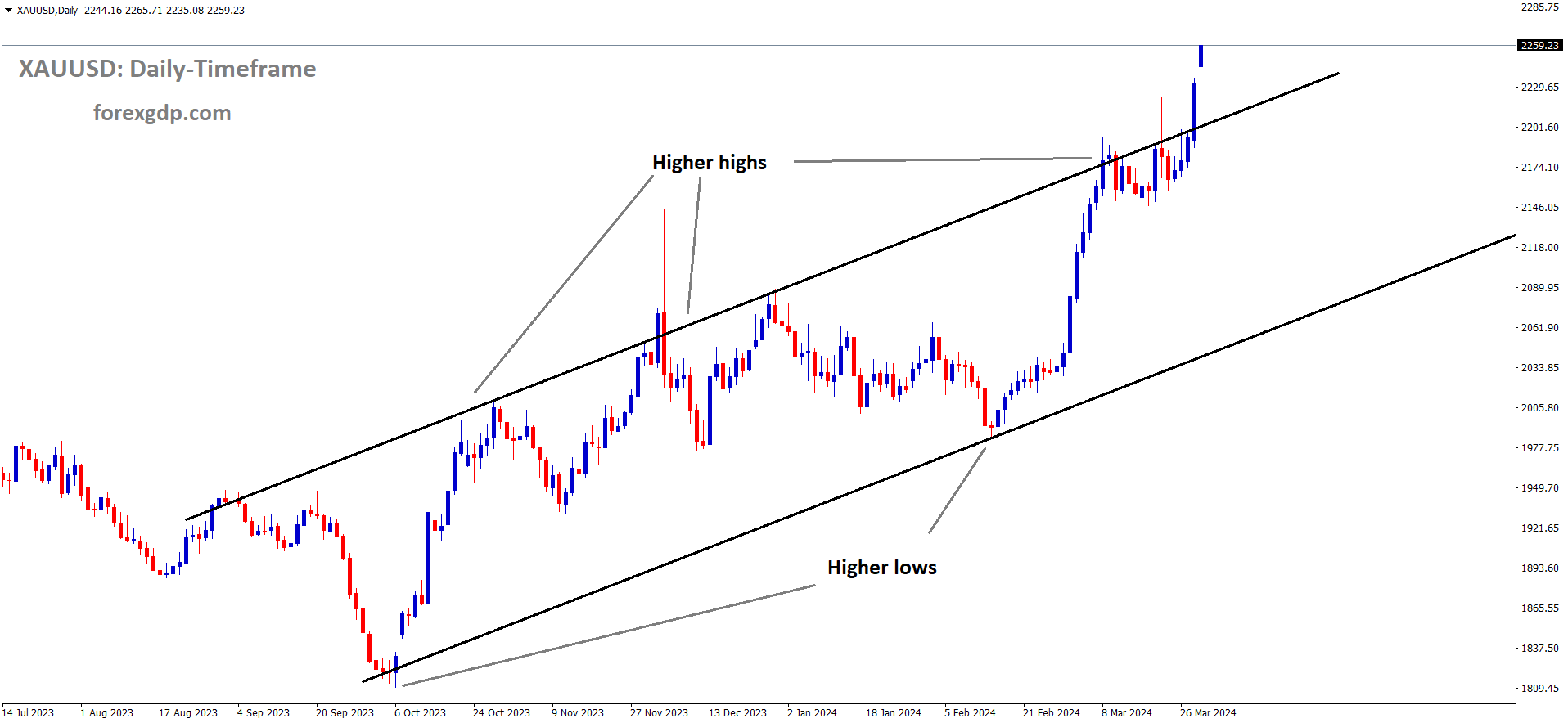

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

XAUUSD – Gold price holds near record peak, bulls remain resilient

Gold prices are flying in the All time highs after the Russia attacked Ukraine Energy and infrastructures as counter attack same as Ukraine revenge. Hamas claimed Israel is doing war crime and shoot up Palestinians whoever in the Gaza city. Friday US PCE index came at 2.5% from 2.4% in January month makes confident for June month rate cut from FED side.

This surge follows heightened speculation regarding an impending shift in the Federal Reserve’s (Fed) policy stance. The release of the US Personal Consumption Expenditures (PCE) Price Index on Friday, indicating a moderate increase in inflation for February, reinforced expectations that the Fed may commence interest rate cuts as early as June. Consequently, the US Dollar (USD) remains on the defensive, staying below its highest level since February 16, and serves as a catalyst supporting the non-yielding precious metal, gold.

In addition to these factors, ongoing geopolitical tensions arising from the prolonged conflict between Russia and Ukraine, as well as ongoing conflicts in the Middle East, provide further support for the safe-haven appeal of gold. Despite a prevailing risk-on sentiment, buoyed by positive Chinese manufacturing data, this sentiment has minimal impact on the strong bullish sentiment surrounding XAU/USD. This indicates that the prevailing direction for the precious metal continues to lean towards the upside. However, caution is advised for bullish investors due to the potential for overextended conditions on the daily chart, particularly in anticipation of the release of the US ISM Manufacturing PMI later in the day.

Market attention is focused on the movement of gold prices, which are drawing increased investor interest amid speculation about a potential rate cut by the Federal Reserve in June and ongoing geopolitical tensions. The release of crucial US inflation data on Friday has left the possibility of a June interest rate cut from the Federal Reserve open, fueling further momentum towards gold, a non-yielding asset.

The US Bureau of Economic Analysis reported that the Personal Consumption Expenditures (PCE) Price Index rose by 0.3% in February, with the yearly rate climbing to 2.5% from 2.4%. When volatile food and energy prices are excluded, the core PCE Price Index, which is the Fed’s preferred inflation measure, increased by 2.8% year-on-year compared to January’s revised reading of 2.9%.

Following the release of this data, Fed Chair Jerome Powell remarked that the latest inflation figures align with the Fed’s objectives, reinforcing expectations for an imminent adjustment in the Fed’s policy stance. According to the CME Group’s FedWatch Tool, market participants are currently pricing in a roughly 70% probability that the Federal Reserve will commence its rate-cutting cycle during the June monetary policy meeting.

In response to recent long-range drone strikes by Ukraine on oil industry assets deep within its territory, Russia has intensified its attacks on Ukraine’s energy and other infrastructure. This escalation of hostilities underscores the ongoing tensions between the two nations and highlights the volatile nature of the conflict.

Meanwhile, Hamas has accused the Israeli military of committing war crimes by implementing what it refers to as “kill zones” across the Gaza Strip. These zones are designated areas where any Palestinian approaching may be subject to being shot and killed by Israeli forces. Hamas’s condemnation underscores the gravity of the situation and adds to the complexity of the ongoing conflict in the region.

These developments further exacerbate geopolitical tensions and have significant implications for regional stability. They also highlight the urgent need for diplomatic efforts to de-escalate conflicts and promote peaceful resolutions.

The release of positive Chinese data on Sunday, indicating an expansion in business activity within the manufacturing sector for the first time in six months, has had a notable impact on the global risk sentiment. This uptick in sentiment reflects a sense of optimism regarding the economic outlook, as it suggests potential improvements in global economic conditions.

In addition to the positive Chinese data, there has been a modest increase in the value of the US Dollar. This slight uptick in the US Dollar’s value may act as a limiting factor on the gains of safe-haven assets, including precious metals like gold. Investors often turn to safe-haven assets during times of economic uncertainty or geopolitical tension, but an increase in the value of the US Dollar can make these assets relatively less attractive to investors.

Looking ahead, traders are now eagerly awaiting the release of the US ISM Manufacturing Purchasing Managers’ Index (PMI) for further short-term market direction. The US ISM Manufacturing PMI is a key economic indicator that provides insights into the health of the manufacturing sector in the United States. Depending on the results of this data release, it could provide additional impetus for market movements and influence investor sentiment in the near term.

EURUSD – ECB’s Stournaras: 4 possible 25bps rate cuts in 2024

ECB Governing council member Yannis Stournaras, Greece Central Bank Governor said, there will be a 4 rate cuts from ECB Side is Possible if inflation trend continue to downturn in coming months. The differences of our opinions is quite small than Media enlarged.

EURUSD is moving in the symmetrical triangle pattern and the market has reached the bottom area of the pattern

During a statement on Sunday, Yannis Stournaras, a member of the European Central Bank’s (ECB) Governing Council, suggested the possibility of implementing a series of interest rate cuts in 2024. He indicated that a total of four rate reductions could be feasible, amounting to a cumulative decrease of 100 basis points (bps) by the end of the year.

Stournaras stated, “If inflation develops in line with our March forecast and if this trend continues until the end of the year, I believe that this year we will have reductions in key interest rates from the ECB.” He expressed personal confidence in the potential for four interest rate cuts of 25 basis points each throughout the year.

He emphasized that this perspective isn’t unanimously shared among council members, acknowledging differing levels of caution among colleagues. Stournaras remarked, “Some colleagues are more cautious and believe that interest rate cuts should be more moderate.” However, he also noted that the divergences in opinion within the ECB’s governing council are narrower than commonly portrayed in the media.

USDJPY – JPY hovers near multi-decade low against USD, remains uncertain

The Tankan Survey shows Large manufacturer confidence eased to 11 in the First quarter from 12 in the last quarter.Non-Manufacturers confidence rose to 34 in March month from 30 in the last month. Jibun bank Manufacturing PMI data came at 48.2 in March month is 10th consecutive month fall in the Japanese economy. JPY dropping against counter pairs after weak monetary policy settings of BoJ.

USDJPY is moving in the Box pattern and the market has rebounded from the support area of the pattern

The Japanese Yen (JPY) continues its sideways movement as it heads into the European session on Monday. It remains within a familiar range against the US Dollar (USD) that it has held for approximately the past two weeks. The Bank of Japan (BoJ) has maintained a cautious approach, and the uncertain outlook regarding future rate hikes, combined with a prevailing risk-on sentiment, continues to exert downward pressure on the safe-haven JPY. However, there are indications that potential government intervention may occur to prevent excessive depreciation of the domestic currency, which could deter bearish sentiment towards the JPY.

Meanwhile, the US Dollar (USD) has struggled to gain significant momentum amid expectations that the Federal Reserve (Fed) will initiate a rate-cutting cycle in June. This sentiment has been reinforced by the release of the US Personal Consumption Expenditures (PCE) Price Index on Friday. The prospect of the Fed implementing rate cuts may limit any substantial appreciation of the USD/JPY pair. Traders are now eagerly awaiting the release of important US macroeconomic data, beginning with the ISM Manufacturing Purchasing Managers’ Index (PMI) on Monday, ahead of the Nonfarm Payrolls (NFP) report on Friday.

In addition to these market dynamics, various economic indicators and policy statements have contributed to shaping the current market sentiment. For instance, the BoJ’s cautious stance during its March meeting has been interpreted as dovish, lacking clear guidance on future policy steps or the pace of policy normalization. This has weighed on the JPY.

Furthermore, China’s positive manufacturing data for March, indicating expansion for the first time in six months, has boosted investor confidence. However, Japan’s own economic indicators, such as the Tankan survey and the au Jibun Bank Japan Manufacturing PMI, present a mixed picture. While business optimism among large manufacturers eased, there are signs of improvement, suggesting that the worst of the economic weakness may have passed.

Additionally, comments from Japanese officials, including Finance Minister Shunichi Suzuki, about potential speculative moves behind the recent JPY decline have underscored the authorities’ readiness to intervene in the currency market if necessary. This has added another layer of uncertainty to the JPY’s outlook.

Overall, the interplay between global economic data, central bank policies, and geopolitical tensions will continue to influence the direction of the USD/JPY pair in the near term, with traders closely monitoring upcoming US economic releases for further guidance.

USDCHF – Trades Slightly Lower Above 0.9000 Ahead of US PMI Data

The SNB has do 25bps rate cut in the last month meeting, SNB said last 2.5 years Inflation is eased as per our Goal of target, So easing of monetary policy is applied. ING Analysts expected 2 more cuts in this 2024 if inflation does not rise by Geopolitical environment. Swiss CPI is due on Thurday and expected to 1.4% in March month.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

During the early European session on Monday, the USD/CHF pair was observed trading with a slight negative bias around 0.9015. This trend follows dovish remarks made by Federal Reserve (Fed) Chairman Jerome Powell on Friday, which have had a dampening effect on the US Dollar (USD) and have consequently capped the upside potential of the USD/CHF pair. Investors are now directing their focus towards the release of the US March ISM Manufacturing Purchasing Managers Index (PMI), scheduled for later in the day. However, trading activity is expected to remain subdued due to the bank holiday in Switzerland for Easter Monday.

Recent inflation data for February was in line with market expectations, which may prompt the Fed to maintain its current interest rate stance before considering any rate cuts later in the year. Market pricing, as indicated by the CME Group’s FedWatch Tool, aligns with Fed projections for three rate cuts. Additionally, the US Bureau of Economic Analysis reported that the Personal Consumption Expenditures Price Index (PCE) rose 2.5% year-on-year (YoY) in February, meeting market consensus. However, the monthly PCE figure showed a softer-than-expected increase of 0.4% month-on-month (MoM) for the same month. Core PCE, the Fed’s preferred inflation measure, also rose in line with market estimations, increasing by 2.8% YoY and 0.3% MoM in February.

Turning to Switzerland, the Swiss National Bank (SNB) announced a 25 basis points (bps) reduction in the benchmark interest rate to 1.5% on March 21. The SNB attributed this easing of monetary policy to the effectiveness of its efforts in combating inflation over the past two and a half years. Analysts at ING anticipate two more rate cuts from the SNB this year unless unforeseen developments in the international economic landscape result in a rapid resurgence of inflationary pressures.

Looking ahead, investors will closely monitor the release of the Swiss Consumer Price Index on Thursday, which is expected to show a 1.4% increase in March. A softer-than-expected reading in the Swiss CPI inflation data could potentially exert downward pressure on the Swiss Franc (CHF). Furthermore, on Friday, attention will shift to the release of US employment data, including the Nonfarm Payrolls (NFP), Unemployment Rate, and Average Hourly Earnings for March.

USDCAD – stays low despite rising Oil prices, stays above 1.3500.

The US Dollar declined against CAD in the market due to Oil prices soaring in strong demand and supply constraint from Oil producing countries. The Canadian Domestic data performed well and gives boosting for Canadian Dollar against counter pairs.

USDCAD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The surge in Crude Oil prices to a five-month high is driven by concerns regarding global supply constraints. Factors contributing to this include OPEC+ production cuts, drone attacks on Russian refineries, and positive Chinese manufacturing data. These developments support the commodity-linked Canadian Dollar (CAD). Additionally, a weakened US Dollar (USD) further weighs on the USD/CAD pair. OPEC+ has committed to extending production cuts until the end of June, contributing to the pressure on the pair.

Russian Deputy Prime Minister Alexander Novak’s statement on Friday indicated a prioritization of reducing output over exports by Russian Oil companies in the second quarter. Moreover, Ukrainian drone attacks have disrupted several Russian refineries, leading to an expected decrease in Oil exports from Russia. The uptick in China’s manufacturing activity after six months of contraction adds to the positive outlook for fuel demand.

The USD faces challenges in attracting buyers amid expectations of an impending rate-cutting cycle by the Federal Reserve (Fed) starting in June. This sentiment is reinforced by the lack of significant surprises in the US Personal Consumption Expenditures (PCE) Price Index released on Friday. The prevailing risk-on sentiment in the market further diminishes the appeal of the safe-haven USD, contributing to the downward pressure on the USD/CAD pair.

Investors are keenly awaiting the release of the US ISM Manufacturing Purchasing Managers’ Index (PMI) for potential market catalysts. Additionally, the Bank of Canada (BoC) Business Outlook Survey is anticipated. These events, coupled with ongoing Oil price movements, are expected to create short-term trading opportunities for the USD/CAD pair. However, attention remains focused on the forthcoming monthly employment reports from both the US and Canada, scheduled for Friday.

USD INDEX – Powell: Economy Strong, No Doubt

The FED Powell speech on Friday shows US economy is doing well , there is no doubt, inflation is on the down track. If inflation is not down, then rates are higher for ever. We do not see every economic calendar and doing changes in the monetary policy settings. If Job market eases, consumer spending lows then we do rate cuts and it will be positive for US Economy.

USD INDEX is moving in an Ascending channel and the market has reached the higher high area of the channel

Federal Reserve Chair Jerome Powell delivered remarks at the Macroeconomics and Monetary Policy Conference held in San Francisco, where he shared insights on various economic factors and the Fed’s stance on monetary policy. Here are some key quotes from his speech:

- Powell acknowledged the recent core inflation figures, stating that they represent significant progress in addressing inflation concerns.

- He expressed the Fed’s expectation that inflation will gradually reach the target of 2%, albeit possibly encountering some fluctuations along the way.

- Powell emphasized that if the anticipated economic scenario does not unfold as expected, the Fed is prepared to maintain interest rates at their current levels for an extended period.

- Regarding the future trajectory of interest rates, Powell indicated uncertainty, stating that it is unclear where rates will settle once prevailing economic conditions stabilize.

- Despite the low interest rate environment, Powell asserted that the economy is not adversely affected and continues to exhibit strength.

- Powell affirmed the robustness of the economy, stating unequivocally that there is no doubt about its strength. He mentioned that the likelihood of a recession at present is not elevated.

- Powell noted that any unexpected weakness in the labor market could prompt the Fed to consider adjustments in its policy stance.

- Finally, Powell emphasized that the Fed’s decision-making process is independent of political considerations or external pressures, emphasizing its commitment to data-driven analysis and economic indicators rather than political calendars.

AUDUSD – AUD trims gains as USD firms; Eyes on ISM PMI

The China NBS Manufacturing data came at 50.8 in March month from 49.1 in the previous month. Non- Manufacturing data came at 53.0 from 51.4 in the previous month. Australia consumer inflation expectations came at 4.3% in March month from 4.5% in the previous month.

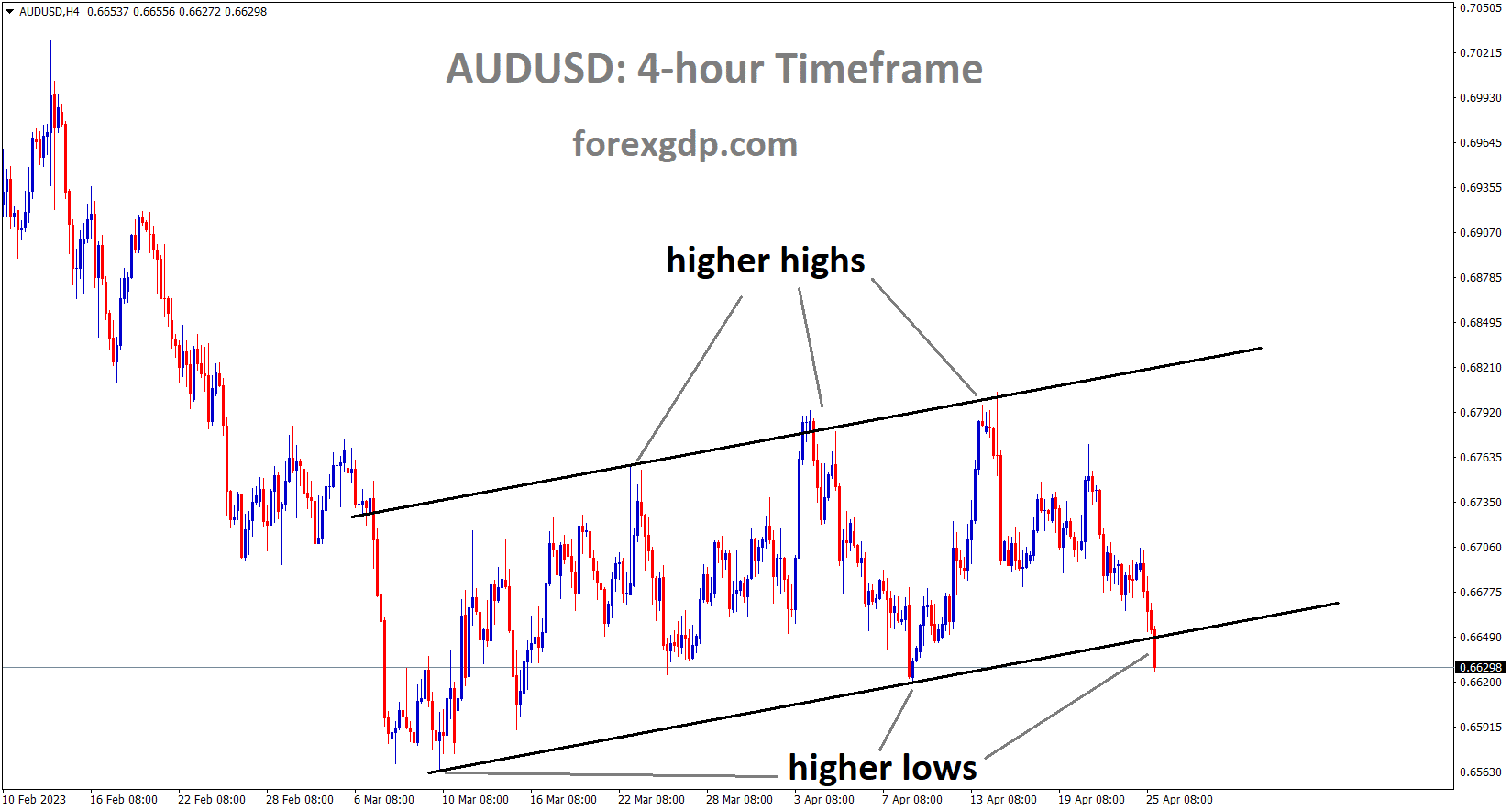

AUDUSD is moving in ascending channel and the market has reached the higher low area of the channel

The Australian Dollar (AUD) retraced some of its recent losses on Monday, likely buoyed by positive Chinese Purchasing Managers Index (PMI) figures. This improvement in sentiment, along with decreased US Treasury yields, exerted downward pressure on the US Dollar (USD), providing support to the AUD/USD pair. Trading activity is expected to be subdued due to Easter Monday, which could further influence market movements.

However, the Australian Dollar faced challenges amid weaker Consumer Inflation Expectations, suggesting potential expectations for interest rate cuts by the Reserve Bank of Australia (RBA) later in 2024. Investors are keenly awaiting the release of the RBA Meeting Minutes scheduled for Tuesday, which could provide insights into the central bank’s monetary policy outlook.

On the other hand, the US Dollar Index (DXY) struggled following dovish remarks from Federal Reserve (Fed) Chairman Jerome Powell on Friday. Powell mentioned that the recent US inflation data aligned with the desired trajectory, reinforcing the Federal Reserve’s stance on potential interest rate cuts for the year. The Personal Consumption Expenditures Price Index (PCE) data from the United States (US) met expectations in February, contributing to the overall market sentiment.

In the broader context, various economic indicators and central bank communications have played a significant role in shaping market sentiment. For instance, Australia’s Consumer Inflation Expectations decreased slightly to 4.3% in March, while China’s Manufacturing PMI and Non-Manufacturing PMI figures showed improvement, signaling potential economic resilience in the region.

Additionally, remarks from Federal Reserve officials, such as San Francisco Fed President Mary C. Daly and Federal Reserve Board Governor Christopher Waller, indicated a cautious approach towards potential rate cuts, emphasizing the strength of the US economy. Meanwhile, US economic data releases, including Core PCE, Initial Jobless Claims, and Gross Domestic Product (GDP) figures, also provided insights into the state of the economy.

Overall, the interplay between various economic factors and central bank policies will continue to influence the AUD/USD pair’s direction, with traders closely monitoring upcoming data releases and central bank communications for further guidance.

GBPUSD – steadies near 1.2530 post-gains, eyes US ISM Manufacturing PMI

The Bank of England is going to do 3 rate cuts in this year. Last half of 2023 shows weaker GDP data and recession of England is showing in the market. Domestic data of UK is not at favourable for GBP at this time. US Domestic data performing well and So US Dollar rises against GBP in the market.

GBPUSD is moving in the Box pattern and the market has reached the support area of the pattern

The US Dollar (USD) managed to recuperate its losses during the trading session due to prevailing risk aversion sentiments, particularly ahead of the awaited release of the ISM Manufacturing Purchasing Managers Index (PMI) data from the United States (US). This rebound in the USD capped the upward momentum of the GBP/USD pair.

However, the US Dollar Index (DXY) faced challenges following remarks made by Federal Reserve (Fed) Chairman Jerome Powell on Friday. Powell’s comments indicated that the recent US inflation data fell in line with expectations, reaffirming the Fed’s stance on potential interest rate cuts throughout 2024. Fed officials have maintained projections of three rate cuts for the year, with market participants anticipating the first of these to occur at the June meeting.

In February, the US Core Personal Consumption Expenditures (PCE) saw a month-over-month (MoM) increase of 0.3%, aligning with market forecasts and slightly lower than January’s 0.5%. The yearly index rose by 2.8%, meeting expectations and slightly lower than the previous increase of 2.9%. US Headline PCE (MoM) recorded a 0.3% increase, slightly below expectations and lower than the previous month’s 0.4% rise. Year-over-year PCE rose by 2.5%, meeting expectations.

Conversely, the Pound Sterling (GBP) faced pressure amid anticipation that the Bank of England (BoE) would implement three quarter-point rate reductions throughout 2024. This pressure intensified due to recent weaker economic data, signaling that the UK economy slipped into recession in the latter half of 2023. BoE Governor Andrew Bailey’s indication of potential interest rate cuts in future policy meetings further exacerbated this pressure.

With limited high-impact data expected from the United Kingdom (UK), traders are likely to assess the UK economic landscape by closely monitoring indicators such as Nationwide Housing Prices, S&P Global PMI, and Halifax House Prices data scheduled for release throughout the week.

NZDUSD – climbs near 0.5980 on dovish Powell remarks; Focus on US ISM PMI

The RBNZ Governor Adrian Orr said there will be a rate cuts in this year if inflation levels controlled to our target. China Caixin Manufacturing PMI Came at 51.1 from 51.0 expected and 50.9 in the previous month. Chinese data positive readings makes positive move for NZD.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The NZD/USD pair saw an upward trajectory following the dovish remarks made by Federal Reserve (Fed) Chairman Jerome Powell on Friday. Powell’s comments highlighted that the recent data on the United States (US) Personal Consumption Expenditures Price Index (PCE) was consistent with expectations, reinforcing the Fed’s stance on potential interest rate cuts for the year.

Federal Reserve Board Governor Christopher Waller reiterated that there is no urgency to implement rate cuts, especially amidst ongoing inflationary pressures. Similarly, San Francisco Fed President Mary C. Daly echoed this sentiment, stressing that while the Fed is prepared to adjust rates based on data, there is currently no immediate need to do so given the strength of the US economy and the minimal risk of a downturn.

The US Dollar Index (DXY) faced challenges due to lower US Treasury yields, hovering around 104.50. The 2-year and 10-year yields on US bond coupons stood at 4.60% and 4.19%, respectively. Fed officials maintain projections of three rate cuts for the year, with expectations that the first cut may occur at the June meeting.

Conversely, the New Zealand Dollar (NZD) experienced downward pressure amid speculation that the Reserve Bank of New Zealand (RBNZ) may begin implementing policy rate cuts from early next year. RBNZ Governor Adrian Orr indicated progress in bringing inflation back within the target range, suggesting that interest rates have peaked and rate cuts are increasingly likely.

Furthermore, the Kiwi Dollar (NZD) received support from positive Chinese Purchasing Managers Index (PMI) figures, indicating the first expansion in Chinese manufacturing activity in six months in March.

China’s Caixin Manufacturing PMI for March exceeded expectations at 51.1, while on Sunday, China’s National Bureau of Statistics (NBS) reported a rise in Manufacturing PMI to 50.8 from 49.1 in the previous month. Additionally, NBS Non-Manufacturing PMI increased to 53.0 from 51.4 in February.

Traders may exercise caution ahead of the release of the United States (US) ISM Manufacturing Purchasing Managers Index (PMI) data scheduled for later in the North American session. Additionally, Building Permits data will be released by Statistics New Zealand on Thursday.

CRUDE OIL – WTI nears $83.10 on expected OPEC+ supply constraints

The OPEC+ Meeting is scheduled this week, Russia Deputy PM said Russia have no intensions on export ban on Oil supply, Ukraine attacks caused only 1 million barrel per day shortage. Russia said exporting companies should reduce the outputs with OPEC+ rule of Output cuts. Goldman Sachs said Europe has exceeded Oil consumption in February month as 100000 barrels per month versus -2 lakhs barrels decline is expected in previous forecast.

XTIUSD Crude Oil price is moving in an Ascending channel and the market has reached the higher high area of the channel

The West Texas Intermediate (WTI) oil price continues its upward trend, marking the third consecutive session of gains as it reaches approximately $83.10 per barrel during Asian trading hours on Monday. This sustained rise in crude oil prices is primarily driven by expectations of limited supply due to production cuts implemented by the Organization of the Petroleum Exporting Countries and their allies (OPEC+).

Investors are closely watching the upcoming joint ministerial meeting of OPEC+, scheduled for this week. It is anticipated that during this meeting, OPEC+ will evaluate the market fundamentals and the adherence of its members to production targets. There is widespread speculation that the current output policies will be maintained.

Additionally, Russian Deputy Prime Minister Alexander Novak highlighted on Friday the importance for oil companies to prioritize reducing output rather than exports in the second quarter to align with OPEC+ production goals. He also indicated that there is no immediate need for Russia to impose export bans on diesel fuel to address rising prices and potential fuel shortages resulting from recent drone attacks that disrupted refining operations.

The recent drone strikes launched by Ukraine have significantly impacted several Russian refineries, leading to a reduction in Russia’s fuel exports. These attacks have resulted in the shutdown of nearly 1 million barrels per day of Russian crude processing capacity.

Official data released indicates that Chinese manufacturing activity expanded for the first time in six months in March, which has positively influenced the outlook for crude oil demand from the world’s largest crude oil importer. Analysts at Goldman Sachs have observed that oil demand in Europe surpassed expectations, recording a year-on-year increase of 100,000 barrels per day (bpd) in February. This contradicts their previous forecast of a 200,000 bpd decline for 2024.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/