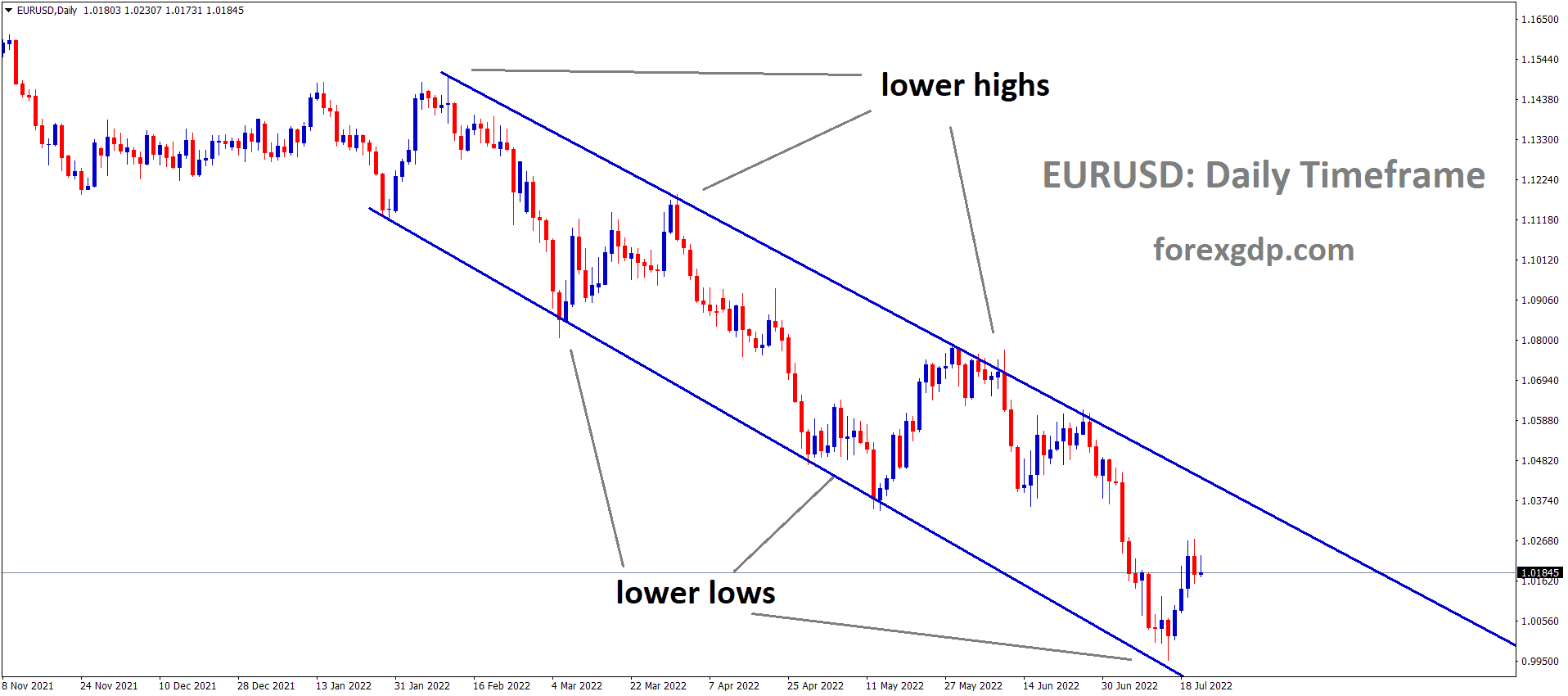

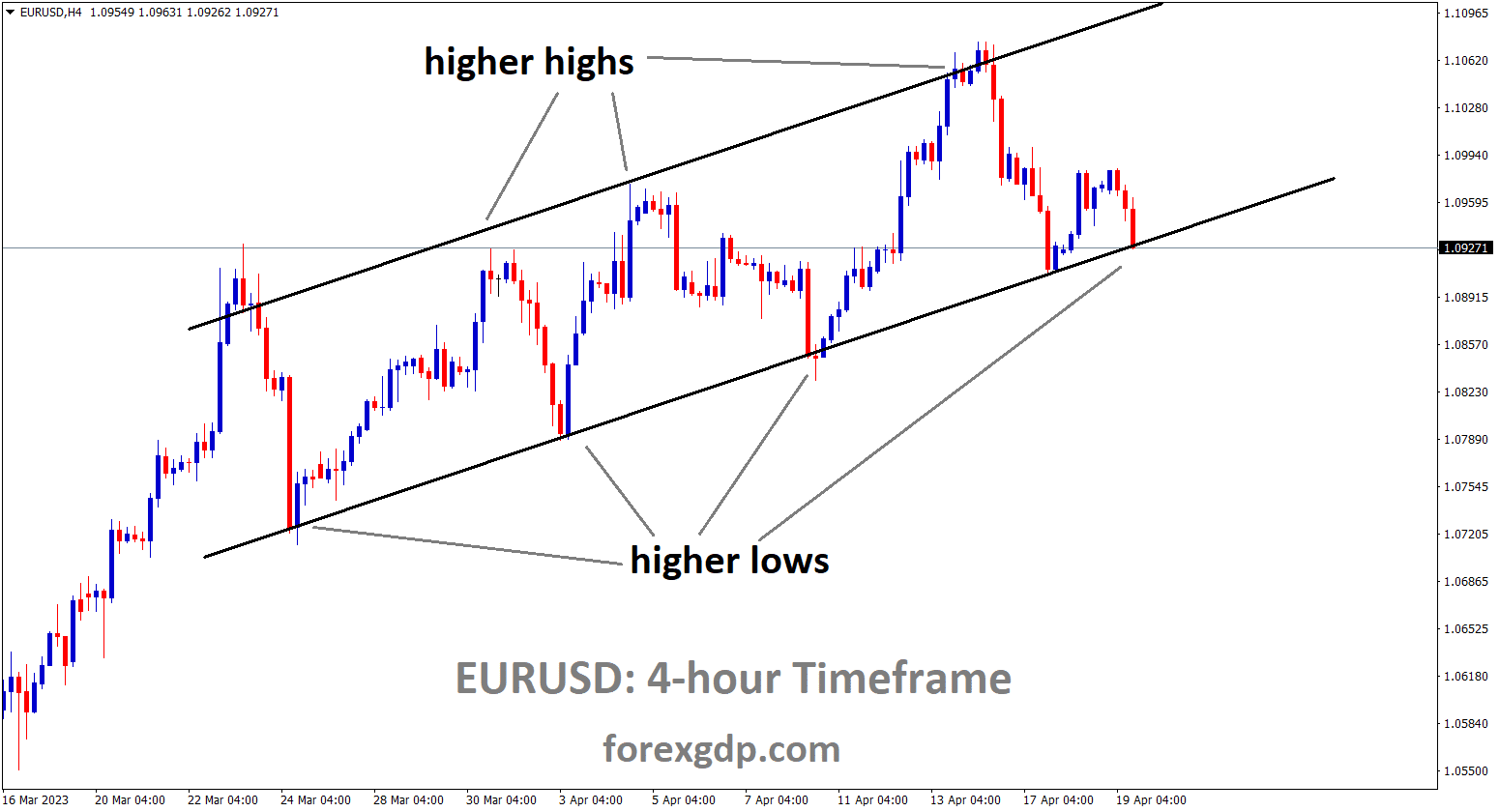

EURUSD Analysis

EURUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

On the strength of a respectable dollar recovery and the continuation of the German 10-year Bund yields’ upward march, the EURUSD extends the turbulent trading it has been experiencing this week and now somewhat fades Tuesday’s gain. Price movement surrounding the pair continues to focus on the upcoming interest rate decisions by the ECB and the Fed, with both central banks projected to hike rates by 25 basis points in May, in the absence of substantial catalysts. The latter appears to be strongly supported by recent hawkish remarks made by policymakers on both sides of the Atlantic, who continued to call for a tighter-for-longer approach in the face of the inflation that is still high. The only publication on Wednesday on the euro calendar will be the final inflation rates for all of Euroland. Along with the release of the Fed’s Beige Book, weekly Mortgage Applications as recorded by MBA are required in the US.

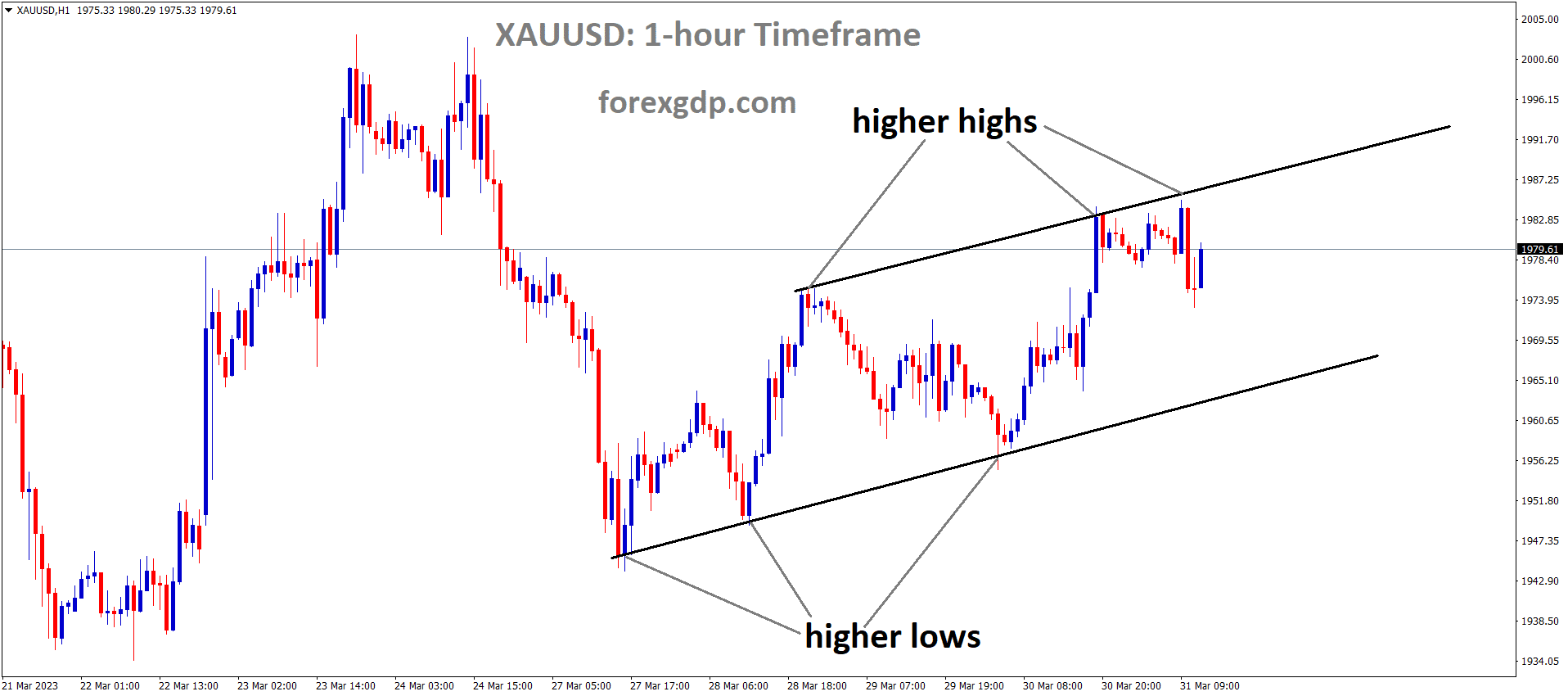

GOLD Analysis

XAUUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

As the US dollar strengthens, the price of gold suffers, falling again below $2,000 to roughly $1,990 after resetting its intraday bottom at the $1,987 level early on Wednesday in Europe. The brilliant metal does this by taking cues from the risk-off sentiment, which is primarily associated with Russia and China, as well as the worries over the US debt payment default. Further supporting the US Dollar’s recovery and depressing the XAUUSD price are positive US Treasury bond yields and hawkish Federal Reserve comments.Concerns over US-China animosity over Taiwan as a result of the US House China Committee’s consideration of the Taiwan invasion scenario and the UK’s warning that Russian hackers are targeting Western critical infrastructure weigh on the risk profile. The Reuters report that US customers are starting to fall behind on their credit card and loan payments as the economy declines may be read in the same vein. In addition, US President Joe Biden’s hesitation to raise the debt ceiling is likely to delay the decision. Bloomberg also reported on China’s possible involvement in the conflict in Russia and Ukraine, which strengthened the risk-off sentiment and boosted the value of the US dollar, which in turn drove down the price of gold.

The markets are almost certain that the Fed will raise interest rates by 0.25% in May, and this certainty joins the lately dropping chances favouring a rate cut in 2023 to show the hawkish slant of the US central bank. The moves are the result of Friday’s US Consumer-centric figures, Monday’s US activity data, and the most recent bullish remarks from James Bullard of the St. Louis Federal Reserve, Thomas Barkin of the Richmond Fed, and Raphael W. Bostic of the Atlanta Fed. However, recent negative US housing data nudge the Fed’s doves and provide gold a floor. Amid these manoeuvres, the US two-year Treasury note yields jumped to a new high in a month while the S&P 500 Futures fell 0.30% intraday after reaching its best levels since early February. The US Dollar Index (DXY) is able to post intraday gains of 0.20% while testing the 102.00 level thanks to the US 10-year bond coupons, which have also increased to 3.61%. Moving forward, gold traders should look to risk factors, particularly those related to geopolitics and the US debt ceiling, for immediate guidance as today’s economic calendar is mostly devoid of events with just the Fed Beige Book scheduled to be released. However, the probable rise in risk aversion and the Fed’s hawkish forecasts could put pressure on the price of XAU/USD.

USDJPY Analysis

USDJPY is moving an Ascending channel and the market has reached the higher high area of the channel.

For the second consecutive day, the USDJPY pair exhibits some tenacity below the 134.00 round-figure level and draws new buyers on Wednesday. Spot prices reach a nearly three-week high in the final hour, around the 134.75 zone, thanks to the intraday upward rise that takes up speed in the early European session but lacks follow-through. The demand for the US Dollar is revivified by a further increase in US Treasury bond yields, which is considered as a major factor supporting the USD/JPY pair. In fact, amid rumours that the Federal Reserve would keep rising interest rates, the yield on the benchmark 10-year US government bond and the two-year US Treasury note both reach more than a four-week high. The hawkish comments made by Fed officials helped to increase the odds. In reality, Fed Governor Christopher Waller stated on Friday that the central bank still has to raise rates since a year of ferocious rate hikes “haven’t made much progress” in bringing inflation back to their 2% target. James Bullard, president of the St. Louis Fed, added to this by supporting the argument for further 75 bps of tightening in a Tuesday interview, in contrast to the market consensus for one more 25 bp raise next month and then likely cuts later this year.

A resilient economy was also supported by the recent excellent US macro data, which also fanned worries that the Fed may still have work to do and kept US Treasury bond yields high. The rate differential between the US and Japan widens as a result. In addition, the Bank of Japan’s dovish position weakens the Japanese Yen and strengthens the USD/JPY pair, albeit gains may be limited by the risk-off urge. Concerns about economic headwinds brought on by increased borrowing costs are exacerbated by the Fed’s potential for additional policy tightening. The equities markets have just experienced a fresh leg down as a result, which tends to boost conventional safe-haven currencies like the JPY by tempering investors’ desire for riskier assets. Therefore, it will be wise to hold off on making any more appreciating moves until some follow-through buying has occurred.

USDCAD Analysis

USDCAD is moving an Ascending channel and the market has rebounded from the higher low area of the channel.

In the Asian session, the USDCAD pair is strengthening and is expected to move above the 1.3400 round-level barrier. The Loonie asset has had a respectable rally following a slow pullback to close to 1.3360. As Canadian inflation has further eased and the likelihood of another rate hike from the Federal Reserve is surging, the upside in the major seems more favourable. The Bank of Canada will maintain interest rates at 4.5%, according to Tuesday’s announcement of the country’s consumer price index. The 0.5% increase in the monthly headline CPI was as anticipated by the market. Additionally, yearly headline inflation decreased to 4.3%, which is in line with market expectations. The core CPI, which excludes the cost of food and oil, dipped from the previous announcement of 4.7% to 4.3%, but it still exceeded estimates of 4.2%.

The fact that Canada’s inflation has been steadily declining shows that the BOC Governor Tiff Macklem’s current monetary policy is restrained enough to stop inflationary pressures. In an opening address before the House of Commons Standing Committee on Finance on Tuesday, BoC Governor firmly backed the need to keep rates higher for a longer amount of time to bring inflation back to the target of 2%. The US Dollar Index is getting close to 102.00 as investors are optimistic about the Fed’s third straight 25 basis point rate hike. The quarter-end result season in the US economy is causing investors to be cautious as their risk appetite is weakening. The S&P500 futures are gradually falling as more rate increases could further reduce corporate profits.

Crude Oil Analysis

Crude Oil has broken the Descending channel in Downside.

According to statistics from the American Petroleum Institute released on Tuesday, the United States’ crude oil stocks decreased by 2.675 million barrels this week despite experts’ expectations for a 2.464 million barrel decline. More than 44 million barrels of crude oil have been added to the world’s reserves so far this year. This week, the SPR’s crude oil inventory fell for the third consecutive week, shedding an additional 1.6 million barrels to reach 368 million barrels, the lowest level since October 1983. Production of U.S. crude oil surged to 12.3 million bpd. U.S. production is currently 500,000 bpd more than at this time last year, but 800,000 bpd lower than the peak production projected in March 2020. Prior to the release of the data on Tuesday, WTI was trading down, but because to OPEC+’s unexpected statement that it would be reducing crude oil output by 1.6 million barrels per day starting in May, the price was still above $80 per barrel. Additionally trading down for the day was Brent crude. Within a short time of the report release, WTI was trading at $80.85. Additionally, petrol inventories decreased by 1 million barrels after increasing by 450,000 barrels the week before. After dropping by 1.98 million barrels the week before, distillate inventories dropped by 1.9 million barrels this week. After plunging 1.36 million barrels the previous week, inventory losses at Cushing, Oklahoma, totaled 600,000 barrels.

USD Index Analysis

USD Index is moving in Descending channel and the market has reached the lower high area of the channel.

On the back of fluctuating patterns in risk appetite, the index continues its range-bound theme this week close to the 102.00 level. US yields continue to trade towards the top of the curve in the interim, supported by a stronger expectation that the Fed would raise interest rates by 25 basis points at its meeting in May. According to CME Group’s Fed Watch Tool, the likelihood of such a scenario is estimated to be around 85%.The weekly data from the EIA on US crude oil inventories follows the MBA Mortgage Applications, which are typically expected in the first turn of the US calendar. The day will culminate with the publication of the Fed’s Beige Book. The price movement surrounding the dollar and the rest of the FX space has been rather subdued so far this week due to the lack of significant catalysts. Meanwhile, the sharp decline in the value of the dollar since March has been supported by a rise in expectations that the Federal Reserve will pause its current tightening cycle shortly after its meeting in May. However, continuing disinflation, emerging weakness in some important fundamentals, and relatively enduring concerns about the banking sector continue to argue in favour of a change in the Fed’s normalisation strategy.

AUDUSD Analysis

AUDUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

Throughout the early European session, the AUDUSD pair struggles to build on the previous day’s gains and swings back and forth between modest gains and slight losses. A technically crucial 200-day Simple Moving Average is still below the pair, which is currently trading slightly above the 0.6700 round-figure level. There are a number of factors that help the US Dollar (USD) get some intraday buying, which is hurting the AUD/USD pair. The recent rise in US Treasury bond yields has been supported by predictions that the Federal Reserve will keep raising interest rates. In fact, the yield on both the rate-sensitive two-year US Treasury note and the benchmark 10-year US government bond rise to levels not seen in over four weeks. This, together with a more subdued atmosphere around the equities markets, helps boost demand for the safe-haven dollar and limits the upside for the perceived riskier Australian dollar.

However, the ambiguity around the Fed’s rate-hike trajectory prevents USD bulls from making risky wagers and provides some support for the AUD/USD pair. The markets have almost priced in a 25 bps lift-off in May, and numerous Fed officials have asked for additional raises. But only a slim possibility of another rate hike in June is indicated by the Fed funds futures. Aside from this, the Australian Dollar’s downside should be constrained by a decreased likelihood of an Australian recession, as well as the hawkish tone of the Reserve Bank of Australia’s April meeting minutes and the encouraging macroeconomic data from China. The aforementioned contradictory fundamental environment, on the other hand, calls for prudence from aggressive traders before positioning for a clear near-term trend for the AUDUSD pair. Investors will pay close attention to the Fed’s Beige Book release, which is scheduled for later in the US session, for the central bank’s assessment of the status of the US economy, as there are no significant market-moving economic data from the US on Wednesday. The USD price dynamics should be affected by this, coupled with US bond yields and the general risk attitude, and allow traders to seize short-term chances surrounding the AUD/USD pair.

GBPUSD Analysis

GBPUSD has broken an Ascending channel in downside.

Chancellor Hunt of the UK: The CPI results demonstrate once again why we must keep up our efforts to reduce inflation. Despite the UK inflation surprise to the upside, the British pound is somewhat weaker against the US dollar this morning. The Fed’s Bostic and Bullard’s pessimistic rhetoric appears to be continuing over from the US trading session, but I believe that when Europe gets going, the pound may recoup some of its lost gains. Food, non-alcoholic beverages, leisure, and culture were the top industry contributions to the inflation print. Core and headline data both exceeded expectations, and PPI followed suit. There is now more pressure on the Bank of England because the UK continues to have the highest inflation rate in western Europe.

Looking at the money market pricing below, there is a nearly 100% chance that the BoE will raise interest rates by another 25bps next month. Beginning with yesterday’s jobs report, which reaffirmed the tight labour market environment in the UK, this week has been very significant for the UK economy and its input data. Combining these two data sets suggests that the BoE may still need to tighten monetary policy more in order to reduce inflationary pressures. In the comment from UK Chancellor Hunt above, the first indications of which have emerged. The BoE’s Catherine Mann is expected to talk later today and may very possibly reaffirm these hawkish views.

EURGBP Analysis

EURGBP is moving in Descending channel and the market has reached the lower high area of the channel.

In response to higher UK consumer inflation data, the EURGBP cross encounters some supply during the early European session on Wednesday and falls to a new weekly low, near the 0.8810 area. After the UK Office for National Statistics reported that the headline UK CPI declined less than anticipated, to a 10.1% YoY rate in March from the 10.4% recorded in the previous month, the British pound strengthened a little bit. Furthermore, contrary to forecasts for a decline to 6.0%, the Core CPI, which excludes volatile food and energy items, remained constant at 6.2% YoY during the reporting month. This follows Tuesday’s better UK wage growth statistics, which should keep pressure on the Bank of England to boost interest rates even further. As a result, the EUR/GBP cross is expected to decline.

The relative underperformance of the common currency may also be a result of the European Central Bank’s policymakers leaving room for a slower pace of interest rate increases. In fact, ECB member Martins Kazaks stated on Monday that the institution may decide to raise interest rates by 25 basis points at its upcoming meeting in May. This adds to the slightly softer atmosphere that exists around the EUR/GBP cross. However, for the time being, aggressive bearish traders should exercise care before positioning for any additional intraday depreciating moves due to the lack of any significant follow-through selling. Market investors are now anticipating the release of the final Eurozone CPI figure, which could have an impact on the Euro and give the EUR/GBP cross some momentum. In addition, traders will rely on the BoE’s Quarterly Bulletin for information about the central bank’s assessment of the UK economy. This may also help to create chances for short-term trading before Catherine Mann’s scheduled speech as a member of the BoE MPC.

GBPJPY Analysis

GBPJPY has broken an Ascending channel in upside.

As the United Kingdom’s Office for National Statistics released higher-than-expected inflation figures, the GBPJPY pair spiked strongly to close to 167.37. The headline Consumer Price Index came in at 10.1%, above expectations of 9.8% but falling short of the previous release of 10.4%. It appears like UK inflation is just about to dip below the double-digit mark. The core CPI, which excludes the cost of food and oil, held unchanged at 6.2%, exceeding the consensus estimate of 6.0%. The Producer Price Index (PPI) data, which has weakened overall, shows that producers have reduced the cost of goods and services at factory gates as a result of a decline in petrol prices. This has diminished the credibility of Bank of England policymakers, who had been sure that February’s optimistic inflation was an anomaly and that inflation will swiftly go down starting next month.

The Three Month Labour Cost Index for Tuesday came in at 6.6%, which was higher than the consensus estimate of 6.2% but in line with the previous announcement. The unemployment rate increased from the consensus and the previous publication of 3.7% to 3.8%, further dampening the employment numbers. Additionally, Claimant Count Change exceeded 28K as the street expected a decline of 11.8K. BoE Governor Andrew Bailey would be compelled to hike rates further as a result of the combined effect of the unexpectedly positive labour cost index and the acceleration of inflation statistics. In regards to the Japanese Yen, new Bank of Japan Governor Kazuo Ueda stated in the Japanese parliament on Tuesday that “The BoJ is buying government debt as part of monetary policy” to support the extension of economic stimulus. He continued by saying that the purpose of buying bonds is not to monetize the national debt.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/