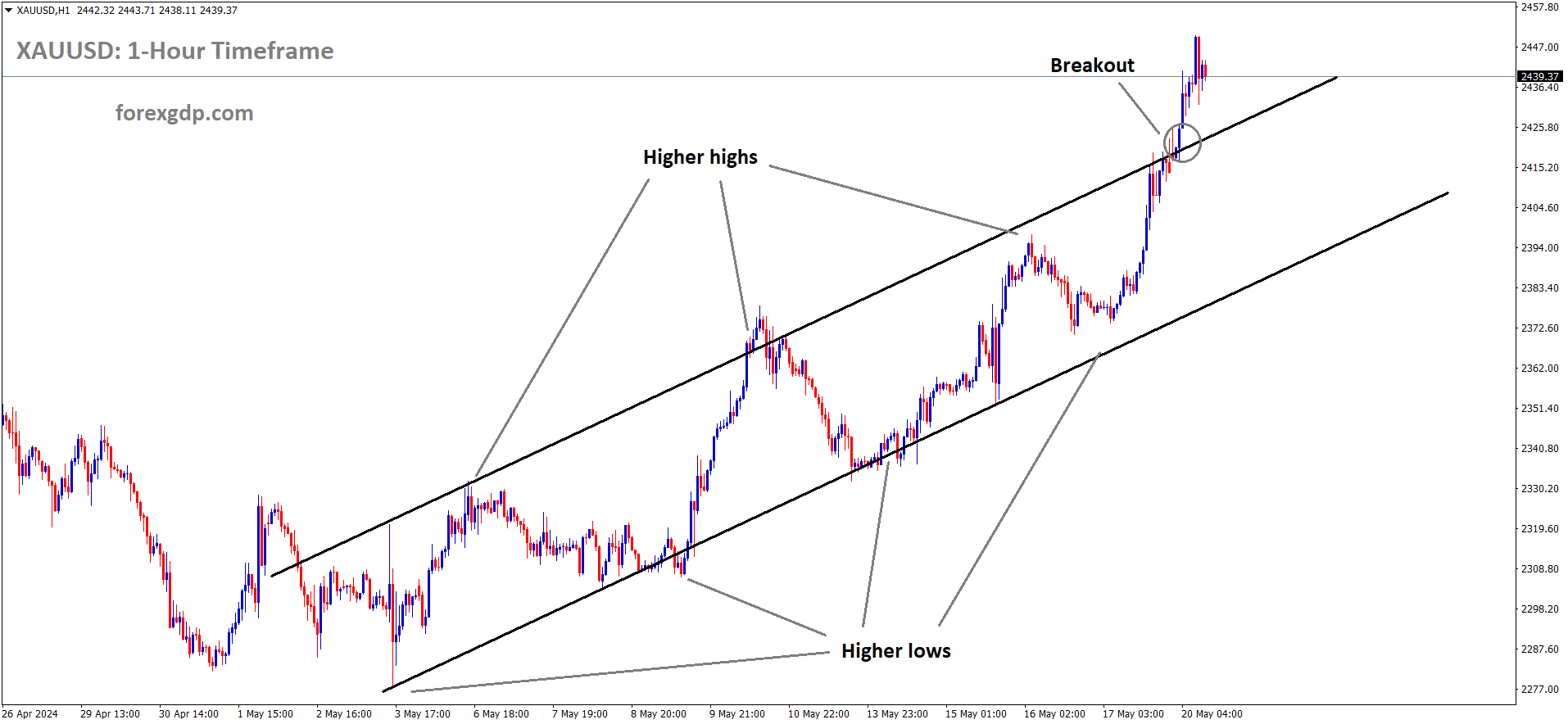

BTCUSD is moving in a descending channel, andthe market has rebounded from the lower low area of the channel

BTCUSD Struggles in Q1 With Heavy Losses, Is History Repeating Itself?

Bitcoin is going through a challenging start to the year. Recent data shows that the world’s largest cryptocurrency has dropped more than 22% since January began. If this trend continues, it could mark Bitcoin’s weakest first quarter performance in nearly eight years.

The year started on a strong note, with Bitcoin trading near $87,700. However, the asset has since fallen by roughly $20,000, sliding to around $68,000. This sharp decline has raised concerns among investors and analysts, especially as it puts Bitcoin on track for its worst first quarter since the 2018 bear market.

Back in 2018, Bitcoin experienced a dramatic fall of nearly 50% during the first three months of the year. While the current decline is not as severe, the comparison highlights how difficult the opening months of a year can be for the cryptocurrency market.

A History of Volatile First Quarters

Bitcoin’s performance during the first quarter has often been unpredictable. In fact, out of the past thirteen first quarters, Bitcoin has finished in the red seven times. That means losses in Q1 are not unusual.

Some recent examples stand out. In 2025, Bitcoin fell by 11.8% in the first quarter. In 2020, it dropped by 10.8%. The steepest decline remains 2018, when it plunged nearly 49.7% in just three months.

Market analysts frequently point out that the first quarter is known for its volatility. Price swings can be sharp, and investor sentiment can shift quickly. Because of this, what happens early in the year does not always set the tone for the rest of it.

Historically, Bitcoin has shown that weak starts do not necessarily lead to weak finishes. There have been several cases where the cryptocurrency struggled early on but recovered later in the year.

Two Consecutive Losing First Quarters Are Rare

Interestingly, Bitcoin has only recorded back-to-back first-quarter losses during major bear market years. This happened in 2018 and again in 2022. Outside of those periods, the asset has generally avoided consecutive Q1 downturns.

This context matters because it shows that sustained weakness in the first quarter is not common unless the broader market is already under heavy pressure.

January and February: A Rare Double Decline

Another unusual trend is developing. Bitcoin may be on track to post its first-ever consecutive January and February losses.

So far this year, Bitcoin dropped 10.2% in January and has fallen another 13.4% in February. If it fails to recover before the month ends, this would mark the first time both months have closed in negative territory back-to-back.

For that to change, Bitcoin would need to climb back above the $80,000 level before February closes. Without such a rebound, the red streak will remain intact.

While short-term monthly performance can grab headlines, it is important to remember that Bitcoin has experienced similar rough patches before and later regained momentum.

Ethereum Also Feeling the Pressure

Bitcoin is not alone in facing losses. Ethereum, the second-largest cryptocurrency, has also struggled this quarter.

ETHUSD is moving in an uptrend channel, and the market has reached the higher low area of the channel

Out of the past nine first quarters, Ethereum has only finished in the red three times. However, the current period is shaping up to be one of its worst. So far, Ethereum has dropped by more than 34%.

This puts the current quarter among Ethereum’s weakest historical performances. While Ethereum’s market dynamics differ from Bitcoin’s, both assets are feeling the impact of broader market uncertainty.

Why Crypto Markets Move This Way

Cryptocurrency markets are highly sensitive to global economic conditions. Factors such as inflation concerns, interest rate decisions, geopolitical tensions, and regulatory developments can all influence investor behavior.

When uncertainty rises, investors often reduce exposure to riskier assets. Cryptocurrencies, despite their growing adoption, are still considered high-risk by many market participants. As a result, they tend to experience sharper swings during periods of global stress.

Is This a Correction or Something Bigger?

Some market experts believe the current downturn is simply a correction rather than a long-term problem.

A correction is a temporary drop after a strong run-up. It allows markets to reset and shake out excessive optimism. According to research analysts, Bitcoin’s recent decline may reflect this normal cycle rather than a deeper structural issue.

They argue that Bitcoin’s long-term outlook remains supported by continued institutional interest and the broader adoption of digital assets. Additionally, Bitcoin’s halving cycle, which reduces the rate at which new coins are created, has historically played a role in shaping long-term trends.

While short-term pressure could continue if global economic uncertainty remains high, history suggests that Bitcoin has often demonstrated resilience after challenging periods.

Five Weeks of Consecutive Losses

Bitcoin has now entered its fifth straight week of losses. This extended streak has added to investor concerns.

Over the past 24 hours alone, Bitcoin fell another 2.3%, trading around $68,670 at the time of reporting. Consecutive weekly declines are not common during strong bull markets, which makes this period stand out.

However, long-term observers of the crypto market know that multi-week downturns are not unusual. Bitcoin has experienced several extended pullbacks in the past, even during broader upward cycles.

Short-Term Pain vs. Long-Term Trends

It is important to separate short-term volatility from long-term trends. Bitcoin’s history is filled with sharp declines followed by powerful recoveries.

In earlier cycles, dramatic pullbacks often created fear among investors. Yet over time, the asset managed to regain strength and reach new highs.

This pattern does not guarantee future performance, but it does highlight the unique nature of the cryptocurrency market. Rapid gains and rapid losses are both part of the journey.

What Investors Are Watching Now

At the moment, investors are closely watching several factors:

-

Global economic stability

-

Central bank policies

-

Institutional adoption trends

-

Broader crypto market sentiment

Any positive shift in these areas could help restore confidence. On the other hand, continued economic uncertainty may keep pressure on digital assets in the short term.

Despite the recent downturn, many long-term holders remain focused on Bitcoin’s broader narrative as a decentralized digital asset with limited supply.

Final Thoughts

Bitcoin’s current first-quarter performance is among the weakest in recent years, with losses exceeding 22% since the start of the year. The asset has fallen sharply from its early-year levels and is experiencing rare back-to-back monthly declines in January and February.

History shows that the first quarter is often volatile, and past performance suggests that early-year weakness does not always determine the outcome for the rest of the year. Both Bitcoin and Ethereum are facing pressure, largely influenced by global economic uncertainty.

While short-term challenges remain, Bitcoin has repeatedly shown resilience throughout its history. Whether this period turns into a deeper downturn or simply a temporary correction will depend on how economic and market conditions evolve in the months ahead.

EURUSD Stays Stable as Euro Area Manufacturing Slows

The EUR/USD currency pair is starting the week on a calm note, hovering near the 1.1865 level. With major financial centers operating at reduced activity due to public holidays, trading has been relatively quiet. Investors are watching recent economic data from both the Eurozone and the United States, but for now, neither side is making a strong move.

EURUSD is rebounding from the retest area of the broken symmetrical triangle pattern

The latest updates on Eurozone industrial production and softer inflation data from the United States are shaping market sentiment. However, low trading volumes are keeping price movements limited. As a result, the euro and the US dollar remain closely matched at the start of the week.

Eurozone Industrial Production Shows Noticeable Decline

Fresh economic data from the Eurozone revealed that industrial production fell sharply in December. Factory output dropped by 1.4% compared to the previous month. This result was largely in line with expectations, as analysts had predicted a similar decline after November’s modest growth.

November’s production increase was also revised lower, adding to concerns about the region’s economic momentum. While output had previously been reported as stronger, updated figures show that the recovery was not as solid as first believed.

On a yearly basis, industrial production grew by 1.2% in December. Although this still represents growth compared to the previous year, it slowed down from November’s stronger pace. Economists had expected slightly better yearly growth, so the data suggests that the Eurozone’s manufacturing sector is facing some headwinds.

Industrial production is an important indicator because it reflects the health of factories and manufacturing companies. When production falls, it can signal weaker demand, supply chain issues, or broader economic challenges. However, since the decline matched market expectations, the euro did not experience a sharp reaction.

US Inflation Data Weighs on the Dollar

While Eurozone data provided little surprise, recent developments in the United States are also influencing the EUR/USD pair. Last week’s Consumer Price Index (CPI) report showed softer inflation than expected. This has reduced pressure on the US Federal Reserve to keep borrowing costs high.

Lower inflation can encourage the Federal Reserve to consider easing monetary policy. When borrowing costs are reduced, it can support economic activity, especially in sectors like housing and employment. However, a more relaxed approach to interest rates can also weaken the US dollar.

The softer inflation figures have acted as a headwind for the dollar’s recent recovery. Investors now believe there is more room for policymakers to support the economy if needed. As a result, the US dollar has struggled to gain strong upward momentum against the euro.

Even so, the euro has not been able to capitalize fully on this situation. Despite the softer US inflation data, the common currency failed to build strong gains. This suggests that traders are still cautious and waiting for clearer signals about future economic trends.

Holiday Closures Keep Trading Activity Subdued

One of the key reasons behind the limited movement in EUR/USD is the reduced trading activity. Many Asian markets, including Japan, remained closed due to the Lunar New Year holiday. In addition, US markets are observing the President’s Day holiday.

When major markets are closed, trading volumes tend to drop significantly. Fewer participants in the market mean fewer transactions and less price movement. Even important economic data may have a muted impact under these conditions.

With both Asia and the United States largely offline, European trading has been quieter than usual. Investors are likely holding off on large positions until full market participation resumes later in the week.

Central Bank Speeches Could Offer Direction

Although the overall session remains calm, investors are paying attention to upcoming speeches from key policymakers. Comments from the Federal Reserve’s Vice Chair for Supervision, Michelle Bowman, and European Central Bank Governor Joachim Nagel could provide fresh insights.

Central bank officials often influence markets through their remarks. Traders listen carefully for any hints about future policy decisions, economic outlooks, or inflation concerns. Even small changes in tone can shift expectations.

For now, however, the market appears to be in a holding pattern. Investors are likely waiting for stronger signals before making significant moves. A busier week of economic data lies ahead, which could bring more volatility.

Broader Economic Picture Remains Mixed

The current situation reflects a mixed economic environment on both sides of the Atlantic.

In the Eurozone, industrial production data highlights ongoing challenges in the manufacturing sector. Slowing growth may point to softer demand, both domestically and globally. European economies have been dealing with various pressures, including energy costs, supply chain adjustments, and global trade uncertainties.

At the same time, the United States is showing signs of cooling inflation. While this may ease pressure on consumers and businesses, it also changes expectations for monetary policy. The Federal Reserve must balance supporting economic growth with keeping inflation under control.

Because both economies face their own challenges and uncertainties, neither currency has gained a decisive advantage. This balance helps explain why EUR/USD remains largely unchanged.

What Traders Are Watching Next

With a quiet start to the week, attention is already shifting to upcoming economic releases. A busier calendar in the days ahead could provide clearer direction for the currency pair.

Investors will likely monitor fresh data on growth, inflation, and employment from both regions. These indicators help shape expectations about future interest rate decisions and overall economic strength.

If new data shows stronger growth in the Eurozone, the euro could find additional support. On the other hand, stronger US data might help the dollar regain momentum. Much will depend on how the numbers compare to market expectations.

Until then, the EUR/USD pair may continue to trade within a narrow range, especially if market participation remains moderate.

Investor Sentiment Remains Cautious

Another factor influencing the market is overall investor sentiment. Many traders prefer to stay cautious ahead of key data releases. Entering large positions before important announcements can carry higher risk.

When uncertainty is high, currency pairs often consolidate rather than trend strongly in one direction. This seems to be the case for EUR/USD at the moment.

The lack of strong reaction to recent data suggests that investors are waiting for more convincing evidence before committing to a clear direction. Stability, at least temporarily, appears to be the dominant theme.

Final Summary

The EUR/USD pair is holding steady near 1.1865 as trading activity remains limited due to public holidays in major financial centers. Eurozone industrial production fell in December, confirming expectations of a slowdown in factory output. Meanwhile, softer US inflation data has reduced pressure on the Federal Reserve and limited the dollar’s recovery.

With markets operating at reduced capacity, price movements have been modest. Investors are now looking ahead to upcoming economic releases and central bank commentary for clearer guidance. Until stronger signals emerge, the euro and the US dollar are likely to remain closely balanced in a calm and cautious market environment.

USDCAD Moves Sideways Above 1.3600 as Presidents’ Day and Family Day Calm Markets

The USD/CAD currency pair started the week with only minor movement, as financial markets in both the United States and Canada observed public holidays. With US Presidents’ Day and Canada’s Family Day keeping many traders away from their desks, overall activity remained quiet. Lower trading volumes often lead to smaller price swings, and that has been the case for the Canadian Dollar and the US Dollar.

USDCAD is moving in a descending channel

Even though the pair edged slightly lower after three straight days of gains, there was no major shift in direction. Instead, investors are taking a cautious approach while waiting for fresh economic data and watching important global events unfold.

Holiday Trading Keeps USD/CAD in a Tight Range

When major financial centers close for holidays, markets tend to slow down. That is exactly what happened with USD/CAD. With fewer participants involved, trading volumes dropped, limiting sharp movements.

The pair hovered near familiar levels during European trading hours, showing that investors were not willing to take strong positions. In thin trading conditions, even small trades can cause noticeable moves. However, in this case, the overall tone remained calm.

Market participants are now looking ahead to key economic reports that could offer clearer direction later in the week.

Focus Turns to Canada’s Inflation Data

One of the main events on traders’ radar is Canada’s upcoming Consumer Price Index (CPI) report. Inflation data plays a crucial role in shaping expectations about future interest rate decisions by the Bank of Canada.

Economists expect annual inflation in Canada to remain at 2.4% for January, unchanged from the previous month. On a monthly basis, inflation is projected to rise slightly after a decline in the previous reading.

Why Inflation Matters for the Canadian Dollar

Inflation figures help central banks decide whether to raise, hold, or cut interest rates. If inflation remains stable or increases, policymakers may be less inclined to lower rates. On the other hand, weaker inflation could open the door for more supportive measures.

For the Canadian Dollar, stronger inflation data could provide some support. However, if inflation softens more than expected, the currency may face pressure. For now, traders are waiting for the official numbers before making any big moves.

Oil Prices Remain Stable, Limiting CAD Momentum

The Canadian Dollar is often influenced by oil prices because Canada is a major oil exporter. When oil prices rise, the Canadian economy typically benefits, which can strengthen the currency. Conversely, falling oil prices often weigh on the Canadian Dollar.

At the moment, crude oil prices have remained mostly flat. With little change in energy markets, the Canadian Dollar has lacked a strong catalyst for movement.

Geopolitical Tensions Keep Energy Markets Cautious

Oil traders are paying close attention to ongoing geopolitical developments. Talks between the United States and Iran are scheduled to continue in Geneva, with signs that Iran may be willing to discuss nuclear concessions if certain sanctions are addressed.

At the same time, negotiations related to the Russia-Ukraine conflict are also set to resume. While these discussions are important, expectations for a quick breakthrough remain limited. As a result, oil markets have not reacted strongly.

The possibility of changes in global oil supply remains a key factor, but until there is clear progress, prices are likely to stay within a narrow range. This stability in oil has helped keep the Canadian Dollar relatively steady.

The US Dollar Faces Mixed Signals

While the Canadian Dollar waits for domestic data and oil market developments, the US Dollar is dealing with its own set of influences.

Recent US inflation data showed softer consumer price growth in January. This has strengthened expectations that the Federal Reserve could lower interest rates later this year. When investors believe interest rates may fall, the US Dollar often loses some support.

However, the picture is not entirely straightforward.

Strong Labor Market Offers Support

January’s Nonfarm Payrolls report showed the strongest job growth in more than a year. At the same time, the unemployment rate unexpectedly declined. These figures suggest that the US labor market remains solid and stable.

A strong labor market can make it harder for the Federal Reserve to justify cutting interest rates quickly. If the economy continues to show resilience, policymakers may prefer to wait before making any major changes.

This mix of softer inflation and strong employment data has created some uncertainty around the US Dollar’s direction. As a result, USD/CAD has struggled to establish a clear trend.

Investors Await Key US Economic Reports

Looking ahead, several important US economic reports could shape expectations about the Federal Reserve’s next steps.

The upcoming release of the Fed Meeting Minutes will offer insight into how policymakers are thinking about inflation, growth, and interest rates. Investors will look for clues about how close the central bank may be to adjusting policy.

In addition, fourth-quarter GDP data will provide a clearer picture of how the US economy performed at the end of last year. Strong growth could support the US Dollar, while weaker numbers may add to speculation about future rate cuts.

Another important release is the core Personal Consumption Expenditures (PCE) price index. This measure is the Federal Reserve’s preferred gauge of inflation. If core PCE shows continued cooling, expectations for rate cuts may increase.

A Wait-and-See Approach Dominates

With so many important events lined up, it is not surprising that traders are taking a cautious approach. Holiday conditions have already reduced trading activity, and many investors prefer to wait for fresh data before committing to larger positions.

The balance between US economic resilience and signs of slowing inflation is creating uncertainty. Meanwhile, Canada’s inflation data and oil price movements will play a key role in shaping the Canadian Dollar’s direction.

For now, USD/CAD remains in a holding pattern, moving slightly but lacking strong momentum in either direction.

Summary

USD/CAD has shown limited movement as markets observe holidays in both the United States and Canada. Lower trading volumes have kept price swings modest, while investors wait for new economic data.

Canada’s upcoming inflation report is expected to influence expectations about future policy decisions, while stable oil prices have kept the Canadian Dollar from making significant moves. On the US side, softer inflation data has increased hopes for potential rate cuts, but strong job growth has added complexity to the outlook.

With important reports such as the Fed Meeting Minutes, GDP data, and core PCE inflation still ahead, traders are likely to remain cautious. Until clearer signals emerge, USD/CAD may continue to trade without a strong directional push.