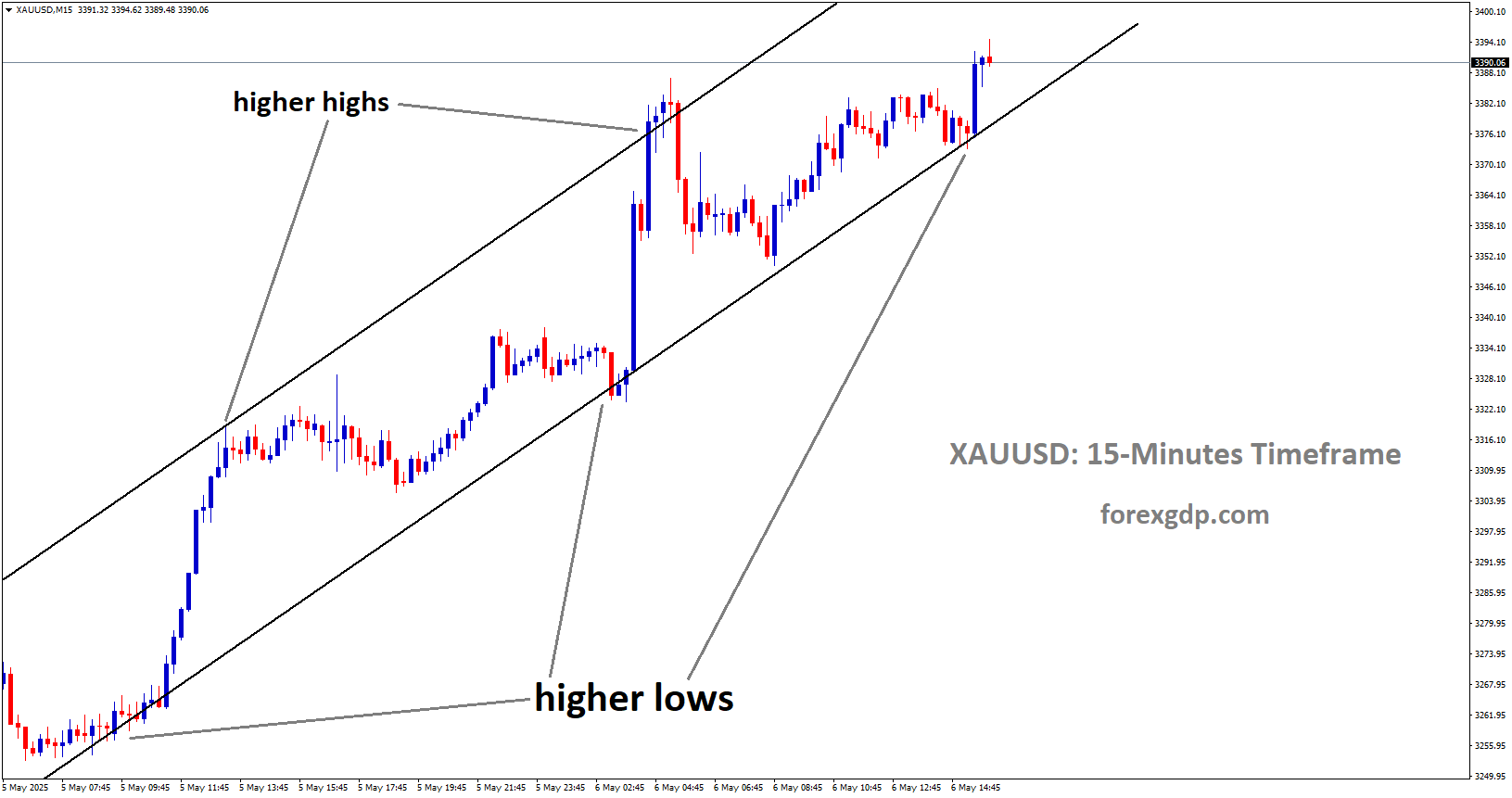

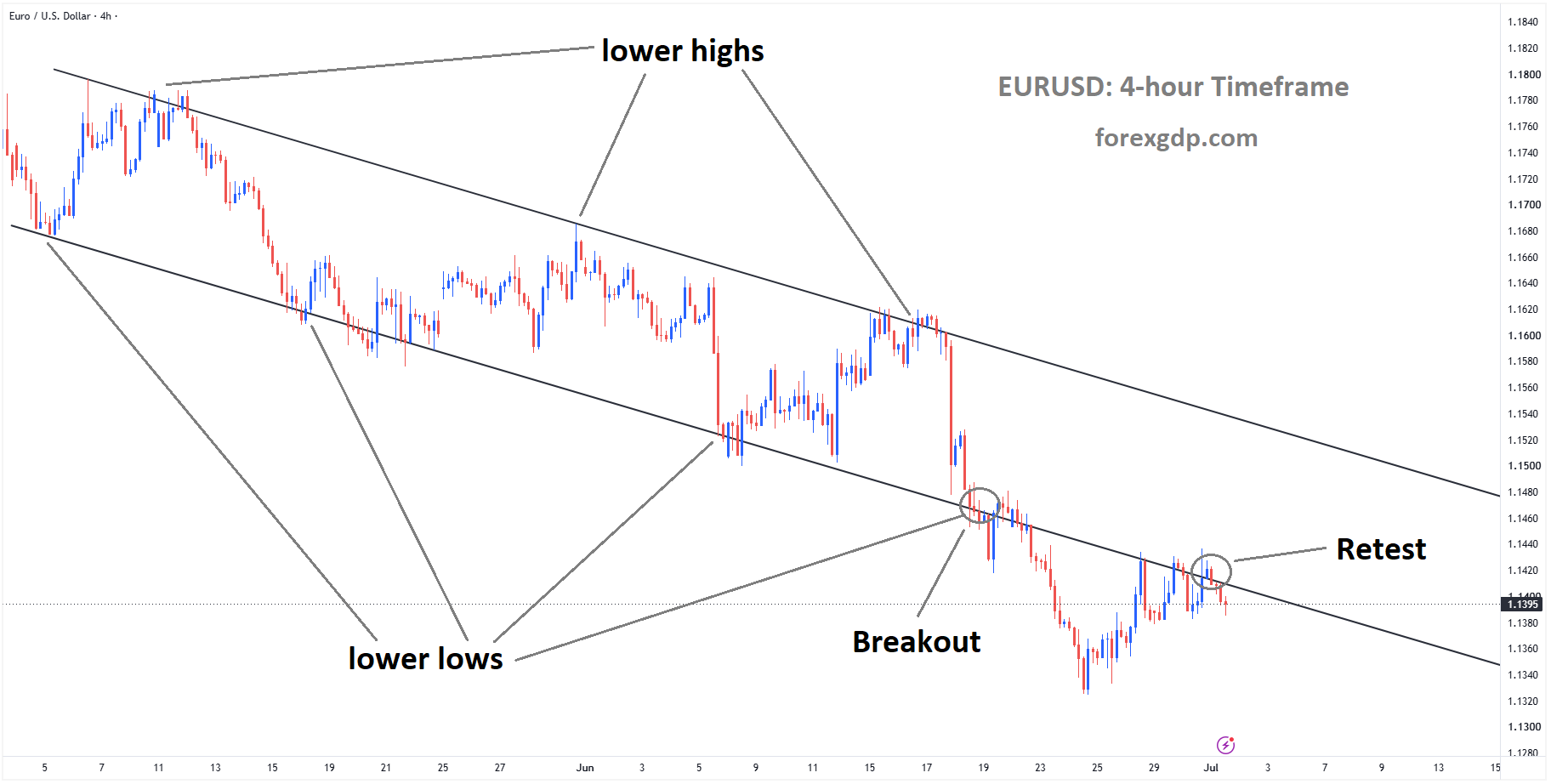

EURUSD reached the retest area of the broken descending channel

EURUSD Under Pressure as Eurozone Price Growth Slows Further

The EUR/USD currency pair lost momentum on Wednesday after a brief recovery earlier in the week. The Euro weakened against the US Dollar as fresh inflation data from the Eurozone came in lower than expected, reducing expectations that the European Central Bank (ECB) will need to raise interest rates again in the near future.

At the same time, confidence in the strength of the US economy continues to support the US Dollar. Investors are now closely watching speeches from ECB President Christine Lagarde and Federal Reserve Chairman Kevin Warsh for fresh clues about the future direction of monetary policy.

Euro Loses Ground After Inflation Slows

The Euro came under pressure after new inflation figures showed that price growth across the Eurozone continued to ease during June. The data suggested that inflation is moving closer to the ECB’s target, lowering the urgency for further interest rate increases.

A slower pace of inflation is generally viewed as positive for consumers because it reduces the pressure of rising living costs. However, for the currency market, it can reduce expectations of tighter monetary policy, making the Euro less attractive to investors seeking higher returns.

As a result, the Euro gave back its earlier gains and moved lower against the US Dollar during the European trading session.

Inflation Trend Brings Relief to the ECB

The latest inflation figures showed a broader slowdown across the Eurozone rather than an isolated decline. Similar reports released earlier from Germany and Italy also pointed to easing price pressures, reinforcing the view that inflation is gradually cooling across the region.

This trend gives the ECB more flexibility. Instead of rushing into additional interest rate increases, policymakers now have more time to evaluate how the economy develops over the coming months.

The recent moderation also suggests that earlier concerns about rising energy costs pushing inflation sharply higher may be easing, allowing central bank officials to take a more measured approach.

Why Lower Inflation Matters

Inflation remains one of the most important factors influencing central bank decisions. When inflation stays high, central banks often respond by raising interest rates to slow spending and reduce price pressures.

However, when inflation begins to cool naturally, policymakers may decide that further tightening is unnecessary. They can wait and observe whether inflation continues to move toward their long-term goal without introducing additional measures.

This change in expectations can quickly influence currency markets, as investors adjust their outlook for future interest rates.

Investors Focus on Christine Lagarde’s Speech

With the latest inflation report now available, attention has shifted to ECB President Christine Lagarde, who is scheduled to speak at the annual central banking forum in Sintra, Portugal.

Earlier in the week, Lagarde delivered comments that were viewed as relatively firm regarding inflation. After Wednesday’s softer inflation numbers, investors will be eager to hear whether her tone changes.

Market participants will closely examine her remarks for any indication that the ECB is becoming more comfortable with current inflation trends or whether it still believes additional policy action may be necessary in the future.

Even small changes in language can influence investor expectations and move currency markets.

Federal Reserve Chairman Kevin Warsh Also in Focus

Later in the day, Federal Reserve Chairman Kevin Warsh is also expected to address the same central banking event.

Unlike some previous Fed leaders who frequently provided detailed guidance about future policy plans, Warsh has generally preferred to avoid making strong commitments in advance.

Because of this approach, investors may receive only limited clues about the Fed’s future decisions. Nevertheless, every public appearance by the Fed Chair is carefully watched, as even subtle comments about the economy or inflation can influence market sentiment.

His remarks may provide additional insight into how the Federal Reserve currently views economic conditions in the United States.

Strong US Economy Continues to Support the Dollar

While the Euro has been weakened by softer inflation data, the US Dollar continues to benefit from confidence in the American economy.

Recent economic reports have continued to show resilience in key areas, helping maintain expectations that the Federal Reserve may keep monetary policy restrictive if necessary.

A stronger economic outlook generally supports a country’s currency because investors expect higher returns and greater stability.

This contrast between a cooling Eurozone economy and a resilient US economy has helped strengthen demand for the US Dollar.

Different Central Bank Paths Matter

Currency markets often react not only to current economic data but also to expectations about future central bank actions.

If investors believe the ECB may pause while the Federal Reserve remains cautious about reducing policy restrictions, the difference between the two central banks’ approaches can influence the EUR/USD exchange rate.

This is why speeches from central bank leaders receive so much attention. Their comments help investors understand how policymakers interpret the latest economic developments and what actions they may consider in the months ahead.

Market Attention Remains on Economic Signals

Although inflation has slowed, policymakers are unlikely to make decisions based on a single report. They will continue monitoring additional economic indicators, including employment, consumer spending, wage growth, and overall economic activity.

Future data releases will play an important role in determining whether inflation continues to ease or whether new risks emerge.

For now, investors remain cautious, waiting for both economic reports and central bank guidance before making stronger market decisions.

Summary

The EUR/USD pair weakened after fresh Eurozone inflation data showed that price growth slowed more than expected in June. The softer inflation figures reduced pressure on the European Central Bank to introduce further interest rate increases, weighing on the Euro.

Meanwhile, continued confidence in the US economy has supported the US Dollar, keeping investors focused on the difference between the economic outlooks of the two regions. With speeches from ECB President Christine Lagarde and Federal Reserve Chairman Kevin Warsh scheduled later in the day, market participants are looking for fresh signals that could shape expectations for future monetary policy and influence the direction of the currency market.

GBPUSD Drops Ahead of Crucial US Economic Reports

The British Pound moved lower against the US Dollar during Wednesday’s European trading session as investors favored the US currency. The stronger performance of the Dollar came after US Treasury yields climbed sharply, reflecting growing confidence in the strength of the American economy.

GBPUSD is moving in a box pattern

Market participants are now turning their attention to several important US economic reports and comments from Federal Reserve Chair Kevin Warsh. These events could influence investor sentiment and shape expectations for the US economy over the coming days.

US Dollar Gains Strength as Treasury Yields Rise

The US Dollar attracted fresh buying interest after Treasury yields continued their recent climb. Rising government bond yields often make US-based investments more attractive to global investors, increasing demand for the Dollar.

The Pound struggled to hold its ground as investors shifted their focus toward the stronger US currency. Higher yields also suggest that financial markets are expecting the US economy to remain resilient, encouraging traders to keep funds in Dollar-denominated assets.

The improvement in the Dollar’s performance created additional pressure on GBP/USD, causing the currency pair to move lower during the trading session.

Stronger US Labor Demand Supports Market Confidence

One of the biggest reasons behind the recent strength in the US Dollar was encouraging labor market data released on Tuesday.

The latest Job Openings and Labor Turnover Survey (JOLTS) showed that US employers posted more job openings in May than economists had expected. The report also slightly exceeded the previous month’s reading, indicating that businesses continue to hire despite ongoing economic uncertainty.

A healthy labor market is generally viewed as a positive sign for the broader economy. When companies continue to recruit workers, it suggests that business activity remains steady and employers are confident about future demand.

This stronger labor market picture helped push Treasury yields higher and gave additional support to the US Dollar.

Investors Wait for More Key Employment Reports

While the latest labor market figures were encouraging, investors know that several more important employment reports are still ahead.

The US ADP Employment Change report will provide another snapshot of private-sector hiring and offer fresh clues about the strength of the labor market. Although the ADP report does not always perfectly match the official employment data, it often helps investors prepare for the larger reports that follow.

Later in the week, the closely watched US Nonfarm Payrolls (NFP) report will become the main focus. This monthly report is considered one of the most influential economic releases because it provides a broad picture of employment growth across the United States.

Since employment plays a major role in economic growth and consumer spending, the NFP report frequently creates significant movement across currency markets.

Manufacturing Data Also Remains in Focus

Alongside employment reports, investors will also pay close attention to the latest ISM Manufacturing PMI.

This report measures activity across the US manufacturing sector and helps indicate whether factory output is expanding or slowing. A stronger reading would reinforce confidence in the economy, while weaker figures could raise concerns about slowing industrial activity.

Manufacturing data often provides valuable insight into business conditions, production levels, and overall economic momentum. Because of this, traders carefully monitor the report before making major investment decisions.

Attention Turns to Federal Reserve Chair Kevin Warsh

Another event drawing investor attention is the scheduled speech by Federal Reserve Chair Kevin Warsh during the North American trading session.

Although central bank speeches can sometimes move financial markets, analysts believe the impact of Warsh’s comments may be relatively limited this time.

During his recent monetary policy press conference, Warsh indicated that providing clear forward-looking guidance is difficult under current economic conditions. This suggests that policymakers remain cautious and prefer to make future decisions based on incoming economic data rather than offering firm commitments in advance.

As a result, investors may focus more on upcoming economic reports than on any major policy signals from his speech.

Why Employment Data Matters for Currency Markets

Employment data plays a vital role in shaping expectations for economic growth. A strong labor market usually supports consumer spending, which is one of the biggest drivers of the US economy.

When employment remains healthy, businesses often continue expanding, household incomes stay stable, and overall economic activity receives support.

Currency traders closely monitor labor market reports because they help determine how central banks may respond to changing economic conditions. Strong employment figures can strengthen confidence in the economy, while weaker numbers may lead investors to reassess future expectations.

Because of this relationship, reports such as JOLTS, ADP Employment Change, and Nonfarm Payrolls regularly attract significant attention from global financial markets.

GBP/USD Faces a Busy Week Ahead

The remainder of the week is expected to remain active for the British Pound and the US Dollar as investors digest a series of major economic updates.

Employment reports, manufacturing data, and comments from Federal Reserve officials will all contribute to market sentiment. Each release has the potential to influence expectations about the health of the US economy and the direction of the Dollar.

For GBP/USD traders, the combination of economic indicators and central bank communication is likely to keep market activity elevated. Investors will carefully compare each new piece of information before adjusting their positions.

Summary

The British Pound weakened against the US Dollar as rising US Treasury yields boosted demand for the American currency. Stronger-than-expected job openings in May reinforced confidence in the US labor market and supported the Dollar’s recent gains.

Looking ahead, investors will closely monitor the ADP Employment report, ISM Manufacturing PMI, the highly anticipated Nonfarm Payrolls report, and remarks from Federal Reserve Chair Kevin Warsh. Together, these events are expected to play a major role in shaping market sentiment and determining the next direction for the GBP/USD currency pair.

USDJPY Trades Firm as Japan Faces Growing Pressure to Defend the Yen

The Japanese Yen continues to struggle against the US Dollar as investors remain focused on the gap between monetary policies in Japan and the United States. Although the USDJPY pair eased slightly after reaching a fresh multi-decade high, the overall trend still reflects strong demand for the US Dollar.

USDJPY has broken the box pattern to the upside

A combination of stronger US economic conditions, expectations for tighter Federal Reserve policy, and Japan’s cautious approach to interest rates has kept the Yen under pressure. At the same time, concerns are growing that Japanese authorities could step into the market if the currency weakens further.

Why the Japanese Yen Remains Under Pressure

The biggest challenge for the Japanese Yen is the clear difference in monetary policy between Japan and the United States. While the Federal Reserve continues to signal a firm stance against inflation, the Bank of Japan is moving much more carefully with its policy adjustments.

This difference has encouraged investors to favor the US Dollar over the Yen. As long as US interest rates remain relatively attractive compared to Japan’s, the Yen is likely to face continued selling pressure.

Although the Japanese currency has shown small recoveries at times, these gains have been short-lived as broader market sentiment continues to support the Dollar.

Bank of Japan Continues Its Careful Approach

The Bank of Japan recently raised interest rates to their highest level in decades, marking another important step away from its long period of ultra-low borrowing costs. Even so, policymakers continue to move cautiously.

Many investors had expected the central bank to continue raising rates more aggressively. However, government officials have emphasized the importance of supporting Japan’s economic growth while avoiding sudden policy changes.

Economic Minister Minoru Kiuchi has encouraged the Bank of Japan to coordinate its actions with the government’s growth strategy. While not directly opposing future rate increases, his comments suggest that policymakers prefer a gradual path rather than rapid tightening.

This cautious message has reduced expectations that Japan will quickly narrow the interest rate gap with the United States.

Federal Reserve Maintains a Firm Policy Outlook

Across the Pacific, the Federal Reserve continues to project confidence in the US economy. Recent economic reports have reduced concerns about slowing growth and the labor market, while inflation remains an important issue for policymakers.

Because of this, investors believe the Federal Reserve may continue maintaining higher interest rates for longer than previously expected.

This outlook has strengthened the appeal of the US Dollar in global financial markets. Investors often seek currencies that offer higher returns, and the current policy difference between the US and Japan has made the Dollar a more attractive choice.

As long as this situation remains unchanged, the Japanese Yen may continue to face difficulties against the US Dollar.

Yield Gap Continues to Influence Currency Markets

One of the strongest drivers behind the current move is the large difference between US and Japanese government bond yields.

Higher US yields generally attract global investors looking for better returns on their investments. At the same time, Japan’s comparatively lower yields reduce the attractiveness of holding Yen-denominated assets.

This steady flow of investment toward the United States increases demand for the US Dollar while limiting demand for the Japanese Yen.

Unless Japan changes its monetary policy more aggressively or US expectations shift significantly, this yield gap is expected to remain an important factor influencing the currency market.

Intervention Concerns Remain in Focus

Despite the Yen’s weakness, traders remain cautious because Japanese authorities have repeatedly warned that they are prepared to act if currency movements become excessive.

Officials in Tokyo have made it clear that they are closely monitoring the foreign exchange market and are willing to intervene when necessary to stabilize the Yen.

These warnings have increased speculation that direct market intervention could happen at any time if authorities believe the currency’s decline is becoming too rapid or disorderly.

However, so far these statements have not been enough to discourage investors from maintaining bullish positions on the US Dollar against the Yen.

Market Watches for the Timing of Possible Action

The main question for investors is not whether intervention is possible, but when it could happen.

Some market participants believe Japanese authorities may choose a period of lower market activity to maximize the impact of any action. With thinner trading conditions expected during the upcoming US bank holiday, speculation has grown that officials could see this as a favorable opportunity.

Lower trading volumes can sometimes make currency interventions more effective because fewer transactions are needed to influence market movements.

While no official confirmation has been given, traders remain alert for any unexpected announcements or sudden changes in market activity.

Speculative Positions Continue to Build

Data from US regulators shows that speculative investors continue to hold large long positions in the USDJPY pair.

This suggests that many traders still expect the US Dollar to outperform the Japanese Yen in the near future. The continued buildup of these positions reflects confidence that the policy gap between the Federal Reserve and the Bank of Japan will remain wide for some time.

At the same time, large speculative positions also increase the possibility of sharp market swings if intervention occurs or if expectations around central bank policies suddenly change.

For this reason, investors are watching official comments from both countries very closely.

Summary

The Japanese Yen remains under heavy pressure as the difference between US and Japanese monetary policies continues to favor the US Dollar. While the Bank of Japan is moving carefully with future policy decisions, the Federal Reserve’s firm stance has strengthened demand for the Dollar.

Government officials in Japan continue to signal that they are ready to intervene if necessary, keeping traders alert for possible action. Meanwhile, speculation over the timing of any intervention remains high, particularly during periods of lighter market activity.

Going forward, investors will closely follow central bank communication, economic developments, and any signs of official intervention, as these factors are likely to shape the next phase of movement for the USDJPY currency pair.

AUDUSD Weakens as Investors Favor US Dollar on Labor Strength and Global Uncertainty

The AUD/USD currency pair remained under pressure on Wednesday as the US Dollar continued to attract buyers in a cautious global market. While fresh economic data from China met expectations, it failed to provide enough momentum to lift the Australian Dollar. At the same time, strong US labor market data and ongoing geopolitical uncertainty encouraged investors to favor the US Dollar.

AUDUSD is rebounding from the retest area of the broken descending channel

With several important US economic reports scheduled for release, traders are closely watching incoming data that could influence the Federal Reserve’s future policy decisions. These developments are also shaping expectations ahead of the highly anticipated US Nonfarm Payrolls report.

Chinese Manufacturing Data Offers Limited Support

China’s latest manufacturing data showed that business activity continued to expand in June, but the figures largely matched market expectations rather than exceeding them. As a result, the report did little to boost confidence in the Australian Dollar.

China is Australia’s largest trading partner, making its economic performance an important factor for the Australian economy. When Chinese factories remain busy, demand for Australian exports often improves. However, when growth remains moderate or domestic demand stays weak, the positive impact on Australia’s currency becomes limited.

Recent official manufacturing reports also pointed to ongoing challenges within China’s economy. Slower domestic demand continues to weigh on factory activity, creating concerns about the pace of economic recovery. This cautious outlook has reduced support for the Australian Dollar despite stable manufacturing readings.

US Dollar Benefits from Strong Labor Market

The US Dollar continued to gain strength as fresh employment data reinforced confidence in the US economy. Recent reports suggested that the labor market remains healthy, supporting expectations that the Federal Reserve may continue to keep monetary policy restrictive if inflation remains persistent.

The latest Job Openings and Labor Turnover Survey (JOLTS) showed a noticeable increase in available job positions, reaching the highest level seen in roughly two years. This signals that businesses continue to hire workers despite ongoing economic uncertainties.

At the same time, the Challenger Job Cuts report revealed a sharp decline in planned layoffs compared to the previous month. Fewer announced job cuts indicate that companies remain confident about their business outlook and are holding onto employees.

Together, these reports strengthen the view that the US labor market remains resilient. A strong employment environment often supports consumer spending and overall economic growth, helping maintain demand for the US Dollar.

Geopolitical Risks Increase Safe-Haven Demand

Apart from economic data, global political developments also played an important role in supporting the US Dollar.

Investors remain concerned about the ongoing negotiations between the United States and Iran. Progress in diplomatic discussions has been limited, increasing uncertainty about the future of relations in the Middle East.

Whenever geopolitical tensions rise, financial markets often become more cautious. During periods of uncertainty, investors typically move money into assets considered safer, with the US Dollar being one of the most popular choices.

This increase in safe-haven demand has added another layer of support for the Greenback, making it more difficult for currencies like the Australian Dollar to recover.

Reserve Bank of Australia Rate Expectations Continue to Ease

The outlook for Australian interest rates has also influenced the movement of the Australian Dollar.

Financial markets are increasingly expecting the Reserve Bank of Australia (RBA) to avoid further interest rate increases this year. While policymakers continue to stress the importance of controlling inflation, expectations for additional tightening have gradually weakened.

Minutes from the RBA’s latest policy meeting suggested that officials still believe monetary policy should remain restrictive for now. However, investors see only a limited chance of another rate increase unless inflation unexpectedly accelerates again.

This shift in market expectations has reduced support for the Australian Dollar, especially as investors compare Australia’s outlook with the relatively strong performance of the US economy.

Investors Await More Important US Economic Reports

Attention now turns to several major US economic releases that could provide fresh direction for financial markets.

The ADP Employment Change report is expected to offer an early look at private-sector hiring before the official government employment figures are published. Strong hiring numbers could reinforce confidence in the US labor market, while weaker results may lead investors to reassess expectations.

Another closely watched release is the Institute for Supply Management (ISM) Manufacturing Purchasing Managers Index. This report measures the health of the US manufacturing sector and provides valuable insight into business activity, production, new orders, and overall economic momentum.

Both reports have the potential to influence market expectations regarding future Federal Reserve decisions.

Focus Shifts Toward the Nonfarm Payrolls Report

The biggest event on investors’ calendars remains the upcoming US Nonfarm Payrolls (NFP) report.

The monthly employment report is considered one of the most influential pieces of economic data because it provides a comprehensive picture of the US labor market. Investors closely examine job creation, unemployment levels, and wage growth to assess the strength of the economy.

Since the Federal Reserve carefully monitors labor market conditions when making interest rate decisions, stronger or weaker employment data can significantly affect market sentiment.

For this reason, traders may remain cautious until the report is released, limiting larger moves in the currency market.

Global Sentiment Continues to Influence Currency Markets

Beyond individual economic reports, overall market sentiment remains an important driver of currency movements.

When uncertainty rises due to geopolitical events or concerns about global economic growth, investors often reduce exposure to riskier assets and seek safer investments. This environment generally benefits the US Dollar while placing pressure on currencies linked to global trade and economic growth, including the Australian Dollar.

As long as cautious sentiment dominates financial markets, the Greenback is likely to remain well supported.

Summary

The Australian Dollar remained under pressure as China’s manufacturing data met expectations but failed to improve confidence about the country’s broader economic outlook. Continued weakness in domestic demand within China also limited support for Australia’s currency.

Meanwhile, the US Dollar strengthened on the back of solid labor market data, lower job cuts, and increased safe-haven demand driven by geopolitical uncertainty in the Middle East. Investors are also expecting the Federal Reserve to maintain a cautious approach as economic conditions remain firm.

Looking ahead, attention is focused on the US ADP Employment Change report, the ISM Manufacturing PMI, and the upcoming Nonfarm Payrolls report. These important releases are expected to provide fresh insight into the health of the US economy and could shape expectations for future Federal Reserve policy, making them key events for AUD/USD traders in the coming days.

NZDUSD Under Selling Pressure as Risk-Off Mood Boosts US Dollar Strength

The NZDUSD currency pair remained under pressure after giving back the modest gains seen in the previous trading session. Several global factors combined to weigh on the New Zealand Dollar while strengthening demand for the US Dollar. Softer business activity signals from China, growing geopolitical uncertainty in the Middle East, and increasing expectations of tighter US monetary policy all played an important role in shaping market sentiment.

NZDUSD reached higher low area of the ascending triangle pattern

Investors are also preparing for a series of major US economic events that could influence the Federal Reserve’s next policy decisions. These developments are keeping traders cautious and increasing volatility across the foreign exchange market.

China’s Manufacturing Data Weighs on the New Zealand Dollar

One of the biggest reasons behind the weakness in the New Zealand Dollar was the latest manufacturing data from China. China’s RatingDog Manufacturing Purchasing Managers’ Index (PMI) came in at 51.7 for June, slightly lower than the previous reading of 51.8. Although the figure matched market expectations, the decline highlighted that manufacturing growth is losing some momentum.

China is New Zealand’s largest trading partner, making its economic performance especially important for the Kiwi. When Chinese factories slow down, investors often worry that demand for New Zealand’s exports could weaken in the coming months.

Because of these close trade ties, any sign of slower economic activity in China tends to reduce confidence in the New Zealand economy. This relationship often causes the New Zealand Dollar to lose strength whenever Chinese economic data disappoints or points toward slower growth.

US Dollar Benefits from Safe-Haven Demand

While the New Zealand Dollar faced pressure, the US Dollar found support as investors looked for safer assets amid rising geopolitical tensions.

Concerns increased after developments surrounding peace efforts between the United States and Iran. US representatives traveled to Doha, Qatar, for discussions aimed at reducing tensions through diplomatic channels. However, hopes for quick progress faded after Iran announced it would not participate in direct talks with the US delegation.

This unexpected setback increased uncertainty about the future of negotiations and reminded investors that geopolitical risks remain elevated. Whenever global tensions rise, many market participants move their money into traditionally safer assets, including the US Dollar.

As a result, the Greenback gained strength against several major currencies, including the New Zealand Dollar.

Geopolitical Uncertainty Continues to Influence Financial Markets

Political developments often have a significant impact on currency markets, especially when they involve major global powers or regions with ongoing conflicts.

The latest news from the Middle East has once again highlighted how quickly market sentiment can change. The lack of direct communication between US and Iranian officials has reduced confidence that a lasting diplomatic solution can be reached in the near future.

Investors generally dislike uncertainty. When geopolitical risks increase, they often reduce exposure to risk-sensitive currencies like the New Zealand Dollar and instead move toward assets considered more stable during periods of uncertainty.

Until there are clearer signs of diplomatic progress, geopolitical concerns are likely to remain an important driver of market sentiment.

Federal Reserve Outlook Continues to Support the US Dollar

Another major factor supporting the US Dollar is the growing belief that the Federal Reserve could maintain a tighter monetary policy for longer.

At its latest policy meeting, the Federal Reserve kept interest rates unchanged. However, policymakers removed earlier language that had suggested possible future rate cuts. This change signaled that the central bank is becoming more cautious about easing monetary policy.

Markets interpreted this shift as a more hawkish stance, leading investors to increase expectations that borrowing costs could remain higher if inflation and economic conditions continue to support such a move.

A stronger outlook for US interest rates generally increases demand for the US Dollar because higher rates can make dollar-based investments more attractive to global investors.

Markets See Higher Chances of Another Rate Hike

Investor expectations have shifted noticeably in recent weeks.

According to the CME FedWatch Tool, futures markets are now pricing in nearly a 63% probability that the Federal Reserve could raise interest rates by September. While future decisions will depend on incoming economic data, this growing expectation has provided additional support for the US Dollar.

Financial markets constantly adjust their expectations as new economic information becomes available. Every important report has the potential to strengthen or weaken confidence in future policy decisions.

For now, expectations of tighter monetary policy continue to favor the US currency over many of its global counterparts.

Key US Economic Reports Are in Focus

The coming days will be packed with important economic events that could influence market direction.

Investors are closely watching Federal Reserve Chairman Kevin Warsh’s appearance at the European Central Bank Forum in Sintra. His comments may provide valuable clues about the central bank’s current thinking and its outlook for the US economy.

In addition, several major economic reports are scheduled for release, including the ADP private employment report and the ISM Manufacturing PMI. These reports will offer fresh insight into the health of the US labor market and manufacturing sector.

The week will conclude with the closely watched Nonfarm Payrolls (NFP) report. This monthly employment report is considered one of the most influential economic releases because it provides a broad picture of job creation, unemployment, and wage growth in the United States.

Strong employment data could reinforce expectations for tighter monetary policy, while weaker results could lead investors to reassess the Federal Reserve’s future plans.

Why Traders Are Remaining Cautious

With several major economic events approaching, traders are avoiding aggressive positions until more information becomes available.

Economic reports, central bank commentary, and geopolitical developments are all arriving within a short period, creating an environment where market sentiment can change rapidly.

This combination of uncertainty encourages investors to carefully monitor every new headline before making significant trading decisions.

For currency markets, balancing economic growth, inflation, central bank policy, and geopolitical developments remains essential when assessing future trends.

Summary

NZDUSD remains under pressure as several global factors continue to favor the US Dollar over the New Zealand Dollar. Softer manufacturing activity in China has raised concerns about demand for New Zealand’s exports, while ongoing geopolitical tensions in the Middle East have increased safe-haven demand for the US currency.

At the same time, expectations that the Federal Reserve could maintain a hawkish policy stance have strengthened confidence in the US Dollar. Investors are now turning their attention to upcoming speeches from Federal Reserve officials and a series of important US economic reports, including employment and manufacturing data, which are expected to provide fresh direction for financial markets in the days ahead.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!