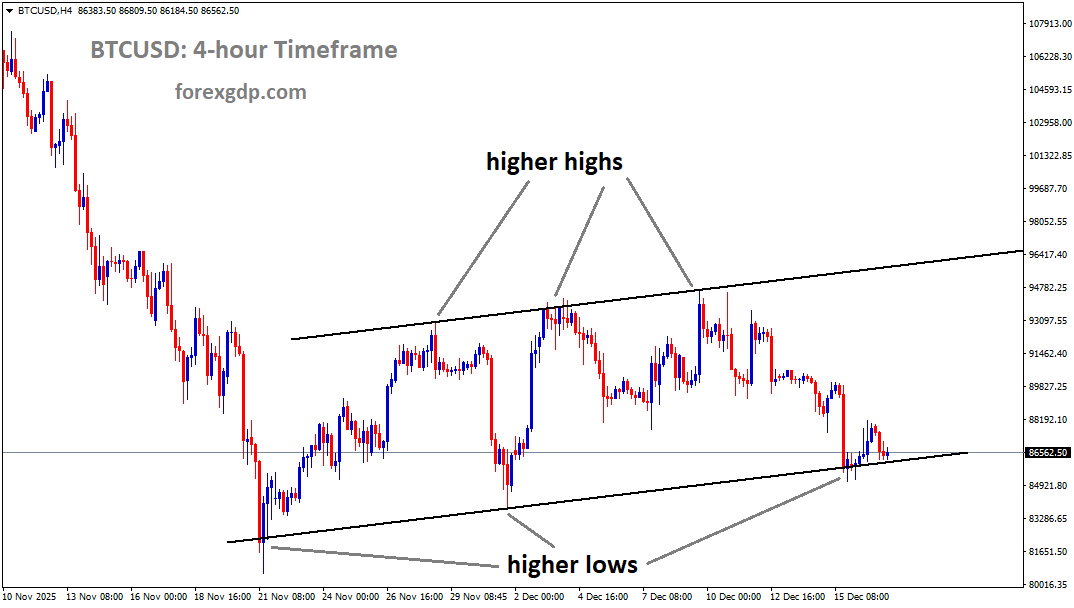

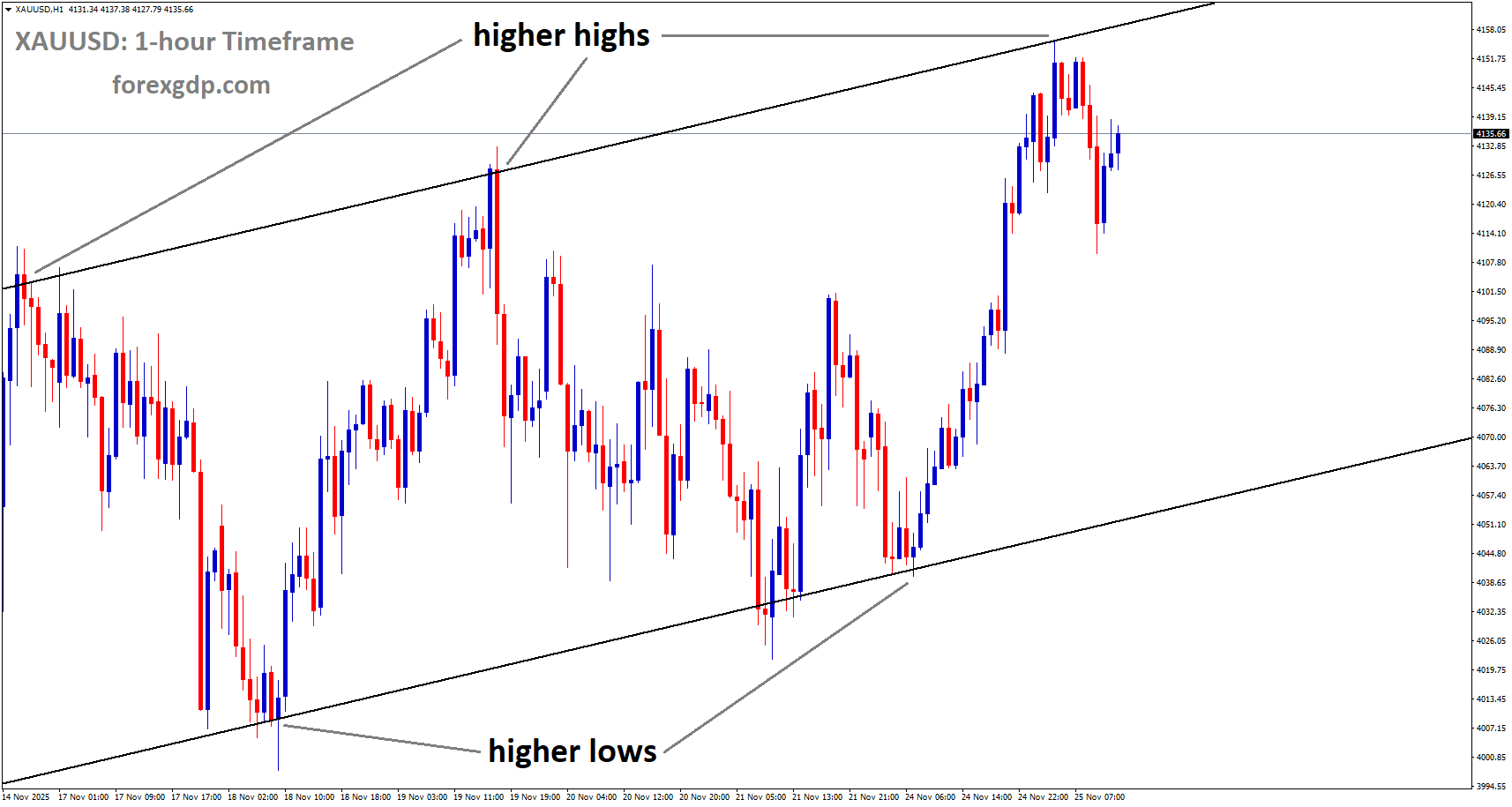

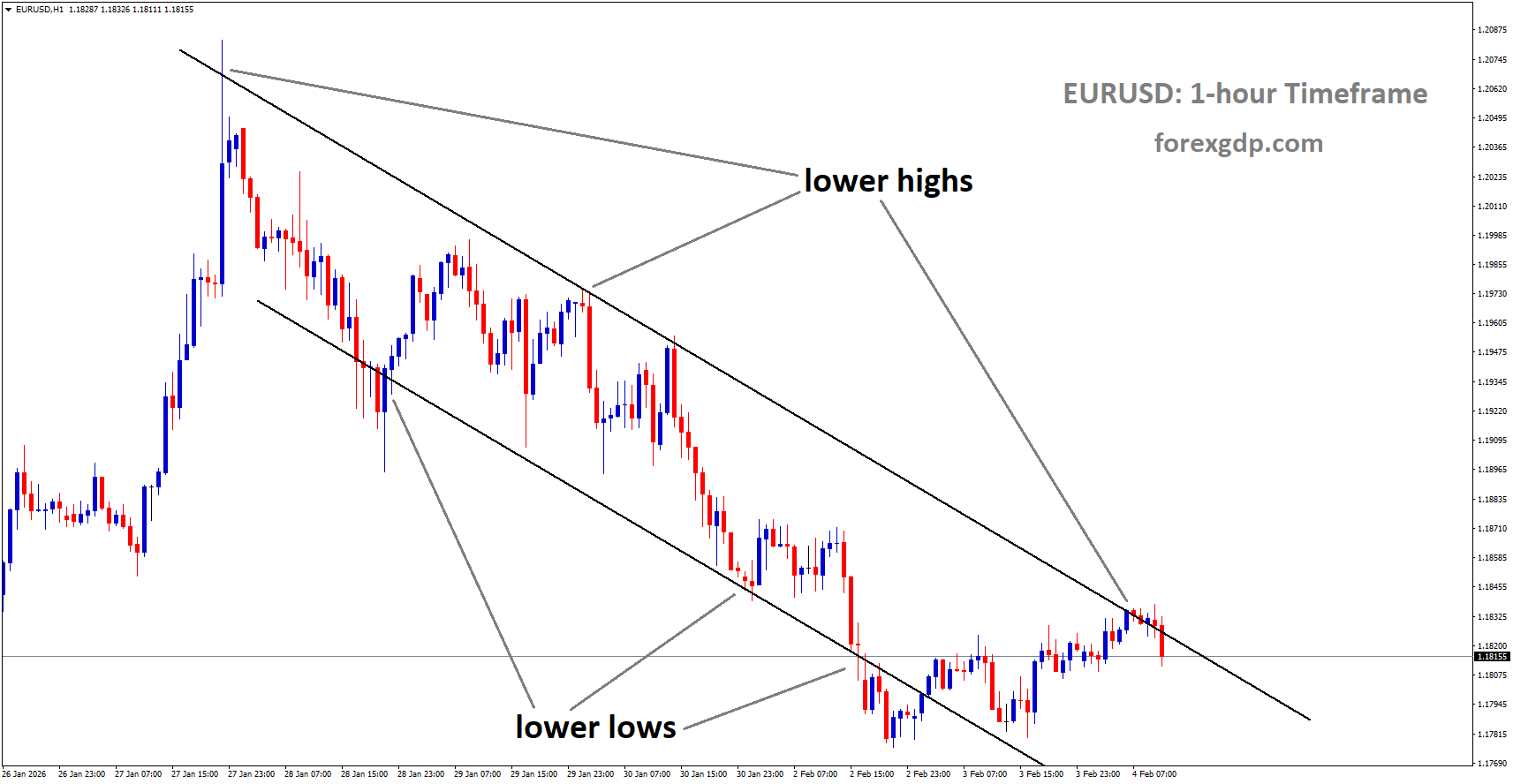

EURUSD is moving in a descending channel, and the market has reached the lower high area of the pattern

EURUSD loses steam following fresh signals of slowing inflation in Europe

The Euro lost some momentum during the latest trading session, slipping back after earlier gains and ending the day slightly weaker against the US Dollar. This move came as fresh economic data from the Eurozone confirmed that inflation pressures are easing and that growth in the services sector is slowing. Together, these signals have made investors more cautious about the region’s short-term outlook.

At the same time, the US Dollar held firm, supported by political developments in Washington and growing confidence around future leadership at the Federal Reserve. With important US employment data still ahead, many market participants are choosing to stay on the sidelines and wait for clearer direction.

Cooling Inflation Changes the Mood in the Eurozone

New data from Eurostat showed that inflation in the Eurozone slowed further in January, reaching its lowest level in well over a year. This confirmed earlier estimates and reinforced the idea that price pressures across the region are losing strength. For households, this may offer some relief, but for the Euro, it has created fresh headwinds.

Lower inflation often reduces the urgency for central banks to keep interest rates high. As a result, investors may start to question how long the European Central Bank will maintain its current policy stance. When inflation eases faster than expected, it can limit a currency’s appeal, especially when compared with economies where price growth remains more resilient.

Core Inflation Holds Steady

While headline inflation slowed, core inflation remained unchanged. Core figures strip out more volatile items and are closely watched by policymakers. The fact that core inflation did not fall suggests that underlying price pressures have not completely disappeared.

This steady core reading likely helped prevent a sharper drop in the Euro. It signals that, despite softer headline numbers, the ECB still has reasons to remain cautious before making any major policy shifts. Even so, the broader slowdown in inflation growth has been enough to weigh on sentiment.

Producer Prices Offer Mixed Signals

Producer price data added another layer to the picture. Prices at the factory gate continued to fall on a yearly basis, reflecting weaker demand and easing cost pressures across supply chains. However, the decline was not as deep as some had feared.

This slightly better-than-expected outcome may have offered limited support to the Euro, suggesting that the industrial side of the economy is not deteriorating as fast as worst-case scenarios had suggested. Still, falling producer prices often point to subdued economic momentum, which can eventually filter through to consumer prices and wages.

Services Sector Shows Signs of Fatigue

Beyond inflation, activity in the services sector also raised concerns. Revised survey data showed that growth in services slowed to its weakest pace in several months. While the sector is still expanding, the loss of momentum is notable, especially given the importance of services to the Eurozone economy.

Services include areas such as hospitality, transport, and professional services, all of which are closely tied to consumer confidence and spending. Slower growth here suggests that households and businesses may be becoming more cautious.

Germany Remains a Key Weak Spot

Germany, the Eurozone’s largest economy, also saw its services activity revised lower. This confirms that growth remains sluggish in a country that often sets the tone for the wider region. Persistent weakness in Germany tends to have an outsized impact on overall Eurozone performance.

For investors, this reinforces concerns that the Eurozone’s recovery remains uneven and fragile. When the bloc’s strongest economy struggles to gain traction, confidence in the broader outlook can quickly fade.

US Developments Support the Dollar

While the Euro faced pressure from softer data, the US Dollar benefited from a more stable backdrop. In Washington, President Donald Trump signed legislation that ended a brief government shutdown. The move eased political uncertainty and helped calm markets that had been unsettled by the disruption.

In addition, investors continued to react positively to the selection of Kevin Warsh as the next Chair of the Federal Reserve. Warsh is widely seen as a cautious and experienced policymaker who values the independence of the central bank. His reputation has reassured markets that monetary policy is likely to remain measured rather than reactive.

This combination of political clarity and confidence in future Fed leadership has helped underpin the Dollar, even as traders await fresh economic data.

Cautious Investors Look Ahead to US Jobs Data

Despite these developments, overall market sentiment remains careful. Investors are closely watching upcoming US employment figures, particularly the private payrolls report. This data has taken on added importance because the more closely followed government employment report has been delayed following the recent shutdown.

Employment data plays a central role in shaping expectations for US economic growth and monetary policy. Strong job creation would support the view that the US economy remains resilient, potentially strengthening the Dollar further. Weaker numbers, on the other hand, could revive speculation about future rate cuts.

Until these figures are released, many investors prefer to limit risk, contributing to relatively subdued trading conditions.

What This Means for the Euro Going Forward

The recent pullback in the Euro reflects a combination of softer inflation, slowing services activity, and cautious investor sentiment. While none of the data points point to an immediate downturn, together they suggest that the Eurozone economy is losing some momentum at a time when global growth remains uncertain.

At the same time, steady core inflation and less severe declines in producer prices indicate that the situation is not uniformly negative. These mixed signals leave the ECB with a delicate balancing act and investors with few clear answers.

In contrast, the US currently enjoys a more supportive backdrop, with political tensions easing and confidence in future monetary leadership strengthening. This divergence in outlook has tilted sentiment in favor of the Dollar, at least for now.

Final Summary

The Euro has come under modest pressure as fresh data confirmed easing inflation and slower growth in the services sector across the Eurozone. While core inflation remains stable and producer prices offered some reassurance, overall momentum appears to be fading, particularly in Germany. Meanwhile, the US Dollar has found support from political clarity and confidence in future Federal Reserve leadership. With key US employment data still ahead, investors remain cautious, waiting for clearer signals before committing to stronger positions.

GBPUSD Strengthens Before Major US Job Growth and Services Activity Reports

The Pound Sterling is attracting renewed attention from global investors as the Bank of England prepares for its first policy meeting of the year. Expectations that interest rates will remain unchanged have helped the British currency strengthen against several of its major counterparts. At the same time, traders are closely watching important economic data from the United States that could shape the next moves by the Federal Reserve.

GBPUSD is rebounding from the retest area of the broken downtrend channel

This mix of central bank decisions, economic forecasts, and employment data is creating an active environment in currency markets. While uncertainty remains, the overall tone suggests cautious optimism around the Pound as investors wait for clearer signals from policymakers on both sides of the Atlantic.

Bank of England Policy Decision Takes Center Stage

The Bank of England’s upcoming monetary policy announcement is the main focus for markets this week. Investors widely expect the central bank to keep interest rates steady following a rate cut delivered late last year. That earlier move was seen as a measured step in response to easing inflation pressures and slower economic momentum.

Holding rates steady now would signal that policymakers are comfortable with the current direction of the economy. It would also reinforce the Bank’s message that any further easing will happen gradually rather than through rapid changes. This approach aims to balance the need to support growth while ensuring inflation continues to move toward its long-term target.

For the Pound, this steady policy outlook has been supportive. Currencies often benefit from predictability, and the expectation that borrowing costs will not change immediately has reduced uncertainty for investors holding UK assets.

Differing Views Within the Monetary Policy Committee

While the broader expectation is for rates to remain unchanged, not all members of the Bank of England’s Monetary Policy Committee share the same outlook. A small number of policymakers are believed to favor another modest rate cut, reflecting their confidence that inflation is under control.

These differing views highlight the ongoing debate within the central bank. Some officials believe inflation is easing faster than previously thought and that borrowing costs could return to a more neutral level sooner. Others prefer a more cautious stance, emphasizing the need to see sustained progress before making additional changes.

One policymaker recently suggested that inflation could reach the Bank’s target earlier than many forecasts currently assume. This view supports the idea that interest rates may eventually move lower, but only after policymakers are confident that price stability is firmly in place.

Despite these internal differences, markets generally expect the majority of committee members to support holding rates steady for now. This consensus outlook has helped stabilize expectations and provided a modest boost to the Pound.

Inflation Outlook and the Importance of the Policy Report

Alongside the interest rate decision, investors are paying close attention to the Bank of England’s quarterly Monetary Policy Report. This document offers detailed insight into how policymakers view inflation, economic growth, and risks over the coming years.

The report’s inflation projections will be especially important. Previous guidance suggested that inflation could move closer to the central bank’s target within the next year or so. If the latest forecasts confirm this view, it would reinforce confidence in the Bank’s current policy stance.

Economic growth assessments will also matter. The report typically outlines how household spending, business investment, and global conditions are shaping the UK economy. Any changes in tone, whether more optimistic or more cautious, could influence market sentiment around the Pound.

Investors often read between the lines of this report to gauge how close the Bank may be to future policy changes. Even without an immediate rate move, subtle shifts in language can have a meaningful impact on expectations.

US Economic Data Adds to Market Tension

While the Bank of England dominates attention in the UK, events in the United States are also playing a key role in shaping global market sentiment. Investors are awaiting fresh data on private-sector employment and activity in the services industry.

Private employment figures offer an early look at labor market conditions and can influence expectations for official job reports later in the week. Strong hiring would suggest that the US economy remains resilient, while weaker numbers could point to cooling momentum.

The services sector data is equally important, as services account for a large share of economic activity. A reading that shows continued expansion would support the view that the economy is growing at a steady pace, even if growth is moderating.

These data points matter because they influence how investors view the Federal Reserve’s next steps. Signs of strength could reduce expectations for near-term rate cuts, while softer data would support the case for easing policy sooner.

Federal Reserve Expectations and Broader Implications

Market participants currently expect the Federal Reserve to begin lowering interest rates later in the year, assuming inflation continues to ease and economic growth remains balanced. Until then, policymakers are likely to keep rates unchanged as they assess incoming data.

This outlook has important implications for currency markets. When expectations for US rate cuts are pushed further into the future, the US Dollar often finds support. On the other hand, growing confidence in upcoming cuts can weaken the currency as investors look for higher returns elsewhere.

The interplay between Federal Reserve expectations and Bank of England policy is a key driver for movements in the Pound against the Dollar. As long as the BoE maintains a steady and predictable approach, shifts in US data could play a larger role in short-term currency moves.

Political Developments in the United States

Adding another layer to the market backdrop, recent political developments in the United States have helped ease some uncertainty. Lawmakers have approved funding measures that bring an end to a partial government shutdown, reducing the risk of immediate disruptions to federal operations.

However, not all challenges have been resolved. Some economic data releases are still facing delays, creating gaps in the information investors typically rely on. This lack of clarity can add to short-term volatility, especially when markets are already sensitive to policy signals.

Despite these issues, the resolution of the funding situation has removed one potential source of stress, allowing investors to refocus on economic fundamentals and central bank decisions.

What Investors Are Watching Next

As the week unfolds, attention will remain firmly on central banks and economic data. The Bank of England’s messaging will be closely analyzed for clues about the timing and pace of any future rate changes. In the United States, labor market and services sector data will help shape expectations for Federal Reserve policy.

For the Pound, a steady policy outlook combined with improving inflation trends could continue to provide support. However, shifts in global sentiment or surprises in economic data could quickly change the picture.

Investors are likely to remain cautious, balancing optimism about easing inflation with awareness of ongoing risks to growth and stability. In this environment, clear communication from policymakers will be crucial in guiding market expectations.

Final Summary

The Pound Sterling has found support as investors anticipate a steady interest rate decision from the Bank of England and look ahead to important economic data from the United States. Expectations of gradual policy easing, rather than abrupt changes, have helped reduce uncertainty around the UK outlook. At the same time, US employment and services data are shaping views on when the Federal Reserve might begin cutting rates. Together, these factors are creating a careful but engaged market environment, where every new signal from policymakers and data releases carries added importance.

USDJPY Pushes Higher While Japan’s Election Uncertainty Hits the Yen

The Japanese Yen has come under heavy pressure, turning into the weakest major currency among developed economies this week. Global investors are steadily moving away from the Yen as political uncertainty builds in Japan and concerns grow around the country’s fiscal direction. This shift in sentiment has pushed demand toward the US Dollar, even though the Greenback itself is not showing exceptional strength.

USDJPY is moving in an ascending channel, and the market has rebounded from the higher low area of the channel

At the center of this move is growing unease ahead of Japan’s upcoming snap elections. Currency markets tend to react quickly when political outcomes may reshape government spending or tax policy, and that is exactly what traders are doing now. The result has been broad-based selling of the Yen, not just against the Dollar but across several major currency pairs.

Why Japan’s Elections Are Weighing on the Yen

Japan’s political landscape has become a key driver of recent currency moves. Prime Minister Sanae Takaichi’s rising popularity has sparked debate about the future direction of fiscal policy. Many investors believe that a strong election result could give her the mandate to expand existing tax cuts and push forward with large-scale stimulus programs.

While such measures may support short-term economic activity, markets are focused on the long-term risks. Increased government spending without clear funding plans raises fears of widening deficits and mounting public debt. For currency traders, this combination often signals trouble.

As election day approaches, investors are choosing caution. Rather than waiting for clarity, many are reducing exposure to the Yen now. This preemptive selling reflects a lack of confidence in Japan’s fiscal outlook and a belief that political momentum could translate into policies that further weaken the currency.

Markets Shrug Off Intervention Warnings

Japanese officials have not stayed silent during the Yen’s slide. Authorities in Tokyo have issued repeated warnings about excessive currency volatility and have hinted that intervention remains an option if market moves become disorderly. In the past, such statements were often enough to slow or reverse Yen losses.

This time, the impact has been limited.

One reason is the tone coming from Japan’s leadership. Prime Minister Takaichi has openly highlighted the advantages of a weaker Yen, particularly for exporters and corporate profits. These remarks have undercut the credibility of intervention threats, leading traders to believe that authorities may tolerate further weakness.

Adding to this view, the US Treasury Secretary recently dismissed the idea of any coordinated effort between the United States and Japan to stabilize the Yen. Without international backing, any unilateral intervention by Japan is seen as less effective. Together, these factors have encouraged markets to continue selling the Yen despite official warnings.

The US Dollar Holds Steady, Not Strong

While the Yen has been under clear pressure, the US Dollar’s role in this move is more subtle. The Dollar has remained relatively stable rather than aggressively strong. Recent support came from positive political and institutional developments in the United States, including renewed optimism following the nomination of Kevin Warsh as the next Federal Reserve Chair.

The resolution of a brief partial government shutdown has also helped calm nerves. Political disruptions often weigh on currencies, and the return to normal government operations removed a short-term risk factor for the Dollar.

Still, the Dollar’s recent gains appear to be losing momentum. Investors are no longer chasing it higher and are instead waiting for fresh economic signals. This suggests that the recent currency move is driven more by Yen weakness than by broad Dollar strength.

Key US Data in Focus for Traders

Attention is now turning toward upcoming US economic reports, which could influence short-term currency direction. Of particular interest is data on services sector activity, an important indicator of overall economic health in the United States. Since services make up a large portion of the economy, any surprise in this report could shift market expectations.

Another closely watched release is the private-sector employment report from ADP. Traders are paying extra attention to this data because delays related to the government shutdown have pushed back the official jobs report. In the absence of that benchmark, ADP figures are being treated as a key clue about labor market conditions.

Expectations point to modest improvement in hiring, which would support the idea that the US economy remains resilient. If confirmed, this could provide the Dollar with a short-term boost, especially against currencies already under pressure like the Yen.

Investor Psychology and the Yen’s Broader Outlook

Beyond immediate political and economic events, the Yen’s weakness reflects a deeper shift in investor psychology. For years, the Japanese currency was viewed as a safe haven during periods of global uncertainty. Recently, that reputation has faded.

Ultra-loose monetary policy, persistent inflation challenges, and now fiscal concerns have changed how investors see Japan. Instead of acting as a shelter, the Yen is increasingly treated as a funding currency, borrowed to invest elsewhere. This dynamic makes it more vulnerable when confidence slips.

Unless there is a clear change in policy direction or a strong signal of coordinated support, the Yen may continue to face headwinds. Markets are watching closely to see whether election results bring reassurance or deepen concerns.

Final Summary

The Japanese Yen has weakened sharply as investors react to rising political uncertainty ahead of Japan’s snap elections. Fears that expanded stimulus and tax cuts could strain public finances have driven widespread selling of the currency. Warnings from Japanese officials about possible intervention have had little effect, especially as government leaders continue to emphasize the benefits of a softer Yen and international coordination appears unlikely.

Meanwhile, the US Dollar remains steady rather than dominant, supported by political stability and cautious optimism around upcoming economic data. With key US services and employment reports on the horizon, traders are positioning carefully. For now, the currency market story is less about Dollar strength and more about the growing doubts surrounding Japan’s fiscal and political outlook.

USDCAD Steadies as Traders Await Fresh Signals from US Hiring Data

The US Dollar is showing mild strength against the Canadian Dollar as traders take a cautious approach midweek. Movement has been limited, with buyers stepping in after a recent pullback, while sellers appear unwilling to push too hard ahead of important economic updates. This quiet tone reflects a broader sense of patience across currency markets, where fresh direction is expected to come from labor data and central bank signals rather than short-term speculation.

USDCAD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

Investors are largely staying on the sidelines, waiting for confirmation about the health of the US job market and clues about where monetary policy is heading next. At the same time, developments in Canada are adding another layer of uncertainty, keeping the USD/CAD pair in a narrow and controlled range.

Why the US Dollar Is Finding Support

The US Dollar has managed to post small gains, even as overall trading activity remains subdued. One reason is the market’s focus on upcoming employment data, which often plays a central role in shaping expectations for interest rate policy.

This week, attention is firmly on the private-sector employment report from ADP. Normally, this data would be one of several indicators feeding into expectations ahead of the official government jobs report. However, the current situation is different, as the release of the widely watched Nonfarm Payrolls data has been pushed back due to a partial government shutdown. That delay has elevated the importance of alternative labor market indicators, including the ADP report.

Traders see this data as a key piece of the puzzle in understanding whether the US labor market is stabilizing or continuing to cool after years of strong growth. With fewer official signals available in the near term, even secondary reports are carrying more weight than usual.

The Labor Market Picture in the United States

What the ADP Employment Report Tells Us

The ADP Employment Change report focuses on private-sector hiring and often provides an early snapshot of employment trends. Expectations point to modest job growth for January, with hiring continuing but at a slower pace than in previous years.

This slower rate of job creation fits with the broader story seen throughout 2025 so far. After a very strong performance in 2024, the US labor market appears to be losing momentum. Monthly job gains are well below last year’s average, suggesting that businesses are becoming more cautious as borrowing costs remain elevated and economic growth cools.

While these numbers may look weak compared to recent history, they are not necessarily alarming. Many policymakers see a slower labor market as a natural and even healthy adjustment after an extended period of tight conditions.

How This Affects the Federal Reserve

The current employment trend supports the Federal Reserve’s cautious approach to monetary easing. Officials have made it clear that they want to see sustained evidence of cooling inflation and balanced labor conditions before making aggressive policy moves.

Gradual easing remains the preferred path, and steady but slower job growth aligns with that goal. For the US Dollar, this environment can still be supportive. A controlled slowdown reduces fears of a sharp economic downturn, while also keeping interest rates relatively attractive compared to other major economies.

Recent political developments have also helped stabilize sentiment. The end of a short government shutdown removed a source of uncertainty, and optimism surrounding the nomination of Kevin Warsh as the next Federal Reserve chair has added to the sense of continuity in US monetary policy.

Canada’s Economic Signals Are Mixed

On the Canadian side, recent data has painted a more complex picture. Manufacturing activity showed a notable improvement, with factory output expanding at its fastest pace in over a year. This was a welcome surprise and suggested that parts of the Canadian economy are finding their footing after a challenging period.

That positive signal helped offset disappointment from earlier Gross Domestic Product data, which pointed to weak monthly growth. Together, these reports suggest that Canada’s economy is neither accelerating strongly nor falling into serious trouble, but rather moving unevenly across different sectors.

For the Canadian Dollar, this mixed backdrop makes it harder to establish a clear direction. Strength in manufacturing offers hope, but softer overall growth keeps expectations in check.

All Eyes on the Bank of Canada and Jobs Data

Governor Macklem’s Speech Matters

Later this week, markets will closely follow remarks from Bank of Canada Governor Tiff Macklem. His comments are expected to provide insight into how policymakers are interpreting recent economic data and whether they see room for changes in monetary policy.

Traders will listen carefully for any hints about the balance between supporting growth and controlling inflation. Even subtle shifts in tone can influence expectations and, by extension, the Canadian Dollar’s performance.

Canadian Employment Figures Could Set the Tone

Alongside central bank communication, Canada’s employment data is scheduled for release toward the end of the week. This report will be critical in shaping near-term expectations for the Canadian economy.

Strong job numbers could reinforce confidence that the economy is holding up better than feared, potentially lending support to the Loonie. On the other hand, signs of weakness in hiring or rising unemployment would raise concerns about growth and could weigh on the currency.

Given the importance of labor market data on both sides of the border, it is no surprise that USD/CAD traders are choosing caution for now.

Why Investors Are Staying Patient

The current environment encourages restraint. With major data releases clustered later in the week and some key reports delayed, there is little incentive to take bold positions. Instead, market participants are waiting for clearer signals that can justify stronger moves.

This wait-and-see approach reflects a broader theme in global markets. After years of rapid change driven by inflation shocks, aggressive rate hikes, and economic reopening, investors are now adjusting to a slower, more measured phase. Small shifts in data and policy guidance matter more because they help define the next chapter.

Final Summary

The US Dollar is holding modest gains against the Canadian Dollar as markets pause ahead of important employment data and central bank signals. In the United States, attention is focused on private-sector job growth, which is expected to confirm a slower but stable labor market. This trend supports the Federal Reserve’s gradual approach to policy easing and helps keep the Dollar supported.

In Canada, economic signals remain mixed, with stronger manufacturing activity offset by weaker overall growth. Upcoming remarks from Bank of Canada Governor Tiff Macklem and fresh employment data will play a key role in shaping expectations for the Canadian Dollar.

Until these events unfold, investors are choosing patience over prediction, leaving USD/CAD trading in a calm and controlled manner while waiting for clearer direction.

USDCHF Pauses Near Recent Levels Ahead of High-Impact US Releases

The USD/CHF currency pair is moving sideways as investors take a cautious pause. Market participants are holding back from big moves while waiting for important economic updates from the United States and fresh guidance from Swiss policymakers. This period of calm reflects a broader sense of uncertainty, with traders trying to understand where interest rates and inflation may head next.

USDCHF is moving in a descending channel, and the market has rebounded from the lower low area of the channel

At the heart of this quiet trading phase are two major themes. First is the outlook for the US economy, especially the strength of its job market and service sector. Second is Switzerland’s ongoing struggle with weak inflation, which continues to shape expectations around the Swiss National Bank’s policy direction.

A Quiet Market Ahead of Important US Data

The US Dollar and Swiss Franc are both seeing limited movement as investors look ahead to key economic releases. In particular, attention is focused on employment data from the US private sector and a closely watched survey of service industry activity.

Private employment figures are often used as an early signal of broader labor market trends. Strong hiring can suggest economic resilience, while softer numbers may raise concerns about slowing growth. Investors use this information to reassess expectations for future interest rate decisions by the Federal Reserve.

Alongside employment data, the services sector report plays an important role. The services industry makes up a large share of the US economy, covering areas such as healthcare, retail, transport, and finance. Even small changes in service activity can influence market sentiment, as they offer clues about consumer demand and business confidence.

With both reports due during the North American session, many traders prefer to wait rather than take strong positions. This explains why the USD/CHF pair is trading in a tight range, reflecting uncertainty rather than conviction.

What the Data Could Mean for Federal Reserve Policy

The Federal Reserve’s next steps remain a major focus for global markets. Investors are closely watching economic indicators to judge whether the central bank is likely to keep interest rates steady or consider changes later in the year.

Recent expectations suggest that US policymakers are comfortable maintaining current interest rate levels for now. Inflation has shown signs of easing, but it has not disappeared as a concern. At the same time, the labor market has remained relatively stable, giving the Fed room to be patient.

Employment growth, even at a moderate pace, supports the idea that the economy is not under immediate stress. Meanwhile, steady expansion in the services sector points to ongoing economic momentum, though at a slower speed than before. Together, these signals suggest a balanced picture rather than one that demands urgent action.

For currency markets, this kind of outlook often leads to consolidation. When traders believe policy is unlikely to change in the near term, they tend to wait for clearer signals before adjusting their positions.

The Swiss Franc and the SNB’s Inflation Challenge

On the Swiss side, the picture looks quite different. Switzerland has been dealing with low inflation for an extended period, and this continues to influence the Swiss National Bank’s approach.

Swiss policymakers have made it clear that price stability is their top priority. However, unlike some other major economies, Switzerland is not facing strong inflationary pressure. Instead, the challenge lies in preventing inflation from staying too low for too long, which can weigh on economic growth.

The SNB is widely expected to keep interest rates unchanged in the near future. This cautious stance reflects concern that tightening policy too early could further weaken inflation. As a result, the Swiss Franc has shown mixed performance, responding not only to domestic policy expectations but also to global risk sentiment.

When investors feel confident, the Swiss Franc often weakens as demand for safe-haven assets fades. During uncertain times, it tends to strengthen as traders seek stability. Right now, these opposing forces are largely canceling each other out, contributing to the current lack of direction in USD/CHF.

Comments from SNB Leadership Reinforce a Careful Approach

Recent remarks from Swiss National Bank leadership have reinforced the cautious tone. The focus remains firmly on inflation and ensuring long-term price stability. Policymakers have emphasized their readiness to act if needed, but they have also signaled that patience is necessary given the current economic environment.

These comments underline the SNB’s commitment to maintaining control over inflation without rushing into policy changes. For investors, this means fewer surprises in the short term, but ongoing sensitivity to any new data that could shift the inflation outlook.

As long as inflation remains subdued, expectations for stable Swiss policy are likely to persist. This stability, while reassuring, also limits the potential for sharp currency moves unless external factors come into play.

Global Factors Also Shape USD/CHF Sentiment

Beyond domestic data and central bank guidance, broader global trends continue to influence the USD/CHF pair. Geopolitical developments, shifts in global growth expectations, and changes in investor risk appetite all play a role.

The US Dollar often benefits from its status as a global reserve currency, especially during times of uncertainty. Meanwhile, the Swiss Franc is also seen as a safe haven, creating an interesting dynamic when global risks rise. In such cases, both currencies can attract demand, leading to muted movements between them.

This shared safe-haven status helps explain why USD/CHF can remain range-bound even during periods of global tension. Investors may prefer one over the other based on relative policy outlooks, but the differences are not always strong enough to drive major trends.

Why Patience Is Dominating the Market Right Now

The current environment rewards patience. With no immediate policy changes expected from either the Federal Reserve or the Swiss National Bank, traders are relying heavily on incoming data to guide their decisions.

Small surprises in employment figures or service sector activity could temporarily shift sentiment, but lasting trends are more likely to emerge only when there is a clearer change in economic direction. Until then, consolidation remains a natural outcome.

For longer-term observers, this phase offers insight into how markets balance competing signals. Moderate growth in the US contrasts with subdued inflation in Switzerland, creating a push-and-pull effect that keeps USD/CHF relatively stable.

Final Summary

USD/CHF is currently moving sideways as investors wait for important signals from both the United States and Switzerland. Upcoming US employment and service sector data are expected to offer fresh insight into the Federal Reserve’s policy outlook, while Switzerland continues to grapple with soft inflation.

The Federal Reserve appears comfortable holding interest rates steady for now, supported by a resilient labor market and moderate economic expansion. At the same time, the Swiss National Bank remains cautious, prioritizing price stability in an environment of weak inflation.

With both central banks signaling patience and global factors offering mixed cues, the USD/CHF pair reflects a market in waiting mode. Until clearer economic trends emerge, calm and consolidation are likely to remain the dominant themes.

EURGBP Under Pressure as Euro Struggles Against Confident Pound

The EUR/GBP currency pair has been under gentle pressure, reflecting a growing contrast between economic signals coming from the Eurozone and the United Kingdom. While Europe continues to send mixed messages about the strength of its recovery, the UK benefits from a clearer monetary policy outlook. This divergence has shaped sentiment around both currencies and explains why the Pound Sterling currently holds the upper hand against the Euro.

EURGBP is moving in a descending triangle, and the market has reached the lower high area of the pattern

Rather than being driven by sudden shocks, recent movements in the pair are rooted in fundamentals. Economic data, inflation trends, and central bank expectations are all playing a role. Understanding these factors helps explain why the Euro is struggling to gain momentum and why the Pound is finding steady support.

Mixed Eurozone Data Weighs on the Euro

Recent economic releases from the Eurozone paint a cautious picture. While some areas show signs of resilience, others point to slowing momentum, especially in the services sector. This uneven performance has limited confidence in the region’s short-term outlook and reduced the Euro’s appeal for investors.

Service sector activity is particularly important because it represents a large share of economic output across the Eurozone. A slowdown here often signals softer consumer demand and weaker business confidence. Recent figures suggest that growth in this area has lost some pace compared to previous months, reinforcing concerns about the durability of the recovery.

Germany, the largest economy in the Eurozone, continues to draw attention. Updated data from the country show that services activity remains subdued, even after revisions. This matters because Germany often sets the tone for the wider region. When its economy struggles to gain traction, it becomes harder for the Eurozone as a whole to show strong and consistent growth.

Taken together, these indicators suggest that the Eurozone economy is not moving in a clear upward direction. Instead, it appears to be advancing in fits and starts, making it difficult for the Euro to build sustained strength against its peers.

Inflation Trends and the ECB’s Steady Hand

Inflation remains a central topic for policymakers and markets alike. In the Eurozone, price pressures have continued to ease, following a trend that has been in place for several months. Headline inflation has slowed compared to late last year, while underlying inflation measures have shown little change.

A key factor behind this easing has been energy prices. As energy costs stabilize or fall, they naturally reduce overall inflation readings. However, this type of disinflation is generally seen as temporary and does not necessarily signal a broader cooling across the economy.

For the European Central Bank, this context is familiar. Policymakers have long expected inflation to moderate as earlier price shocks fade. As a result, the recent data are unlikely to prompt any immediate changes in policy. The ECB is widely expected to maintain its current stance, focusing on keeping financial conditions stable while monitoring economic developments closely.

This steady approach has its advantages, but it also limits excitement around the Euro. Without a clear signal of stronger growth or a shift in policy direction, investors have little reason to increase exposure to the single currency in the near term.

Pound Sterling Finds Support in Policy Expectations

On the other side of the equation, the Pound Sterling benefits from a more predictable policy outlook in the United Kingdom. Expectations around the Bank of England’s next move have been a key source of support for the currency.

After a rate cut late last year, markets broadly anticipate that the central bank will pause and keep its main policy rate unchanged at the upcoming meeting. This expectation of stability helps anchor investor confidence. When interest rate paths are clearer, currencies tend to trade with less uncertainty.

In addition to the decision itself, attention is firmly on the Bank of England’s guidance. Investors expect policymakers to emphasize a gradual approach to any future easing. Such messaging suggests that the central bank remains cautious about inflation risks and is not in a hurry to loosen conditions further.

This careful tone contrasts with the more fragile outlook in the Eurozone and helps explain why the Pound has remained relatively firm. Stability, even without aggressive tightening, can be attractive when compared to regions facing uneven growth.

UK Economic Activity Adds to Confidence

Beyond central bank expectations, recent UK economic data have also played a role in supporting the Pound. Activity in the services sector has shown notable improvement, reaching its strongest level in several months.

The services industry is a major driver of the UK economy, covering everything from retail and hospitality to finance and professional services. Stronger readings here suggest that businesses are seeing better demand and that consumers remain engaged despite ongoing cost pressures.

While revised figures came in slightly below initial estimates, the overall trend still points to a meaningful rebound compared to the previous month. This improvement offers reassurance that the UK economy is holding up better than some had feared, at least in the short term.

Such data do not eliminate longer-term challenges, but they do provide a cushion for the Pound. When combined with a steady central bank message, they create a more supportive environment for the currency.

How Diverging Outlooks Shape EUR/GBP

The current balance between the Euro and the Pound reflects a broader theme of diverging economic narratives. In the Eurozone, growth remains fragile and uneven, limiting enthusiasm for the Euro. In the UK, clearer policy expectations and improving activity data help underpin confidence in the Pound.

This does not mean the outlook is one-sided or fixed. Economic conditions can change, and both central banks remain data-dependent. However, for now, the contrast is clear enough to influence how the currency pair behaves.

Investors are paying close attention to upcoming central bank communications, particularly the details within policy statements and economic projections. These insights often shape expectations well beyond the immediate decision and can influence currency trends over weeks or months.

Final Summary

EUR/GBP reflects the shifting balance between two different economic stories. The Euro faces headwinds from mixed data and a fragile recovery, especially within the services sector and key economies like Germany. Inflation is easing, but largely for expected reasons, leaving the European Central Bank comfortable with a steady policy stance.

Meanwhile, the Pound Sterling draws support from a clearer outlook at the Bank of England and signs of renewed strength in UK services activity. Expectations of a policy pause and gradual future easing provide stability, while recent data suggest the economy is showing resilience.

As long as these contrasting dynamics remain in place, they are likely to continue shaping sentiment around the pair. For now, stability in the UK and uncertainty in the Eurozone define the underlying tone of EUR/GBP.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!