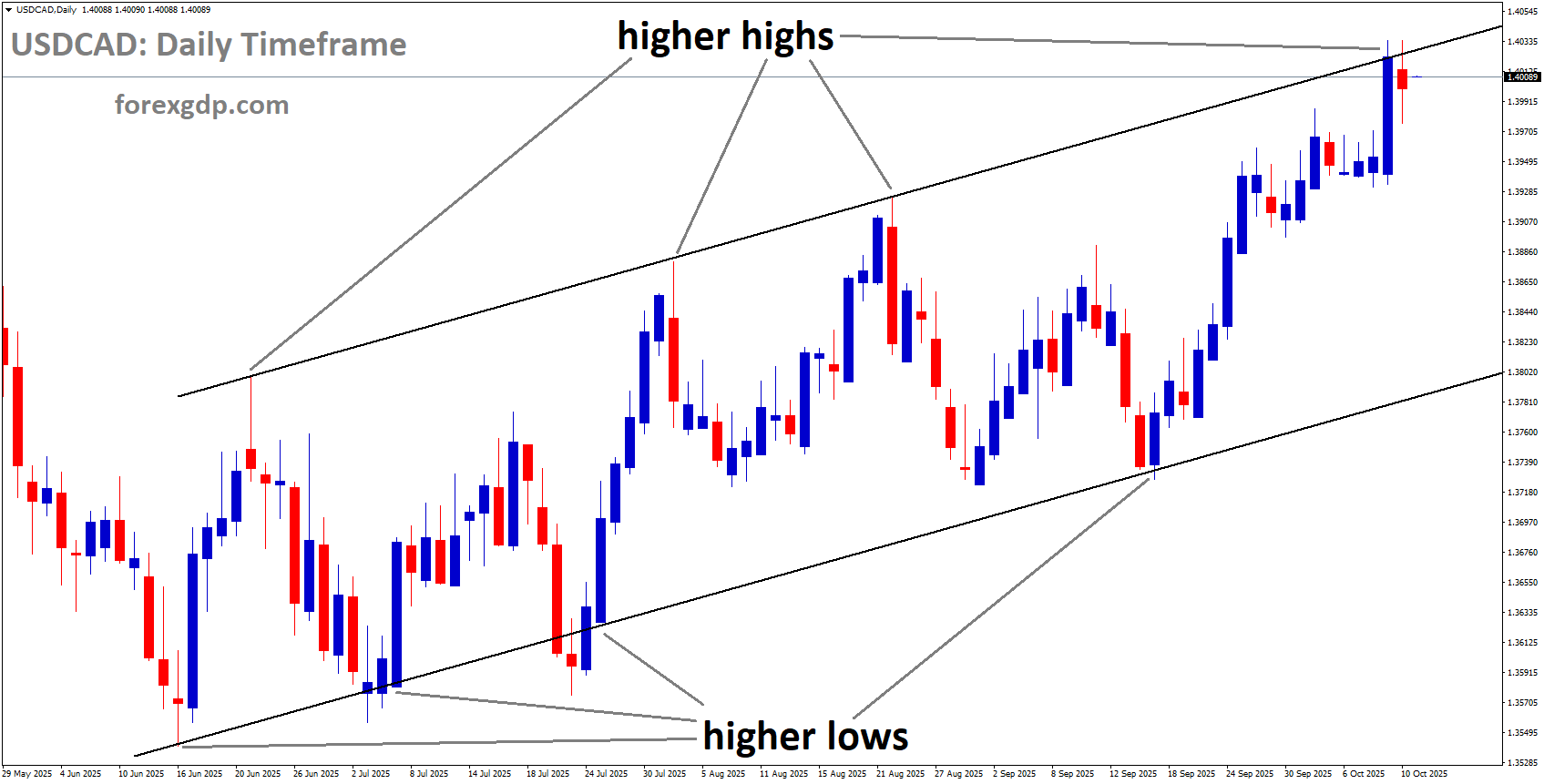

USDCAD is moving in an uptrend channel, and the market has reached a higher high area of the channel

USDCAD Weakens as Canada’s Job Surge Shifts Market Outlook for BoC Policy

The USD/CAD currency pair started the week on a softer note, weakening near the 1.40 mark in early European trading hours. The Canadian Dollar (CAD) gained ground against the US Dollar (USD) after Canada’s labor market data showed impressive strength in September. With job creation exceeding expectations, traders are rethinking their bets on another interest rate cut by the Bank of Canada (BoC). Meanwhile, a calmer tone in US-China trade relations offered some modest support to the Greenback, preventing a deeper decline.

Canada’s Job Market Surprises with Strong Growth

One of the main reasons behind the recent strength of the Canadian Dollar is the country’s remarkable employment report. According to Statistics Canada, the economy added over 60,000 jobs in September, far surpassing the modest expectations of around 5,000. This growth points to a resilient labor market despite global uncertainty and slowing growth in some sectors.

Unemployment Holds Steady

The unemployment rate remained unchanged at 7.1%, slightly better than analysts had predicted. This stability, combined with strong job creation, signals that Canada’s labor market continues to perform well even as other advanced economies struggle with softer employment trends. The mix of steady unemployment and strong hiring provides the Bank of Canada with a bit more breathing room when it comes to future monetary policy decisions.

What the Jobs Data Means for the Bank of Canada

The BoC recently lowered its benchmark interest rate by 25 basis points to 2.50%—its first cut since March. This move was intended to cushion the economy against trade-related pressures and slower global demand. However, the latest employment data may prompt policymakers to pause before delivering another rate cut.

Traders Rethink Interest Rate Bets

Before the release of the September job report, markets were pricing in a roughly 70% chance of another rate cut later this month. After the upbeat numbers, that probability dropped closer to 50%. The shift highlights how sensitive market expectations are to key economic indicators, especially employment data that reflects consumer spending potential and overall economic health.

Why This Matters to the Loonie

Interest rates play a crucial role in currency valuation. When rates remain stable or higher than expected, they often attract investors seeking better returns. This makes the Canadian Dollar more appealing relative to the US Dollar. If the BoC decides to keep rates steady for now, it could support the CAD further in the coming weeks.

Oil Prices Add Fuel to the Loonie’s Strength

Another key factor helping the Canadian Dollar is the recovery in crude oil prices. As the world’s largest oil exporter to the United States, Canada’s economy is heavily influenced by the energy market. When oil prices rise, the value of the Canadian Dollar typically strengthens, as it boosts export revenues and improves the country’s trade balance.

Higher oil prices can also encourage more foreign investment in Canadian energy sectors, indirectly supporting the currency. The combination of strong job data and an improving energy outlook provides a solid foundation for the Loonie’s recent gains.

The US Dollar Finds Some Relief from Trade Tensions

While the Canadian Dollar enjoyed support from local fundamentals, the US Dollar found a bit of comfort in political developments. Over the weekend, US President Donald Trump made remarks that temporarily eased concerns about escalating trade tensions with China. He stated that the situation with China “will all be fine,” signaling a more conciliatory stance compared to previous weeks.

Softened Rhetoric on Tariffs

Trump also suggested that he might not move forward with his earlier threat to impose a “massive increase of tariffs” on Chinese goods. This shift in tone was echoed by Vice President JD Vance, who said that the US was willing to negotiate as long as Beijing showed a “reasonable” attitude. These statements helped calm markets that had grown wary of another round of trade-related volatility.

Impact on the Greenback

Although the easing tensions offered a brief boost to market sentiment, it wasn’t enough to completely reverse the USD’s weakness against the CAD. Investors still view the Canadian economy’s recent performance as relatively stronger, especially when supported by domestic data rather than political commentary.

Investor Sentiment and the Broader Picture

The interplay between economic data, central bank policy, and global politics continues to shape currency movements. For the USD/CAD pair, these dynamics are especially important given the close trade relationship between the two countries and Canada’s dependence on exports.

Market Outlook

Traders are now watching for the next major event: the Bank of Canada’s policy decision scheduled for late October. If the central bank hints at maintaining rates rather than cutting further, it could extend the Canadian Dollar’s momentum. However, any signals of economic slowdown or dovish commentary might reverse some of the recent gains.

Meanwhile, investors are also keeping an eye on US economic indicators, including inflation and consumer spending, to gauge whether the Federal Reserve might shift its stance. If the Fed adopts a more cautious or dovish tone, the US Dollar could remain under pressure against most major currencies, including the Canadian Dollar.

What Could Happen Next?

Looking ahead, the USD/CAD pair may continue to experience fluctuations depending on several key factors:

-

Upcoming Canadian economic data – If other sectors such as retail sales or manufacturing also show strength, it would reinforce confidence in Canada’s growth outlook.

-

Oil market trends – Sustained strength in crude oil prices could further bolster the Loonie’s performance.

-

US political and economic developments – Any changes in trade policy or shifts in Federal Reserve communication could influence overall USD sentiment.

For now, the Canadian Dollar appears to have the upper hand, supported by domestic fundamentals and reduced expectations of further monetary easing.

Final Summary

The start of the week saw the USD/CAD pair weaken as Canada’s robust employment report gave the Loonie a solid boost. With over 60,000 new jobs created in September and unemployment steady, the market is less convinced that the Bank of Canada will deliver another rate cut soon. Rising oil prices and easing US-China trade tensions have also played their part in shaping recent movements.

While the US Dollar managed to stay afloat on improving trade sentiment, the Canadian Dollar remains supported by genuine economic strength rather than political rhetoric. Investors will now look toward upcoming BoC announcements and energy market trends for clues about where the pair might head next. For the moment, the Canadian Dollar stands on firmer ground, showing that strong domestic data can outshine global uncertainty.

EURUSD Dips as Global Risk Sentiment Fades and French Leadership Faces Scrutiny

The Euro has started the week on a weaker note, losing its earlier momentum as renewed worries over global trade disputes cloud investor sentiment. While the U.S.–China trade situation dominates the headlines, Europe is also facing political uncertainty, particularly in France, where changes in government leadership have added another layer of caution to the market mood.

This mix of global and regional developments has left traders unsure about the short-term direction of the Euro, leading to a more defensive stance across the market.

Global Trade Tensions: The Core of Market Anxiety

The biggest factor affecting market sentiment right now is the renewed tension between the United States and China. Recent remarks from both sides have reignited fears that the fragile balance in global trade could once again tip toward confrontation.

EURUSD has broken the Ascending Triangle on the downside

The Tariff Threat and Market Reaction

The latest spark came after U.S. President Donald Trump hinted at the possibility of imposing 100% tariffs on Chinese goods. The announcement immediately unsettled markets, as it revived memories of the previous trade war that slowed global growth and disrupted supply chains.

However, over the weekend, Trump softened his tone on social media, suggesting that the situation might not escalate further. His remarks helped calm some of the panic, though investors remain cautious, knowing how quickly political statements can shift.

For now, the markets appear to be taking a “wait and see” approach—hoping that the rhetoric cools down before concrete measures are taken. Still, the uncertainty has already affected risk appetite, with investors showing a preference for safe-haven assets and currencies.

China’s Response: A Firm Stand

In response to the U.S. threats, China’s Commerce Ministry defended its recent export restrictions on rare earth materials. These materials are essential for advanced manufacturing, including electronics and defense industries. According to Chinese officials, these limits are a matter of national interest and not a direct retaliation.

However, the ministry made it clear that China will not hesitate to act if the U.S. follows through with its tariff threats. This firm stance signals that neither side is willing to back down easily, keeping the global market on edge.

For currency traders, this tension has translated into increased volatility. Whenever trade concerns rise, the U.S. Dollar often strengthens as a safe-haven asset, while currencies like the Euro tend to weaken slightly in comparison.

Political Uncertainty in Europe Adds More Pressure

While global trade issues dominate headlines, Europe has its own set of challenges. In France, political uncertainty continues to weigh on investor confidence after recent government changes.

Macron’s Cabinet Shuffle

French President Emmanuel Macron recently reappointed Sébastien Lecornu as Prime Minister, just a week after his earlier resignation. This decision was seen as an effort to restore stability within the French government. Lecornu’s appointment of Roland Lescure, a close ally of Macron, as Finance Minister has been a key development.

Lescure faces a difficult task—introducing a strict budget that may include spending cuts and economic reforms. The French public has shown signs of frustration with similar measures in the past, so political resistance could be strong. For markets, this situation adds another layer of uncertainty, as France’s financial policies play a crucial role in shaping overall European economic confidence.

Cautious Investors Across Europe

Investors across the Eurozone are taking a conservative stance amid these developments. Many are waiting for more clarity on how France’s new government will handle fiscal challenges, especially at a time when inflation remains a concern and growth is uneven across the region.

The European Central Bank (ECB) also remains in the spotlight. ECB President Christine Lagarde is scheduled to speak at the International Monetary Fund (IMF) and World Bank meetings, where investors hope to gain insight into the central bank’s view on inflation trends and monetary policy direction. Her comments could provide hints about whether interest rates will remain steady or shift in the coming months.

Market Sentiment and Global Events Ahead

As the week begins, market activity may remain relatively quiet due to the U.S. holiday for Columbus Day. This means lower trading volumes, which can sometimes lead to more pronounced market moves on limited news.

Economic Indicators to Watch

Although the economic calendar is light, some key data from last week still linger in the background. The U.S. Michigan Consumer Sentiment Index showed slight improvement, suggesting that American consumers are feeling somewhat better about the economy. However, this small uptick hasn’t been enough to offset broader concerns about global trade and inflation pressures.

Meanwhile, investors are closely monitoring statements from global policymakers during the G20 meeting. Central bankers and finance ministers will be discussing global financial stability, inflation management, and trade cooperation. These conversations often influence future market expectations, especially regarding policy alignment between the U.S. Federal Reserve and the ECB.

The Broader Picture

Despite temporary optimism following Trump’s reassuring remarks, most analysts agree that uncertainty remains high. Trade tensions are not just about tariffs—they reflect deeper geopolitical rivalries that could take months, or even years, to fully resolve.

For Europe, this uncertainty comes at a delicate time. Economic recovery remains uneven, and the region still faces challenges in balancing fiscal responsibility with the need to support growth. France’s budget adjustments, for instance, could become a test case for how European economies manage competing priorities under pressure.

Final Summary

The Euro’s recent dip reflects a broader sense of caution spreading through global markets. Renewed fears of a U.S.–China trade conflict have dampened investor enthusiasm, while Europe’s internal political changes—particularly in France—add to the complexity.

Even though short-term reassurance came from softer U.S. rhetoric, markets are still walking on eggshells. Investors are waiting for more concrete signs that tensions will not escalate further and that European policymakers can maintain economic stability.

As the week progresses, attention will likely shift toward global finance meetings and central bank communications. These events could set the tone for how traders and investors navigate the remainder of the month.

In simple terms, the Euro’s struggle is not just about currency fluctuations—it reflects the world’s uneasy balance between political decisions, economic uncertainty, and the ongoing search for stability in unpredictable times.

GBPUSD Slips Lower as Traders Eye Renewed US-China Trade Uncertainty

The GBP/USD currency pair started the week on a quieter and weaker note, softening in the early Asian session. The global market’s focus has once again shifted to renewed trade tensions and upcoming UK economic updates. With political and financial uncertainties on both sides of the Atlantic, traders are keeping a cautious stance, closely watching how the situation unfolds.

US-China Tensions Take Center Stage Again

The global financial community is no stranger to trade tensions between the United States and China. Recently, these tensions have resurfaced after former US President Donald Trump threatened to impose fresh tariffs on Chinese imports. This move, aimed at putting pressure on Beijing, has triggered fresh worries among investors about a possible escalation in trade disputes.

GBPUSD reached the retest area of the broken descending Triangle pattern

Beijing’s Response and Its Global Impact

China responded by defending its export restrictions on rare earth materials and manufacturing equipment, citing them as necessary countermeasures to protect national interests. Although Beijing avoided announcing new tariffs in response, the tension itself has been enough to stir uncertainty in global markets.

When two of the world’s largest economies clash, it’s not just their bilateral trade that gets affected—it creates ripples across currencies, commodities, and investor sentiment globally.

How This Affects the US Dollar and the Pound

While one might expect such geopolitical tensions to weaken the US Dollar, the opposite has happened in the short term. Investors, seeking safety amid uncertainty, tend to flock toward the Dollar as a safe-haven currency. This behavior has put the Pound Sterling under pressure, leading to a softer GBP/USD movement.

The strength of the USD has thus overshadowed the tariff concerns, showing how deeply market sentiment can influence short-term currency movements.

UK’s Domestic Worries Add to the Pressure

Across the Atlantic, the UK economy faces its own challenges. The British Pound is dealing with multiple domestic concerns—ranging from fiscal policies to slowing growth indicators. While external events like US-China tensions affect market direction, internal economic conditions play an equally vital role in shaping the Pound’s performance.

Upcoming Bank of England Remarks

Traders are waiting for a scheduled speech by Catherine Mann, a member of the Bank of England’s Monetary Policy Committee. Mann is known for her firm stance on inflation control, and any hints about interest rate paths could move the market quickly.

If she suggests that inflation remains stubborn or that rate cuts are off the table for now, the Pound might find some temporary support. However, if her tone leans toward caution due to slowing economic activity, that could add further downside risk for GBP/USD.

Fiscal Policy Concerns: Tax Hikes on the Horizon

Adding to the uncertainty, reports suggest that the UK Chancellor of the Exchequer, Rachel Reeves, is expected to announce possible tax increases in the upcoming Autumn Statement. The move is aimed at managing the country’s rising debt levels, but it comes at a time when household budgets are already stretched.

Higher taxes could weigh on consumer confidence and spending, which in turn can slow down overall economic recovery. For the currency market, that’s another reason to stay cautious on the Pound in the coming weeks.

All Eyes on UK Employment Data

The next major event for the UK economy is the release of employment figures for the three months ending in August. Job market data has always been a critical indicator of economic health. If the report shows weakening job creation or a rise in unemployment, it could reinforce expectations that the UK economy is cooling faster than anticipated.

Such an outcome would likely pressure the Pound further, as it might push the Bank of England to adopt a more cautious stance in its monetary policy decisions.

Why Employment Data Matters So Much

Strong employment growth generally signals a stable economy, while a slowdown hints at underlying weaknesses. For traders, these numbers are crucial because they help predict future interest rate decisions. A weak job market gives policymakers reason to pause or even cut rates, whereas strong job growth supports rate hikes.

This is why even a small deviation from expectations in the employment data can trigger sharp reactions in the GBP/USD pair.

Global Market Mood: A Mix of Caution and Anticipation

The overall sentiment in the global market remains mixed. While some investors expect that tensions between the US and China may eventually ease through negotiation, others believe the situation could worsen before it improves. The uncertainty surrounding trade policies, combined with domestic challenges in the UK, makes it difficult for the Pound to find strong footing.

With the US markets closed for Columbus Day, trading volumes are expected to stay light early in the week. This often leads to more cautious trading behavior as investors prefer to wait for key speeches and data releases before taking large positions.

What Traders Are Watching Next

-

Catherine Mann’s Speech: Traders will closely monitor her tone and comments for any clues on future interest rate moves.

-

UK Employment Report: A potential slowdown here could pressure the Bank of England to take a softer policy approach.

-

US-China Developments: Any new statements or actions from either side could quickly shift market sentiment.

Each of these factors could independently move the market, but combined, they form a complex web of influences that determine how GBP/USD behaves in the near term.

Final Summary

The GBP/USD pair is facing a delicate balancing act between external pressures and domestic challenges. On one side, renewed trade tensions between the US and China have injected volatility into global markets, driving investors toward the Dollar. On the other, concerns about the UK’s fiscal outlook, possible tax increases, and slowing job growth are weighing on the Pound.

As the week progresses, all eyes remain on upcoming UK employment data and comments from BoE officials, which could define the currency’s short-term direction. While short-term fluctuations are expected, the broader picture shows that the Pound is struggling to gain momentum amid both global and domestic headwinds.

In times like these, traders often prefer patience over speculation, waiting for clearer economic signals before making big moves. Whether GBP/USD stabilizes or continues to slide will depend largely on how these upcoming events unfold—and how policymakers in both the UK and US choose to respond to the growing economic challenges.

USDJPY struggles while market optimism and Japan’s turmoil weigh on Yen

The Japanese Yen (JPY) has been struggling to hold its ground lately, weighed down by a mix of political instability, shifting market moods, and global monetary policy differences. Investors who once viewed the Yen as a safe-haven currency now find fewer reasons to rely on it, especially as new developments continue to shape the economic outlook. Let’s take a closer look at what’s driving the Yen’s current weakness and how broader market dynamics are influencing its direction.

USDJPY is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

Political Turmoil Adds to the Yen’s Weakness

Japan’s domestic politics have recently taken center stage, unsettling investor confidence and putting extra pressure on the Yen. The long-standing partnership between Japan’s Komeito party and the ruling Liberal Democratic Party (LDP) has come to an unexpected end after 26 years. This political shake-up is significant because it disrupts the country’s leadership stability, raising questions about future policies and governance.

Adding to the uncertainty, Sanae Takaichi’s push to become Japan’s first female Prime Minister now faces an uphill battle without Komeito’s support. For global investors, such political shifts often translate into hesitation and reduced demand for the Yen. Political unpredictability tends to drive funds toward more stable or higher-yielding assets elsewhere, leaving Japan’s currency exposed.

How Political Changes Affect Investor Confidence

When a country faces leadership uncertainty, it can delay crucial policy decisions, including those on economic reforms or fiscal stimulus. Investors want clarity, and without it, they often seek safety in other markets. Japan’s government now faces the challenge of rebuilding political unity while restoring investor trust. Until that happens, the Yen’s vulnerability may continue.

Global Risk Appetite and Market Mood Shift

Another key factor behind the Yen’s decline is the changing global risk sentiment. Recently, markets have seen a renewed sense of optimism after former U.S. President Donald Trump attempted to cool tensions with China over trade issues. His comments suggesting that both countries wish to avoid economic harm triggered a “risk-on” mood across markets, pushing investors back toward riskier assets such as equities and away from traditional safe havens like the Yen.

Earlier, tensions between the U.S. and China had sent waves of uncertainty through global markets. Trump’s threat of additional tariffs and China’s response hinted at a potential escalation in the trade dispute. However, when both sides signaled a willingness to cooperate, investor fear eased, leading to a sell-off in the Yen. This is a classic example of how quickly global sentiment can shift and influence currency values.

The Safe-Haven Paradox

The Yen has long been considered a go-to safe-haven currency during times of market turbulence. But when the overall sentiment turns positive, investors tend to unwind their Yen holdings in favor of assets with better returns. As a result, whenever optimism resurfaces in global markets, the Japanese Yen often finds itself under pressure.

Interestingly, while the Yen is losing ground, there remains an underlying caution among investors. Speculation that Japanese authorities could step in to curb excessive Yen weakness keeps traders from betting too heavily against the currency. Yet, the overall market tone continues to favor risk-taking, which limits the Yen’s ability to recover meaningfully in the short term.

Central Bank Divergence: BoJ and Fed Move in Opposite Directions

Perhaps the most influential factor shaping the Yen’s recent performance lies in the contrasting monetary policies of the Bank of Japan (BoJ) and the U.S. Federal Reserve (Fed). The two central banks appear to be heading in opposite directions, creating a policy gap that has a direct impact on currency flows.

While the BoJ is taking a cautious approach to raising interest rates, the Federal Reserve is widely expected to start cutting borrowing costs soon. This divergence makes the U.S. Dollar more appealing compared to the Yen, especially for investors seeking yield. The result is a steady flow of capital into U.S. assets, further weakening the Japanese currency.

Why the BoJ Is Holding Back

The Bank of Japan faces a delicate balancing act. On one hand, it wants to move away from ultra-loose monetary policies that have persisted for years. On the other hand, Japan’s economy is still fragile, and policymakers are wary of tightening too quickly. Domestic political uncertainty adds yet another layer of hesitation, making it harder for the BoJ to make bold moves.

This hesitation contrasts sharply with global trends. Other central banks have already acted aggressively to fight inflation or support growth, while Japan remains cautious. As a result, traders see limited incentive to buy the Yen, especially when other currencies offer better returns.

Fed’s Expected Rate Cuts Offer Only Temporary Relief

While the Federal Reserve is expected to cut interest rates further this year, it hasn’t yet translated into a strong rebound for the Yen. The reason is that even with rate cuts, U.S. yields remain relatively high compared to Japan’s. Moreover, the ongoing U.S. government shutdown has added uncertainty, keeping the Dollar’s movement unpredictable but still strong enough to overshadow the Yen.

The U.S. government’s budget freeze, which has already led to federal employee layoffs, reflects deeper political and economic concerns. Normally, such events might support safe-haven currencies like the Yen, but because Japan faces its own political and monetary challenges, the benefit has been limited.

Market Sentiment and Intervention Speculation

Even as the Yen struggles, the market remains alert to the possibility of Japanese government intervention. Historically, Japanese authorities have stepped in to stabilize the currency when its decline became too rapid or damaging for the economy. While there’s no confirmation of any imminent action, speculation alone can influence trading behavior.

Traders are now more cautious about taking large short positions against the Yen. This hesitancy has prevented a steeper decline, but it hasn’t been enough to trigger a meaningful recovery either. The result is a market caught between fear of intervention and the reality of a stronger global appetite for risk.

How Intervention Rumors Shape the Market

When investors suspect that the government might intervene, it introduces an element of unpredictability. Short sellers, who profit from the Yen’s fall, often reduce their exposure to avoid losses in case of a sudden policy move. This dynamic can create short-lived stability in the currency, even if the broader trend remains bearish.

What Lies Ahead for the Japanese Yen

Looking ahead, the Yen’s direction will likely depend on how Japan handles its internal political issues and how global risk sentiment evolves. If the government manages to restore confidence and the BoJ signals a clearer policy path, the Yen could regain some strength. However, as long as uncertainty lingers and the policy gap with the U.S. persists, the downward pressure is likely to continue.

The interplay between domestic politics, central bank actions, and global market moods will remain crucial. For now, the Yen’s safe-haven appeal appears diminished, replaced by cautious optimism among investors seeking higher returns elsewhere.

Final Summary

The Japanese Yen finds itself in a challenging position — pulled down by domestic political instability, overshadowed by a more attractive U.S. Dollar, and affected by shifting global sentiment. The end of a long political alliance, the uncertainty over Japan’s next leader, and the cautious stance of the Bank of Japan have combined to make the Yen vulnerable.

At the same time, a global return to risk-taking, triggered by easing trade tensions between the U.S. and China, has reduced the Yen’s safe-haven demand. While speculation of government intervention offers some temporary support, it is unlikely to change the broader trend.

Unless Japan can stabilize its political environment and present a more confident economic strategy, the Yen may continue facing headwinds. In a world where investors chase higher yields and clarity, the Japanese currency’s path forward will depend on how swiftly both its leaders and policymakers can restore balance and confidence.