EURUSD Analysis

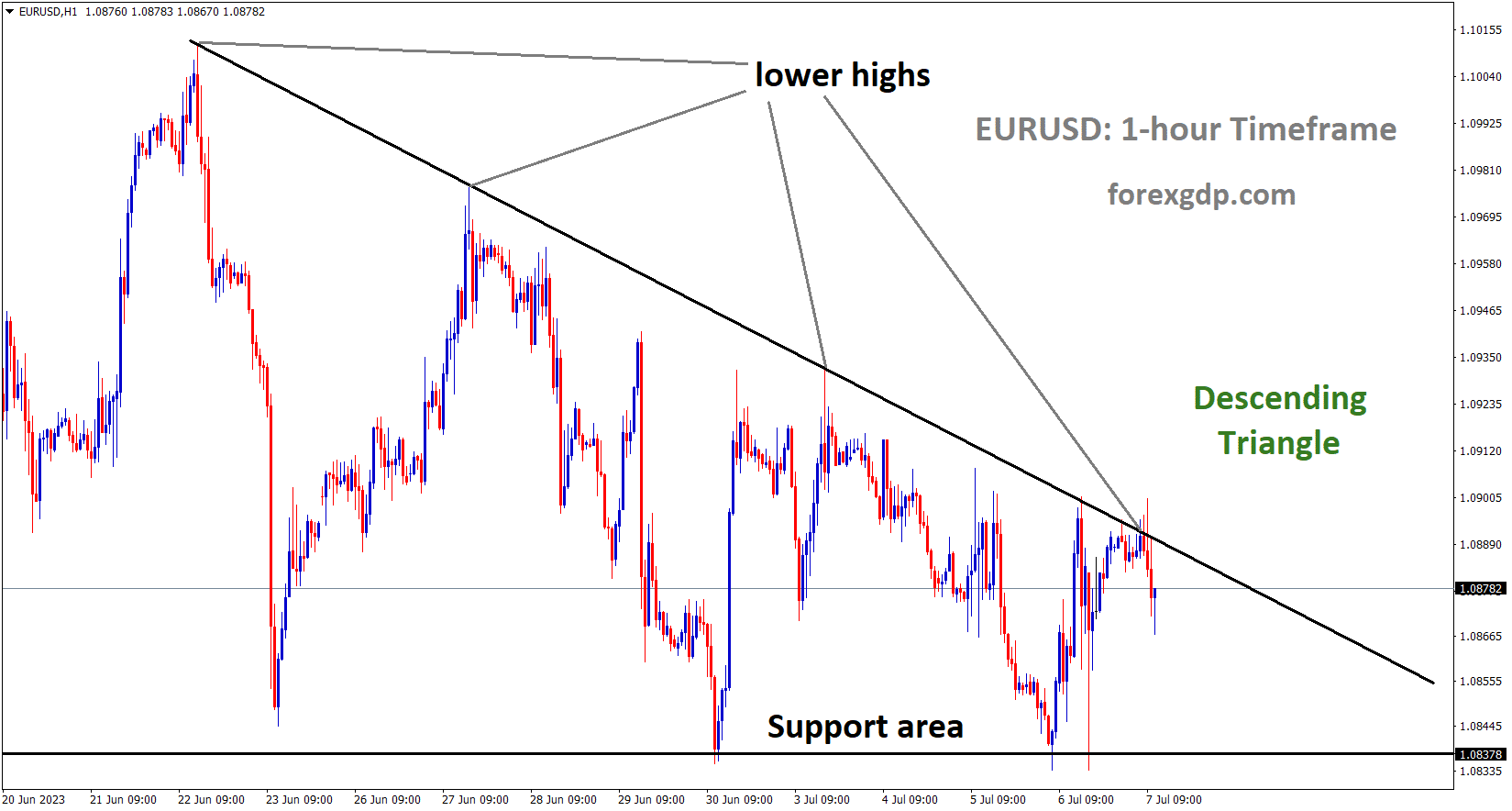

EURUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

Inflation in the Eurozone is declining, according to ECB President Christine Lagarde, but we still need price stability and more monetary policy changes to keep it under control in Europe.

We still have work to do to get inflation back down to our target, said Christine Lagarde, president of the European Central Bank, in an interview with La Provence on Friday. Maintaining price stability is a top priority. The rate of inflation has begun to drop. The initial effects of monetary policy decisions play a role in that. But we still need to work because inflation is still above the 2% target.

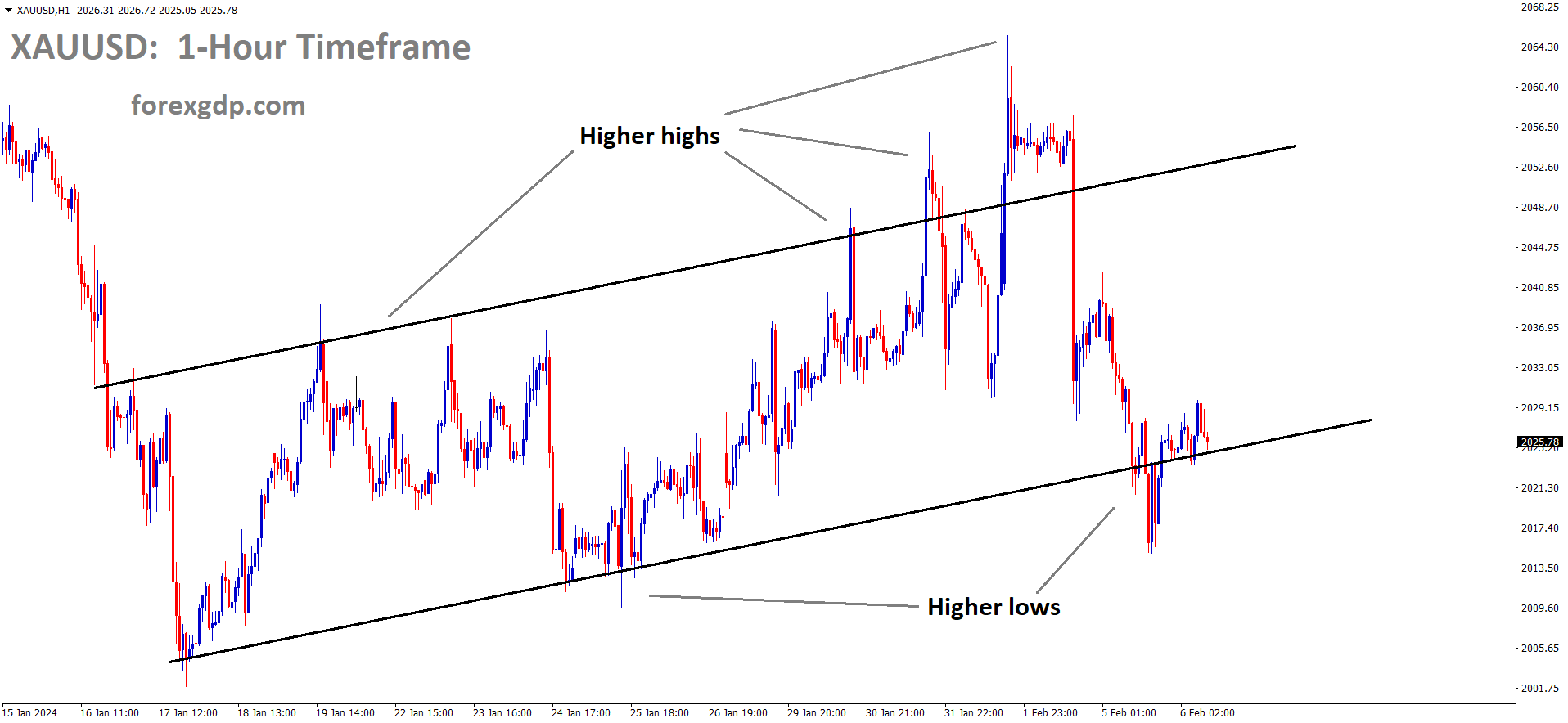

XAUUSD Analysis

XAUUSD Gold Price is moving in the Consolidation pattern and minor descending channel, market is rebounded from the lower low area and horizontal support area of the pattern.

Due to US domestic data printing at higher-than-anticipated numbers this week, gold prices are down. In June, 225,000 jobs were projected by US NFP data; if this number turns out to be significantly higher than expected, gold prices will this week be entirely driven by US domestic data.

Following a hawkish repricing of central bank monetary policy, gold prices were muted on Thursday and extended losses from the previous session. This was due to rising rates in the fixed-income market in both Europe and the United States. As U.S. yields staged a significant rally in late afternoon trading, the 2-year note rocketed past 5.0% and the 10-year note pushed above 4.0%, the former reaching its highest level since 2007 and the latter matching its March peak in the wake of strong U.S. economic reports. XAU/USD was down about 0.3% to $1,910 at the time. Payroll processing company ADP reports that private sector headcount increased significantly in June, causing U.S. businesses to add nearly 500,000 workers, more than double the median projection in a Bloomberg News poll.

XAGUSD Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The ADP survey offers useful information about the labour market, which currently appears to be in excellent health and firing on all cylinders despite the increasingly restrictive monetary policy environment, despite the fact that it has a poor correlation with national employment data. When the U.S. government releases the June nonfarm payrolls (NFP) report on Friday, we will learn more details about the general hiring trend. According to estimates, the U.S. economy added 225,000 jobs last month, which helped lower the unemployment rate from 3.7% to 3.6%. Since the Wall Street consensus has consistently underestimated job growth for 13 months in a row, it would not be shocking to see tomorrow’s headline NFP number come in hotter than expected. If this scenario comes to pass, rate expectations may continue to shift in favour of the hawks, making the market unfavourable for non-yielding assets like gold.

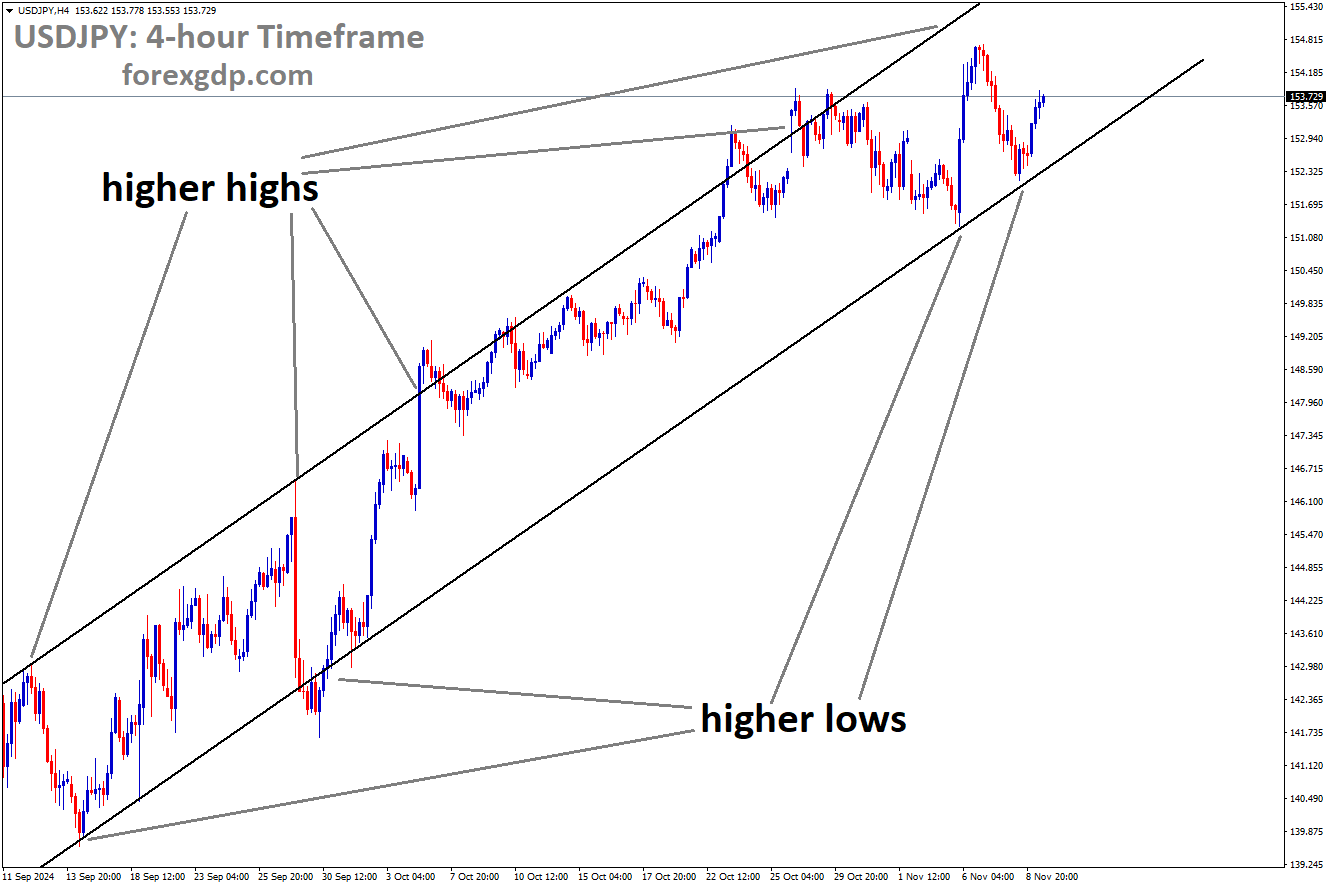

USDJPY Analysis

USDJPY has broken the Box pattern in downside.

In May, Japanese workers’ wages increased by 2.5% compared to the expected 1.2% and 1.0% in April. The Yen’s strength and the Bank of Japan’s holding rates and monetary policies are both benefited by this news.

After Japanese wages increased significantly more than anticipated, the Japanese yen found some buyers, making it easier for the Bank of Japan to alter its ultra-loose monetary policy. As a result of the major labour unions’ wage negotiations this spring, which led to the largest pay increase in decades, Japanese workers’ wages increased by 2.5% in May compared to the expected 1.2% increase and 1.0% increase in April. The BOJ is unlikely to change its policy this year, but some analysts anticipate changes to the yield curve control (YCC) policy later this month. The global economy’s continued resilience and the pressure it puts on bond yields to rise could lead to a change in the YCC policy. A credit crunch could result from an overly tightening of financial conditions, putting strain on the financial system and necessitating an easing of monetary policy. One board member was quoted in the BOJ summary of viewpoints from the June policy meeting as saying that the central bank should discuss modifying YCC to enhance market function and reduce its high cost.

Earlier this month, the BOJ maintained its ultra-loose policy settings, particularly the closely watched YCC policy, in an effort to support the fledgling economic recovery and sustainably meet its inflation target. The central bank will ‘patiently’ maintain the current policy, according to BOJ Governor Kazuo Ueda, because there is still some work to be done in order to stably and sustainably achieve its 2% inflation target. The USDJPY recently touched 145.00, close to the level that precipitated an intervention last year for the first time in more than 20 years, and the market is still on high alert for a possible intervention by the Japanese government. Top Japanese officials have stated that no options have been disregarded.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Due to improved US domestic data and rising US demand, oil prices increased. A rate hike in the US could cause the Canadian dollar to decline in 2023, and the Bank of Canada’s table shows more rate pauses. The Canadian economy’s employment report is due out today, and the Canadian dollar is expected to move in that direction as a result.

Following the release of positive US domestic data yesterday, the Australian Dollar fell. The RBA paused rate hike earlier this week, which was bad for the AUD.

The USDCAD pair crosses into a bullish consolidation phase and trades within a constrained range, just below the high point since June 13 reached on Friday during the Asian session. Trading participants are anxiously awaiting the publication of the critical monthly employment data from the US and Canada. Spot prices are currently circling between 1.3360 and 1.3365, almost unchanged for the day. However, it is more likely that the closely anticipated US NFP report will overshadow the Canadian jobs data, which could have an impact on the Federal Reserve’s outlook for policy and boost demand for the US Dollar. The USD bulls are on guard in the meantime due to the uncertainty surrounding the Fed’s path for future rate hikes. In addition, the recent rise in crude oil prices is thought to be supporting the commodity-linked Loonie and acting as a drag on the USDCAD pair. The June FOMC meeting minutes, which were released on Wednesday, showed that almost all members favoured starting rate hikes again because inflation is still too high. Furthermore, bets for a 25 bps lift-off at the July FOMC meeting were reiterated by Thursday’s positive US ADP report and the ISM Services PMI. However, the Prices Paid sub-component of the ISM survey dropped to a more than two-year low and stoked rumours that the Fed would soon abandon its hawkish stance.

USD Index Analysis

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel.

This reading gives the US Dollar significant strength against other currencies. The US ISM Services Purchasing Managers index reached its highest reading in four months, coming in at 53.9 versus 51 Forecasted, according to the US ADP Report, which shows 497000 jobs added in June versus 228000 jobs expected.

Wall Street did not react favourably yesterday to the persistent prices in the services sector and the resilient labour market conditions, as the overnight data called for a hawkish bias in Federal Reserve Fed policy. The US ISM services purchasing managers index PMI data came in at its highest reading in four months 53.9 versus 51 forecast, which was the result of a significant beat in the US ADP report 497,000 versus 228,000 forecast. A new expansion in the services PMI employment index 53.1 versus 49.9 forecast added support to the still strong labour demand. The Fed has previously expressed concern about the inflation of services, so the persistence of services prices from the ISM data 54.1 versus 53.3 forecast posed an additional challenge to the rate of inflation progress. Due to recent resistance to rate cuts from January to May of next year, the overall data caused a sharp increase in US Treasury yields. Notably, the 10-year US Treasury yield has surpassed 4% for the first time since March of this year.

Even though the ADP has historically not been a reliable indicator of the US non-farm payroll, some indications of a robust labour market increase the likelihood of a stronger US jobs report today. With a notable reacceleration seen over the past two months, the US job report has outperformed market expectations on 11 out of 12 occasions in the past year. According to projections, there will be an increase of 200,000 in June while the unemployment rate stays the same at 3.7%. Another set of readings that are better than anticipated may boost expectations for a soft landing, but they may also put pressure on the Fed to take additional action as it keeps an eye on the wage inflation rate. For the time being, the S&P 500 has encountered some resistance at the upper trendline of an ascending channel pattern, and lower highs on the daily RSI indicate that upward momentum is moderating. The Fear and Greed Index returned to “extreme greed” territory late last week, which may be a sign of short-term overcrowded sentiments. However, seasonality in July still favours the continuation of the upward trend, so any formation of a higher low should be closely watched. For the time being, more downward movement is likely to lead to the formation of a double-top pattern, with the 4,330 level acting as the critical neckline that the bulls must hold.

US Treasury Secretary Janet Yellen stated on Friday that China’s new export controls on essential minerals have the US concerned and that they are still assessing the impact during her four-day visit to Beijing. At the senior level, open lines of communication are in both the US and China’s best interests. China would benefit from a shift towards market reforms because earlier reforms sparked explosive growth. The US wants to ‘diversify’ rather than completely decouple its economies. Particularly uneasy about China’s use of punitive measures against American businesses. The US will work with allies to address China’s unfair economic practises in order to create a level playing field for US businesses.

AUDCAD Analysis

AUDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

While this is going on, the price of crude oil remains stable near the two-week high it reached on Thursday. This is due in large part to the US inventories dropping more than expected last week, which indicated strong refining demand. This comes after the two largest oil exporters, Saudi Arabia and Russia, announced new output cuts for August, which continues to support the dark liquid. However, concerns about a worsening global economic downturn, especially in China, could limit gains. Furthermore, the likelihood of further Fed interest rate increases continues to be favourable for high US Treasury bond yields, which is seen as a positive for the USD and should help support the USDCAD pair. In fact, while the benchmark 10-year US Treasury yield is maintaining its position above the 4.0% level, the yield on the two-year US government bond, which typically moves in tandem with expectations for interest rates, is close to its highest level since June 2007. However, the USDCAD pair is still expected to end the week in the black for the second time in a row, and the aforementioned fundamental backdrop is in the USD bulls’ favour. Despite this, it will still be wise to hold off on positioning for a continuation of the recent strong recovery from the 1.3115 region, or the lowest level since September 2022, which was reached last Tuesday.

GBPUSD Analysis

GBPUSD is moving in an Ascending Channel and the market has rebounded from the higher low area of the channel.

The Bank of England Governor Bailey’s speech yesterday caused the GBP to decline against the USD. The overcharging of customers must stop, according to Governor Bailey, or prices must be reduced for consumer purchases. In the coming days, borrowers will experience greater suffering, so the Bank of England must work hard to support lower inflation. Additionally, UK Prime Minister Rishi Sunak expressed confidence in the UK economy’s price stability and the impending decline of inflation.

The headlines that Bank of England BoE Governor Andrew Bailey had urged industry regulators not to overcharge customers caused the Pound Sterling GBP to lose half of its gains. The GBPUSD pair has reached a new two-week high at 1.2775 as a result of BoE Bailey’s optimism that regulatory actions will help to reduce inflationary pressures. Although borrowers would suffer serious consequences and the timing of the rate cut is uncertain, Andrew Bailey is confident that stubborn inflation will decline. The BoE has been acting decisively to improve financial conditions. Because of anticipated worsening labour shortages, inflation in the United Kingdom appears poised to accelerate once more. Rishi Sunk, the prime minister of the United Kingdom, expressed optimism about price stability this week. This week, Rishi Sunak, the prime minister of the United Kingdom, pledged to make full use of monetary and fiscal policy to combat persistent inflation. Inflationary pressures are persisting longer than anticipated, according to UK Sunak, but that does not mean the current policy measures are ineffective. The British government has declared its intention to contribute 11.6 billion pounds to global climate finance.

Businesses are increasing their investments in Germany to make up for the lengthy bureaucracy and delays at the border brought on by Britain’s exit from the EU. According to the Financial Times, the Bank of England intends to talk with foreign banks about establishing subsidiaries.

The UK economy is experiencing higher inflationary pressures due to labour shortages and food price inflation that is at a 45-year high. As nearly one in three female workers are anticipated to consider early retirement due to health issues, labour shortages are predicted to worsen. According to Reuters, UK Finance Minister Jeremy Hunt endorsed the Financial Conduct Authority’s FCA efforts to ensure banks are providing customers with better savings rates. The UK’s June Services PMI came in at 53.7, in line with expectations. Consumer inflation expectations for the next year increased from 4.7% in May to 5.0% in June, according to a monthly survey conducted by Citi Bank and the polling company YouGov.

Markets believe that the BoE will eventually increase interest rates from their current level of 5% to 6.25%. The risk profile is improving as interest in risk-sensitive assets increases. Investor caution ahead of Automatic Data Processing ADP Employment and Services PMI data has caused the US Dollar Index DXY to decline after hitting a new four-day high at 103.40. The US ADP report is anticipated to show 228K new hires, down from the previous addition of 278K.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

SNB revised its inflation forecast upward in 2024 and 2025, to 2.2% and 2.1%, respectively, after lowering it in 2023 to 2.2% from 2.6%. The Swiss Franc performs well against counter pairs as a result of SNB actions.

The SNB’s rhetoric reveals ongoing worries about price stability. We believe that part of the SNB’s hawkish rhetoric is an effort to eliminate any perception of divergence that might encourage CHF weakness. At this point, a further rate increase of 25 basis points in September seems more probable than not. The SNB’s policy rate would enter positive territory in real terms if another rate hike were to occur with core CPI remaining unchanged at the current rate (1.9%) or lower, joining the RBNZ, Fed, and BoC. The SNB increased its forecasts for 2024 and 2025 by 0.2% and 0.1%, respectively, but decreased its forecast for inflation this year from 2.6% to 2.2%. This demonstrates the SNB’s bias towards tightening even more, which will support CHF.

NZDUSD Analysis

NZDUSD has broken the Descending channel in upside.

Investors are concerned about the RBNZ’s actions of multiple rate increases, which will have a greater impact on the economy and have already caused a technical recession. Both the 1Q2023 and the 4Q2023 results fell far short of the predicted 0.30% positive growth.

In the London session, the NZDUSD pair reached a new two-week high of 0.6215. The US Dollar Index DXY has experienced extreme weakness, and the Kiwi asset has gained significantly. Investor caution has increased ahead of the Employment and Services PMI data, which has caused the USD Index to crash sharply to close to 103.10. The S&P500 futures sell-off has continued as investors stay away ahead of the second-quarter results season. In light of rising interest rates and strict credit standards set by commercial banks, it is anticipated that corporate earnings will remain uncertain. The minutes of the Federal Open Market Committee FOMC were made public, and it became clear that policymakers were concerned about the economy’s potential impact on economic activity, hiring, and inflation from tighter credit conditions, including higher interest rates for households and businesses.

Future US Nonfarm Payrolls NFP data will be closely scrutinised. Compared to the previous release of 3.7%, the unemployment rate is predicted to fall to 3.6%. While the June Nonfarm Payrolls NFP report is anticipated to show 225K new payrolls compared to the 339K addition in May. The monthly average hourly wage is seen to be stable at 0.3%. But before that, attention will remain on the US ISM Services PMI. In contrast to factory activities, the US Services PMI is expanding. Compared to the previous release of 50.3, the economic data has increased to 51.0. New Orders Index, which had previously been 56.2, is now down to 53.3.

Investors in the New Zealand Dollar are concerned that further interest rate increases from the Reserve Bank of New Zealand RBNZ could scuttle the country’s economic prospects. According to economists at UOB, New Zealand has entered a technical recession as a result of the economy contracting by 0.1% qq in 1Q23 as opposed to the previously reported 0.7% qq decline in 4Q22 -0.6% qq. The result fell significantly short of the Reserve Bank of New Zealand’s RBNZ forecast of 0.3% growth.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/