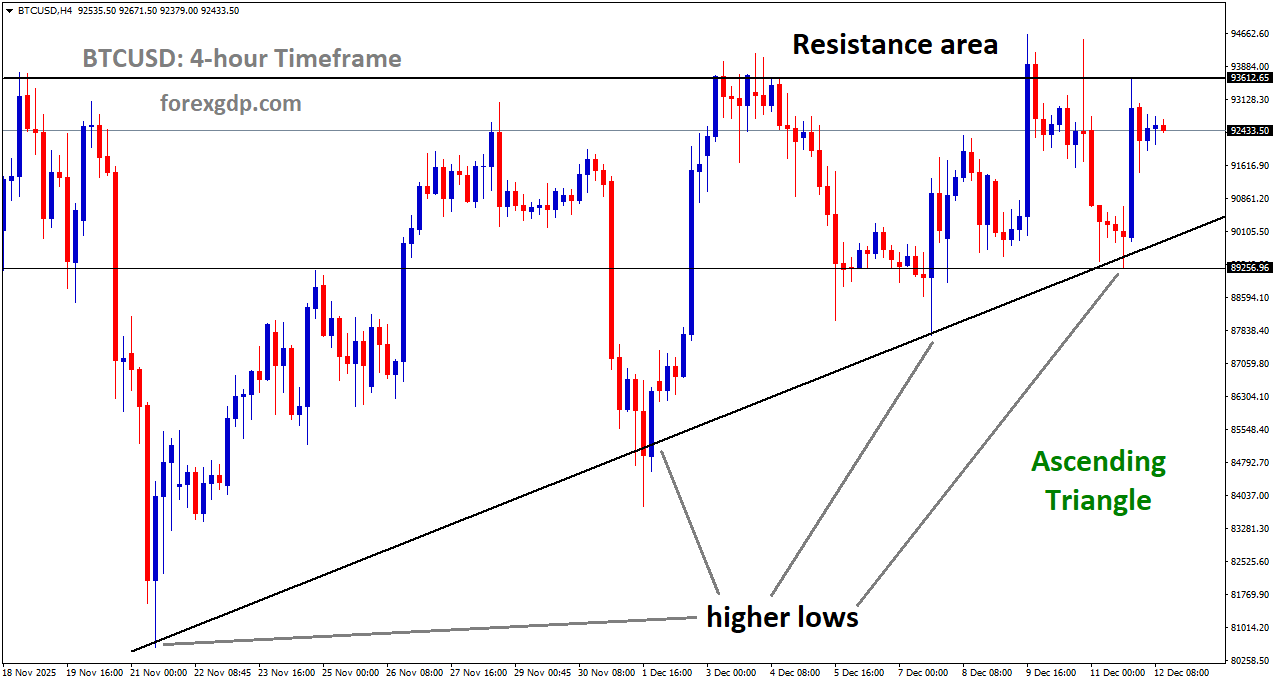

BTCUSD is moving in an Ascending Triangle pattern, and the market has reached the resistance area of the pattern

BTCUSD: The Fed Acts, Crypto Markets Shrug It Off

Bitcoin has been moving sideways for much of the week, as traders and long-term holders try to make sense of a changing macro backdrop. After a brief push higher early in the week, the market cooled down following the latest Federal Reserve meeting. That shift in tone has kept many investors cautious, especially those who tend to treat crypto as a “risk-on” asset that performs best when money is cheap and confidence is high.

Even with this hesitation, Bitcoin has not broken down in any dramatic way. Instead, it has stayed in a broad consolidation zone, hovering around the low $90,000s at the end of the week. That type of pause is common after a strong move, and it often reflects a market searching for its next big reason to trend—either up or down.

At the same time, there are signs that bigger players have not lost interest. Spot Bitcoin ETFs saw mild inflows, and Strategy increased its Bitcoin holdings again with another large purchase. Together, these developments paint a picture of a market that is cautious in the short term, but not necessarily bearish in the bigger view.

Why the Federal Reserve’s Tone Matters for Bitcoin

The Federal Reserve made a widely expected decision to cut rates by a small amount in December. On the surface, a rate cut can sound like good news for markets. But what mattered more this week was the message around what might happen next.

Investors were listening closely for hints about the pace of future cuts. The Fed’s guidance suggested a slower, more careful approach than some traders hoped for. When markets expect faster rate cuts and then hear a more reserved outlook, it can quickly shift the mood. That often leads to a “wait and see” phase across risk assets—including Bitcoin.

Bitcoin began the week with strength and held above a key level early on. But after the Fed meeting, momentum faded and the price slipped, showing how sensitive the crypto market still is to central bank communication. There was a dip midweek, followed by a rebound that helped Bitcoin recover back into its recent range by Thursday.

What happens next without major data releases

With no major US economic reports immediately ahead, attention typically moves to other signals. This includes comments from Fed officials in speeches and interviews, plus broader market sentiment in stocks and bonds. When the calendar is light, markets sometimes drift—especially when traders don’t feel pressured to make bold bets.

For Bitcoin, that could mean continued consolidation unless a strong catalyst appears. And in a market like crypto, catalysts can come from many places: regulation headlines, ETF demand, major corporate moves, or sudden shifts in global risk appetite.

Geopolitical Tension Keeps Risk Appetite in Check

Beyond interest rates, global uncertainty can also shape how investors behave. This week, the ongoing Russia-Ukraine situation remained a background pressure on market confidence.

Reports suggested frustration in the US over stalled progress, while comments from Ukraine’s leadership pointed to disagreements over what a potential deal could require. When geopolitical tension stays unresolved, investors often become more defensive. That doesn’t always cause a sharp sell-off, but it can reduce the willingness to chase rallies.

For Bitcoin, this matters because it often trades like a global risk asset during uncertain periods. When investors feel confident, Bitcoin can benefit from stronger risk-taking. When uncertainty rises, even strong markets can pause as traders reduce exposure and wait for clarity.

Why this leads to consolidation instead of a big drop

It’s important to note that uncertainty doesn’t always mean panic. Sometimes it simply means hesitation. This week’s behavior fits that pattern: some selling pressure appeared during moments of risk-off sentiment, but buyers also stepped in quickly enough to prevent a deeper slide.

Institutional Activity Adds Supportive Signals

While day-to-day price moves can be driven by sentiment, institutional activity often shapes the medium-term story. This week offered two key signals that larger buyers are still active: mild inflows into spot Bitcoin ETFs and another sizeable purchase from Strategy.

Spot Bitcoin ETFs in the US recorded net inflows across the week after a prior week of modest outflows. That shift suggests that some institutional investors are still allocating to Bitcoin, even if the pace is not aggressive. These inflows were not as large as some of the stronger periods seen earlier in the year, but the direction matters. In markets, improving flow trends can help stabilize price action.

Why ETF flows get so much attention

Spot ETFs are often seen as a bridge between traditional finance and Bitcoin. When inflows rise, it can signal that professional investors are warming up. When outflows dominate, it can show caution or profit-taking. Even small changes can influence sentiment because ETFs have become a highly visible measure of demand.

On the corporate side, Strategy added another large chunk of Bitcoin to its holdings. The company has built a reputation for treating Bitcoin as a major treasury asset, and it continues to accumulate. This kind of buying doesn’t guarantee price gains, but it does reinforce the idea that some corporate players see Bitcoin as a long-term store of value.

There is also ongoing discussion about Strategy’s ability to raise more capital, which could potentially support additional future buying. Whether that happens quickly or slowly, the market tends to watch these updates closely because they represent consistent demand from a high-profile buyer.

A Key Chart Level Is Becoming the Next Big Talking Point

As Bitcoin moves sideways, traders naturally look for technical areas that might shape the next move. One of the main focus points right now is a descending trendline that Bitcoin is approaching. In simple market terms, this is an area where price has struggled to push higher in recent attempts.

If Bitcoin breaks above that kind of level and holds, it can shift market psychology. Traders who were waiting may step in, short sellers may back off, and momentum can build. On the other hand, if Bitcoin fails to break through and gets rejected again, the market may stay stuck in its range for longer.

What makes this setup interesting is the timing: macro investors are cautious, but institutional participation has not disappeared. That combination often leads to a market that feels tense but stable—like it’s coiling and waiting for a clearer direction.

What could push Bitcoin out of this range

Several developments could act as a trigger:

-

A noticeable increase in spot Bitcoin ETF inflows over multiple days

-

A meaningful shift in market expectations about future Fed policy

-

A calming of geopolitical headlines that improves risk sentiment

-

Another wave of corporate accumulation that changes the supply-demand balance

None of these are guaranteed, but they represent the types of catalysts that can turn consolidation into a directional move.

Summary

Bitcoin is spending the week in a consolidation phase as investors react to the Federal Reserve’s cautious messaging on future rate cuts. Global geopolitical uncertainty has also limited risk-taking, keeping traders more careful than usual. Even so, institutional signals are mildly supportive, with spot Bitcoin ETFs showing improved flows and Strategy adding more Bitcoin to its treasury. As Bitcoin nears a closely watched descending trendline, the market appears to be waiting for a stronger catalyst that can determine whether the next move is a renewed rally or an extended period of sideways trading.

EURUSD ticks lower as markets stay steady and the US dollar remains soft

The euro has taken a small step back against the US dollar after reaching its strongest point in more than two months earlier in the week. After several days of steady gains, traders appear to be taking a pause. This mild retreat does not signal a major change in direction, but it does suggest that the recent rally may be losing some energy.

Even with this short-term dip, the broader picture still favors the euro. The main driver continues to be the growing difference in how the European Central Bank and the US Federal Reserve are handling monetary policy. This gap has kept the US dollar under pressure and has helped limit losses for the euro.

EURUSD has broken the uptrend channel on the downside

Rather than a sharp reversal, the current move looks more like a natural breather. Markets often slow down after a strong advance, especially when investors wait for fresh news or confirmation from policymakers.

Central Bank Policies Shape Market Sentiment

One of the biggest forces influencing the euro and the dollar right now is the clear split in policy direction between the ECB and the Fed. While both central banks are focused on managing inflation and economic growth, they are moving at different speeds.

The US Federal Reserve recently lowered interest rates and signaled that only limited easing may be needed further down the road. Despite this message, many investors believe that the Fed may still be pushed to act more aggressively. This belief is tied to signs of cooling in the US economy and expectations of a leadership change that could favor lower borrowing costs.

Jerome Powell’s term as Fed Chair is widely discussed in political and financial circles. Market participants are increasingly focused on Kevin Hassett, a well-known economic adviser to the White House, who is often described as supportive of looser monetary conditions. This possibility has added to expectations that US rates could fall more than the Fed currently suggests.

In contrast, the European Central Bank is approaching policy easing more cautiously. While inflation in the euro area has shown signs of easing over time, recent data suggests that price pressures are not fully under control. This has allowed the ECB to maintain a steadier stance, which supports the euro when compared to the dollar.

US Dollar Weakness Supports the Euro

The euro’s ability to stay resilient, even during pullbacks, is closely tied to broad weakness in the US dollar. The dollar has struggled as investors continue to factor in the likelihood of additional rate cuts in the United States.

Many major central banks around the world are nearing the end of their easing cycles. The Fed stands out because markets believe it still has more work to do. This difference has reduced demand for the dollar and made alternative currencies, including the euro, more attractive.

US economic data has also played a role in shaping this view. Recent figures on employment have raised concerns about the strength of the labor market. A notable rise in new claims for unemployment benefits has added to worries that job growth may be slowing faster than expected.

When labor market conditions weaken, central banks often respond by making credit cheaper to support growth. This has reinforced the idea that the Fed may need to take further action, keeping pressure on the dollar and helping the euro hold its ground.

Inflation Data From Germany Offers Mixed Signals

On the European side, inflation data from Germany has drawn attention but failed to spark a strong market reaction. Consumer price figures confirmed that annual inflation picked up in November compared to the previous month. At the same time, prices fell on a monthly basis.

This mixed outcome suggests that inflation pressures are still present but not moving in a straight line. Because the figures matched earlier estimates, traders did not see a reason to significantly adjust their expectations for ECB policy.

Germany’s inflation data is closely watched because it often sets the tone for the broader euro area. While the recent increase in yearly inflation may encourage caution at the ECB, the monthly decline shows that price growth is not running out of control.

As a result, the euro remained stable following the release. Investors appear comfortable with the idea that the ECB can afford to move slowly and avoid rushing into aggressive rate cuts.

Focus Turns to US Policymakers

Attention is now shifting toward comments from several US Federal Reserve officials. Policymakers from different regional Fed banks are scheduled to speak, offering their views on the economy, inflation, and future policy steps.

These speeches matter because they can help clarify whether the central bank is leaning toward further easing or planning to hold steady. Even small changes in tone can influence expectations and, in turn, affect currency markets.

Investors will be listening closely for any acknowledgment of weakening economic conditions, especially in the labor market. If officials emphasize caution or express concern about growth, it could strengthen the case for additional rate cuts.

On the other hand, if policymakers stress patience and confidence in the current outlook, the dollar may find some short-term support. Until then, uncertainty is likely to keep the euro-dollar pair moving in a tight range.

A Market Pausing, Not Reversing

After a solid climb over recent weeks, the euro’s latest pullback looks more like a pause than a shift in trend. Momentum has slowed, but the fundamental drivers that supported the rally are still in place.

The contrast between a cautious ECB and a potentially more accommodative Fed remains a key theme. As long as investors believe US rates have further room to fall, the dollar may continue to struggle.

At the same time, the euro faces its own challenges. Economic growth in parts of the euro area remains uneven, and inflation developments will continue to influence ECB decisions. These factors could limit how far and how fast the euro can rise.

For now, markets appear content to wait for clearer signals from policymakers and upcoming economic data before making their next big move.

Final Summary

The euro has eased slightly after a strong run, but underlying support remains intact. The main force behind this resilience is the widening gap between US and European monetary policy, which has weighed on the dollar. Expectations of further easing by the Federal Reserve, combined with signs of a cooling US labor market, have kept pressure on the greenback. Meanwhile, steady but mixed inflation data from Germany has allowed the ECB to maintain a careful stance. With several US policymakers set to speak, investors are watching closely for clues on the next phase of monetary policy, while the euro continues to hold firm despite short-term pauses.

GBPUSD weakens as UK output dips again, extending the slowdown

The Pound Sterling lost ground against many major currencies on Friday after new data showed the UK economy is still struggling to find its footing. The latest Gross Domestic Product (GDP) report revealed that the UK economy contracted by 0.1% in October, marking the second month in a row of shrinking activity. Markets had been looking for a small rise, so the surprise drop quickly put pressure on the Pound.

When GDP turns negative for back-to-back months, it sends a clear message: growth is weak, and confidence can fade fast. That matters for currency markets because investors often prefer countries that show steady expansion and stable momentum. When the numbers disappoint, money can flow elsewhere.

GBPUSD reached the retest area of the broken symmetrical Triangle

At the same time, the UK’s weak GDP reading is creating a bigger story—one that could shape the Pound’s direction in the days ahead: expectations are rising that the Bank of England (BoE) may cut interest rates at its next policy meeting.

What the Latest GDP Reading Really Signals

A monthly GDP figure might sound like a small data point, but it often sets the tone for how investors think about an economy. In this case, the numbers raised fresh concerns that the UK is moving through a sluggish patch that isn’t ending quickly.

The October GDP report showed the economy fell by 0.1%, while forecasts suggested it would grow by 0.1%. That may look like a narrow miss, but the direction is what mattered most. Growth turning negative again suggests that demand is soft, business activity may be slowing, and households could be feeling pressure from higher living costs and tighter financial conditions.

Why this conflicts with earlier optimism

This new contraction also stands out because it goes against a recent upgrade from the Office for Budget Responsibility (OBR). The OBR had raised its growth forecast for the current year, projecting 1.5% growth instead of the 1.0% estimate it made earlier in the year.

When official projections improve but real-world data weakens, investors often start questioning whether the optimism was premature. That disconnect can be uncomfortable for markets, especially when central bank decisions are just around the corner.

Rate Cut Expectations Grow Ahead of the Bank of England Meeting

Weak growth doesn’t just hurt sentiment—it changes the policy debate. If the economy is shrinking, central banks are more likely to consider easing financial conditions to support activity. That is why the latest GDP report is feeding expectations that the BoE could cut interest rates at its upcoming meeting.

Traders are already leaning toward a quarter-point cut, which would bring the main rate down to 3.75%. While the final decision is never guaranteed, the GDP data strengthens the argument for action. A slowing economy can reduce inflation pressure over time, which gives policymakers more room to lower rates.

Why rate cuts often weigh on a currency

Interest rates matter for currencies because they influence global investment flows. When rates are higher, investors may earn more by holding assets in that currency. When rates are expected to fall, that advantage can shrink, and the currency may look less attractive compared with others.

So even before the BoE announces anything, the expectation of easier policy can weaken the Pound as traders adjust positions ahead of time.

Mixed Signals Inside the Report: Industry Shows Some Improvement

While GDP was the main headline, other parts of the report offered a more mixed picture. Some industrial figures surprised to the upside, suggesting that not all areas of the economy are moving in the same direction.

Industrial Production rose by 1.1% in October compared with the previous month, beating expectations of a smaller increase. That’s notable because September’s reading was a steep decline, so October’s rebound suggests there was at least some recovery in output.

On a yearly basis, Industrial Production still fell, but the decline was less severe than expected. That kind of “less bad” result can matter, because it hints that the industrial side of the economy may be stabilizing even if overall growth remains weak.

Manufacturing Production, however, told a slightly different story. It increased, but not as strongly as hoped. After a previous drop in September, markets were looking for a stronger bounce. A softer manufacturing rebound can be read as a sign that higher costs and uncertain demand are still holding back factory activity.

What investors may take from the mixed data

When GDP is weak but parts of industry improve, the market message becomes nuanced. Investors may see an economy that is not collapsing, but also not strong enough to feel comfortable. That kind of “stuck in the middle” outlook often keeps currencies under pressure because it creates uncertainty about what comes next—especially from central banks.

GBP/USD Reaction: The US Dollar Side of the Story Matters Too

Even though the UK data pushed the Pound lower, the broader move in the GBP/USD pair has also been shaped by what’s happening in the United States. The US Dollar has been softer lately after the Federal Reserve delivered a rate cut and signaled a path that markets did not fully expect.

In the latest decision, the Fed reduced rates by a quarter-point and indicated that there could be one more cut in 2026. Comments from the Fed also added to the sense that inflation could peak in early 2026 if no new tariffs are introduced. That guidance weighed on the Dollar because many investors had expected a tougher stance—one that would suggest fewer cuts unless inflation risks clearly improved.

US political messaging has added another layer as well, with President Donald Trump calling for further rate cuts after the Fed meeting, according to remarks reported by Reuters through White House spokeswoman Karoline Leavitt. When markets hear mixed signals—central bank caution on one side, political pressure on the other—it can create volatility in the Dollar and ripple through currency pairs like GBP/USD.

Key Data Next Week That Could Shape the Pound’s Direction

With growth shrinking and rate expectations rising, the next wave of economic updates will be closely watched. Several UK releases scheduled for next week could influence the Pound by shifting expectations around inflation, jobs, and business activity.

UK labour market data

Employment numbers for the three months ending October will matter because the job market has been a key support for consumer spending. If hiring slows or unemployment rises, it could strengthen the case for rate cuts. If the labour market holds up better than expected, it could calm some of the pressure on the Pound.

UK inflation update

The UK Consumer Price Index (CPI) data for November will be another major focus. Inflation trends can either give the BoE confidence to cut rates or force it to stay cautious. If inflation cools faster than expected, rate cut expectations could grow. If inflation stays sticky, the BoE might hesitate.

UK business activity snapshot

Preliminary S&P Global Purchasing Managers’ Index (PMI) figures for December will provide an early read on whether businesses are seeing improvement or further slowdown. PMIs can move markets quickly because they offer a timely look at momentum before broader data is published.

US Employment Data: A Major Trigger for the Dollar and Global Markets

Across the Atlantic, US employment data will be one of the most important drivers for currency markets. The US Nonfarm Payrolls (NFP) report for November is expected to heavily influence expectations for the Fed’s next steps.

The reason is simple: one major factor behind the Fed’s rate cuts has been signs of weakening labour demand. If job growth comes in strong, markets could rethink how quickly rates might fall. If jobs data shows weakness, it could reinforce expectations of easier policy and keep the Dollar under pressure.

Because GBP/USD is influenced by both sides of the equation, next week’s job reports—UK and US—may set the tone for where the pair goes next.

Final Summary

The Pound Sterling weakened after the UK economy contracted by 0.1% in October, extending a second straight month of decline and missing expectations for growth. That renewed weakness is strengthening market bets that the Bank of England may cut rates at its upcoming meeting, a shift that often weighs on a currency. While parts of industrial output improved, the overall picture remains uncertain. Next week brings key updates on UK jobs, inflation, and business activity, alongside critical US employment data, which could reshape expectations for both the BoE and the Federal Reserve—and drive the next major move in the Pound.