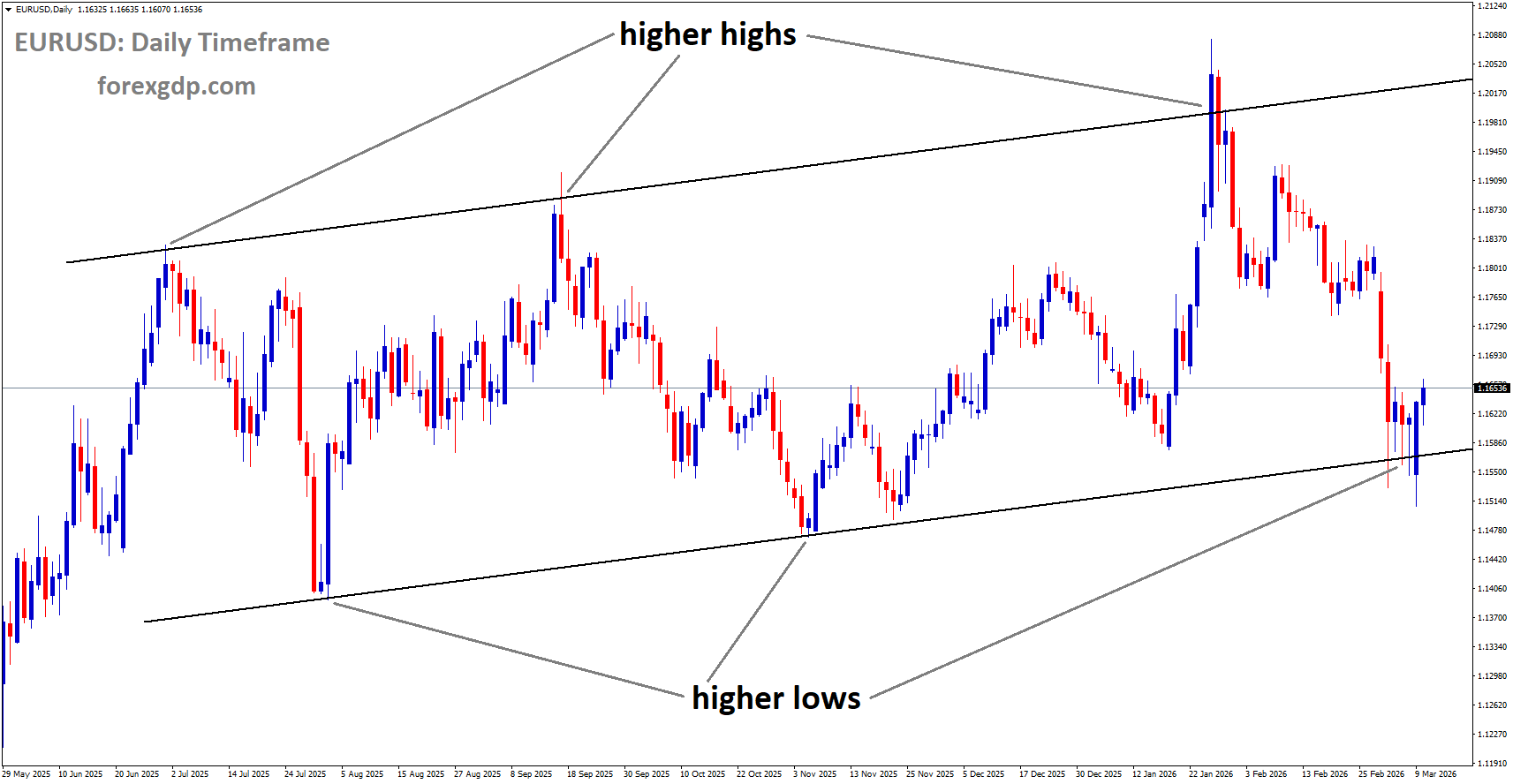

EURUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

EURUSD Weakens Near 1.1600 While Rising Middle East Tensions Support US Dollar

The EUR/USD currency pair moved slightly lower during the early European trading session on Tuesday, drifting toward the 1.1615 level. The decline comes as investors shift their attention to rising geopolitical tensions in the Middle East and upcoming US inflation data.

The US Dollar has gained strength as global uncertainty pushes investors toward safer assets. At the same time, markets are preparing for the release of the United States Consumer Price Index (CPI) data for February, which is expected to influence expectations around monetary policy in the months ahead.

Rising Middle East Tensions Strengthen the US Dollar

One of the main factors influencing currency markets recently is the ongoing conflict in the Middle East. The situation has raised fears about potential disruptions to global oil supplies, particularly through the Strait of Hormuz, a key shipping route for oil exports.

Iran’s Islamic Revolutionary Guard Corps (IRGC) stated that Tehran will decide when the conflict comes to an end rather than outside powers. The group also warned that continued attacks by the United States or Israel could lead Iran to block oil exports from the region.

These warnings have raised serious concerns among global investors. Any disruption in the Strait of Hormuz could significantly affect oil supply, which would have wide-reaching consequences for the global economy.

In response to the escalating tensions, US President Donald Trump said that any attempt by Iran to block the flow of oil through the Strait of Hormuz would trigger a strong response from the United States.

The uncertainty surrounding this situation has pushed many investors toward assets considered safe during times of instability. The US Dollar is often viewed as one of the most reliable safe-haven currencies because of its deep liquidity and the strength of the US financial system.

Why the US Dollar Acts as a Safe Haven

During periods of geopolitical uncertainty, investors often move their money into assets that are considered stable and dependable. The US Dollar frequently benefits from this trend.

Matthew Ryan, head of market strategy at financial services firm Ebury, noted that the dollar continues to attract demand due to its liquidity and the recent rise in oil prices. According to him, the currency could remain supported if the conflict continues without a quick resolution.

When global risks increase, investors typically reduce exposure to riskier assets and seek currencies backed by large, stable economies. The United States, with its large financial markets and global economic influence, often becomes a preferred destination for capital during uncertain times.

As a result, the strengthening of the dollar tends to create pressure on other major currencies, including the euro.

Oil Prices and Inflation Concerns Add Complexity

Another important factor affecting currency markets is the impact of rising oil prices on inflation.

Geopolitical tensions in oil-producing regions can lead to higher energy costs. When oil prices increase, the cost of transportation, manufacturing, and goods production often rises as well. This can push overall inflation higher across the economy.

For policymakers at the US Federal Reserve, this creates a complicated situation. The central bank aims to control inflation while supporting economic growth. If energy prices remain elevated, inflation could stay higher for longer than expected.

Because of this possibility, expectations for future interest rate cuts in the United States have been reduced. Investors are becoming more cautious about assuming that the Federal Reserve will move quickly to lower borrowing costs.

The shift in expectations has provided additional support to the US Dollar, as higher interest rates generally make a currency more attractive to investors.

Investors Await Key US Inflation Data

Market participants are now closely watching the upcoming release of the February Consumer Price Index data from the United States. This report is one of the most closely followed indicators of inflation and plays a major role in shaping expectations for monetary policy.

Economists expect the headline inflation rate to show a yearly increase of around 2.4 percent in February. Meanwhile, core inflation, which excludes volatile items such as food and energy, is expected to rise by about 2.5 percent compared to the same period last year.

These figures suggest that inflation may be stabilizing, but investors remain cautious because global risks could easily influence price pressures in the coming months.

If the inflation numbers come in higher than expected, it could reinforce the view that the Federal Reserve may need to keep interest rates elevated for longer. This outcome would likely support the US Dollar further.

On the other hand, if inflation turns out to be softer than predicted, it may revive expectations that the central bank could eventually ease monetary policy. In that case, the dollar could lose some of its recent strength.

Impact on the EUR/USD Pair

The euro has been facing pressure as the US Dollar strengthens amid global uncertainty. Since the EUR/USD pair measures the value of the euro relative to the dollar, a stronger dollar naturally leads to downward movement in the pair.

Investors are carefully balancing several factors at once. These include geopolitical developments in the Middle East, changes in oil prices, and the upcoming inflation data from the United States.

Any major shift in these factors could influence the direction of the currency pair in the short term. For example, a sudden easing of geopolitical tensions might reduce demand for safe-haven assets, which could weaken the dollar.

At the same time, unexpected inflation data could quickly change market expectations regarding the Federal Reserve’s policy decisions.

What Traders and Investors Are Watching Next

Currency markets are likely to remain sensitive to global news in the coming days. The combination of geopolitical uncertainty and important economic data releases can create rapid shifts in investor sentiment.

Several key developments are currently on the radar for market participants:

-

Updates related to the Middle East conflict and potential risks to oil supply routes

-

Changes in global oil prices and their impact on inflation

-

The release of the US Consumer Price Index data

-

Signals from the Federal Reserve regarding future monetary policy decisions

Each of these factors has the potential to influence the strength of the US Dollar and, by extension, the movement of the EUR/USD pair.

Final Summary

The EUR/USD currency pair moved slightly lower during Tuesday’s early European session as the US Dollar gained support from rising geopolitical tensions in the Middle East. Concerns about potential disruptions to oil shipments through the Strait of Hormuz have increased global uncertainty, encouraging investors to move toward safe-haven assets like the US Dollar.

At the same time, higher oil prices have complicated the outlook for inflation and monetary policy in the United States. With expectations for interest rate cuts becoming less certain, the dollar has received additional support.

All eyes are now on the upcoming US CPI inflation data for February. The results of this report could shape expectations for future Federal Reserve decisions and play a key role in determining the next move for the EUR/USD pair. Until more clarity emerges, global tensions and economic data will continue to guide the direction of currency markets.

GBPUSD Pushes Higher Past 1.3400 During Period of Market Uncertainty

The Pound Sterling started the week on a positive note, showing steady strength against the US Dollar. The GBP/USD currency pair moved higher on Monday, continuing a pattern of stability that has been visible over the past several trading sessions. While the gains were modest, the movement signals growing confidence among market participants as a series of important economic reports approach later in the week.

GBPUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Several major economic updates from both the United Kingdom and the United States are expected over the coming days. These reports could influence how traders and investors view inflation, economic growth, and future interest rate decisions. Because of this, the current week is shaping up to be particularly important for the direction of the Pound and the Dollar.

Pound Sterling Extends Its Positive Momentum

The British Pound managed to record a solid session on Monday, rising by roughly 0.3% against the US Dollar. During the early part of the trading day, the pair briefly dropped toward the 1.3280 area before recovering and moving higher again. By the end of the session, the pair was trading close to the 1.3450 level but did not fully break past it.

Over the past several sessions, the GBP/USD pair has been moving around a similar price region, suggesting that the market may be entering a period of consolidation. This simply means that the currency pair is taking time to stabilize after previous movements, as traders wait for new economic signals.

Even with this temporary pause, the Pound still appears to have some positive momentum. The pair’s ability to hold near the upper part of its recent range suggests that buyers remain interested, at least in the short term. This steady positioning could keep the Pound supported while markets prepare for the upcoming data releases.

Changing Expectations for Bank of England Interest Rates

One of the major factors supporting the Pound recently has been a shift in expectations surrounding interest rate decisions by the Bank of England. Only a short time ago, financial markets believed that the central bank might soon begin lowering borrowing costs.

However, that outlook has changed significantly.

Earlier expectations suggested there was a very high chance that the Bank of England would introduce a rate cut this month. Since geopolitical tensions increased around the Strait of Hormuz, those expectations have dropped sharply. Markets now estimate the likelihood of an immediate rate cut to be relatively low.

In addition, forecasts for the rest of the year have also changed. Current projections indicate that the Bank of England may deliver less than a single quarter-percentage-point reduction in interest rates during 2026.

Energy Costs and Inflation Concerns

A key reason behind these shifting expectations is the rise in global energy prices. When energy costs increase, they often push overall inflation higher because businesses and consumers end up paying more for transportation, heating, and production.

If inflation remains elevated, central banks may choose to keep interest rates higher for longer. Higher rates are often used as a tool to slow down price increases and keep inflation under control.

Because of this dynamic, investors are closely watching how energy markets and inflation indicators evolve in the coming months.

US Inflation Data Becomes the Week’s Main Event

While several economic reports are scheduled throughout the week, one of the most important will arrive from the United States. On Wednesday, the US government will release its latest Consumer Price Index report for February.

The Consumer Price Index, often called CPI, measures changes in the prices consumers pay for everyday goods and services. It is one of the most widely watched indicators of inflation.

Economists currently expect the monthly CPI reading to increase by around 0.3%. On a yearly basis, inflation is projected to come in near 2.4%.

These numbers will be closely examined because inflation trends strongly influence decisions by the US Federal Reserve. If inflation shows signs of rising faster than expected, policymakers may choose to maintain tighter monetary policy. On the other hand, slower inflation could support the case for potential rate adjustments later on.

The outcome of this report could therefore have a noticeable effect on the US Dollar and global financial markets.

Important UK Developments on Thursday

The United Kingdom will also release significant economic information later in the week. On Thursday, attention will turn to industrial production data for January.

Industrial production measures how much output factories, mines, and utilities generate within the economy. It provides insight into the health of the country’s manufacturing and energy sectors.

Strong production figures can signal growing economic activity, while weaker numbers may suggest slowing momentum.

Another important event scheduled for Thursday is a speech from Bank of England Governor Andrew Bailey. As the leader of the central bank, Bailey’s comments often provide clues about how policymakers view inflation, economic conditions, and potential interest rate decisions.

Investors and analysts will be listening closely to see whether Bailey offers any hints about the future direction of monetary policy.

A Busy Friday for Both Economies

The final trading day of the week will bring several major economic reports from both sides of the Atlantic.

In the United Kingdom, new data will reveal how the economy performed at the start of the year. January Gross Domestic Product figures are expected to show modest growth of around 0.2% compared with the previous month.

GDP represents the total value of goods and services produced within a country and is widely used as a measure of economic growth. Even small changes in GDP can influence investor sentiment and expectations about the broader economic outlook.

Manufacturing production numbers for January will also be released on the same day. Like industrial production, these figures provide a deeper look at activity within the manufacturing sector.

Key US Reports Arriving the Same Day

The United States will also publish several important indicators on Friday.

One of the most closely watched will be the core Personal Consumption Expenditures price index, often referred to as core PCE. This measure tracks inflation but excludes volatile categories such as food and energy. It is considered one of the Federal Reserve’s preferred gauges for monitoring inflation trends.

Economists expect the monthly core PCE reading to show a moderate increase, while the yearly figure may remain around the 3% level.

Additional US reports will include preliminary data on economic growth for the fourth quarter as well as the University of Michigan’s consumer sentiment index for March.

The consumer sentiment survey measures how optimistic or pessimistic households feel about the economy. When confidence is high, people tend to spend more, which can help support economic growth. Lower confidence, however, may signal caution among consumers.

Why This Week Matters for Currency Markets

With so many important reports scheduled within a short period of time, the current week could play a significant role in shaping expectations for both the British and American economies.

Inflation data from the United States, economic growth figures from the United Kingdom, and comments from central bank officials all have the potential to shift market sentiment.

Currency markets are particularly sensitive to these developments because exchange rates often reflect expectations about future interest rates, inflation, and economic performance.

As a result, traders and investors will be paying close attention to each release, looking for clues about where the global economy might be heading.

Summary

The Pound Sterling began the week with modest gains against the US Dollar, continuing a steady performance that has been building over recent sessions. While movement in the currency pair has been relatively calm, several major economic events scheduled for the coming days could influence its direction.

Shifting expectations about Bank of England interest rates have supported the Pound, especially as rising energy costs raise concerns about persistent inflation. At the same time, the United States will release key inflation data that may shape views on Federal Reserve policy.

Later in the week, additional reports covering economic growth, manufacturing activity, and consumer confidence will offer further insight into the health of both economies.

With multiple influential updates arriving within a few days, the global currency market is entering an important period that could define the near-term outlook for the Pound Sterling and the US Dollar.

USDJPY pushes upward as escalating conflict and energy costs challenge Japan’s currency

The Japanese Yen continues to face challenges in global currency markets, even as investors look for safer assets during times of uncertainty. Recent geopolitical tensions in the Middle East, combined with sharp movements in energy markets, are shaping investor sentiment and influencing currency performance.

USDJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

At the same time, traders and analysts are closely watching upcoming economic data from both Japan and the United States. Important indicators such as Japan’s revised economic growth figures and US inflation data could play a key role in determining the next direction for the Yen and the US Dollar.

Middle East Tensions Push Oil Prices Higher

Global energy markets reacted strongly after recent military strikes targeting Iranian facilities. Air attacks reportedly carried out by the United States and Israel have increased concerns about stability in the region, especially around key oil supply routes.

Following these developments, oil prices rose sharply. At one point, prices surged significantly during the trading session before easing slightly later in the day. The sudden spike highlighted how quickly geopolitical events can disrupt global markets.

Energy traders also reacted to reports suggesting that the Group of Seven (G7) nations and the International Energy Agency might consider releasing emergency oil reserves. Such a move could help stabilize supply and prevent prices from climbing further. The possibility of coordinated action helped reduce some of the earlier price surge, but uncertainty remains.

The Middle East conflict has now entered its tenth day, and the situation continues to influence global markets. One of the main concerns is the potential disruption of oil shipments through the Strait of Hormuz, one of the world’s most important energy transit routes. Any interruption in this narrow waterway could have major consequences for global energy supply.

Why Rising Oil Prices Hurt the Japanese Yen

Higher oil prices tend to create difficulties for Japan’s economy. Unlike many energy-producing countries, Japan relies heavily on imported energy to meet its needs. As one of the world’s largest energy importers, the country must purchase large amounts of oil and gas from abroad.

When energy prices increase, Japan’s import costs rise significantly. This can weaken the country’s trade balance, meaning that more money flows out of the country to pay for energy purchases. Over time, this situation can put pressure on the national currency.

For this reason, rising oil prices are generally viewed as negative for the Japanese Yen. The recent surge in energy costs has therefore contributed to the currency’s ongoing weakness.

Japan’s Prime Minister, Sanae Takaichi, addressed the issue on Monday, acknowledging that households are becoming increasingly concerned about higher gasoline prices. Rising fuel costs affect transportation, daily commuting, and overall living expenses for many families.

The government is reportedly considering possible measures to help reduce the impact on consumers. However, officials have also stated that it is still too early to determine how the ongoing conflict in the Middle East could ultimately affect Japan’s broader economic outlook.

Investors Await Japan’s Revised GDP Data

In addition to geopolitical developments, investors are also focusing on Japan’s upcoming economic data releases. One of the most important indicators scheduled for release is the revised Gross Domestic Product (GDP) report for the fourth quarter.

Economic growth figures are closely monitored because they provide insight into the overall health of the economy. Stronger growth can improve investor confidence and may provide support for a country’s currency.

Economists currently expect the revised data to show slightly stronger growth than the initial estimate. If the updated figures confirm better economic performance, it could offer some support to the Japanese Yen, which has been under pressure in recent weeks.

However, even positive domestic data may struggle to offset the global factors currently influencing the currency market. The combination of rising energy costs, geopolitical uncertainty, and shifting expectations around global interest rates continues to shape investor behavior.

The US Dollar Remains Firm

While the Japanese Yen faces pressure, the US Dollar has shown resilience. The Dollar often benefits during periods of global uncertainty because investors view it as a reliable and stable currency.

The US Dollar Index, which measures the strength of the currency against several major global currencies, has remained steady. This reflects ongoing demand for the Dollar as markets react to geopolitical tensions and economic developments.

Another important factor supporting the Dollar is the current outlook for US interest rates. Expectations that borrowing costs may remain elevated for longer have helped maintain demand for the currency.

Central bank policymakers in the United States continue to monitor inflation closely. Persistent price pressures have made officials cautious about lowering interest rates too quickly. The recent rise in energy costs adds another layer of complexity to the situation, as higher oil prices can contribute to inflation.

Mixed Signals from the US Economy

Despite the Dollar’s strength, the US economy is also showing some signs of strain. Recent labor market data revealed job losses and a rising unemployment rate, raising concerns about slowing economic momentum.

These developments have sparked discussions about the possibility of stagflation, a challenging economic environment where inflation remains high while economic growth weakens. This scenario can make policy decisions more difficult for central banks.

The Federal Reserve now faces a delicate balancing act. On one hand, inflation pressures may require interest rates to stay elevated. On the other hand, signs of economic weakness could call for a more supportive monetary policy.

How the central bank responds will depend heavily on upcoming economic data.

Upcoming US Inflation Data Could Be Crucial

One of the most closely watched reports this week is the US Consumer Price Index (CPI), which measures changes in the prices consumers pay for goods and services.

Inflation data plays a major role in shaping expectations about interest rate policy. If inflation remains high, policymakers may choose to keep borrowing costs elevated for a longer period. On the other hand, a noticeable slowdown in inflation could open the door for future rate reductions.

Currency traders are particularly focused on this data because it can influence the relative strength of the US Dollar against other major currencies, including the Japanese Yen.

A stronger inflation reading could reinforce the Dollar’s advantage, while weaker inflation might reduce some of the currency’s momentum.

Summary

The Japanese Yen continues to face pressure as global markets react to rising oil prices and ongoing geopolitical tensions in the Middle East. Japan’s heavy reliance on imported energy makes the country particularly vulnerable when oil prices increase, creating additional challenges for the national currency.

At the same time, investors are closely watching key economic indicators. Japan’s revised GDP data may offer insight into the country’s economic performance, while upcoming US inflation figures could significantly influence expectations around Federal Reserve policy.

With geopolitical risks, energy markets, and economic data all playing a role, currency markets are likely to remain sensitive to new developments in the days ahead. The interaction between global events and economic fundamentals will continue to shape the relationship between the Japanese Yen and the US Dollar.