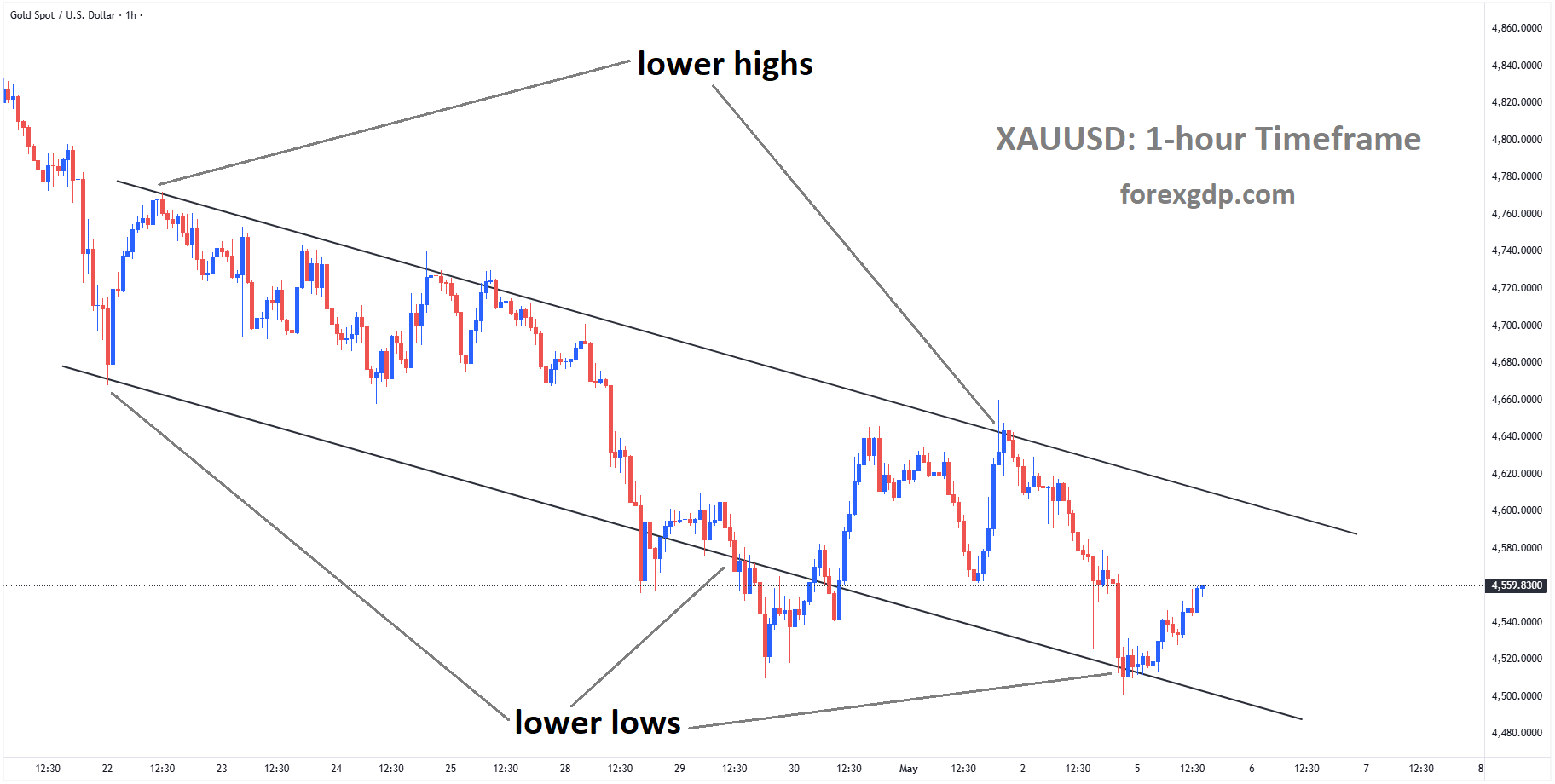

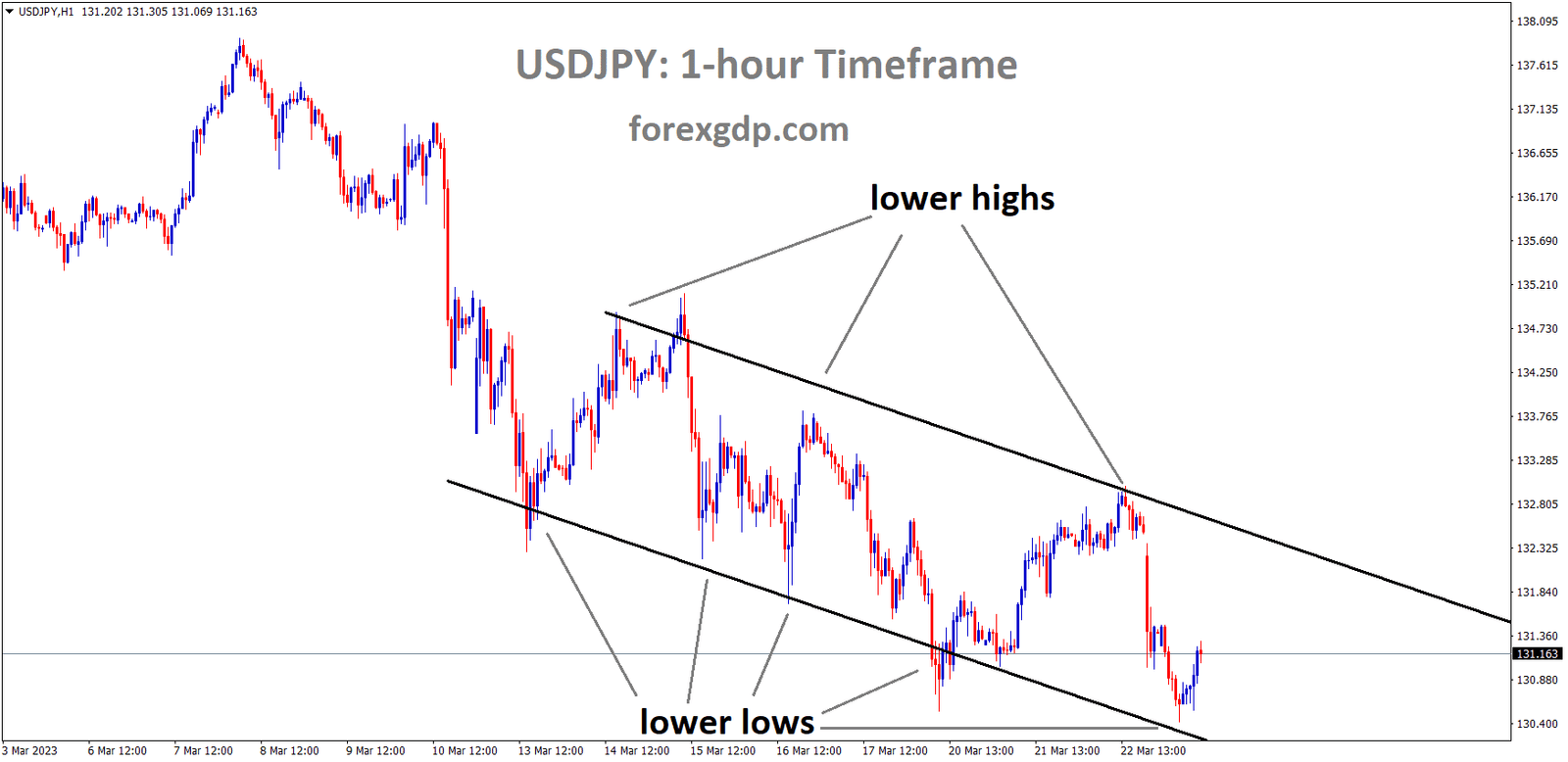

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

The sentiment indicator for major manufacturers in Reuter’s tankan survey is now at -3 from -5 the previous month, indicating pessimism among major manufacturers in Japan.

The findings point to sluggish global development and slower-than-expected Japanese exports in the near future.

The monetary policy of the Bank of Japan for the upcoming month demonstrates a lack of business trust in major manufacturers.

According to the closely watched Reuters Tankan survey, major Japanese manufacturers stayed pessimistic about business conditions for a third consecutive month in March. Concern over slowing global growth, which could harm the nation’s export-driven economy, is also reflected in the findings. According to a survey performed March 8–17, “the sentiment index for big manufacturers stood at minus 3 versus minus 5 seen in the previous month,” according to Reuters.

The manufacturers’ indicator declined 11 points from three months prior, indicating a decline in big manufacturers’ sentiment as measured by the BOJ tankan’s headline big manufacturers index. Over the following three months, it is anticipated that the Reuters Tankan indicator will increase to plus 10. From plus 17 in February, the big service-sector firms index increased to plus 21 in March. In June, the indicator is predicted to decrease to plus 16.

The outlook for service-sector businesses improved as a sign of a domestic demand-driven recovery, in which households may be encouraged to spend their way out of the COVID-induced doldrums by the possibility of higher wages among large businesses at the spring labor talks. The unsatisfactory outcomes highlighted the vulnerability of the third-largest economy in the world, where exports are slowing and private spending, which makes up more than half of the economy, is stagnant. The poll from the central bank, which is expected on April 3, is likely to reveal a decline in business confidence at major manufacturers.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The day after the FED lifted the 25bps rate hike, gold values increased to 1.6%. FED Powell made it plain in a statement that no rate cuts were anticipated for 2023. Investors anticipated that the US banking collapse would make a pause in the rate increase cycle this year.

The abrupt movement of Yellow Metal suggested that the FED may reduce interest rates if more US banks experience a collapse in the future.

SILVER Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has reached the higher high area of the channel.

Following the Federal Reserve’s rate decision and Chair Jerome Powell’s news conference, gold prices rose by about 1.6% on Wednesday. The Fed’s main message was that officials did not currently see a need for rate cuts this year. Mr. Powell emphasized this point. Since the collapse of SVB, markets have been actively pricing in the latter. Market attention was nevertheless drawn to the Fed’s less hawkish change in its policy statement. Policymakers changed the language regarding rate rises from being “ongoing increases” to “anticipating” some additional firming as necessary. On the Fed, the yield on the 2-year Treasury note and the US dollar declined. Usually, gold serves as the anti-fiat currency. As a result, the drop in the dollar and bond yields was greeted by XAUUSD.

Recognize that, contrary to Fed projections, markets are still firmly on the rate-cut route for this year. If the latter turns out to be the case, gold may abandon the gains it has made so far this month. What challenges does gold face over the next 24 hours in light of this? The focus is on the US’s initial jobless claims, which are expected at 12:30 GMT. According to economists, there were +197k jobless claims last week as opposed to +192k the week before. One of the few timely pieces of information we have on the job market is unemployment claims. It will give a glimmer of how the economy is doing in the first complete week following the failure of Silicon Valley Bank. A sudden spike in strength could validate market predictions of rate drops. That might help metal.

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has reached the horizontal support area of the pattern.

After the FED raised interest rates by 25 basis points yesterday, the price of oil increased. China’s recovery from the Covid-19 economic crisis indicates that oil usage will increase rather than decrease.

The Canadian dollar will gain confidence this week from statistics on retail sales, but this week’s lower-than-expected CAD CPI readings raise concerns about a rate pause at upcoming BoC meetings.

After a two-day hiatus, USDCAD bears are back at the table as widespread US Dollar weakness coincides with early Thursday’s rise in oil prices. Thus, during the sluggish Asian session, the Loonie pair revisits its intraday bottom near 1.3700. Nevertheless, the US Dollar Index falls for the sixth day in a row as bulls continue to hover near the previous day’s lows, which date back to early February, as they approach the 102.30 level. In doing so, the US central bank’s (Fed) 25 basis points (bps) rate increase is not greeted with enthusiasm by the US currency’s gauge against six major currencies due to dovish concerns about the Fed’s next move and worries about the US banking industry. The Fed’s announcement of a 0.25% rate increase was in line with market expectations, but the statement that “some additional policy firming may be appropriate, instead of previous remarks like ongoing increases in the target range will be appropriate” rebuffed the policy hawks.

It should be mentioned that Fed Chair Jerome Powell and US Treasury Secretary Janet Yellen’s remarks were more significant because Powell’s statement that rate cuts are not expected this year gave the dollar bears breathing room in the previous. The US Treasury Secretary Janet Yellen, on the other hand, disqualified the idea of “blanket insurance” for bank deposits. The Federal Deposit Insurance Corporation is reportedly delaying the bid date for a Silicon Valley private bank, according to recent news reports from Bloomberg. In other news, WTI crude oil is up for the fourth day in a row, continuing the early-week recovery from the lowest levels since December 2021. As of press time, it was up 0.52% intraday near $70.30. In doing so, the black gold ignores a surprise build in weekly inventories in favor of cheering up expectations for increased energy demand, driven by optimism surrounding China. However, according to the US Energy Information Administration’s (EIA) weekly Crude Oil inventory statistics, the stockpile increased by 1.117 million barrels compared to the estimates of -1.448 million and 1.55 million barrels, respectively.

In this environment, US 10-year and 2-year Treasury note yields remain under pressure at latest 3.48% and 3.96%, while the S&P 500 Futures post modest gains despite Wall Street’s negative performance. Prior to Friday’s important Canadian retail sales and US durable goods orders for January and February, respectively, second-tier data from the US and Canada can amuse USD/CAD pair speculators.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

It will be determined whether the Swiss Franc will perform better or worse based on today’s SNB monetary policy meeting.

Commerzbank economists believe that the Swiss Franc will only experience a lessened negative effect if the SNB prints a rate increase of 25 basis points; otherwise, the CHF will depreciate.

The Swiss franc’s moves today will be determined by Thomas Jordan, the chairman of the SNB.

Today’s agenda item is the judgment made by the Swiss National Bank. Commerzbank economists assess the potential effects of the SNB Monetary Policy Announcement on the Franc.The Franc would not instantly benefit if the SNB only implemented a 25 bps rate step or decided against one altogether. The SNB may, however, be taking into account the possibility of minimizing the medium-term harm.

The outcome would not necessarily be as bad for CHF as one might think if the SNB were to communicate credibly to the market today that no step or 25 bps are nothing more than a wait-and-see approach until the effects of the recent turbulence can be assessed. In that scenario, the success of today’s SNB press conference would be entirely dependent on SNB Chair Thomas Jordan’s ability to communicate.

USD Index Analysis

US Dollar Index is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

After the FED raised rates by 25 basis points on the final day, the US Dollar Index fell yesterday. FED We make choices based on the state of the US economy, so a fast-indicated rate hike is not an option.

The US has a competitive labor market and a low jobless rate. GDP was downgraded to 0.40% from 0.50% in the March summary of economic forecasts, and the unemployment rate was predicted to drop to 4.5% from 4.6%. For 2023 and 2024, the core PCE inflation is higher forecast at 3.6% and 2.6%, respectively.

The U.S. dollar immediately took a turn to the downside following the FOMC announcement, with the DXY indicator dropping more than 0.8%. This was caused by the sharp decline in Treasury yields, particularly those at the front end of the curve. The Fed’s less hawkish guidance—issued in response to the recent turmoil in the financial sector—was what spurred this action. All of this points to the end of the central bank’s cycle of rate increases, which is bad news for the U.S. currency. The Federal Reserve wrapped up one of its most eagerly awaited meetings today with a unanimous vote to increase interest rates by a quarter of a percentage point to 4.75%-5.00%, broadly in line with forecasts. With this change, borrowing costs have reached their most stringent level since 2007, demonstrating the central bank’s commitment to reestablishing market stability. Wall Street’s expectations were in flux prior to today’s statement due to the banking sector’s unrest following the failure of two lending institutions and the bailout of Credit Suisse earlier this month. After government officials swiftly unveiled coordinated steps to support the financial system, market stress has started to lessen, but sentiment was still shaky.

The FOMC observed in its policy statement that the labor market is still strong and that inflation is still high. Although the Fed emphasized that the situation could lead to tighter credit conditions for consumers and businesses, generating downside risks for economic activity, hiring, and inflation, it stressed that the banking system is sound and resilient. The phrase “ongoing increases in the target range will be appropriate” was changed to “additional policy firming may be appropriate” in the forward guidance section. While indicating further tightening, this message is less hawkish than earlier ones, indicating that the hiking cycle is nearing its conclusion. Over the medium run, this is probably bad for the US dollar.

The March Summary of Economic Projections (SEP) differed significantly from the information provided in December 2022. The unemployment rate was reduced to 4.5% from 4.6%, reflecting continued trust in the labor market despite escalating economic headwinds, while the GDP forecast was revised downward to 0.4% from 0.5% previously. The core PCE inflation rate for 2023 and 2024 was also increased by 0.10% to 3.6% and 2.6%, respectively. The following highlights important information. The median projection for 2023 was unchanged at 5.1%, indicating an extra 25 basis points of tightening through the end of the year according to the Fed’s so-called dot plot, which depicts the trajectory of interest rates. Rates are projected to be 4.3% in 2024 as opposed to 4.1% in December, suggesting a slight easing of the terminal rate in the near future.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Madis Muller, a member of the ECB’s Governing Council, stated that future sessions may see a small increase in interest rates.

Once inflation in Europe is under control, it will be the primary impediment to rising borrowing costs.

Madis Muller, a member of the Governing Council of the European Central Bank (ECB), stated on Thursday that the ECB should probably increase interest rates slightly. A larger issue than the increase in borrowing costs is inflation. It is essential that we manage inflation.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Last day’s UK CPI data were greater than anticipated, strengthening the pound against other currency pairs. This CPI may decline to 2.9% in the second half of 2023, as predicted by the Office for Budget Responsibility.

Support for a 25bps rate increase by the FED renders a 25–50bps rate increase by the Bank of England today a strong expectation.

The UK PM Rishi Sunak’s resolution of the Northern Ireland Protocol problem is good news for the UK pound.

Headline Inflation in the UK deviated from a three-month pattern and increased in February, reaching 10.4% y/y from January’s 10.1% y/y and exceeding market expectations of 9.9%. Additionally, core inflation increased sharply, by half a point, to 6.2% from 5.8%, exceeding market expectations. “The increase in the annual inflation rate in February 2023 mainly reflected price rises in the restaurants and hotels, food and non-alcoholic beverages, and clothing and footwear divisions,” The Office for National Statistics states. In the transport sector, negative effects from motor fuels and recreation and culture partly offset these positive effects.Due to reduced energy prices, UK inflation is anticipated to drop significantly at the end of Q2 and was most recently predicted by the Office for Budget Responsibility to reach 2.9% by the end of the year.

The UK’s inflation figures released today reverse a three-month downward trend, increasing pressure on the BoE to raise interest rates at tomorrow’s MPC meeting by at least 25 basis points and perhaps even 50 basis points. Although the UK has so far escaped the recent global banking crisis, there are still worries that any additional bank runs could significantly slow economic development as banks reduce their lending activity. Following the publication of the inflation data, cable has increased as a result of higher market expectations for rate hikes. Before 1.2292 enters the picture, the pair wants to challenge the most recent double high at around 1.2283. 1.2448 becomes a medium-term goal above this point. The most recent US monetary policy judgment is scheduled for later today. The Fed is anticipated to increase interest rates by 25 basis points and present a dovish message during the news conference. The US dollar and cable will both move quickly whenever an unexpected event occurs.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Following the US FED’s 25bps rate increase last night, the Australian dollar recovered from its lows.It was not a statement from US Treasury Secretary Janet Yellen that caused the US Dollar to decline; rather, it was the lack of insurance to all deposits to all banks.

Australia’s robust labor market prompts the RBA to consider raising rates once more in April.

Inflation is brought under control if household spending is low and business operations are slowed when credits are not obtained from banks. Tight credit conditions in US banks cause house holds and business credits to suffer.

Early in the European session, the AUDUSD pair increased to 0.6750. The Australian dollar has gained value as a result of signals from Federal Reserve (Fed) head Jerome Powell about stopping the rate hike cycle after raising rates by 25 basis points (bps) to 4.75%–5.00%. The general public anticipates that Fed Powell has given consideration to a pause due to worries about a banking crisis following the failure of three mid-sized US institutions.

In spite of this, the Fed has not yet given up the fight against persistent inflation because it still plans to raise interest rates one more time this year.As investors turn their attention to rate-hiking pause signals from forecasts of tight credit conditions by US banks for advances, S&P500 futures have dramatically extended their recovery. Fed Powell claimed that US banks are robust and resilient in his commentary about the state of the US banking sector, but recent events of financial instability could not rule out more filter execution from banks while disbursement of advances.

US banks’ stringent credit policies would cause delays in loans to individuals and companies, which could have an effect on inflation, total demand, and economic activity. If advances are delayed, businesses may experience a working capital crisis and become more vulnerable to running losses. In the early European session, the US Dollar Index (DXY) is just one inch away from the 102.00 safety net. Further declines in the USD Index cannot be ruled out, as investors’ faith in the US government has been shaken by Treasury Secretary Janet Yellen’s failure to guarantee universal protection for all deposits. Investors are anticipating the release of preliminary S&P Global PMI (March) statistics on the Australian Dollar front. According to agreement, the Manufacturing PMI will drop to 50.3 and the Service PMI to 49.9.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Following the US FED’s 25bps rate increase last night, the Australian dollar recovered from its lows.It was not a statement from US Treasury Secretary Janet Yellen that caused the US Dollar to decline; rather, it was the lack of insurance to all deposits to all banks.

Australia’s robust labor market prompts the RBA to consider raising rates once more in April.

Inflation is brought under control if household spending is low and business operations are slowed when credits are not obtained from banks. Tight credit conditions in US banks cause house holds and business credits to suffer.

In the Asian session, the NZDUSD pair’s rebound movement has gotten closer to 0.6250. The US Dollar Index (DXY), which had dropped to close to 102.00, experienced a brief pullback move as the Kiwi asset solidly recovered from 0.6220. The Federal Reserve (Fed) has come close to reaching its terminal rate, and the USD Index is currently hovering around its six-month low. It is anticipated that this downward trend will continue.

Rates rose to 4.75–5.00% as a result of the Fed’s expected 25 basis point rate increase. Jerome Powell, the head of the Fed, made a stronger effort to uphold his conservative position by claiming that rate cuts in 2023 are not likely because a tightening of monetary policy is crucial to bringing inflation down to 2%. The Fed’s Powell’s remark that additional policy firming may be appropriate signaled that the Fed was getting close to stopping its recent string of rate hikes, derailing the stage of hawkish stance. On Wednesday, there was a significant decline in US stock prices as Fed Powell allayed concerns about a bleak economic forecast brought on by lower demand and the size of economic activity. The US banking system is “sound and resilient,” according to Fed Powell’s commentary, but tight credit conditions for individuals and companies cannot be ruled out.

In Asia-Pacific, the New Zealand Dollar is having trouble staying afloat because market observers believe that the flood scenario will result in slower growth in the kiwi zone. Paul Conway, the chief economist at the Reserve Bank of New Zealand, stated on Thursday that although it was still unclear whether inflation expectations were under control, interest rates were undoubtedly falling and creating a welcome slowdown in economic demand.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/