusted their expectations for a 25-basis-point rate cut in June, reducing the probability from 72% to 68% according to the CME FedWatch Tool.

On Tuesday, Australia’s economic calendar featured NAB Business Conditions for February, showing an improvement from 6.0 to 10.0, while Business Confidence decreased from 1.0 to 0.0.

Looking ahead, Australia’s economic calendar is empty for the rest of the week, while in the US, Retail Sales for February are anticipated to increase by 0.8% month-on-month, with the control group expected to rise by 0.4% month-on-month.

NZDUSD – Slips Near 0.6150 Amid Stronger US Dollar

The lack of Support measures from Foreign investments in China Real estate developers makes drawback for NZ Dollar in the market. Moody’s rating agency thumbs down for Vanke China real estate developers recently.

NZDUSD is moving in the Ascending channel and the market has fallen from the higher high area of the channel

NZD/USD Dips Near 0.6150 Amid Stronger US Dollar and Higher Treasury Yields

The NZD/USD pair is affected by USD dynamics and risk sentiment as economic data remains sparse. At present, it trades at 0.6147, down 0.06%. February US CPI data exceeded expectations, potentially delaying Fed rate cuts. Uncertainty in China’s property market also weighs on the NZD. Traders await US Retail Sales data on Thursday for further direction.

CADJPY – Japanese Firms Fully Agree to Union Wage Hikes

The Largest Japan Trade union Confederation Rengo demand the pay rises of 5.85% to Japanese Firms, Companies are agreed to Give the Bonuses and Pay hike of 5.0% above as per Demand. Toyota said there will be Bonuses and Pay hikes to all its employees is addition positive news for Japan Labours. This news is Positive for Rule of Wage to inflation cycle ratio in Japan, So BoJ may be considered for rate hikes in near term if wage hiked inflation rose happened in the economy.

CADJPY is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Early Wednesday, attention is focused on Japan’s wage negotiations. Rengo, the largest trade union confederation, pushed for a 5.85% pay increase this year, marking the first time in 30 years it exceeded 5.0%.

Reuters, citing Japanese media, reported that the demand for a JPY18,215 hike has been met.

Toyota responded in full to wage and bonus demands from its workers’ union, aligning with record-high levels, as per Reuters.

Wage increase amounts vary by job type and rank, with a maximum of 28,440 Yen per month. Okuma Corp raised wages by 15,960 Yen per month.

In other news, GS Yuasa agreed to full union wage rise demands. Mitsubishi Heavy plans an average 8.3% wage increase with an 18,000 yen base pay raise. Nissan Motor and Nippon Steel also responded fully to union wage hike demands, while Hitachi’s response marks its highest since 1998.

Market-wise, Japanese firms’ compliance with union wage hikes signals a positive outlook for the Bank of Japan’s hawkish policy shift anticipated in its March meeting next week. Expectations of a March rate hike have boosted the Japanese Yen across markets.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/