GOLD Analysis

XAUUSD Gold price is moving in the Box pattern and the market has reached the resistance area of the pattern.

The primary cause of the gold price’s 50$ increase in a single day, which caused it to cross the 2025 dollar mark, was OPEC+ and Russian oil production cuts. Factory spies increased input costs and fixed higher output rates for the final consumers. The US FED must raise interest rates further to stimulate the economy as a result of the US inflation figure being too high. The notion of the FED delaying rate increases is not appropriate at this time.

In the early Asian session, the gold price has moved its bid profile above $2,020.00. On Tuesday, after weak Job Openings data confirmed that the United States labour market is cooling down and the Federal Reserve would prefer to take a neutral stance on interest rates, the precious metal gave a decisive break above the psychological resistance of $2,000.00. According to the CME Fedwatch indicator, the likelihood of keeping rates steady is now close to 59%.

As policy divergence between the Fed and other central banks continues, the US Dollar Index has dropped to a new monthly bottom of 101.45, and further declines are expected. Meanwhile, after a down day on Tuesday, S&P500 futures are higher in early Tokyo, suggesting investors are becoming more risk-tolerant again. As the only factor that could derail Gold’s upward rally, investors will be keeping a close watch on oil prices. Inflation around the world would be stoked by the reality that manufacturers would have to pass the cost of more expensive oil on to consumers. This may cause markets to once again anticipate further Fed policy easing. US employment and ISM services PMI figures will continue to receive close attention going forward. The consensus estimate for US employment growth in March is 200,000, down from the previous 242,000.

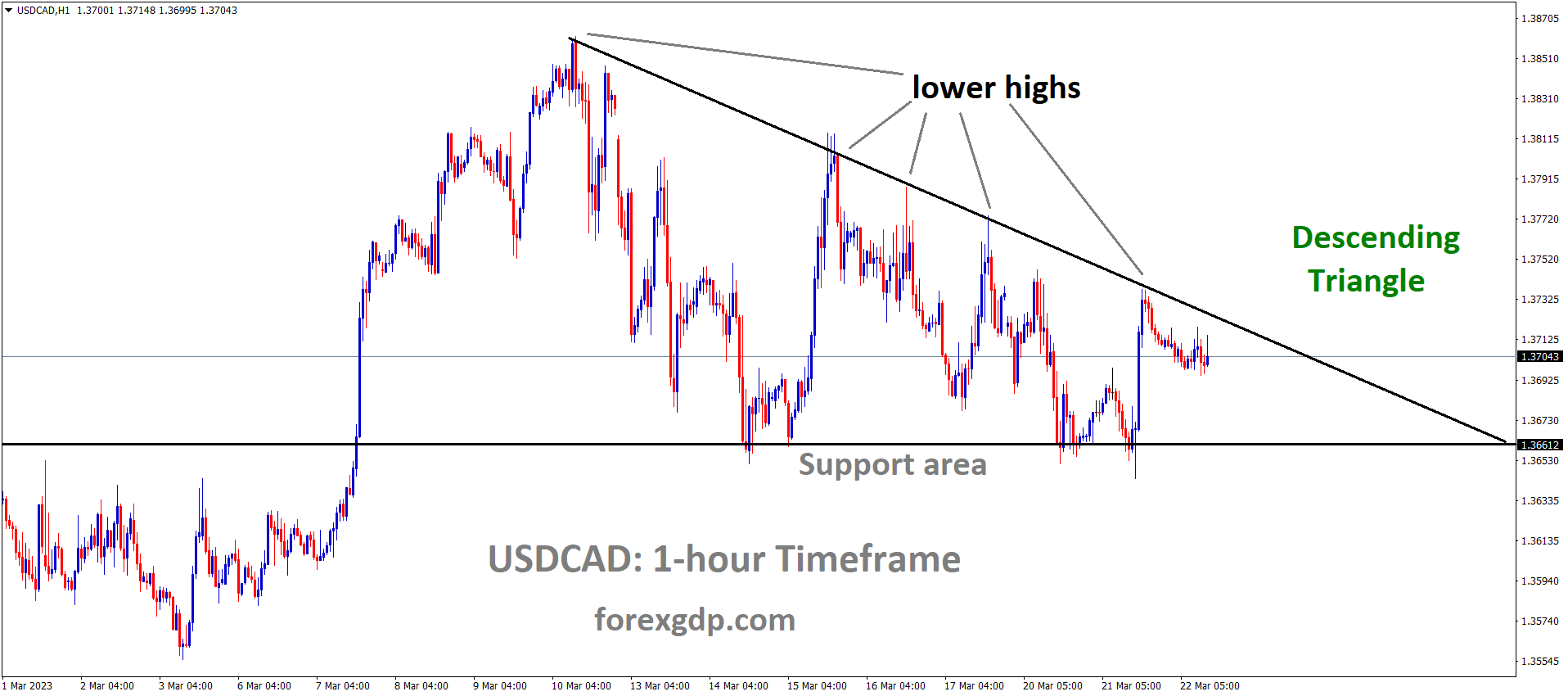

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

According to the Scotia Bank report, the Canadian dollar did well in the month of April. After a weak first quarter, the Canadian dollar was better in the second and third quarters. Strong Oil prices contributed to the Canadian Dollar’s strength versus other currency combinations. According to a 20-year average of 1% average returns provided 75% of the time, April is the best month for Canadian dollars.

Crude Oil Analysis

Crude Oil is moving in the Descending channel and the market has reached the lower high area of the channel.

Economists at Scotiabank predict that April’s favourable seasonality for the CAD will continue the Loonie’s recovery that began in late March. After a weak first quarter, the CAD usually trades at a slight premium in the second and third quarters. In the last 20 years, the Canadian dollar has performed best in April.

The chances of a deeper USD decline towards 1.3275/1.3325 are increasing as trend momentum signals are leaning USD bearish on intraday and daily studies, and the market is effectively chopping around trend support at 1.3430. The 1.3445-50 and 1.3490-00 levels represent USD support.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Because Russia prefers to deal in Chinese Yuan rather than US Dollar as a foreign currency, the Swiss Franc is stronger against the US Dollar. The US Dollar’s strength against the Swiss Franc decreased as a result of this report. The SNB is prepared to take action in the foreign exchange markets to support the CHF/USD exchange rate by bolstering the Swiss Franc’s value.

As traders look for more signs to prolong the two-day downtrend at the lowest levels since August 2021, the USDCHF makes rounds to 0.9050-60 ahead of Wednesday’s European session. Ahead of crucial US jobs and PMI statistics, the Swiss Franc pair follows a corrective bounce in US Treasury bond yields. US 10-year and 2-year Treasury bond yields, which have dropped for five and three days, respectively, take a break around 3.35 percent and 3.86 percent while depicting the bond market’s movements. In addition to the easing hawkish bias of the Federal Reserve, negative US job clues have weighed on US bond coupons.

Factories orders and job openings in the United States were both disappointing in February, which weighs on the value of the US dollar. Russia’s preference for the Chinese Yuan and an agreement between China and Brazil to bypass the US dollar as an intermediary currency could be related. On a separate note, Federal Reserve Bank of Cleveland President Loretta Mester’s recent hawkish remarks have joined the cautious mood ahead of the US ISM Services PMI and ADP Employment Change, which should help stabilise yields and the US Dollar despite the off in China. In this environment, yields and the US Dollar are licking their scars while S&P 500 Futures flounder near 4,130. Further USD/CHF consolidation may occur before the aforementioned US statistics. After that, however, the pair prices may be swept away by the expected gloomy US data.

USD Index Analysis

USD Index is moving in the Descending channel and the market has reached the lower high area of the channel.

After US JOLTS Job Openings came in lower than expected with a 9.931M number instead of the 10.4M anticipated, the US Dollar index dipped to two-month lows.

According to US Cleveland FED President Mester, a rate increase above 5% for the US economy is urgently required this time in order to contain inflation; rate increases may then be paused. US Factory Orders were lower than anticipated, at -0.7% month over month. Instead of using the US Dollar as an intermediary money, Russia and Brazil chose to use the Yuan.

As traders anticipate the crucial US activity and employment data on early Wednesday, the US Dollar Index has paused at a two-month low and is also probing the two-day downtrend. As a result, the US dollar index rises to 101.50 against a basket of six major currencies, erasing gains made late Tuesday after the index hit a multiday low of 101.45. DXY takes the hit for disappointing US data and attacks on the dollar’s position as the world’s reserve currency. Even if Fed policymakers predict more rate hikes, the most recent decrease in the hawkish Federal Reserve has added strength to the US Dollar’s bearish bias. The newest decline in the value of the US dollar has been highlighted in a report published by Bloomberg, which also suggests that the dollar is losing favour as a reserve currency in Russia.

According to reports, the Chinese Yuan overtook the US Dollar in monthly trading volume in Russia for the first time in February, and the disparity between the two currencies has only widened since then in March. Brazil and China have recently stopped using the US dollar as a commerce intermediary. The United States’ Factory Orders for February came in at -0.7% MoM on Tuesday, below the -0.5% forecast and the -2.1% lower revision from January. The United States Job Openings and Labor Turnover Survey reported 9.931M openings in February, down from 10.4M forecasted and 10.563M corrected in January. Federal Reserve Bank of Cleveland President Loretta Mester has lately called for interest rates to be raised above 5% and held there for some time when discussing Fed policymakers. DXY prices should have been supported by global concerns, but they have not been as of late. The European Union has abandoned Russia, Russian Foreign Minister Sergei Lavrov said, fueling concerns of an escalating conflict between Moscow and Brussels. The official also said that Moscow would take a hard line with Europe if necessary.

The escalating conflict between the United States and China is also discussed, as Beijing continues to express its disapproval of US-Taiwan relations. A representative for China’s Los Angeles consulate has spoken out against President Tsai Ing-wen of Taiwan’s meeting with US House Speaker Kevin McCarthy on Tuesday morning. Wall Street finished with modest losses despite these plays, and US Treasury bond yields stay depressed, with the benchmark 10-year coupon holding lower grounds near 3.34%. It is worth noting that the FedWatch Tool on the CME Group website indicates odds of a May rate increase of 0.25 percent by the US Federal Reserve are close to even. Traders in the US Dollar Index should keep an eye out for stronger readings of US ISM Services PMI and ADP Employment Change in the coming days and weeks in order to recoup some of their recent losses and delay the likelihood of the index falling to a new yearly bottom below 101.00.

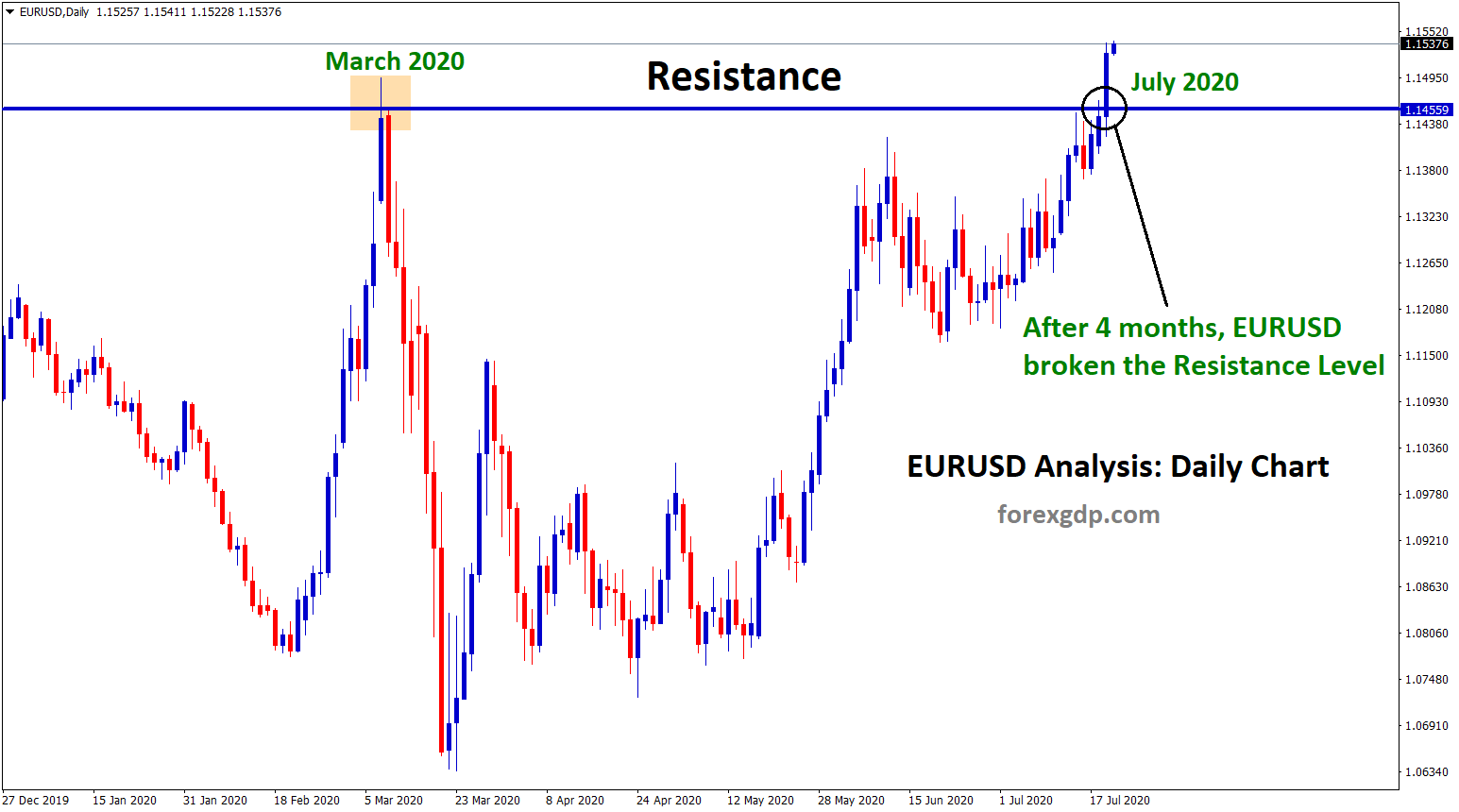

EURUSD Analysis

EURUSD is moving in an Ascending triangle pattern and the market has reached the resistance area of the pattern.

ECB Based on a poll of consumer sentiment regarding price changes over the next 12 months, inflationary pressures may ease to 4.6% in February’s report from 4.9% in January’s survey. Inflation in the Eurozone can be kept under control if the European Central Bank raises interest rates. As a result of the conflict between Russia and Ukraine, oil prices soared on global markets, reviving concerns about an impending energy catastrophe in the Eurozone. The outlook for the Eurozone economy over the next year remains optimistic, and a decline in the jobless rate is anticipated.

Following in the footsteps of the US Dollar Index, EURUSD has been trading in a tight range near 1.0960. After investors show interest in the United States due to the release of Automatic Data Processing Employment and ISM Services PMI data, the major currency pair is battling to find a decisive move. After showing modest gains in the Asian session, S&P500 futures have reversed course, signalling a further drop in market participants’ risk appetite. On Tuesday, investors dumped US stocks after the release of dismal data on US Job Openings, which came on the heels of a drop in Manufacturing activity that raised the prospect of a recession. On the other hand, the US Dollar Index has shown a modest recovery after retracing to 101.45 from the monthly bottom, with support coming from higher US Treasury yields. Despite increasing expectations for steady monetary policy from the Federal Reserve, investor interest in US government bonds has waned. Yields on 10-year US Treasuries have increased to around 3.35 percent. The tight labour market in the United States has been a significant contributor to rising interest rates and persistent inflationary pressures over the past year. As a result of the labour shortage, households were flush with extra cash; this boosted store demand and prevented prices from falling. U.S. job openings dropped below 10 million for the first time since 2021 on Tuesday, signalling a decrease in economic demand for labour. This enabled the shrinking US manufacturing sector to band together with the lowering demand for labour to send the message that the US labour market was cooling due to a gloomy economic outlook. Consistently dismal economic reports are fueling concerns that the US economy is entering a recession. As a result, market participants are betting that the Federal Reserve will temporarily halt its policy tightening phase. According to the CME Fedwatch index, market participants favour leaving interest rates steady at the upcoming May meeting.

The state of the US labour market can be better understood upon the release of the US ADP Employment statistics. The average estimate for employment growth in the United States in March is 200 thousand, down from February’s revised figure of 242,000. Further clarification will come with the release of the US ISM Services PMI statistics. Since a reading below 50.0 indicates a decline, the manufacturing industry in the United States has been contracting for the past five months. Additionally, quarterly GDP declines could be foreseen as a result of a weakening services industry. It is anticipated that the US ISM Services PMI for March will fall from 55.1 to 54.5. In addition, the forward-looking New Orders Index would fall to 57.6 from its previous report of 62.6. Median inflation expectations for the next 12 months in the Eurozone dropped to 4.6% in February from 4.9% in January, according to a poll of consumer expectations for inflation performed monthly by the European Central Bank. Christine Lagarde, president of the European Central Bank, has been hiking interest rates steadily in an effort to reduce inflation in the Eurozone. However, the recent spike in oil costs is not reflected in the economic data, which could lead to a surge in global inflation. The high reliance of the Eurozone economy on energy imports raises the risk of a revival of inflationary pressures, which could bring the continent back to square one. Other than that, people have less pessimistic outlooks on economic development in the coming year and on the unemployment rate in the following year.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

More rate increases sooner, according to BoE policymaker Silvana Tenreyro, should help with the UK’s significant increase in inflation. The US dollar fell against the British pound as a result of US JOLTS job opportunities being less than anticipated.

Today’s scheduled UK Services and Composite PMI will determine how far the pound moves in the UK.

Bulls and bears in the GBPUSD currency pair wrestle at the 10-month high near 1.2500 as they wait for important USUK statistics early on Wednesday. The recent corrective bounces in the US Dollar and yields have also allowed the Cable pair buyers to pause before key data, in addition to the cautious mood that has been prevalent lately. On Tuesday, the Cable pair experienced its strongest rally in three weeks, rising to levels last seen in June 2022 as a result of widespread US Dollar weakening and hawkish remarks from Bank of England officials. Nevertheless, on Tuesday, the US Dollar Index fell to its lowest values in five weeks before reestablishing the multi-day low and rebounding off the 101.43 level to around 101.54 by the time of publication. It’s important to keep in mind that the US Dollar has recently suffered from negative US data and a decline in support from major players in international commerce.

Speaking of the data, the US JOLTS Job Openings fell to their lowest levels since May 2021, flashing a number of 9.931 million for February, compared to the 10.4 million expected and the 10.563 million revised earlier. In a similar vein, US factory orders for February came in at -0.7% MoM, below expectations of -0.5%, and were downwardly revised from -2.1% previous. It should be mentioned that the US Dollar appears to be suffering as a result of Russia’s recent preference for the Chinese Tuan and the China-Brazil agreement to disregard the US Dollar as an intermediary currency. On the other hand, according to Reuters, Bank of England Chief Economist Huw Pill stated on Tuesday that due to the possible persistence of domestically generated inflation, caution is still required when evaluating inflation prospects. Silvana Tenreyro, a policymaker for the BoE, stated that she anticipates that the high bank rate at the moment will necessitate an earlier and faster reversal in order to prevent a substantial undershoot in inflation.

Loretta Mester, president of the Federal Reserve Bank of Cleveland, mentioned the necessity of raising interest rates above 5% and keeping them there for some time earlier in the day. The S&P 500 Futures show modest gains while reflecting the mood, even though Wall Street ended with modest losses. Additionally, after declining for the previous four and three straight days, the yields on US Treasury bonds for two and ten years also take a break, settling around 3.35% and 3.85%, respectively. Before the US ISM Services PMI and ADP Employment Change for March, the Cable pair can immediately follow the final readings of the UK’s S&P Global Composite PMI and Services PMI for March.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Philip Lowe, Governor of the RBA, stated Overall, the Australian economy is doing well, and crisis fears are fading. The rate paused in this meeting is not for rate cuts or rate pausing throughout the year; rather, it is a plan to see if inflation falls in the economy this month. This is not good news for the Australian dollar.

Since last night’s hawkish comments from the Fed’s Mester, the Australian currency has continued its decline against the U.S. dollar. The dollar has gained some ground as a result of President Cleveland’s demand for a terminal rate above 5% while keeping a restrictive monetary policy. While deciding to leave interest rates unchanged this morning, Reserve Bank of Australia Governor Philip Lowe erred on the more aggressive side by leaving the door open for future rate hikes. Given the complexity of the global economy, the RBA’s plan appears to be one of patience and observation. Despite global recessionary fears, Australia’s economy has proven to be resilient, and now the pro-growth AUD is looking to a favourable re-open in China for even more upside.

The ADP report on US employment will give markets a glimpse into the current state of US employment, but the ISM non-manufacturing release will be the primary focus. Important for US and USD crosses as the US is mainly a services driven economy, this report could provide relief for the AUD if actual data confirms the small downside revision to the print.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The formal cash rate is now 5.25% from 4.75% after the RBNZ unexpectedly increased interest rates by 50 basis points.The RBNZ stated that the short-term inflation rate is too high and that steps have been made to control inflation rates in the New Zealand economy. Despite the slow decline of the economy, demand is greater than supply. After today’s unexpected rate increase of 50 basis points, the New Zealand dollar surged higher.

After the Reserve Bank of New Zealand shocked the markets with a more aggressive rate increase, the New Zealand Dollar gained ground against its major peers. Prior to the rate determination, the RBNZ was expected to raise rates from 4.75% to 5%. Instead, the central bank went all out and increased benchmark loan rates by 50 basis points, or 5.25%. Policymakers emphasised that the official cash rate must be at a level to lower costs because inflation is still too high and persistent. Despite the economy slowing, the central bank observed that supply is still outpacing demand. It’s interesting to observe that the committee has noticed an increase in short-term inflationary pressures. The banking system is prepared to handle a slowdown, the RBNZ concluded. The RBNZ stands out from its important competitors with this action. For instance, the Reserve Bank of Australia stopped all tightening while the Federal Reserve significantly slowed down its speed. It’s interesting to note that RBA Governor Philip Lowe gave a speech soon after the RBNZ. He emphasised that their break does not mean that rate increases are finished.

When considering overnight index swaps, it appears that traders are still factoring in further tightening to a level of about 5.5%, with chances of that being the case being around 70%. As a result, from the viewpoint of yield, this is giving NZD a competitive advantage over its key competitors. In the immediate future, that might continue to provide it with upside support. In light of this, Friday’s non-farm payrolls data in the US will be the main topic of discussion for NZDUSD. While stock markets will be closed on Good Friday, forex markets will be open for business. Still, given a significant departure from expectations, this implies less liquidity, which increases the risk of volatility. Despite statements to the opposite from the Federal Reserve, markets are still anticipating rate cuts this year. A strong print could counter predictions of a rate reduction, strengthening the US Dollar.

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has rebounded from the horizontal support area of Minor Box pattern.

In contrast to predictions of 0.30% and a prior estimate of 0.50%, German factory orders came in at 4.8%. According to this indicator, Germany’s manufacturing industry is improving. In contrast to forecasts of -10.5% and the actual reading of -12.0% seen in January, manufacturing orders in Germany came in at -5.7%.

The manufacturing sector recovery appears to be picking up steam as the German Factory Orders data revealed a much larger increase in February than was anticipated. Contracts for goods “Made in Germany” came in at 4.8% on the month, compared to 0.3% expected and 0.5% prior, as shown by the latest data released by the Federal Statistics Office on Wednesday.

Germany’s annualised Industrial Orders came in at -5.7% in the reported month, lower than the -10.5% predicted and the -12.0% recorded in January.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/