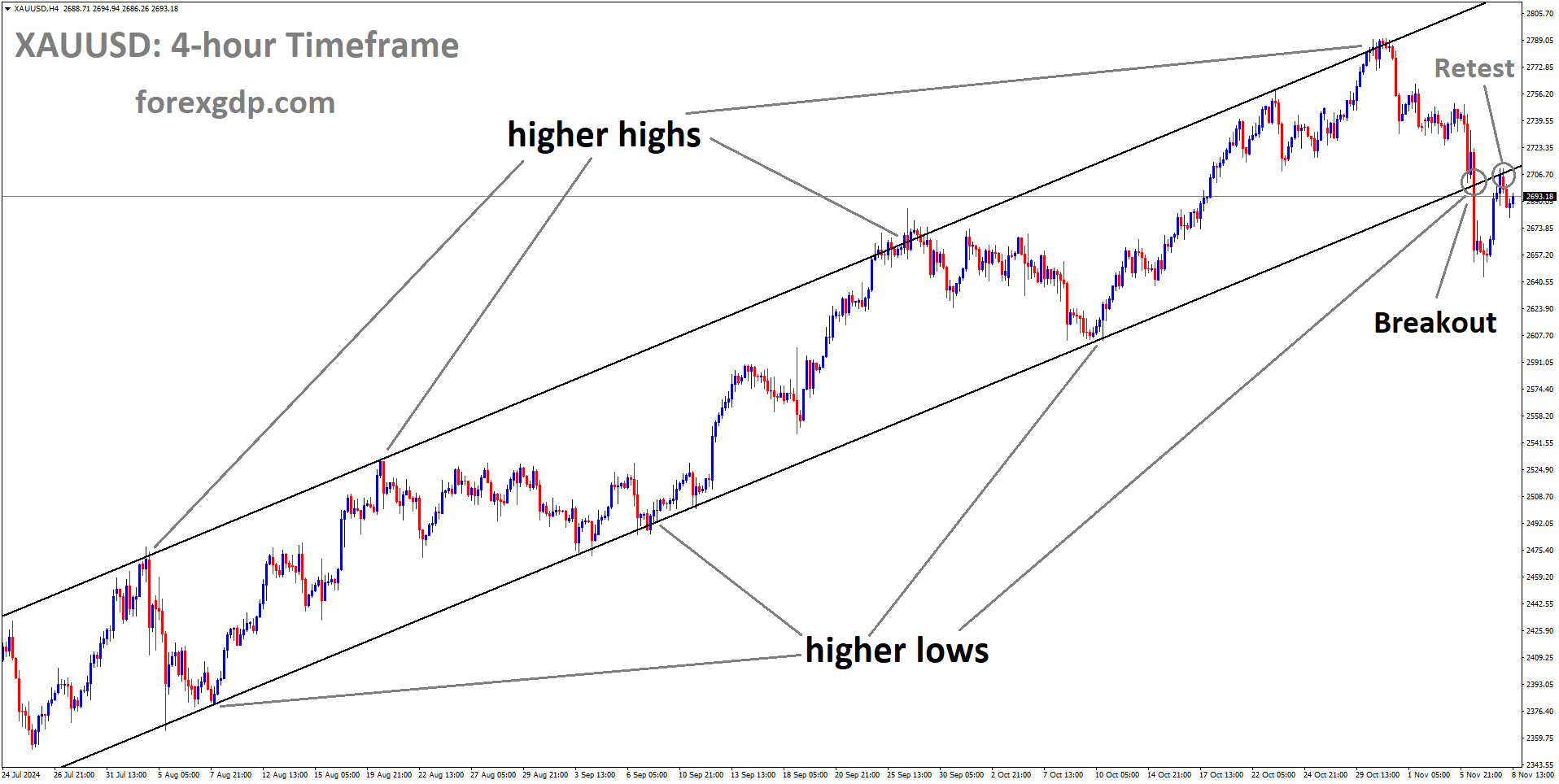

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD – Gold price nears record high, around $2,300 amidst geopolitical risks

Gold prices are moved to Record high of $2300 after the FED Powell dovish speech on Wednesday. Rate cuts in this year are based on evaluation of incoming data. Israel attacked Iran Embassy in Syria, Five military advisers and 2 Army Generals were killed. It created third party Iran fears entered into this conflict between Israel and Gaza. This fears of uncertainity moved Gold prices higher in the market.

In light of geopolitical tensions from the Russia-Ukraine conflict and Middle East turmoil, along with a significant earthquake in Taiwan, the demand for gold as a safe-haven asset is expected to persist. Additionally, the recent decline in the US Dollar amidst uncertainty regarding the Federal Reserve’s interest rate plans supports a positive outlook for gold in the short term.

However, despite these factors, a positive sentiment in equity markets and overextended conditions in daily charts may deter bullish activity in the gold market. Investors may opt to await further clarity on the Fed’s rate-cut strategy before committing to new positions. Focus will likely center on the upcoming release of the US Nonfarm Payrolls report on Friday, with attention also on speeches by influential Federal Open Market Committee (FOMC) members for potential trading opportunities.

Mixed signals regarding interest rates from Federal Reserve officials have pushed the US Dollar to a one-week low, contributing to the rise in the price of gold. Notably, influential members of the Federal Open Market Committee (FOMC), including Fed Chair Jerome Powell, have reiterated the central bank’s intention to cut rates in 2024, although they have provided limited guidance on the timing of such actions. Powell emphasized the importance of thoroughly assessing the current state of inflation and stressed the need for further discussion and data before any decision on rate cuts. Moreover, the retreat of the yield on the benchmark 10-year US government bond from a four-month high on Wednesday has provided additional support for gold, which does not yield interest like bonds.

EURUSD – climbs to weekly peak at 1.0835 on weak US data

The Euro pair is moved up after the US Services PMI data came at 51.4 in March month from 52.6 in February month. US ADP Data printed at 188K from 155K in previous month. Euro CPI Data came at lower as 2.4% in March month versus 2.6% expected. Euro pairs moved up against USD after the mixed bags of data on both economy sides.

EURUSD is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern

The Euro is experiencing a notable rebound during Wednesday’s US trading session. The EUR/USD pair has surged approximately 60 pips, driven by disappointing US services sector data, which has alleviated concerns of a hawkish stance by the Federal Reserve.

Data released by the Institute for Supply Management (ISM) revealed a slowdown in business activity in the US services sector, with the PMI dropping to 51.4 in March from 52.6 in the previous month. This contrasts with expectations of a slight acceleration to 52.7. Additionally, the Prices Paid sub-index declined to 53.4 from 58.6 in February, indicating a disinflationary trend in the sector.

These PMI figures have overshadowed the impact of a robust ADP employment report, which suggests a resilient labor market ahead of Friday’s Nonfarm Payrolls report. Furthermore, remarks from Atlanta Fed President Bostic and Fed Chair Powell later in the day tempered expectations of imminent rate cuts, although they had minimal impact on the EUR/USD pair.

Earlier during the European session, Eurozone Consumer Price Index (CPI) data confirmed subdued inflation readings observed in Germany on Tuesday. Core inflation fell below the 3% annual rate, while the headline CPI eased to 2.4%, significantly lower than the market’s forecast of 2.6%. These figures indicate the potential for the European Central Bank (ECB) to implement rate cuts in the coming months, although their impact on the Euro has been relatively limited.

USDJPY – JPY struggles, near multi-decade low vs. USD

The Japanese Yen moving lower against counter pairs after the BoJ announced there will be no change in Government Bond buying scheme. Continuous purchases of Bonds make JPY weakness in the market against rivals. US Domestic data printed higher last day in private jobs and Service PMI data as lower numbers.

USDJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

The Japanese Yen (JPY) continues to face downward pressure against the US Dollar (USD) as it hovers just above a multi-decade low reached last week, signaling weakness in the Japanese currency. The Bank of Japan’s (BoJ) expressed commitment to maintaining an accommodative monetary policy for an extended period, combined with a generally positive market sentiment, contributes to the depreciation of the safe-haven JPY. However, the prospect of potential intervention by Japanese authorities to support the domestic currency limits aggressive selling pressure on the JPY.

Conversely, the USD extends its recent decline for the third consecutive day, deviating from its peak since February 14, as uncertainty looms over the Federal Reserve’s (Fed) stance on interest rate cuts. Nonetheless, the downside for the USD is mitigated by expectations of sustained interest rate differentials between the US and Japan. Traders are also exercising caution ahead of the release of the crucial US Nonfarm Payrolls (NFP) report on Friday.

In the daily market movements, Japanese officials continue verbal interventions to support the JPY, albeit with limited impact. Notably, former Vice Finance Minister for International Affairs, Tatsuo Yamasaki, reiterated Japan’s readiness to intervene in the currency market if the JPY weakens beyond its current range. On the US front, the latest data from Automatic Data Processing reveals a stronger-than-expected increase in private sector employment, while the Institute for Supply Management reports a decline in the US Services Purchasing Managers Index (PMI) and the Prices Paid Index for March.

Federal Reserve Chair Jerome Powell refrains from specifying the timing or scale of potential rate cuts, emphasizing the need for a thorough assessment of inflation before any policy adjustments. Despite this, market expectations lean towards a rate cut at the June policy meeting, influenced by various Fed officials’ cautious comments. The retreat in yields on the 10-year US government bond, following a recent high, prompts a sell-off of the USD, restricting the USD/JPY pair’s ascent towards the 152.00 threshold.

Overall, the combination of the BoJ’s dovish stance, ongoing market sentiment, and anticipation of Fed policy adjustments keeps the JPY under pressure, while uncertainty surrounding the USD’s trajectory limits its gains against the JPY.

USDCHF – Swiss CPI Inflation Hits 2.5-Year Low

The Swiss CPI Data for the March month came at 1% well below the 1.3% expected data and 1.2% in February month. Now SNB target of 0-2% range is fulfilled by March month data. Further meetings may be rate cuts from SNB is possible have more chances, So Swiss Franc pulled down from highs after the data printed.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the pattern

In March, Switzerland’s annual consumer inflation rate saw a further decline, dropping to 1% from 1.2% in February, according to data released by the Swiss Federal Statistical Office.

This figure surprised market analysts who had expected an increase to 1.3%, marking the lowest CPI inflation rate since September 2021.

")

The prices of food and non-alcoholic beverages experienced a decline of 0.4% year-on-year (YoY) in March, compared to a rise of 0.8% in February. Similarly, the cost of healthcare and transportation both decreased by 0.5% YoY in March.

However, certain categories saw an increase in inflation rates. Housing and utilities experienced a slight acceleration with a 3.2% YoY increase compared to 3.1% YoY in February. Recreation and culture also saw a rise to 1.8% YoY from 1.7% YoY in February, while other goods and services experienced a 1.1% YoY increase compared to 1% YoY in February.

Reflecting a divergence in monetary policy between the Swiss National Bank (SNB) and the Federal Reserve. The SNB notably reduced its key interest rate by 25 basis points to 1.5% in March, marking the first major rate cut by a central bank since the onset of global disinflation in 2023.

USDCAD – pressured below 1.3530 on weak USD, elevated oil prices

The Canadian Dollar pushing up against counter pairs after the Oil prices increased upside in the global market. Middle east conflicts continue to burns as war fears, US ISM Services index came down at 51.4 in March from 52.6 in February month. US ADP employment data added 184000, but US Dollar failed to move upside against CAD last day.

USDCAD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The recent surge in crude oil prices, reaching their highest levels since October, has bolstered the commodity-linked Canadian Dollar (CAD), commonly known as the Loonie.

Firstly, the release of weaker-than-expected US ISM Services PMI data for March contributed to the depreciation of the US Dollar (USD). The Institute for Supply Management (ISM) reported a decline in the US Services Purchasing Managers Index (PMI) to 51.4 from 52.6 in February, falling below market expectations of 52.7. This disappointing figure led to increased selling pressure on the USD.

However, contrasting data from Automatic Data Processing (ADP) showed that private sector employment in the US rose by 184,000 in March, surpassing the market consensus of 148,000 and providing some support to the USD.

Furthermore, Federal Reserve (Fed) Governor Adriana Kugler’s remarks on Wednesday regarding gradual inflation slowdowns and potential interest rate cuts contributed to the weakening of the USD. Fed Chair Jerome Powell’s dovish comments, stating that the policy rate may have peaked and hinting at possible rate cuts, also added selling pressure on the USD and weighed on the USD/CAD pair.

Meanwhile, geopolitical tensions in the Middle East heightened fears of oil supply disruptions, boosting crude oil prices and consequently strengthening the Canadian Dollar (CAD). Given that Canada is a major exporter of crude oil, higher oil prices have a positive impact on the country’s economic performance and contribute to the appreciation of the CAD.

Looking ahead, market participants will closely monitor the release of US February Goods Trade Balance and weekly Initial Jobless Claims. Additionally, speeches from Fed officials Barkin, Goolsbee, Kashkari, and Mester on Thursday are expected to provide further insights into the monetary policy outlook.

USD INDEX – Fed’s Kugler forecasts further inflation slowdown and rate cuts this year

The FED President Adriana Kugler said she is expected the rate cuts once inflation trend continue to slow down. Still Core PCE index at 2.8% in March month above the FED’s 2% target. New Businessess created 150K new jobs for US Economy. 2024 GDP will be lower than 2023 3.1% GDP numbers. Disinflation trend has to continue with lower unemployment rate, wage adjusted inflation is expected in the US Economy in my view then only we see rate cuts from FED, Iam go with March month monetary policy settings is appropriate for current stance as per she said.

USD Index has broken the Ascending channel in downside

On Wednesday, Federal Reserve (Fed) Governor Adriana Kugler expressed her outlook regarding inflation, stating that she anticipates a continued decline in inflation throughout the year. She believes this trend will lead the central bank to consider cutting interest rates, according to Reuters.

In her remarks, Kugler made several key points:

– She indicated that her expectations regarding policy rates align with the projections made by policymakers during the March Federal Open Market Committee (FOMC) meeting.

– Kugler emphasized that if disinflation and labor market conditions progress as she anticipates, it would be appropriate for the Fed to lower the policy rate this year.

– She highlighted her belief that the disinflationary trend will persist, despite the current restrictive policy environment, although she acknowledged that this outcome is not guaranteed.

– Kugler noted that while progress in inflation has been uneven, annual core Personal Consumption Expenditures (PCE) at 2.8% represents considerable progress, yet still remains above the Fed’s 2% target.

– She mentioned that data on new tenant rent agreements suggest a continued cooling of housing inflation.

– Kugler stressed that further disinflation will require progress in both housing and non-housing services sectors.

– Regarding the labor market, she observed that it has moved into a better balance, attributing this partly to strong population growth.

– She emphasized the importance of wage growth being consistent with 2% inflation over time, noting that the US is moving back toward that level of wage growth.

– Kugler pointed out that anchored inflation expectations are evident in consumer and business surveys.

– She expects consumption growth to slow somewhat this year, citing soft consumer spending in January and February.

– While she anticipates solid GDP growth this year, she expects it to be slower than the pace seen in 2023.

– Kugler’s baseline expectation is that further disinflation can be achieved without a significant increase in unemployment.

– She commented on the adaptation of supply networks to disruptions, such as those seen at the port of Baltimore.

– Kugler highlighted the role of new businesses in job creation, noting that around 150,000 jobs per month have originated from new businesses.

GBPUSD – GBP strengthens on better UK economic prospects, USD weakness

The UK economy is moving higher after the manufacturing PMI data came at higher in March month after the 20 months of contraction data. 58% of Business owners express their expansion of manufacturing activity in the next 12 months.The UK house prices rose to 1.6% in March months despite higher rates in the UK.

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The GBP/USD pair is demonstrating strength as recent economic indicators in the United Kingdom point to a potential return to growth after experiencing a technical recession in the latter half of 2023. Additionally, the US Dollar weakened due to disappointing data from the United States Institute of Supply Management (ISM) Services PMI for March, further boosting the Cable.

In the UK, the Manufacturing PMI surprisingly expanded in March following 20 consecutive months of contraction, driven by strong domestic demand. This robust data has led to heightened business optimism, with 58% of manufacturers expecting an increase in production levels over the next 12 months. Furthermore, British house prices saw a 1.6% rise in March, marking the fastest pace since December 2022, indicating resilience in the real estate sector despite historically high interest rates.

Market Analysis:

The Pound Sterling experienced a slight consolidation after reaching 1.2660 against the US Dollar, with expectations of further upside given bullish market sentiment and the impact of the weak US ISM Services PMI on the US Dollar. S&P 500 futures also posted significant gains during the Asian session.

The US Services PMI unexpectedly declined to 51.4 in March, below expectations of 52.7 and the previous reading of 52.6. Given that the service sector accounts for a significant portion of the US economy, this poor data had a substantial negative impact on the US Dollar, leading the US Dollar Index (DXY) to drop by over 0.5% to 104.15. The ISM report also indicated significant decreases in new orders and prices paid sub-indexes.

The focus for the US Dollar this week will be on the US Nonfarm Payrolls (NFP) report for March, scheduled for release on Friday. Market participants will closely analyze this data to gauge whether the Federal Reserve will begin interest rate reductions starting from the June meeting. Expectations for the NFP report suggest a hiring figure of around 200K workers, lower than February’s reading of 275K.

In the UK, market sentiment regarding Bank of England (BoE) rate cuts and the S&P Global/CIPS Services PMI, scheduled for release at 08:30 GMT, will guide the Pound Sterling. With UK inflation consistently slowing, there is an expectation that the BoE may initiate a rate-cut cycle in June, with BoE Governor Andrew Bailey suggesting two or three rate cut expectations for the year.

The Services PMI is forecasted to remain unchanged from its preliminary reading of 53.4. A positive PMI outcome would further strengthen the UK economic outlook, following the return to growth in the final Manufacturing PMI reading for March, released earlier this week after 20 consecutive months of contraction.

AUDUSD – Judo Bank Services PMI climbs to 54.4 in March from 53.5 before

The Australian Judo Bank Services PMI came at higher reading in March month as 54.4 from 53.5 in February month, Composite PMI came at 53.3 in March from 52.4 in February month.The Austrlian Business index hits at this March 2024 is highest reading since 2022 after the RBA began rate hikes. Cost pressure index is higher after the rate hikes.

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

According to the latest data released by Judo Bank and S&P Global on Thursday, the final reading of Australia’s Judo Bank Services Purchasing Managers Index (PMI) saw an improvement to 54.4 in March, up from the previous reading of 53.5.

The Judo Bank Australian Composite PMI also showed growth, rising to 53.3 in March compared to 52.4 in the previous reading.

Key points from the data include:

– The output index reached a new cyclical high of 54.4 in March, marking the fourth consecutive month of improvement. This increase in the services output index by 8.4 points represents the largest gain in the series outside of recovery from lockdowns.

– The services output index has surpassed its long-run average level of 51.7.

– The March 2024 reading is the highest since April 2022, coinciding with the commencement of the monetary policy tightening cycle.

– The Outstanding Business Index reached its highest level since the Reserve Bank of Australia began raising interest rates in May 2022.

– Although other activity indicators in the survey dipped slightly in March, they remained comfortably above the neutral 50 index level.

– Cost pressures persist at elevated levels, although there are indications of gradual easing over the past six months.

– The input price index declined slightly to 61.5, the lowest since 2021, but still not significantly lower than the average reading of 62.8 observed through the second half of 2023.

– The Prices Charged Index remained unchanged at 55.0 in March, slightly higher than the average over the past quarter and broadly in line with index readings from the past year.

NZDUSD – rises on better Kiwi Building Permits, hovers near 0.6020

The NZ Building permits for February month came at 14.9% from decline of 8.6% in January month. RBNZ meeting is scheduled for new week, inflation is still more than 1-3% target of RBNZ in the NZ economy. Earth Quake hits at 7.2 Magnitude at Taiwan mainly semiconductor company in NZ. NZ Dollar pushed up after the Building permit data printed at higher numbers.

NZDUSD has broken the Descending channel in upside

This movement follows the release of seasonally adjusted Building Permits (Month-on-Month) data by Statistics New Zealand, indicating significant improvement with a notable increase of 14.9% in February. This rebound comes after a previous decline of 8.6%.

Despite this positive economic indicator, the Reserve Bank of New Zealand (RBNZ) has expressed caution, noting that headline inflation remains outside the desired range of 1 to 3%. Market participants are eagerly anticipating the RBNZ’s upcoming policy meeting scheduled for next week. Additionally, concerns have arisen regarding the potential economic impact of the 7.2 magnitude earthquake that struck Taiwan on Wednesday, particularly on the semiconductor supply chain in New Zealand.

The US Dollar (USD) faced challenges following the release of mixed economic data from the United States (US), providing support to the NZD/USD pair. In March, the US ADP Employment Change increased by 184,000, surpassing February’s rise of 155,000 and exceeding the market consensus of 148,000. However, the US ISM Services PMI declined to 51.4 from 52.6 in February, falling short of the anticipated level of 52.7.

The US Dollar Index (DXY) struggled as Federal Reserve (Fed) Chair Jerome Powell reiterated the central bank’s readiness to implement rate cuts, emphasizing a data-dependent approach. Additionally, remarks from Atlanta Fed President Raphael Bostic advocating for a rate cut in the final quarter of 2024 further weighed on the USD. Market participants are expected to closely monitor the release of US Initial Jobless Claims for the week ending on March 29, scheduled for Thursday.

CRUDE OIL – WTI nears multi-month peak, hovers above $85.00/barrel

The Crude Oilmarket seems higher due to middle east conflict rising fears after the attack of Iran embassy in Syria. OPEC+ meeting outcome is no change in output cuts and pushed other nations to cut with their level. Chinese data doing performance well is additional support for Crude oil exports. US and China is doing well means then Oil demand will be picked up and no supply issue will come.

XTIUSD Crude Oil price is moving in an Ascending channel and the market has reached the higher low area of the channel.

During the Asian session on Thursday, West Texas Intermediate (WTI) US Crude Oil prices embarked on a bullish consolidation phase. They exhibited slight fluctuations within a narrow trading band, hovering close to the highest level since October 2023, which was attained the previous day. Currently, the commodity is positioned just above the $85.00 mark, experiencing minimal change for the day. This stability is attributed to a confluence of factors exerting influence on the market.

The official report released by the Energy Information Administration (EIA) on Wednesday revealed an unexpected increase in US Crude stockpiles. This development is perceived as a significant factor impeding the progress of the commodity, often referred to as the “black liquid.” However, despite this bearish indicator, the downward pressure on Crude Oil prices is mitigated by prevailing concerns regarding potential supply disruptions in the Middle East, coupled with a global supply deficit and indications of an uptick in demand. These factors collectively support the market sentiment and contribute to the resilience of Crude Oil prices.

Amid Ukrainian attacks on Russian refineries disrupting fuel supply and the potential expansion of the Israel-Hamas conflict to involve Iran, concerns over supply disruptions in the Middle East are bolstering Crude Oil prices. Furthermore, a recent meeting of top OPEC+ ministers maintained oil supply policy unchanged while urging some nations to enhance compliance with output cuts.

Meanwhile, Federal Reserve Chair Jerome Powell adopted a cautious stance on future interest rate cuts, citing the resilience of the US economy. Additionally, optimistic Chinese manufacturing data, released earlier in the week, has fueled expectations of increased Oil demand from the world’s largest crude importer. This positive outlook could provide further support to Crude Oil prices and help mitigate any significant corrective downturns.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/