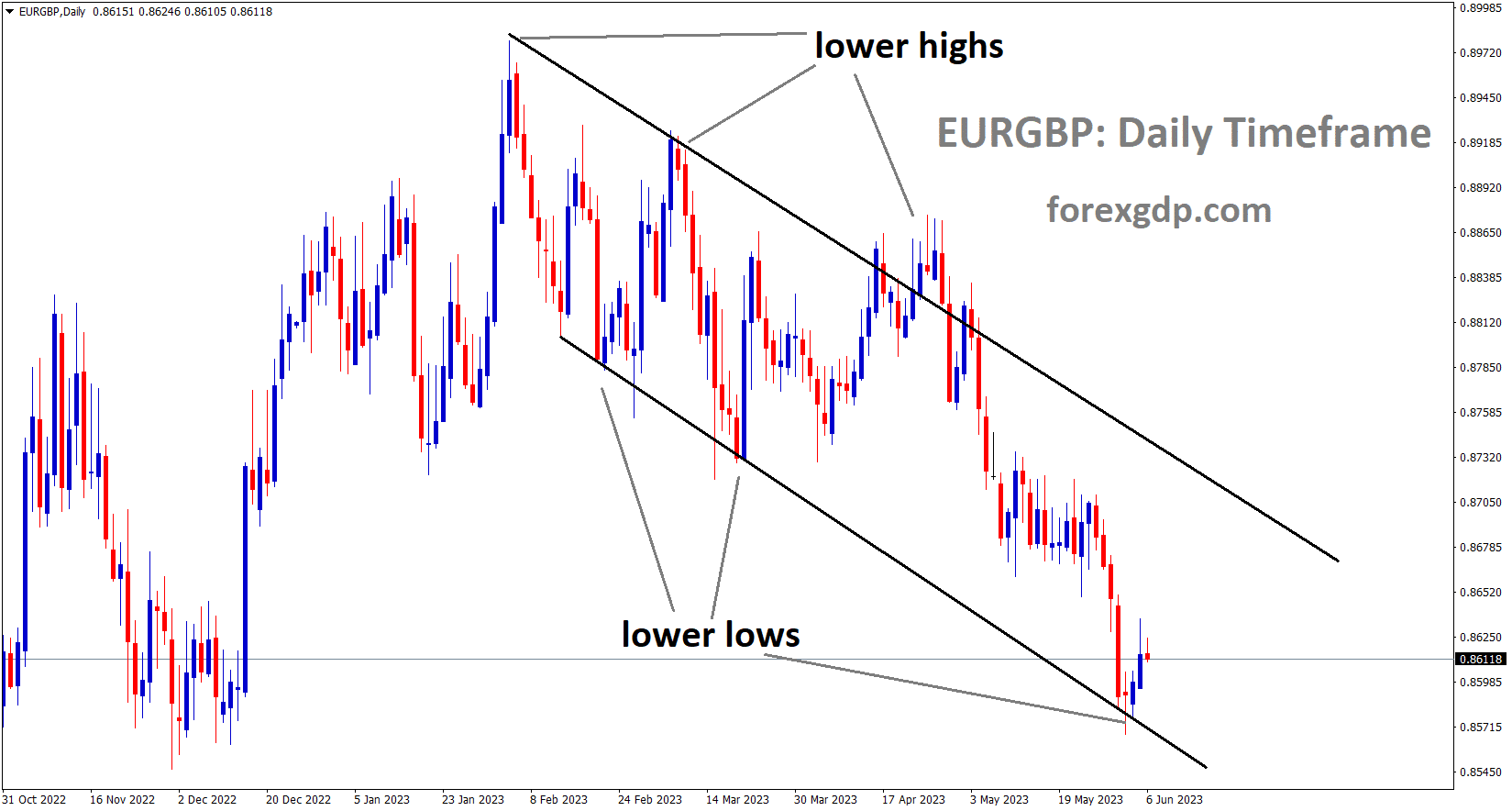

EURGBP Analysis

EURGBP is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

German exports increased in April compared to the previous March month’s decline. Lower orders for Germany are a result of Asia’s expanding manufacturing capabilities and China’s reduction in imports. Germany is the industrial economy’s growing centre in Europe, and its weakness when compared to other currencies is a problem.

The dollar regained control after a strong US jobs report and NFP print on Friday, pushing EURUSD back towards their weekly lows. Unexpectedly, though, the market expectations for the US Federal Reserve’s June meeting have actually been dovishly repriced, with the likelihood of a pause from the US Federal Reserve rising to 70%. The increasing unemployment rate, along with the fact that wages increased but are now beginning to show signs of slowing down, may be to blame for the dovish repricing. If one paid closer attention to the details, it was an interesting jobs report all in all.

We did receive some Euro Area data this morning, showing that German exports recovered from their March decline in April. With supply chain problems, China’s uneven recovery, and lower imports from China as the Asian region increases its production capabilities, which lowers its imports from countries like Germany, the German export sector continues to face a slew of challenges as it attempts to demonstrate a sustained recovery. This morning, the Sentix Economic Index was also released, showing a continued decline in the Euro Area as economic worries increase. German was identified in the report as the “problem child” of the Euro Area, with a rising likelihood that the most industrialised economy in Europe will experience a recession.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

In contrast to the US dollar, gold prices are rising, and the US debt ceiling limit has been raised for the upcoming two years. To increase money supply and pay for US Treasury bills, US Treasuries are currently selling government bonds. Therefore, the US dollar’s value relative to other currency pairs is lower. The US Dollar suffers from the FED’s 75% chance of pausing the rate hike at its meeting on June 14.

Gold is testing a series of recent lows that, if broken, would make the precious metal vulnerable to further declines as it continues Friday’s post-NFP sell-off. Despite a growing perception in the market that the Federal Reserve will not raise rates at this month’s FOMC meeting and will instead choose to pause and monitor incoming data over the coming weeks, the US dollar is still rising. The most recent CME Fed Fund probabilities indicate that the FOMC meeting on June 14 will be delayed. The market is pricing a 25 bp hike with a 22.4% probability and a pause with a 77.6% probability. Prior to one week, the market had a 35.8% chance of a pause and a 64.2% chance of a quarter-point increase priced in.

SILVER Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Now that the US debt ceiling issue is settled for the next two years, the US Treasury must restock its funds, which were critically low at the beginning of this month. In order to replenish the US Treasury General Account, the US Treasury is anticipated to sell a sizable amount of government bonds. This will not only reduce market dollar liquidity but will also cause yields along the US Treasury curve to increase as investors demand higher returns on their investments. The price of gold is being affected by this expectation of higher yields. As concerns about short-term yields increase, the price of gold is moving closer to a recent multi-week low at $1,932/oz. The price of the precious metal is still below the 20-, 50-, and 23.6% Fibonacci retracement levels. The big figure level of $1,900/oz is guarded below by the 38.2% Fibonacci level at $1,904/oz.

USD Index Analysis

US Dollar index is moving in an Ascending channel and the market has rebounded from the support area of the minor box pattern.

Data from the US ISM Services PMI survey show a reading of 50.3 in May, down from the previous reading of 51.9 and under the forecasted reading of 52.2. This reading provides evidence that the FOMC meeting on June 14th will pause interest rate increases.

Today’s Asian session saw the US Dollar hold steady after it fell following some weak data. Results from the ISM services PMI survey for May fell short of expectations, coming in at 50.3 as opposed to the 52.2 predicted and 51.9 prior. This seems to have given the market more hope that the Federal Open Market Committee meeting on June 14th will include a pause. Although APAC equities have seen somewhat lacklustre trading, Wall Street ended the cash session slightly lower, and Hong Kong’s Hang Seng Index managed some respectable gains. The RBA increased the cash rate by 25 basis points to 4.10% today. As interest rate markets had not anticipated the change, AUDUSD rose by half a cent immediately. At the same time, the ASX 200 fell by more than 1%. Even though the 1-year note is still trading at close to 23-year highs at about 5.25%, Treasury yields have hardly changed today.The front-month COMEX gold futures have been stable today above US$ 1,970 after bouncing off an ascending trend line support overnight.

Similar to how crude oil has calmed down following the Monday’s fireworks after OPEC+ cut its production target once more. While the Brent contract is close to US$ 76.50 bbl, the WTI futures contract is just under US$ 72 bbl.With markets acting as they do, volatility has decreased across a wide range of asset classes. This past week, the closely followed VIX index, which measures market-priced volatility on the S&P 500, fell to its lowest point since November 2021. Similar measures of volatility for bonds, currencies, commodities like oil and gold have fallen recently. Look at the graph below. More range trading scenarios might be possible if volatility is lower. The weekend’s resolution of the US debt ceiling debate may have contributed to the decrease in price fluctuations. Market attention may shift to the upcoming FOMC meeting, where the interest rate swaps and futures markets do not anticipate a hike. However, they have given a 25 basis point lift at the July meeting a probability of about 70%. Future data points may influence speculation regarding the rate path, which could lead to volatility spikes.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The QQE programme will continue, according to Bank of Japan Governor Ueda, until the 2% inflation target is met and sustained. Expectations of inflation are still low, so any changes will come gradually if wages and prices are difficult to raise. If no action is taken, inflation in Japan will increase until it reaches the 2% target.

According to central bank governor Kazuo Ueda, the Bank of Japan will continue QQE until the inflation target is met. Due to extended periods of zero inflation and deflation, inflation expectations have remained low. Both inflation and expectations of inflation are rising. The public’s tendency to behave in Japan under the presumption that wages and inflation will remain low is gradually changing. The deflationary mindset that wages and prices are difficult to rise is gradually changing. Inflation expectations would be at 2% when the inflation target is met.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Swiss inflation data for May month was published at 2.2%, which is in line with expectations and is less than the 2.6% printed for April month.

The SNB’s goal of 0-2% is still marginally higher than the current state of the economy. Another rate increase of between 25 and 50 basis points is anticipated for June. Inflation in Switzerland is lower than in other nations, and the Credit Suisse bank crisis has little impact on the financial stability of Swiss banks.

According to government data released on Monday, Swiss annual inflation decreased to 2.2% in May as anticipated. The Swiss National Bank is still anticipated to raise interest rates later this month. The Federal Statistics Office reported a year-over-year increase in consumer prices that was lower than the 2.6% rate in April and in line with the 2.2% forecast in a Refinitiv poll. Swiss headline inflation, while modest when compared to other nations—many of which have experienced double-digit price growth—has remained above the central bank’s target range of 0-2% since February 2022. The May CPI release will not have an impact on the persistently broad-based nature of inflationary pressures, according to Credit Suisse economist Maxime Botteron. In light of this, a rate increase by the SNB is very likely to occur in June, he added, adding that he anticipated the SNB to increase its policy rate by 50 basis points to 2% because inflation will likely continue to be above the threshold of price stability over the next few quarters.

Karsten Junius, an economist for J.Safra Sarasin, predicts a rate increase as well, but only by a more modest 25 basis points because the pressure from rising wages appeared to be only moderate. According to Junius, the second-round effects of the inflationary push from last year are not as severe as they are in most other nations. As a result, the SNB will not need to raise its key rates as quickly as it would in the euro zone. On Monday, the SNB declined to comment. Last week, Chairman Thomas Jordan expressed concerns about ingrained inflation, and Vice Chairman Martin Schlegel stated that the bank remained prepared to raise interest rates. The market currently anticipates a further 25 basis point increase from the current 1.5% level when the SNB makes its next assessment on June 22. The SNB has increased interest rates four times over the past year. Swiss prices rose 0.3% month over month, primarily due to rising rents and package vacation costs, according to the Federal Statistics Office. Vegetables also increased in price. The annual core inflation rate, which excludes volatile items like food and fuel, fell from 2.2% in April to 1.9%.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

From -0.20% expected and -1.7% in the previous reading, the NZD Commodity Price Index increased to 0.30%. The previous day, Reuters made Successful relationships that uphold US-Sino relations give the New Zealand dollar a boost against other currencies. By managing their differences appropriately and moving forward with a positive attitude, a US State Department official and the vice foreign minister of China had a productive conversation yesterday.

The Kiwi couple cheers upbeat domestic data, risk-positive news about US-China relations, as well as negative US data. The traders are currently on the risky floor due to a lack of significant data or events and a cautious attitude before the Reserve Bank of Australia Monetary Policy Meeting. Despite this, the ANZ Commodity Price Index for May in New Zealand increased past -1.7% previous readings and -0.2% anticipated figures to reach 0.3%. Additionally, early on Tuesday in Europe, Reuters published headlines suggesting an improvement in US-China relations by citing Chinese media. A senior US State Department official and China’s vice foreign minister had a frank, constructive, and fruitful communication on promoting Sino-US relations and properly managing differences, according to the news.

The International Monetary Fund’s Managing Director Kristalina Georgieva’s remarks to bolster market sentiment amid a light calendar and the Fed blackout period contrast with the largely negative US data. The sentiment is also prompted by worries about the need for US large banks to hold more capital to combat the housing crisis. However, the US ISM Services PMI fell to 50.3 in May from 51.5 expected and 51.9 previously, and factory order growth also slowed down, falling to 0.4% from 0.5% market expectations and 0.9% previously. It should be noted that the S&P Global Composite PMI and Services PMI final readings both indicated weaker results for May. Georgieva of the IMF, on the other hand, expressed worry about further rate increases by the Fed.

GBPCHF Analysis

GBPCHF is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern. In contrast to expectations of 53.9 and 55.1, the UK Final CIPS Services PMI and composite PMI data were positive at 54.0 and 55.2 respectively. UK BRC Retail sales growth decreased from 5.2% in April to 3.7% in May. Consumer spending in the UK increased by 3.6% YoY in May as higher food prices restrained usual spending. To prevent a recession in the UK in 2023, the Bank of England will need to hold the rate steady at its upcoming meeting.

The Cable pair both demonstrates the market’s apathy and fails to uplift the depressing US data amid conflicting concerns regarding the Bank of England’s next move. Market participants on Monday saw disappointing US statistics as well as improved UK S&P Global/CIPS PMI readings. However, before the recession problems and BoE indecision weighed on the Pound Sterling. However, the US ISM Services PMI dropped to 50.3 in May from 51.5 expected and 51.9 previously, and factory order growth also slowed down, falling to 0.4% from 0.5% market expectations and 0.9% previously. It should be noted that the S&P Global Composite PMI and Services PMI final readings both indicated weaker results for May.

On the other hand, final May UK S&P Global/CIPS Services PMI and Composite PMI readings improved to 54.0 and 55.2 from initial expectations of 53.9 and 55.1, respectively. In May, UK BRC Like-for-Like Retail Sales growth decreased from 5.2% to 3.7% YoY. In addition, the most recent Barclays survey notes that UK consumer spending increased 3.6% year over year in May despite higher food prices restricting discretionary spending. Following the release of the data, Reuters reported: “Recent data indicates previous BoE hikes are slowing the UK economy, which could reignite UK recession fears and pressure more MPC members to vote for steady rates to help jumpstart the economy, removing the primary stimulus sterling strength. In other places, US policymakers’ ability to prevent the debt-ceiling expiration contrasts with US hawkish bets on the Federal Reserve declining and worries about the need for the US large banks to hold more capital to combat the housing crisis.

AUDCAD Analysis

AUDCAD has broken the Descending channel in upside.

The 1 million barrels per day reduction in Saudi Arabia’s oil production that was announced yesterday causes less volatility in oil prices. Russia did not reduce its oil production, which is the concern for an increase in oil prices, and this is primarily due to improper coordination with OPEC+ members. Since oil is the main factor influencing Canadian exports, the Canadian Dollar is still weaker than other major currencies.

Over the past 24 hours, the Canadian Dollar has lost ground against the US Dollar. This is true despite recent developments involving crude oil. The most recent OPEC meeting ended over the weekend with Saudi Arabia reducing production by roughly 1 million barrels per day from July. The coalition’s failure to reach broad consensus regarding the necessity of reducing output in order to boost oil prices made the meeting somewhat unusual. Despite the fact that this news caused WTI to gap over 4% higher to start the trading week, the commodity quickly filled the gap and ended the session unchanged. Fundamentally speaking, crude oil still has a long way to go. The tightening of monetary policy globally is slowing down economic expansion. Recent manufacturing data from China showed disappointment in this area.

In light of this, it might be challenging for one country to support the market alone if there is insufficient comprehensive coordination among OPEC+ members. Since oil is a significant export from Canada and the USDCAD, this is important. Important repercussions for the economy, inflation, and the Bank of Canada could result from a significant departure from the commodity’s price trajectory. The Loonie may continue to pay attention to the unfolding narrative of where global growth is going in the interim. Aside from the Reserve Bank of Australia rate decision, the economic calendar for the next 24 hours is relatively light. However, USDCAD may continue to pay attention to market sentiment. A rather pessimistic Wall Street trading session may indicate that the currency will face future headwinds.

AUDCHF Analysis

AUDCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

After the RBA unexpectedly raised interest rates by 25 basis points from the previous reading of 3.85% to 4.10% today, the Australian dollar surged. The recent increase in wage prices prompts the RBA to consider raising rates at this meeting. A 2-3% inflation target was predicted by the RBA for mid-2025. The CPI for April was 6.8% for the month and 7.0% on a quarterly basis, both below the peak of 7.9%.

The Reserve Bank of Australia unexpectedly increased interest rates by 25 basis points and stated that additional tightening may be necessary in order to bring inflation back to its target. As a result, the Australian dollar surged. The minimum wage increase last week made it difficult for the RBA to maintain its benchmark cash rate at 3.85%. The benchmark rate was expected to reach 4.18% by September, with the market pricing in a roughly 30% chance of a rate increase of 25 basis points at today’s meeting. The odds showed a terminal rate of 4.26% as of the time of writing. According to the central bank, there are now more upside risks to the inflation outlook, and the board has adjusted as a result. It kept its hawkish slant, arguing that a further rise in interest rates will boost confidence that inflation will reach its target within a reasonable time frame.

After taking a break in April, the Australian central bank shocked the markets by raising rates last month. They also kept their hawkish stance in an effort to contain price pressures. The minimum wage increase may further delay Australia’s inflation from reaching the target level, necessitating higher interest rates. Australia’s inflation has already been running well above the target level. Only the top of the RBA’s 2-3% target range is expected to be reached by mid-2025; headline inflation increased 6.8% on-year in April and 7.0% in the first quarter, moderately slowing from a peak of 7.9%. The labour market has also been tight, with the unemployment rate circling near five-decade lows, but signs of moderation are starting to appear.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/