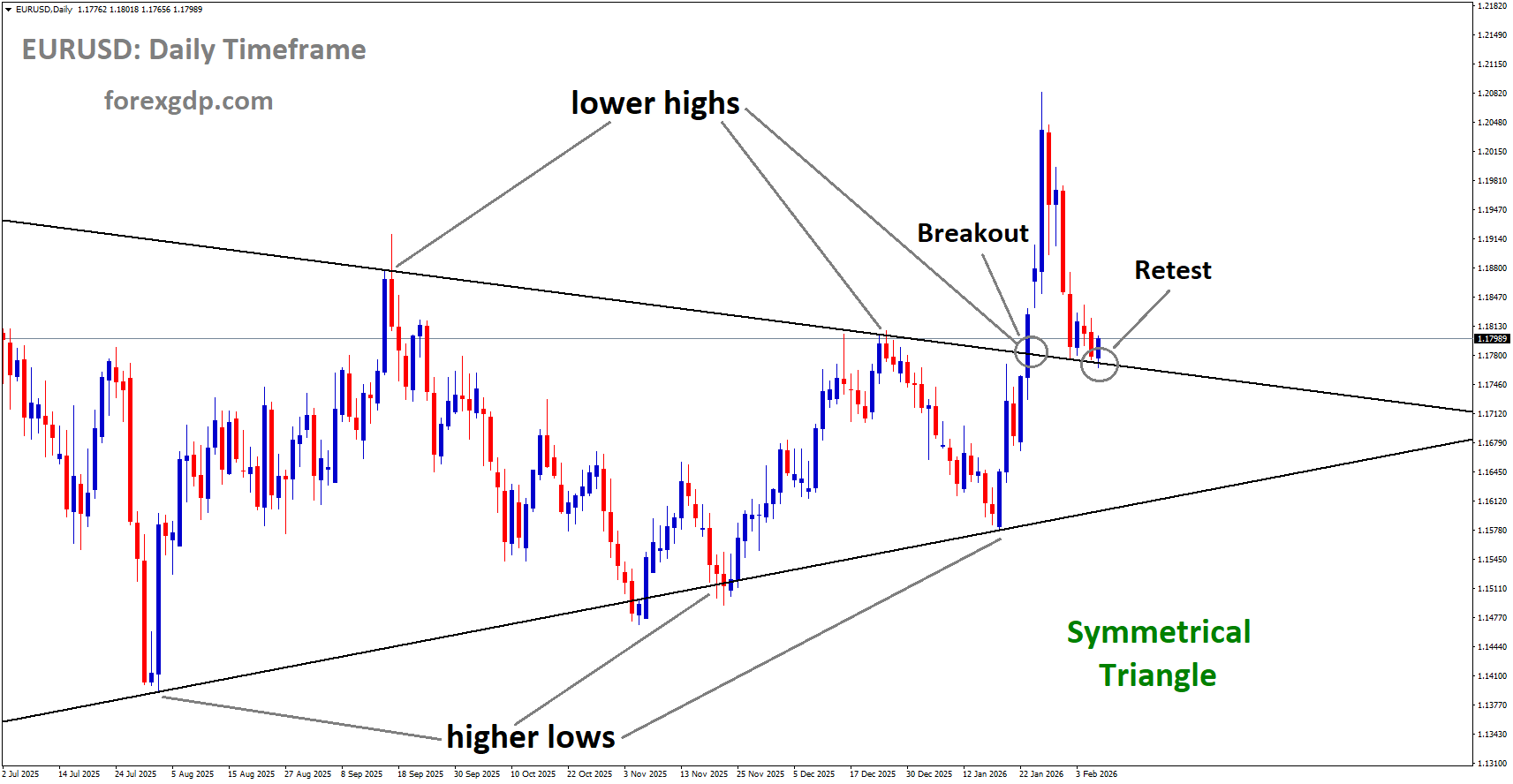

EURUSD reached the retest area of the broken symmetrical triangle pattern

EURUSD Struggles for Direction While Safe-Haven Demand Lifts the Dollar

The Euro managed to recover some ground against the US Dollar on Friday after slipping earlier in the day. While the single currency showed signs of stability, it continued to face clear limits as investors stayed cautious. A mix of global market anxiety, weak economic data from Germany, and steady signals from the European Central Bank shaped trading conditions.

Across financial markets, confidence remained fragile. Falling equity prices encouraged investors to seek safety, which supported the US Dollar. At the same time, disappointing industrial data from Europe’s largest economy added pressure on the Euro, preventing a stronger rebound.

This uneasy balance left currency traders focused on central bank guidance and upcoming US economic signals, both of which could influence market direction in the days ahead.

Risk-Off Mood Strengthens the US Dollar

Global markets have been in a defensive mood, and that has played a major role in supporting the US Dollar. Equity markets extended losses for a third straight session, with technology stocks leading the decline. Recent earnings reports have raised fresh doubts about heavy investment in artificial intelligence, prompting concerns that expectations may have run too far ahead of reality.

When stock markets struggle, investors often turn to safer assets. The US Dollar typically benefits from this shift, and that pattern has held true. Even though recent US economic data has not been particularly strong, the Dollar has continued to attract demand due to its safe-haven status.

Political developments have also influenced sentiment. The announcement that former Federal Reserve Governor Kevin Warsh was chosen to succeed Jerome Powell as Fed Chair reassured markets. Many investors see Warsh as a supporter of central bank independence and a cautious policymaker, which helped stabilize confidence in US monetary leadership.

This combination of risk aversion and political clarity has allowed the Dollar to remain firm, even as some domestic indicators point to a cooling labor market.

Weak German Data Weighs on the Euro

On the European side, fresh data out of Germany added another challenge for the Euro. Industrial production in December fell sharply, far more than analysts had expected. This setback followed a downward revision to the previous month’s figures, reinforcing concerns that Europe’s manufacturing sector remains under strain.

Germany is often seen as the economic engine of the Eurozone, so weak performance there tends to have a broad impact on regional sentiment. Sluggish factory output suggests that high borrowing costs and softer global demand are continuing to bite, especially in export-driven industries.

These disappointing numbers made it harder for the Euro to benefit from any weakness in the US Dollar. Instead, traders remained cautious, viewing the data as another sign that economic momentum in the Eurozone is fragile.

ECB Signals Steady Policy Path

The European Central Bank offered little in the way of surprises at its latest policy meeting. As widely expected, interest rates were left unchanged. More importantly, ECB officials signaled that they are comfortable with the current policy stance and see no urgent need for adjustments.

ECB President Christine Lagarde emphasized that inflation is expected to stabilize around the central bank’s target over time. She described monetary policy as being in a “good place” and downplayed concerns that a stronger Euro could pose a serious risk to price stability.

Other policymakers echoed this message. ECB committee member Martin Kocher noted that the central bank does not see excessive strength in the Euro and reiterated that exchange rates are not a reliable guide for policy decisions. This consistent messaging reinforced the view that the ECB is likely to stay on hold for the foreseeable future.

While policy stability can be reassuring, it also means the Euro lacks a strong catalyst for gains, especially when economic data continues to disappoint.

US Labor Market Sends Mixed Signals

Recent US employment data has added another layer of complexity to the market outlook. Weekly jobless claims rose noticeably, and job openings fell to levels not seen in several years. These figures followed a softer private-sector employment report earlier in the week.

Together, these indicators suggest that the US labor market may be losing some momentum. This has fueled expectations that the Federal Reserve could consider cutting interest rates later in the year to support job growth.

Market participants have adjusted their outlook accordingly, with rising expectations for policy easing in the first half of the year. However, the impact of these expectations has been muted by the broader risk-off environment, which continues to favor the US Dollar.

The highly anticipated US jobs report has been delayed until next week due to a partial government shutdown. Until then, traders are relying on secondary indicators to gauge the health of the labor market.

Consumer Sentiment and Fed Commentary in Focus

Looking ahead, attention is turning to upcoming US data and official commentary. One key release is the preliminary Michigan Consumer Sentiment Index, which is expected to show a slight decline. Consumer confidence is closely watched because it offers insight into household spending behavior, a major driver of economic growth.

In addition, remarks from Federal Reserve Governor Philip Jefferson are scheduled during the US trading session. Any hints about how the Fed views recent labor market softness or financial market volatility could influence expectations around future policy moves.

With the main employment report postponed, these events take on added importance. Traders are likely to react quickly to any signals that shift the balance between growth concerns and inflation risks.

Why Markets Remain Cautious

Several factors are combining to keep markets on edge. Concerns about stretched valuations in the technology sector, uncertainty around global growth, and mixed economic signals from major economies all contribute to a cautious mood.

In Europe, weak industrial performance highlights ongoing structural challenges. In the US, slowing job growth raises questions about how long the economy can maintain its current pace without additional policy support.

Against this backdrop, central banks are trying to strike a careful balance. The ECB is signaling patience, while the Federal Reserve faces growing pressure to respond if labor market conditions continue to soften. Until there is greater clarity, investors are likely to remain defensive.

Final Summary

The Euro has managed a modest recovery after recent losses, but it remains under pressure from weak economic data and a cautious global market environment. Disappointing industrial figures from Germany have highlighted ongoing challenges in the Eurozone, while the European Central Bank’s steady policy stance offers stability but little fresh support.

Meanwhile, the US Dollar continues to benefit from risk-averse sentiment, political developments, and its role as a safe haven, even as signs emerge that the US labor market may be cooling. With key data releases and central bank comments still ahead, currency markets are likely to stay sensitive to shifts in sentiment.

For now, uncertainty remains the dominant theme, keeping traders alert and limiting decisive moves in either direction.

GBPUSD Gains Momentum as US Rate Cut Speculation Pressures the Dollar

The Pound Sterling managed to recover some lost ground after a rough previous session, steadying itself against several major currencies. The rebound came as traders reassessed the signals sent by the Bank of England and weighed them against fresh developments from the United States.

GBPUSD reached the retest area of the broken downtrend channel

Earlier weakness in the British currency was triggered by a clear shift in tone from the central bank. While no immediate policy change was made, the message suggested that borrowing costs may start to move lower sooner than many had expected. That surprise pushed the Pound down sharply at first, before calmer thinking set in and buyers stepped back in.

By the end of the week, attention had moved away from the initial shock and toward what the next steps might look like. With both the UK and US facing changing economic conditions, currency markets began to balance expectations on both sides of the Atlantic.

What the Bank of England Communicated

At its latest policy meeting, the Bank of England chose to keep interest rates unchanged. That decision itself did not catch anyone off guard. What did surprise the market was how divided the decision turned out to be.

More members of the Monetary Policy Committee were open to easing policy than investors had expected. This sent a strong signal that the debate inside the central bank is shifting. Instead of focusing solely on keeping inflation under control, policymakers appear increasingly confident that price pressures are easing faster than earlier forecasts suggested.

The central bank repeated its view that interest rates are likely to move lower over time rather than stay high indefinitely. Officials also expressed growing confidence that inflation is on track to return to its long-term target earlier than previously thought. This reinforced the idea that restrictive policy may not be needed for much longer.

Why the Vote Split Mattered

The split in the policy vote was a key reason for the Pound’s sudden drop. Markets often focus less on the final decision and more on the direction of thinking inside a central bank. A narrow vote tells investors that change is coming, even if it has not arrived yet.

Governor Andrew Bailey avoided committing to a clear timeline for the first rate cut. He also declined to confirm where interest rates might eventually settle. This cautious approach left room for interpretation, and traders wasted little time adjusting their expectations.

Initially, that adjustment worked against the Pound. Investors moved quickly to reflect a higher chance of policy easing in the near future. However, once the dust settled, many market participants began to question whether the reaction had gone too far.

Market Reaction and the Path Ahead

Following the initial sell-off, the Pound found support as traders stepped back to consider the broader picture. While the Bank of England signaled openness to rate cuts, it also stressed that any moves would be gradual and carefully managed.

This balanced message helped calm fears of an aggressive shift. The recovery suggested that investors still see the UK economy as relatively resilient, especially compared with some global peers. As a result, the British currency was able to claw back part of its earlier losses.

Looking ahead, comments from senior central bank officials remain in focus. Remarks from the Bank of England’s chief economist are expected to offer more detail on how policymakers view the current economic outlook. Since he was among those who supported holding rates steady, his perspective could help clarify how close the bank really is to changing course.

US Data Softens the Dollar’s Tone

The US Dollar, which had been strong earlier in the week, lost some momentum as new economic data pointed to cooling conditions in the labor market. Signs of softer hiring and fewer available jobs added weight to the argument that the Federal Reserve may soon be in a position to ease policy.

Recent reports showed that demand for workers is not as strong as it was in previous months. Private sector job creation also came in lighter than expected, reinforcing the view that the labor market is slowly losing steam. Together, these figures suggested that tighter financial conditions are having the intended effect.

As expectations for future US policy shifted, the Dollar gave back some of its recent gains. This move helped other major currencies, including the Pound, regain traction.

Why Labor Data Matters So Much

Labor market data plays a central role in shaping central bank decisions, especially in the United States. Strong job growth can keep inflation pressures alive, while weaker hiring trends often give policymakers room to support growth.

With signs pointing to a gradual slowdown, investors have become more confident that the Federal Reserve may be able to lower interest rates without risking a new surge in inflation. This change in outlook has made the Dollar less attractive in the short term.

Traders are now waiting for the next major employment report to confirm whether the slowdown is continuing. A clear signal either way could set the tone for currency markets in the days ahead.

What Traders Are Watching Next

Both sides of the Atlantic have key events on the calendar that could influence market direction. In the UK, further guidance from central bank officials will be closely examined for clues about timing and pace of any future policy moves.

In the US, upcoming labor market data is expected to play a decisive role. If job growth continues to cool, expectations for easier policy could strengthen further. On the other hand, a surprise rebound in hiring could revive support for the Dollar.

For now, markets appear to be in a wait-and-see mode. Investors are balancing early signs of economic slowdown with the understanding that central banks want to avoid acting too quickly.

Final Summary

The Pound Sterling’s recent bounce reflects a market that is adjusting to new information rather than rushing to judgment. A more divided Bank of England vote signaled that change may be coming, but officials also stressed caution and gradualism. This helped limit longer-term damage to the British currency.

At the same time, softer US labor data eased pressure on other currencies by weakening the Dollar. As expectations shift on both UK and US policy paths, traders are likely to remain sensitive to every new data release and official comment.

With uncertainty still high, the coming days are set to be shaped by central bank guidance and employment figures. Until clearer trends emerge, currency markets are likely to stay responsive, reflecting a careful balance between optimism and caution.

USDJPY Stalls While Political Risks and Spending Worries Cloud Yen Outlook

The Japanese Yen has been under pressure recently, but the mood is beginning to shift. After several days of weakness, the currency is showing signs of stabilizing as investors reassess their positions ahead of Japan’s snap election on Sunday. Political uncertainty, changing expectations around central bank policy, and a cautious global market mood are all shaping how traders view the Yen right now.

USDJPY reached the retest area of the broken uptrend channel

At the same time, the US Dollar has paused its recent rebound. Growing expectations that the US Federal Reserve may cut interest rates again are weighing on the greenback. This combination has eased some of the pressure on the Yen, even though strong conviction remains limited.

Political Uncertainty Weighs on Investor Confidence

Japan’s upcoming snap election is a major source of hesitation for currency traders. Prime Minister Sanae Takaichi’s Liberal Democratic Party is expected to perform well, which could give her more control over parliament. While political stability is usually welcomed, markets are uneasy about what may follow.

Takaichi has made it clear that she supports expansionary fiscal policies aimed at stimulating growth. Investors worry that aggressive government spending could further strain Japan’s already stretched public finances. This concern has made traders reluctant to place strong bullish bets on the Yen until there is more clarity on the country’s political and fiscal direction.

Because elections can quickly change policy expectations, many investors are choosing to reduce risk and wait on the sidelines. This cautious stance explains why the Yen’s recent gains have been modest rather than decisive.

Rising Expectations of a Bank of Japan Rate Hike

While politics create uncertainty, monetary policy is offering the Yen some support. There is growing belief that the Bank of Japan may raise interest rates sooner rather than later. Recent economic data and central bank commentary have strengthened this view.

Japan’s household spending data showed a notable decline in December, reversing the previous month’s growth. This suggests that higher living costs are starting to bite, putting pressure on consumers. For policymakers, this reinforces the need to address inflation more seriously, even if economic growth remains uneven.

The Bank of Japan’s recent Summary of Opinions revealed active debate among policymakers about rising price pressures. A weaker Yen was highlighted as a factor contributing to higher import costs, which feed into inflation. Several board members agreed that gradual interest rate increases would be appropriate over time.

These signals have encouraged investors to believe that Japan’s long-standing ultra-loose monetary stance is slowly coming to an end. Even small steps toward higher rates can make a meaningful difference for a currency that has been weighed down by low returns for years.

Risk-Off Mood Boosts the Yen’s Safe-Haven Appeal

Global market sentiment has also played a role in supporting the Yen. Asian stock markets have extended losses, following a sharp selloff in US equities driven largely by weakness in technology shares. When markets turn cautious, investors often seek safer assets, and the Japanese Yen has traditionally benefited from this behavior.

This renewed demand for safety has helped the Yen snap a multi-day losing streak. While the gains are not dramatic, they reflect a shift in short-term sentiment. Traders are more focused on protecting capital than chasing higher returns, which naturally favors currencies seen as stable during turbulent times.

At the same time, there is ongoing awareness of the possibility of coordinated action by Japanese and US authorities to slow excessive Yen weakness. Even the hint of such intervention can make traders more cautious about betting against the currency.

US Economic Data Weakens the Dollar’s Momentum

Across the Pacific, the US Dollar is facing its own challenges. Recent labor market data has pointed to cooling conditions, adding to expectations that the Federal Reserve may continue easing policy in the future.

New applications for unemployment benefits rose more than expected in the latest weekly report. This followed disappointing private-sector employment figures earlier in the week, reinforcing the idea that the US job market is losing momentum.

Further evidence came from the Job Openings and Labor Turnover Survey, which showed a decline in available positions at the end of December. Fewer job openings suggest that employers are becoming more cautious, a trend that aligns with slower economic growth.

Together, these data points have strengthened the case for additional interest rate cuts from the Federal Reserve. Markets are increasingly pricing in the possibility of multiple reductions in borrowing costs next year, which limits how much the Dollar can strengthen in the near term.

USD and Yen Dynamics Ahead of Key Events

With both the Japanese and US sides facing important developments, the balance between the two currencies remains delicate. The Dollar’s recent recovery has stalled, while the Yen is trying to regain footing without a clear catalyst.

Investors are now turning their attention to upcoming US consumer sentiment data and inflation expectations. Comments from influential Federal Reserve officials may also shape short-term market moves. However, many traders expect reactions to be restrained until Japan’s election results are known.

The political outcome could influence not only fiscal policy but also how aggressively the Bank of Japan proceeds with policy normalization. As a result, the election acts as a temporary anchor on market activity, encouraging patience rather than bold positioning.

What This Means for the Japanese Yen Going Forward

The current environment highlights how sensitive the Japanese Yen is to a mix of domestic and global factors. Political uncertainty is limiting enthusiasm, but rising confidence in a Bank of Japan rate hike and a cautious global mood are providing a counterbalance.

For now, the Yen appears to be finding a fragile equilibrium. It is no longer falling sharply, but it has yet to attract strong buying interest. Much will depend on how Japan’s leadership chooses to balance economic stimulus with fiscal responsibility, and how quickly the central bank is willing to act.

On the global stage, the direction of US monetary policy will remain just as important. If expectations for Federal Reserve rate cuts continue to grow, the Dollar may struggle to regain momentum, giving the Yen more breathing room.

Final Summary

The Japanese Yen is navigating a complex landscape shaped by political uncertainty, shifting central bank expectations, and a cautious global market mood. Ahead of Japan’s snap election, investors are trimming risk and waiting for clearer signals on fiscal policy. At the same time, growing confidence in a Bank of Japan rate hike and safe-haven demand are offering the Yen some support. With the US Dollar losing steam amid signs of a softer labor market, the balance between the two currencies remains finely poised as markets await the next key developments.

NZDUSD Strengthens as Markets Await Fresh Signals from US Consumers

The NZD/USD currency pair has found fresh support after a brief period of weakness, helped by a softer US Dollar and changing expectations around US interest rates. Recent economic signals from the United States suggest that the once-strong labor market may be cooling, and that shift is influencing how investors see the Federal Reserve’s next moves. At the same time, mixed signals from New Zealand’s own job market are shaping the outlook for the New Zealand Dollar.

NZDUSD is moving in a descending channel, and the market has reached the lower high area of the pattern

Together, these developments are creating a push-and-pull effect on the NZD/USD pair, with global monetary policy expectations playing a central role in day-to-day market sentiment.

Cooling US Labor Data Changes the Fed Narrative

The US Dollar has eased as investors react to signs that hiring momentum in the United States is slowing. For months, strong employment data helped keep the Dollar supported, as markets believed the Federal Reserve would keep interest rates high for longer. That story is now being questioned.

Recent labor reports point to softer conditions. Initial jobless claims increased more than expected, suggesting that layoffs may be becoming more common. At the same time, private sector job creation came in well below forecasts, adding to the sense that the US job market is losing some of its strength.

These signals matter because the Federal Reserve has repeatedly said that future policy decisions depend on economic data. When employment growth slows, it reduces inflation pressure and gives policymakers more room to ease monetary policy. As a result, expectations for interest rate cuts have started to firm up.

Fed Rate Cut Expectations Gain Traction

Markets are now increasingly confident that the Federal Reserve will begin cutting interest rates later this year. Current expectations point to two rate reductions, with the first likely around mid-year and a possible follow-up later in the year if economic conditions continue to soften.

For now, investors largely expect the Fed to keep rates unchanged at its upcoming meeting, but the focus has clearly shifted to what happens next. Any further evidence of cooling in jobs, wages, or consumer spending could reinforce the case for easing policy.

A more dovish Federal Reserve generally weighs on the US Dollar. Lower interest rates reduce the appeal of holding Dollar-denominated assets, especially when compared to currencies linked to higher yields or stronger growth prospects. This shift has helped the NZD/USD pair recover after recent losses.

New Zealand Dollar Faces Domestic Headwinds

While the US Dollar has weakened, the New Zealand Dollar is dealing with its own challenges. A recent labor market report from New Zealand sent mixed signals, leaving investors uncertain about the country’s economic direction.

On one hand, employment growth surprised to the upside, showing that businesses are still hiring. On the other hand, the unemployment rate rose unexpectedly and reached its highest level in many years. This increase suggests that spare capacity remains in the labor market and that wage pressures may not be as strong as previously thought.

For policymakers at the Reserve Bank of New Zealand, this data complicates the picture. Rising unemployment reduces the urgency to tighten policy, even if some parts of the economy continue to show resilience. As a result, expectations for a near-term interest rate hike have faded.

RBNZ Policy Outlook Under New Leadership

The Reserve Bank of New Zealand is entering an important period, with its first policy meeting under new Governor Anna Breman approaching soon. Markets widely expect the central bank to leave interest rates unchanged at this meeting, reflecting the mixed economic backdrop.

Updated economic forecasts and interest rate projections will be closely watched. These updates will offer insight into how the RBNZ views inflation risks, labor market slack, and overall growth prospects. For now, traders have pushed back expectations for the next rate increase, with most no longer fully pricing in a move until later in the year.

This delay in tightening expectations has limited the New Zealand Dollar’s upside. Even as the US Dollar softens, the NZD struggles to gain strong momentum because its own central bank is in no hurry to raise rates.

Key Data and Events on the Radar

Looking ahead, market attention is turning to upcoming US data releases, including consumer sentiment figures. These reports help gauge how households feel about the economy, jobs, and future spending. Weak sentiment could reinforce the idea that higher interest rates are starting to bite, strengthening the case for Fed rate cuts.

At the same time, investors will keep a close eye on commentary from Federal Reserve officials. Any hints about the timing or pace of potential rate reductions can quickly shift currency markets.

In New Zealand, focus remains on how the RBNZ interprets recent labor data and whether future reports confirm a trend of rising unemployment or renewed strength. Clarity on this front will be essential for determining the longer-term direction of the New Zealand Dollar.

Balancing Global and Local Forces

The NZD/USD pair is currently influenced by two competing forces. On one side, a softer US Dollar driven by cooling labor data and growing expectations of Fed rate cuts is providing support. On the other side, uncertainty around New Zealand’s economic outlook and delayed policy tightening is acting as a drag.

This balance means that gains may be gradual rather than explosive. Traders are likely to remain cautious, reacting quickly to fresh data and central bank signals from both countries.

Final Summary

The recent rebound in NZD/USD reflects a changing global mood, as signs of a slowing US labor market revive expectations for Federal Reserve rate cuts. This shift has weakened the US Dollar and given the currency pair some breathing room. However, mixed labor data from New Zealand and fading hopes for near-term tightening by the Reserve Bank of New Zealand continue to limit the New Zealand Dollar’s strength.

With major central bank decisions and key economic reports ahead, the NZD/USD outlook remains closely tied to how quickly inflation and employment conditions evolve on both sides of the Pacific.

XAGUSD Strains to Recover as Selling Pressure Lingers

Silver has recently tried to steady itself after a dramatic fall that shook investor confidence across the precious metals space. Following weeks of heavy selling, the metal showed signs of a short-term bounce, but the broader mood around silver remains cautious. Many market participants are still weighing whether this recovery has real strength behind it or if it is simply a pause after a steep decline.

XAGUSD reached the retest area of the broken uptrend channel

The past couple of weeks have been especially difficult for silver. A rapid loss of value erased gains built over several months and reminded traders how quickly sentiment can shift. While brief recoveries can happen after such sharp moves, they do not always signal a full turnaround. Instead, they often reflect temporary adjustments as investors reassess risk and rebalance positions.

Silver’s recent behavior highlights how sensitive it is to global confidence, political developments, and changes in economic leadership. Unlike gold, which is often seen as a pure safe-haven asset, silver sits at the crossroads of investment demand and industrial use. This dual role can amplify price swings when uncertainty fades or returns.

What Drove the Recent Decline in Silver

The sharp drop in silver did not happen in isolation. It was the result of several major developments coming together at the same time. One of the most important factors was a sudden improvement in overall market confidence. When fear eases, investors often reduce exposure to assets they see as defensive, including precious metals.

Another key driver was the reaction to changes in leadership at the US central bank. The announcement of a new chairperson brought a sense of relief to financial markets. Investors interpreted the move as a sign of stability and continuity in monetary policy, reducing concerns about unexpected shifts in interest rate direction or economic management.

This renewed confidence encouraged money to flow back into riskier assets such as equities and growth-focused investments. As a result, silver faced selling pressure as traders moved capital away from defensive positions and toward opportunities with higher perceived returns.

At the same time, broader economic worries that had previously supported silver began to fade. With fewer immediate threats on the horizon, the metal lost some of the appeal it had enjoyed during periods of heightened uncertainty.

Investor Sentiment and Risk Appetite

Investor psychology plays a powerful role in shaping silver’s performance. When fear dominates the market, silver often benefits as investors look for assets that can preserve value. However, when optimism returns, that same demand can quickly disappear.

Over the past two weeks, risk appetite improved noticeably. Markets responded positively to signals of political stability and reduced conflict risks. This shift led many investors to unwind positions in precious metals and focus instead on assets linked to economic growth.

Silver is particularly vulnerable during these transitions. Because it is used heavily in manufacturing, electronics, and renewable energy, its outlook depends not only on financial sentiment but also on expectations for industrial demand. When economic confidence improves, investors may prefer to gain exposure through stocks or industrial commodities rather than silver itself.

This tug-of-war between silver’s role as a defensive asset and its industrial identity can lead to sharp and sometimes confusing movements. Even when the metal attempts to recover, lingering doubts about the broader direction of the market can limit enthusiasm.

Geopolitics and the Changing Demand for Safe Havens

Geopolitical tension has long been one of the strongest drivers of safe-haven demand. When conflicts appear likely, investors often seek protection in assets like gold and silver. Recently, however, that dynamic shifted.

The opening of diplomatic talks between major global players helped calm fears of an escalating conflict. This reduction in geopolitical stress removed a layer of support that had previously benefited silver. As the risk of confrontation appeared to decrease, investors felt less urgency to hold assets designed to hedge against instability.

This does not mean geopolitics will stop influencing silver altogether. Rather, it shows how quickly demand can change when the global outlook improves, even temporarily. Precious metals thrive on uncertainty, and when that uncertainty fades, prices often struggle to maintain momentum.

For silver, which lacks the same level of central bank backing as gold, this effect can be even more pronounced. Without strong institutional demand, the metal relies heavily on investor sentiment and industrial outlooks to sustain interest.

Central Bank Leadership and Market Confidence

Changes at the top of major financial institutions can have far-reaching effects. The recent appointment of a new central bank leader in the United States played a significant role in shaping market expectations. Investors viewed the decision as a move toward predictability, reducing concerns about abrupt policy changes.

Stable monetary leadership tends to support confidence in traditional financial markets. When investors feel assured about interest rate policy and economic guidance, they are less likely to seek shelter in precious metals. This environment can be challenging for silver, especially after a period when it benefited from uncertainty.

While central bank decisions do not directly control silver demand, they influence the broader financial landscape. Confidence in monetary policy often leads to stronger currencies and improved market sentiment, both of which can weigh on metals that do not generate income.

Silver’s recent struggle reflects this reality. Even as it attempts to recover, the absence of fear-driven buying limits the strength of any rebound.

What This Means for Silver Going Forward

The recent episode serves as a reminder that silver can be highly volatile, especially during periods of shifting global sentiment. Sharp declines are often followed by short-lived recoveries, but lasting strength usually requires a clear catalyst.

Looking ahead, silver’s direction will likely depend on a mix of economic data, geopolitical developments, and investor mood. If uncertainty returns, whether through economic slowdown or renewed political tensions, interest in silver could pick up again. On the other hand, sustained optimism may continue to pressure the metal.

Industrial demand will also play a role. As technologies tied to clean energy and electronics continue to grow, silver’s long-term fundamentals remain relevant. However, short-term movements are still dominated by financial flows and market psychology.

For investors, the recent downturn highlights the importance of understanding silver’s unique position in the market. It is neither purely a safe haven nor purely an industrial commodity, and that dual nature can lead to sudden changes in direction.

Final Summary

Silver has attempted to stabilize after a steep and unsettling decline, but its recovery remains uncertain. Improved market confidence, easing geopolitical tensions, and renewed trust in economic leadership have all reduced the demand that previously supported the metal. As investors shift toward riskier assets, silver faces challenges in regaining momentum.

The coming weeks will test whether silver can attract fresh interest or if cautious sentiment will continue to dominate. Its future path will depend on how global confidence evolves and whether new sources of uncertainty emerge. For now, silver stands as a clear example of how quickly market dynamics can change when fear gives way to optimism.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!