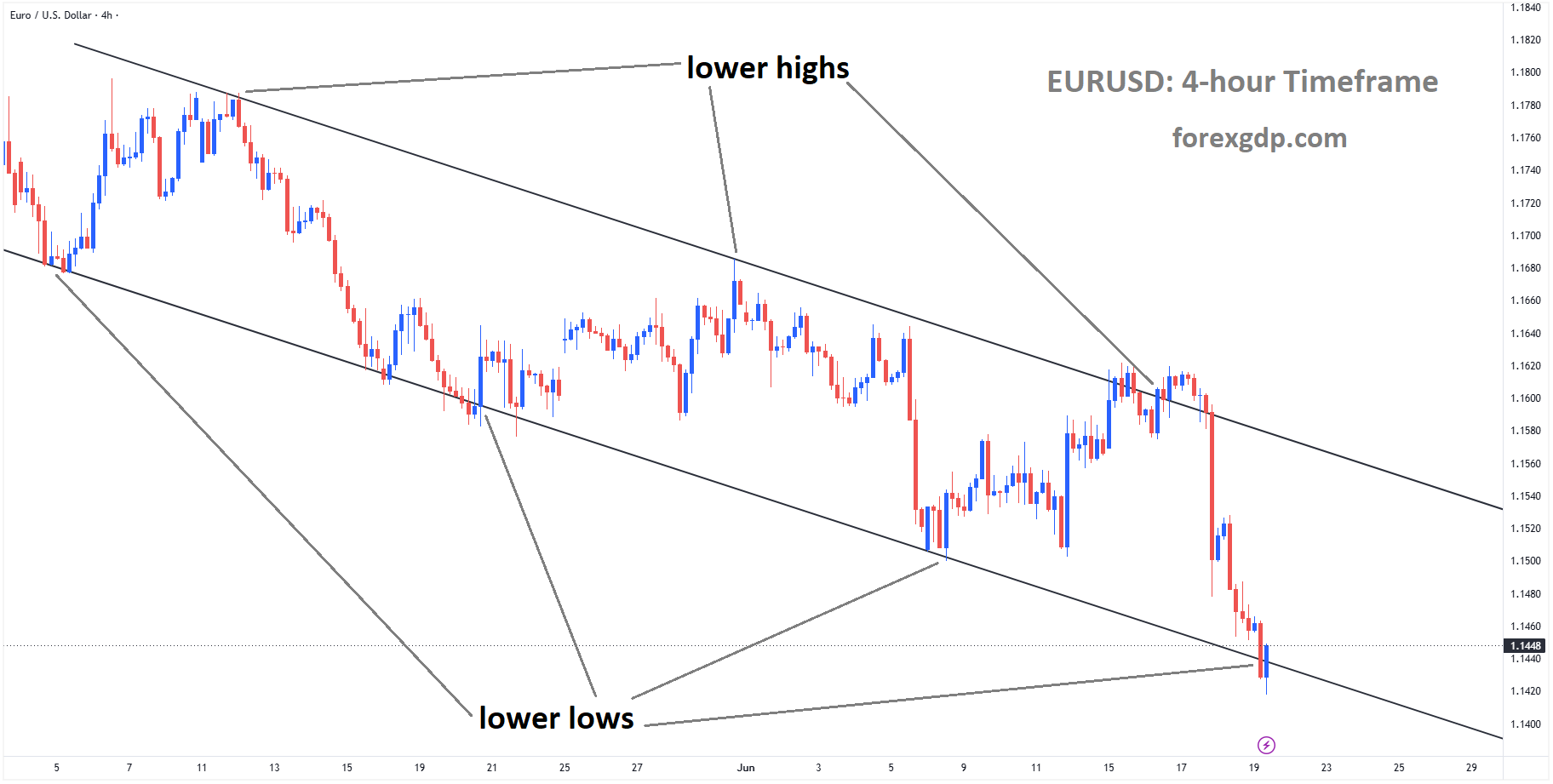

EURUSD is moving in a descending channel, and the market has reached the lower low area of the channel

EURUSD Finds Support as Traders Lock In Dollar Gains Following Recent Surge

The EUR/USD currency pair showed a modest recovery on Friday, climbing back toward the 1.1460 area after touching its lowest level in three months. Despite the rebound, the Euro remains under pressure and is still set to finish the week with notable losses against the US Dollar.

The recent weakness in the Euro has largely been driven by growing confidence that the US Federal Reserve could maintain a tighter monetary policy stance for longer than previously expected. This shift in expectations has strengthened demand for the US Dollar and weighed on major rival currencies.

US Dollar Pauses After Strong Weekly Rally

After several days of gains, the US Dollar eased slightly on Friday as trading activity remained subdued due to the Juneteenth holiday in the United States. With many financial institutions closed, market participation was lower than usual, leading to limited price movements across currency markets.

The temporary pullback in the Dollar allowed the Euro to recover some ground from recent lows. However, the rebound lacked strong momentum, suggesting that investors remain cautious about significantly reducing their exposure to the US currency.

While global sentiment received some support from optimism surrounding a reported US-Iran peace agreement and declining oil prices, these developments did not provide enough strength to trigger a meaningful recovery in the Euro.

Federal Reserve Policy Expectations Continue to Drive Markets

A major factor supporting the US Dollar is the growing belief that the Federal Reserve may still have room to tighten monetary policy later this year.

Earlier this week, the Fed decided to leave interest rates unchanged. However, updated projections from policymakers indicated that a significant portion of the committee still expects at least one additional rate increase before the end of the year.

Adding to the market’s confidence, Federal Reserve Chairman Kevin Warsh reaffirmed the central bank’s commitment to bringing inflation back to its target level. His comments reinforced expectations that policymakers remain focused on controlling price pressures and are prepared to take further action if necessary.

This outlook has encouraged investors to favor the Dollar, as higher interest rates generally make US assets more attractive compared to those in other regions.

Strong US Economic Data Supports the Dollar

Economic data released during the week also helped strengthen confidence in the US economy.

Recent reports showed that consumer spending remained healthy, with retail sales in May exceeding expectations. Strong consumer activity is often viewed as a sign of economic resilience because household spending accounts for a large share of overall economic growth.

At the same time, the Philadelphia Federal Reserve Manufacturing Survey pointed to a significant improvement in business conditions during June. The stronger-than-expected results suggested that parts of the manufacturing sector are regaining momentum despite ongoing geopolitical uncertainties.

These indicators have helped reassure investors that the US economy remains relatively strong, reducing concerns about an immediate slowdown and supporting the case for maintaining a firm monetary policy stance.

Eurozone Faces a Different Economic Picture

While the United States has continued to deliver encouraging economic data, the situation in the Eurozone appears more mixed.

One of the latest indicators came from Germany, the region’s largest economy. Producer price data showed that prices at the factory gate increased compared to a year earlier, signaling that inflationary pressures have not completely disappeared.

However, the pace of monthly price growth slowed noticeably from the previous month. This moderation suggests that some of the inflation pressures linked to earlier energy market disruptions may be beginning to fade.

The easing of energy-related costs is generally positive for businesses and consumers. However, it also reduces pressure on the European Central Bank (ECB) to maintain an aggressive policy approach.

Lower Energy Costs Could Influence ECB Decisions

The recent decline in oil prices has become another important factor for European policymakers.

Lower energy costs can help ease inflation across the Eurozone by reducing expenses for transportation, manufacturing, and households. While this supports economic stability, it may also lessen the urgency for the ECB to introduce further interest-rate increases.

As a result, investors are increasingly comparing the policy outlooks of the ECB and the Federal Reserve. At present, the Fed appears more willing to keep a restrictive stance if inflation remains elevated, while expectations for additional ECB tightening have become less certain.

This divergence in policy expectations has created a favorable environment for the US Dollar and limited the Euro’s ability to stage a stronger recovery.

Market Focus Shifts to Future Central Bank Signals

Looking ahead, traders will continue monitoring economic releases and comments from central bank officials on both sides of the Atlantic.

Any signs that inflation remains stubbornly high in the United States could strengthen expectations for further Federal Reserve action, potentially providing additional support for the Dollar. Conversely, evidence of slowing economic momentum could prompt investors to reassess the outlook.

In Europe, upcoming inflation and growth figures will play a key role in shaping expectations for the ECB. Policymakers will need to balance the benefits of easing price pressures with the need to maintain economic growth across the region.

Summary

The Euro managed a modest rebound against the US Dollar after falling to a three-month low, but it remains on track for a weekly decline. Investor attention continues to focus on the Federal Reserve, where expectations for possible future policy tightening have strengthened support for the Dollar.

Strong US economic data, combined with the Fed’s commitment to controlling inflation, has reinforced confidence in the American economy. Meanwhile, slower producer price growth and lower energy costs in Europe have reduced expectations for aggressive policy action from the European Central Bank.

As markets continue to assess the outlook for both central banks, differences in monetary policy expectations remain the key force shaping the direction of the EUR/USD exchange rate.

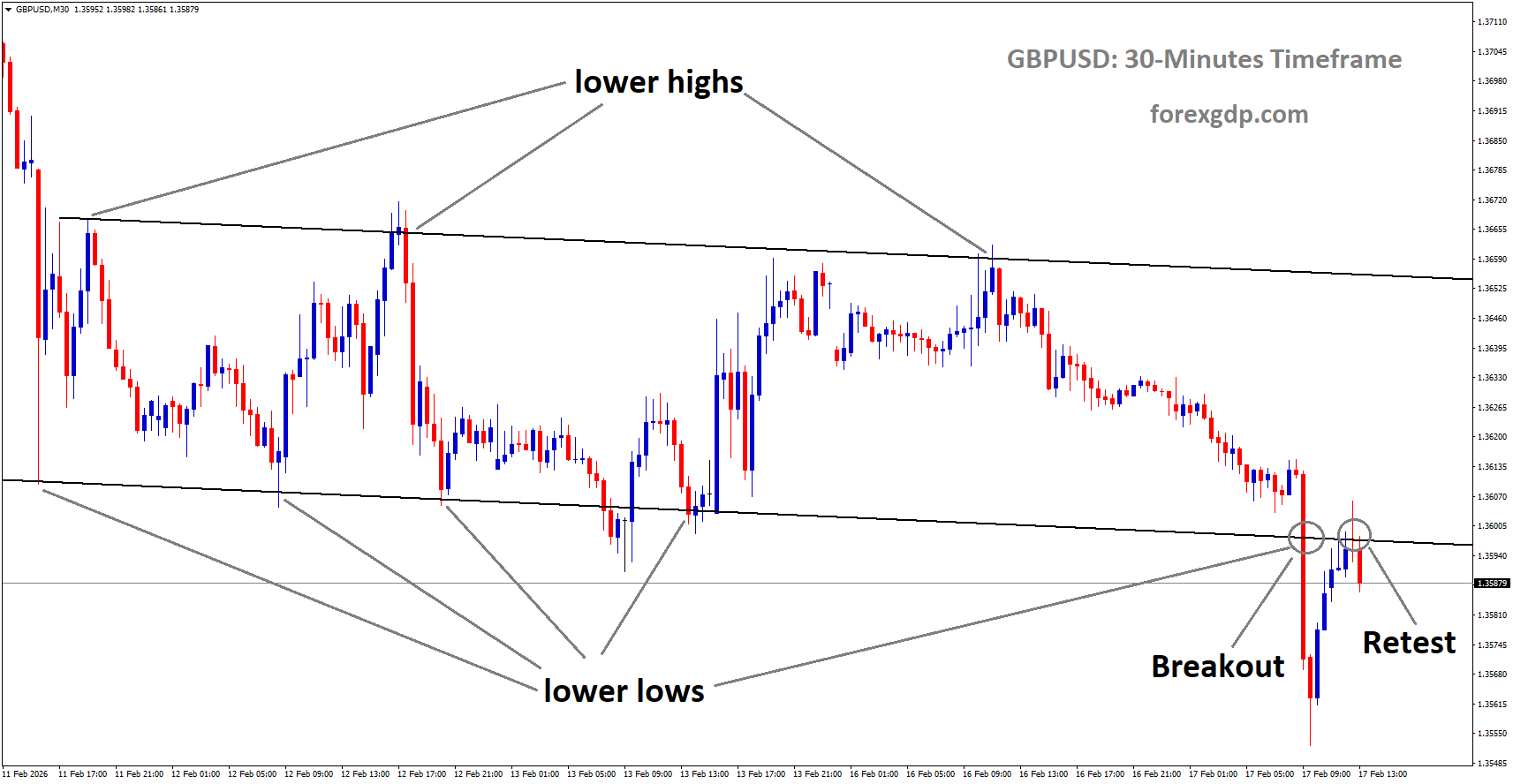

GBPUSD Extends Sharp Decline with Pound Under Pressure from UK Leadership Uncertainty

The British Pound continued to struggle against the US Dollar on Friday, with GBP/USD falling for a third consecutive trading session. The currency pair slipped below the 1.3200 level during Asian trading hours, reaching its weakest point since April and adding to a difficult week for the Pound.

GBPUSD reached the support area of the box pattern

A combination of political uncertainty in the United Kingdom, changing expectations for Bank of England policy, and renewed strength in the US Dollar has created a challenging environment for Sterling. As investors reassess economic and geopolitical developments, market sentiment continues to favor the US currency.

UK Political Developments Add Pressure on the Pound

One of the key factors affecting the British Pound is growing political uncertainty within the UK. Investors are closely watching domestic political events after Greater Manchester Mayor Andy Burnham secured a parliamentary seat in northern England.

Following his victory, Burnham suggested that the result could mark a significant moment in British politics. He also indicated that his party faces a crucial opportunity to change direction, comments that have fueled speculation about future political shifts and leadership challenges.

Political instability often creates uncertainty for investors because it can complicate government decision-making and economic planning. As a result, concerns surrounding the UK’s political landscape have contributed to weaker demand for the Pound.

Bank of England Rate Expectations Continue to Shift

The Pound has also come under pressure from changing expectations regarding future monetary policy decisions by the Bank of England (BoE).

Earlier this week, softer-than-expected inflation data prompted investors to reduce expectations for aggressive interest rate increases in the coming months. Inflation figures are closely monitored because they often influence central bank decisions on borrowing costs.

In addition, easing concerns about a major energy price shock have reinforced expectations that the BoE may be comfortable maintaining its current policy stance for a longer period. A recently announced US-Iran peace agreement has helped reduce fears of disruptions in energy markets, which could lessen inflationary pressures globally.

With traders now expecting a more cautious approach from the Bank of England, the Pound has lost one of the key supports that previously helped strengthen the currency.

Federal Reserve Supports a Stronger Dollar

While the British Pound faces multiple headwinds, the US Dollar continues to benefit from supportive economic and policy factors.

The Federal Reserve has recently maintained a relatively hawkish tone, signaling that additional policy tightening remains possible before the end of the year. Policymakers have indicated that inflation risks still require close attention, leading investors to believe that interest rates could remain elevated for longer than previously expected.

This outlook has helped strengthen the Dollar against several major currencies, including the Pound. Investors often favor currencies backed by higher interest rate expectations because they can offer more attractive returns on investments.

As a result, the widening contrast between Federal Reserve and Bank of England policy expectations has further boosted demand for the US currency.

Geopolitical Risks Increase Demand for Safe-Haven Assets

Global geopolitical developments are also influencing currency markets.

Recent uncertainty surrounding diplomatic efforts between the United States and Iran has created fresh concerns among investors. US Vice President JD Vance reportedly canceled a planned trip to Switzerland for discussions with Iranian officials, stating that the meeting had not yet been finalized.

At the same time, reports of Israeli air strikes in Lebanon have raised fears that tensions in the region could escalate and potentially undermine progress made through the US-Iran agreement.

Whenever geopolitical uncertainty increases, investors often seek the relative safety of assets perceived as more stable. The US Dollar is widely regarded as one of the world’s leading safe-haven currencies, meaning it tends to attract demand during periods of global uncertainty.

This shift toward safety has provided additional support for the Dollar while adding further pressure on GBP/USD.

Investors Await Fresh UK Economic Data

Market participants are now turning their attention to upcoming UK economic releases for potential clues about the country’s economic health and the future direction of monetary policy.

The latest monthly Retail Sales data is expected to be closely watched. Consumer spending remains a critical part of the UK economy, and stronger or weaker spending figures could influence expectations for future Bank of England decisions.

A positive surprise could provide some temporary support for the Pound. However, given the current combination of political uncertainty, softer inflation trends, and a stronger US Dollar, any recovery attempts may face significant challenges.

Why GBP/USD Remains Under Pressure

Several factors are currently working against the British Pound:

Ongoing political uncertainty in the United Kingdom.

Reduced expectations for aggressive Bank of England rate increases.

Stronger US Dollar demand supported by Federal Reserve policy expectations.

Increased geopolitical risks encouraging investors to seek safe-haven assets.

Cautious sentiment ahead of important UK economic data releases.

Together, these developments have created a difficult environment for Sterling and have helped drive GBP/USD lower throughout the week.

Summary

GBP/USD has extended its decline for a third straight day as investors continue to favor the US Dollar over the British Pound. Political uncertainty in the UK, softer inflation data, and expectations that the Bank of England may keep interest rates unchanged have weakened support for Sterling. Meanwhile, the Federal Reserve’s firm policy stance and renewed geopolitical concerns have strengthened the appeal of the US Dollar. With traders awaiting fresh UK Retail Sales figures, market attention remains focused on whether upcoming economic data can provide any relief for the struggling Pound.

USDJPY Retreats from Recent Highs as BoJ Tightening Outlook Lifts Japanese Yen

The Japanese Yen gained strength against the US Dollar after fresh signals from the Bank of Japan (BoJ) suggested that further interest rate increases remain a possibility. As a result, the USD/JPY currency pair moved lower, ending a strong multi-day rally that had pushed it to its highest level since mid-2024.

USDJPY reached a higher high area of the ascending channel

While the decline reflects growing confidence in the Japanese currency, the broader outlook remains mixed. Investors continue to weigh the possibility of tighter monetary policy in Japan against the still-significant interest rate gap between Japan and the United States.

BoJ Minutes Highlight Concerns About Inflation

The latest support for the Yen came after the release of minutes from the Bank of Japan’s April policy meeting. The document revealed that several policymakers favored moving more quickly with interest rate increases to prevent inflation from rising too far above desired levels.

Officials noted that inflationary pressures could strengthen in the coming months as higher business costs are gradually passed on to consumers. This assessment reinforced expectations that Japan’s central bank may continue normalizing monetary policy after years of maintaining extremely low interest rates.

The minutes added to recent comments from BoJ Deputy Governor Shinichi Himino, who indicated that future rate decisions would depend on economic growth, inflation trends, and financial market conditions. His remarks suggested that additional policy tightening remains a realistic possibility if economic data continue to support such action.

Currency Intervention Concerns Boost the Yen

Apart from expectations of higher interest rates, concerns about potential government intervention also provided support to the Japanese currency.

Japanese officials have repeatedly expressed concern about excessive currency movements. Recent comments from government representatives emphasized that authorities remain prepared to respond if exchange-rate fluctuations become too disruptive.

These statements have fueled speculation that policymakers could step in if the Yen weakens too rapidly. Such intervention concerns often discourage traders from aggressively betting against the Japanese currency, helping it maintain support even during periods of broader market pressure.

The combination of possible rate hikes and intervention risks created a favorable backdrop for the Yen, contributing to the pullback in USD/JPY.

Inflation Data Sends Mixed Signals

Recent inflation figures from Japan offered a more nuanced picture of the country’s economic conditions.

Data showed that consumer inflation continued to rise on an annual basis during May. However, some underlying inflation measures remained below the Bank of Japan’s long-term target.

A closely watched indicator that excludes both fresh food and energy prices slowed slightly compared to the previous month. It also remained below the BoJ’s 2% inflation objective for a fourth consecutive month, marking the weakest pace in several years.

Under normal circumstances, softer inflation readings could reduce expectations for future rate increases. However, financial markets largely focused on the central bank’s policy signals rather than the weaker inflation data.

Investors appear to believe that policymakers remain concerned about longer-term inflation risks and could continue tightening policy if economic conditions remain supportive.

US Dollar Remains Supported by Federal Reserve Policy

Despite the Yen’s recent gains, the US Dollar continues to benefit from relatively higher interest rates in the United States.

The Federal Reserve recently chose to keep its benchmark interest rate unchanged, maintaining a significantly higher rate environment than Japan. While markets continue to monitor future Fed policy decisions, current settings still offer stronger returns for investors holding Dollar-denominated assets.

This advantage has helped the US Dollar maintain broad strength against many global currencies throughout the week.

As a result, any substantial decline in USD/JPY may face resistance, especially if US economic data remain resilient and Federal Reserve officials continue to adopt a cautious approach toward rate reductions.

Interest Rate Gap Remains a Key Factor

One of the most important drivers of the USD/JPY pair continues to be the difference between interest rates in the United States and Japan.

Although the Bank of Japan has gradually moved away from its ultra-loose monetary policy stance, Japanese rates remain considerably lower than those in the US. This gap encourages investors to borrow in low-yielding currencies such as the Yen and invest in higher-yielding assets elsewhere, a strategy commonly known as the carry trade.

The popularity of these trades tends to limit sustained Yen appreciation because demand for foreign currencies remains strong.

Even after Japan’s recent rate increases, the overall yield advantage still favors the US Dollar. This dynamic explains why many market participants remain cautious about expecting a prolonged decline in USD/JPY despite the recent pullback.

Investors Looking for Stronger Confirmation

The latest drop in USD/JPY reflects a combination of factors supporting the Japanese currency, including hawkish signals from the Bank of Japan and renewed concerns about potential government intervention.

However, the broader picture remains more balanced. While Japan is gradually moving toward tighter monetary policy, the United States continues to maintain a higher interest rate environment that supports the Dollar.

Because of these competing forces, traders may look for additional economic data and policy guidance before making stronger commitments in either direction. Future comments from central bank officials, inflation reports, and broader economic indicators are likely to play a crucial role in shaping the next major move for the currency pair.

Summary

The Japanese Yen strengthened after Bank of Japan meeting minutes revealed growing support for further interest rate increases. Additional support came from concerns that Japanese authorities could intervene to address excessive currency movements. While softer inflation data offered some caution, investors focused more on the possibility of continued policy tightening.

At the same time, the US Dollar remains supported by higher interest rates in the United States, maintaining a significant yield advantage over Japan. This ongoing rate gap continues to limit the potential for a deeper USD/JPY decline, leaving investors closely watching upcoming economic and central bank developments for clearer direction.

USDCHF Extends Rally as Traders Brace for Possible US Rate Increase and Geopolitical Uncertainty

The US Dollar continued to strengthen against the Swiss Franc on Friday, pushing the USD/CHF currency pair to its highest level since December 2025. The move reflects growing confidence in the US Dollar after the Federal Reserve maintained a firm policy stance, while ongoing geopolitical uncertainty has also contributed to demand for the greenback.

USDCHF reached a higher high area of the ascending channel

At the same time, the Swiss National Bank (SNB) kept its benchmark interest rate unchanged and reiterated its willingness to step into currency markets if necessary, highlighting concerns about excessive strength in the Swiss Franc.

Federal Reserve Supports US Dollar Strength

One of the main drivers behind the recent gains in USD/CHF has been the Federal Reserve’s latest policy decision.

During its June meeting, the US central bank chose to leave interest rates unchanged. While the decision itself was widely expected, investors focused more closely on the Fed’s broader message. Policymakers indicated that additional rate increases remain possible later in the year if inflation pressures continue to require attention.

The meeting also marked the first policy gathering under the leadership of Federal Reserve Chair Kevin Warsh. Speaking after the decision, Warsh emphasized that maintaining price stability remains the central bank’s primary objective.

His comments reinforced expectations that the Fed is not yet ready to declare victory over inflation. As a result, market participants increasingly believe that tighter monetary policy could still be on the table in the coming months.

Investors Adjust Expectations for Future Rate Decisions

Financial markets quickly reacted to the Fed’s messaging.

Many traders now expect the possibility of another rate increase before the end of the year. Expectations of tighter monetary policy generally support the US Dollar because higher interest rates can make dollar-denominated assets more attractive to global investors.

The shift in market sentiment has helped strengthen the greenback against several major currencies, including the Swiss Franc. As investors reassess the outlook for US monetary policy, the Dollar has gained additional momentum, especially against currencies associated with lower interest-rate environments.

This divergence between US and Swiss monetary policy has become an important factor influencing currency markets.

Geopolitical Developments Add to Market Uncertainty

Beyond monetary policy, geopolitical events are also shaping investor sentiment.

Attention has recently turned to developments involving the United States and Iran. US Vice President JD Vance reportedly canceled a planned visit to Switzerland, where discussions with Iranian representatives were expected to begin regarding the implementation of a broader agreement aimed at ending hostilities between Washington and Tehran.

The planned negotiations were viewed as an important step toward stabilizing relations following a period of conflict. However, the cancellation has raised questions about the timing and progress of future diplomatic efforts.

Markets generally react quickly to uncertainty in politically sensitive regions. Any signs of delays or complications in peace-related discussions can increase investor caution and support demand for assets viewed as relatively stable.

As developments unfold, traders will continue monitoring headlines related to the US-Iran agreement and broader Middle East stability.

Swiss National Bank Maintains Cautious Approach

While the Federal Reserve maintained a firm tone, the Swiss National Bank took a different path.

The SNB left its key policy rate unchanged at 0%, a decision that matched market expectations. Switzerland continues to maintain one of the lowest interest-rate environments among major developed economies.

The central bank’s decision reflects its ongoing effort to balance economic growth, inflation trends, and currency stability.

Importantly, Swiss policymakers also reiterated that they remain prepared to intervene in foreign exchange markets if necessary. Such intervention could be used to prevent excessive appreciation of the Swiss Franc, which often attracts investors during periods of global uncertainty.

A stronger Franc can create challenges for Switzerland’s export-driven economy by making Swiss goods and services more expensive in international markets. As a result, the SNB remains attentive to currency movements and has left the door open for future action if market conditions require it.

Why the Swiss Franc Remains a Key Safe-Haven Currency

The Swiss Franc has long been considered one of the world’s leading safe-haven currencies.

During periods of economic uncertainty, geopolitical tensions, or financial market volatility, investors often move funds into the Franc because of Switzerland’s reputation for political stability, strong institutions, and a resilient financial system.

However, the current environment has created competing forces. On one hand, geopolitical concerns could support demand for safe-haven assets like the Franc. On the other hand, expectations of potentially higher US interest rates have increased the attractiveness of the US Dollar.

For now, the latter factor appears to be having a stronger influence on market sentiment, helping the Dollar outperform the Swiss currency.

Market Focus Turns to Upcoming Economic and Political Events

Looking ahead, investors will continue to watch several key developments that could influence the direction of USD/CHF.

Federal Reserve officials are expected to provide additional guidance through speeches and economic assessments in the coming weeks. Any indication that policymakers are becoming more confident about future rate increases could further support the Dollar.

Meanwhile, diplomatic developments involving the United States and Iran remain an important source of uncertainty. Progress toward implementing existing agreements could calm market concerns, while setbacks could increase volatility.

In Switzerland, traders will monitor any further comments from the SNB regarding currency intervention and economic conditions. The central bank’s approach to managing Franc strength will remain a significant factor for currency markets.

Summary

USD/CHF moved higher on Friday, reaching its strongest level in more than six months as investors responded positively to the Federal Reserve’s firm policy stance. Expectations that US interest rates could rise again later this year have strengthened the Dollar and boosted demand for US assets.

At the same time, geopolitical uncertainty surrounding US-Iran relations has added another layer of support for the greenback. Meanwhile, the Swiss National Bank maintained its benchmark rate at 0% and reaffirmed its readiness to act if the Swiss Franc becomes excessively strong.

With monetary policy expectations, global diplomacy, and central bank actions all influencing market sentiment, traders are likely to remain focused on both economic signals and geopolitical developments in the weeks ahead.

USDCAD Extends Rally with Canadian Dollar Hit by Cooling Crude Prices

The USD/CAD currency pair extended its gains for a third consecutive session on Friday, supported by weakness in the Canadian Dollar and renewed strength in the US Dollar. A combination of declining oil prices, improving geopolitical conditions in the Middle East, and a firm stance from the US Federal Reserve helped push the pair higher during Asian trading hours.

USDCAD reached the higher high area of the ascending channel

The Canadian Dollar, often influenced by movements in the energy market, faced renewed pressure as crude oil prices moved lower. At the same time, investors continued to assess the Federal Reserve’s latest policy decision, which signaled that further interest rate increases remain a possibility despite rates being left unchanged this week.

Falling Oil Prices Weigh on the Canadian Dollar

One of the main drivers behind the latest move in USD/CAD has been the decline in oil prices. Canada is among the world’s largest oil exporters, with a significant portion of its crude shipments heading to the United States. As a result, fluctuations in oil prices often have a direct impact on the value of the Canadian Dollar.

Crude oil prices slipped after signs of easing tensions in the Middle East improved confidence in global energy supply routes. The decline erased some of the gains recorded earlier in the week and contributed to broader weakness in commodity-linked currencies.

When oil prices fall, Canada’s export revenues can come under pressure. Lower income from energy exports may reduce demand for the Canadian Dollar, making it less attractive to investors and traders. This relationship frequently causes the currency to weaken during periods of declining crude prices.

US-Iran Agreement Improves Market Sentiment

A major development influencing the energy market has been the progress made between the United States and Iran.

According to reports, both countries have reached an initial agreement that opens the door to a 60-day negotiation period aimed at achieving a broader peace deal. The announcement has been viewed as a positive step toward reducing tensions in the region.

Adding to the optimism, the US military confirmed that maritime restrictions around Iranian ports and coastal waters have been removed. The decision effectively restores normal shipping activity through important trade routes, including areas connected to the Strait of Hormuz.

The Strait of Hormuz is one of the world’s most critical energy transit corridors, with millions of barrels of oil moving through the waterway each day. Any disruption in the region can create concerns about supply shortages and drive energy prices higher. Conversely, improved shipping conditions tend to reduce fears of supply constraints, which can place downward pressure on oil prices.

The return of smoother maritime traffic has reassured energy markets that global oil flows are becoming more stable. This development has been a key factor behind the recent weakness in crude prices.

Federal Reserve Maintains Rates but Keeps Hawkish Tone

While developments in the oil market affected the Canadian Dollar, the US Dollar found support from the Federal Reserve’s latest policy meeting.

The Federal Open Market Committee decided to leave its benchmark interest rate unchanged. The decision was widely expected by financial markets and received unanimous support from policymakers.

However, the overall message from the central bank was far from dovish. Policymakers signaled that inflation remains a concern and that additional tightening may still be necessary if price pressures persist.

Notably, nearly half of the Federal Reserve officials indicated that at least one more interest rate increase could be appropriate before the end of the year. This outlook reinforced expectations that US monetary policy could remain restrictive for an extended period.

New Fed Leadership Reinforces Focus on Inflation

Investors also paid close attention to comments from newly appointed Federal Reserve Chairman Kevin Warsh, who delivered his first press conference following the policy announcement.

Warsh emphasized that maintaining price stability remains the central bank’s primary objective. His remarks highlighted the Fed’s commitment to controlling inflation even as economic conditions continue to evolve.

The chairman’s comments were interpreted as supportive for the US Dollar because higher interest rates generally increase the appeal of dollar-denominated assets. When investors expect rates to remain elevated or move higher, demand for the US currency often strengthens.

This policy outlook has helped provide additional momentum for USD/CAD, especially at a time when the Canadian Dollar is already facing headwinds from lower oil prices.

Why USD/CAD Is Moving Higher

The recent rise in USD/CAD reflects the combined impact of two important market themes.

On one side, declining oil prices are reducing support for the Canadian Dollar by raising concerns about weaker export earnings from Canada’s energy sector. On the other side, the Federal Reserve’s firm stance on inflation is boosting confidence in the US Dollar.

Geopolitical developments have further amplified these trends. Progress in negotiations between the United States and Iran has improved the outlook for global energy supplies, easing concerns about disruptions and contributing to lower crude prices.

At the same time, expectations that US interest rates could remain high for longer continue to attract investor interest toward the greenback.

Summary

USD/CAD continued its upward momentum as the Canadian Dollar struggled under the weight of falling oil prices. Improved shipping conditions around Iran and progress toward a potential US-Iran peace agreement have helped stabilize global energy supplies, reducing support for crude oil prices and, by extension, the Canadian currency.

Meanwhile, the US Dollar received backing from the Federal Reserve’s latest policy message. Although interest rates were left unchanged, officials signaled that further tightening remains possible, reinforcing expectations of a higher-for-longer rate environment. With oil prices weakening and the Fed maintaining a firm focus on inflation, USD/CAD remains supported by both commodity and monetary policy factors.

Don’t trade all the time, trade forex only at the confirmed trade setups