EURJPY Analysis

EURJPY is moving in the Box pattern and the market has reached the support area of the pattern.

Jibun Bank Services PMI for Japan was 52.1 in June compared to 54.2 the month prior, supporting the Dovish stance of the Bank of Japan.Yesterday, in anticipation of the FOMC meeting minutes, US 10-year Treasury Bond yields increased.

In other news, dismal readings of China’s Caixin Services PMI for June, to 53.9 from 57.1 the month before, add to rising concerns about US-China tension amid new Beijing warnings of additional trade restrictions. The same enables yields to continue to be firmer while also jabbing Euro bulls. It should be noted that the EURJPY bears remain optimistic despite the negative German data and scepticism regarding the ECB’s hawkish signals. In contrast, Japan’s Jibun Bank Services PMI eased to 52.1 in June from 54.2 the month before and supports the Bank of Japan’s (BoJ) dovish stance, which in turn supports the upward movement of the EURJPY. The key to predicting near-term movements in the EUR/JPY will be new information regarding the Japanese government’s market intervention to defend the Yen. The Eurozone Producer Price Index (PPI) for May and news stories pertaining to the major risk factors, such as the US-China disputes and the recession difficulties, will also be crucial.

XAUUSD Analysis

XAUUSD Gold Price has broken the Descending channel in upside.

Following the fears of a trade war between the US and China, gold prices are slightly higher relative to the US. Commodity prices are rising as Russia reduces its oil production, and demand for gold is slightly rising as a result of China adding more stimulus to its economy.

With the US on vacation, markets seem a little lacklustre going into Tuesday’s trading session, but the price of gold has stabilised. As of last week’s end, Treasury yields were still up, with the benchmark 10-year bond trading at about 3.85%. As markets wait for Wednesday’s release of the minutes from the Fed meeting, the policy-sensitive 2-year note has risen back above 4.90%. After Beijing announced restrictions on the export of gallium and germanium, further hopes of a thawing of tensions between the US and China were dashed. The metals are essential for electric vehicles, semiconductors, and telecommunications. This action seems to be in retaliation for the US pushing chip restrictions on China. Before this week’s OPEC+ meeting in Vienna, Saudi Arabia and Russia pledged to extend their production cuts, which helped the price of crude oil rise. While the Brent contract is getting close to US$ 75 bbl, the WTI futures contract is fluctuating around US$ 70 bbl. Here are the current prices.

XAGUSD Analysis

XAGUSD Silver Price is moving in the Consolidation pattern and the market has fallen from the resistance area of the pattern.

The cash rate target remains at 4.10% as the RBA paused its cycle of rate increases today. As a result of the news, the ASX 200 gained stability while the AUDUSD declined. The Nikkei 225 equity index of Japan fell, and the USD/JPY moved slightly lower. Other APAC stocks have been relatively quiet today. Despite yesterday’s hawkish remarks from Joachim Nagel, President of the Bundesbank and policymaker for the European Central Bank (ECB), EURUSD has not moved much so far today. Today, Yannis Stournaras and Mr. Nagel, another member of the ECB Governing Council, will both make additional remarks. On Friday, Christine Lagarde, president of the ECB, will speak.

USDJPY Analysis

USDJPY is moving in the Box Pattern and the market has reached the support area of the pattern.

As it recovers from the previous day’s losses going into Wednesday’s European session, EURJPY posts modest gains around 157.35–157.40. The cross-currency pair does this while tracking the optimistic US Treasury bond yields amid concerns about the economy slowing down and rumours about Japan interfering to defend the Yen. The policymakers have been vocal in order to signal that they can intervene in the markets and protect domestic interests ever since the Japanese Yen (JPY) renewed its annual top in the previous week. Among them, Masato Kanda, Japan’s top currency diplomat, and Shunichi Suzuki, the country’s finance minister, draw a lot of attention. However, nothing significant has been reported thus far, leaving the Japanese yen open to further decline. On the other hand, the gap between the yields on two-day US Treasury bonds and those on 10-year bonds widened to its widest in 42 years on Monday, signalling recession fears. This in turn prodded sentiment and encouraged EUR/JPY buyers because the Yen appeared to be in heaven. However, the US 10-year and 2-year Treasury bond yields continue to rise, reaching nearly 3.86% and 4.92% by the time of publication, respectively, while the S&P00 Futures show only slight losses.

USD index Analysis

USD index is moving in the Descending channel and the market has reached the lower high area of the channel.

Following yesterday’s US Independence Day holiday, markets are currently moving quickly in advance of the FOMC meeting minutes scheduled for today. As retaliation for the US restricting chips and cloud computing services to China, China is now restricting semiconductors to the US. Today, Janet Yellen, the US Treasury Secretary, is gathering in Beijing to discuss how to resolve this tit-for-tat problem.

Due to the US markets being closed for the Fourth of July holiday, the risk environment was met with a more sombre tone and a lack of significant economic data. While US equity futures are also on some wait-and-see trading at the time of writing, European markets were flat to slightly lower on a thinly traded session. The minutes of the Federal Open Market Committee will be today’s market focus. The upcoming minutes will attempt to provide more clarity on policymakers’ perspectives on that guidance in light of the higher terminal rate forecasts made at its previous meeting. Even so, the minutes might be seen as a little dated in light of recent positive economic surprises and a core PCE inflation rate that was released after the Fed meeting that was softer than anticipated. Previous hawkish Fedspeak has not changed market rate expectations either, so it might take much more from the Fed minutes to persuade markets of a more hawkish outlook.

Since November of last year, the DJIA has primarily traded in a long-ranging pattern. Now, the index is returning to retest the upper edge of the consolidation zone at the 34,500 level. Since late-2022, numerous attempts to break through this level have been unsuccessful, making it a crucial level of resistance to monitor. It has also been accompanied by recent lower highs on the daily Relative Strength Index (RSI). The Nasdaq Composite has increased by 33% year to date, far outpacing the DJIA, which is more value-oriented. A break above this level may be required to increase confidence in further catch-up performance in value stocks as talk of the risk rally becomes more widespread. Any breakthrough above the 34,500 level may open the door for a subsequent retest of the high from April 2022.

According to a report by the Wall Street Journal, the US plans to limit Chinese access to US cloud computing services as a response to China’s decision to restrict key materials for the production of semiconductors. Recent actions from both sides appear to be a display of their tough stance in the bilateral relationship, possibly to highlight their competitive advantage to gain leverage in any discussions, ahead of US Treasury Secretary Janet Yellen’s visit to Beijing this week. The visit is resolution or lack thereof might be the subject of some attention the following week. China’s services Purchasing Managers Index (PMI) reading will be closely watched today in order to shed light on the progress of the nation’s consumption-led economic recovery. The reading has exceeded expectations five out of the last six times since the year began, which, if the trend holds, could provide some short-term relief for Chinese equities. A hawkish pause was the key finding from the most recent Reserve Bank of Australia (RBA) meeting, which caused the AUDJPY to tick marginally higher and retest the 96.84 level of resistance. This comes after a bounce off a trendline in the upward direction at a level of 95.34, which also served as a horizontal resistance that later turned into support. Any move above the 96.84 level could point the way to a retest of the year-to-date high, then the 98.75 level, as the market has been trading on higher highs and higher lows since March of this year.

EURCAD Analysis

EURCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Commodity currency pairs like the AUD, NZD, and CAD are supported by rising commodity prices. Crude oil prices have recently increased due to supply cuts from Russia and Saudi Arabia; this could help the Canadian dollar.

The strengthening of risk appetite in the midst of robust global growth, indications of a turnaround in commodity prices, and expectations of additional Chinese stimulus points to further gains for the Canadian dollar against the US dollar as it rises above key resistance. The Bloomberg Industrial Metals index appears to have found a floor, while commodity prices (as measured by the Bloomberg Commodity Total Return Index) sharply recovered in the week ending June 16. Commodity-sensitive currencies, such as the Canadian, Australian, and New Zealand dollars, have benefited from the recovery in commodity prices. Investor confidence in risky assets, particularly technology stocks, has increased as a result of the raising of the US debt ceiling, easing stress in the banking and financial sector, resilience in global growth, and expectations that global interest rates are peaking.

Furthermore, China cut a few key policy rates in the past week, raising hopes for additional stimulus to support the shaky economic recovery in the coming months, just as global central banks were reaching a turning point in the cycle of hikes. According to media reports, Beijing is considering issuing special treasury bonds worth about one trillion yuan to aid financially strapped local governments and increase business confidence. Stretched speculative short CAD positioning does, however, leave room for the possibility of unwinding some of those positions, particularly in the absence of a sharp decline in global growth.

EURCHF Analysis

EURCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In contrast to the FED, the ECB will need to hold rates steady at upcoming meetings because domestic data for the Euro region came in weaker than anticipated. Germany has already recorded two consecutive quarters of negative data, and May month data for the Euro CPI were lower than anticipated. Rate increases by the ECB have an effect on households and businesses and are reflected in domestic data numbers.

The policymakers of the European Central Bank ECB adopted a more hawkish stance, stating that they anticipate raising rates again at both the July and September meetings. In addition, ECB President Lagarde noted that inflation has changed and may continue for some time, and she added that it is unlikely that they will be able to say with certainty that interest rates have peaked anytime soon.

The Producer Price Index PPI and final Services PMI data for the Euro Zone may not do much to spur the market, suggesting that spot prices may continue the range-bound price action seen over the previous few days.

Due to the greater price changes that occurred before and after Credit Suisse acquired UBS, its shareholders proposed legal action against the company. These lower share prices must be made up for with real rate changes, according to the shareholders’ proposal.

A class action lawsuit seeking a better price from UBS for its takeover of its cross-town rival has the support of a Swiss proxy adviser representing some former Credit Suisse shareholders, it was announced on Tuesday. The Lausanne-based legal start-up LegalPass has decided to support [its] legal action against the exchange ratio set in the context of the acquisition of Credit Suisse by UBS, the Ethos Foundation, which represents a Swiss pension fund that owned more than 3% of Credit Suisse, said in a statement. According to the agreement, which was finalised last month, shareholders of Credit Suisse were offered one UBS share for 22.48 Credit Suisse shares, valuing the troubled bank at 3.35 billion Swiss francs. According to Ethos, Credit Suisse had a value of 7 billion francs just 48 hours prior to the deal being signed. According to Ethos CEO Vincent Kaufmann, the exchange ratio was really not in the best interest of Credit Suisse’s shareholders and that there is room to improve it. If adopted, the new exchange ratio would be advantageous to all Credit Suisse shareholders, according to the statement.

The case is the most recent court battle brought on by the emergency takeover, and it includes compensation claims from holders of Credit Suisse’s Additional Tier 1 bonds, which were all written down to zero. A class action lawsuit has also been brought by a group of Credit Suisse AT1 bondholders accusing former bank executives, including three previous CEOs, of being to blame for the bank’s failure. According to LegalPass, the claim is based on the Swiss mergers act, which permits the verification of the exchange ratio and allows shareholders to demand adequate compensation for their shares. The goal is to make it possible for shareholders to receive monetary compensation for the value difference between the share price set forth in the merger contract and the price established by the court. Ethos has previously expressed dissatisfaction with the way in which UBS acquired Credit Suisse, particularly the fact that the transaction was pushed through without consulting shareholders. The only way to contest the exchange ratio now that FINMA the Swiss financial regulator has decided to remove shareholders’ voting rights is in court, which is what LegalPass intends to do, Kaufmann continued. UBS declined to respond to inquiries about the lawsuit, which will be presented to a Zurich court. LegalPass first made the claim last month, claiming that UBS’s acquisition of Credit Suisse, Switzerland’s second-largest bank, was a steal based on a UBS document that valued the company at close to $34 billion. Credit Suisse was sold below its market price during secret negotiations and under governmental pressure, all without shareholders having any say in that matter, claimed Alexandre Osti, an attorney with LegalPass.

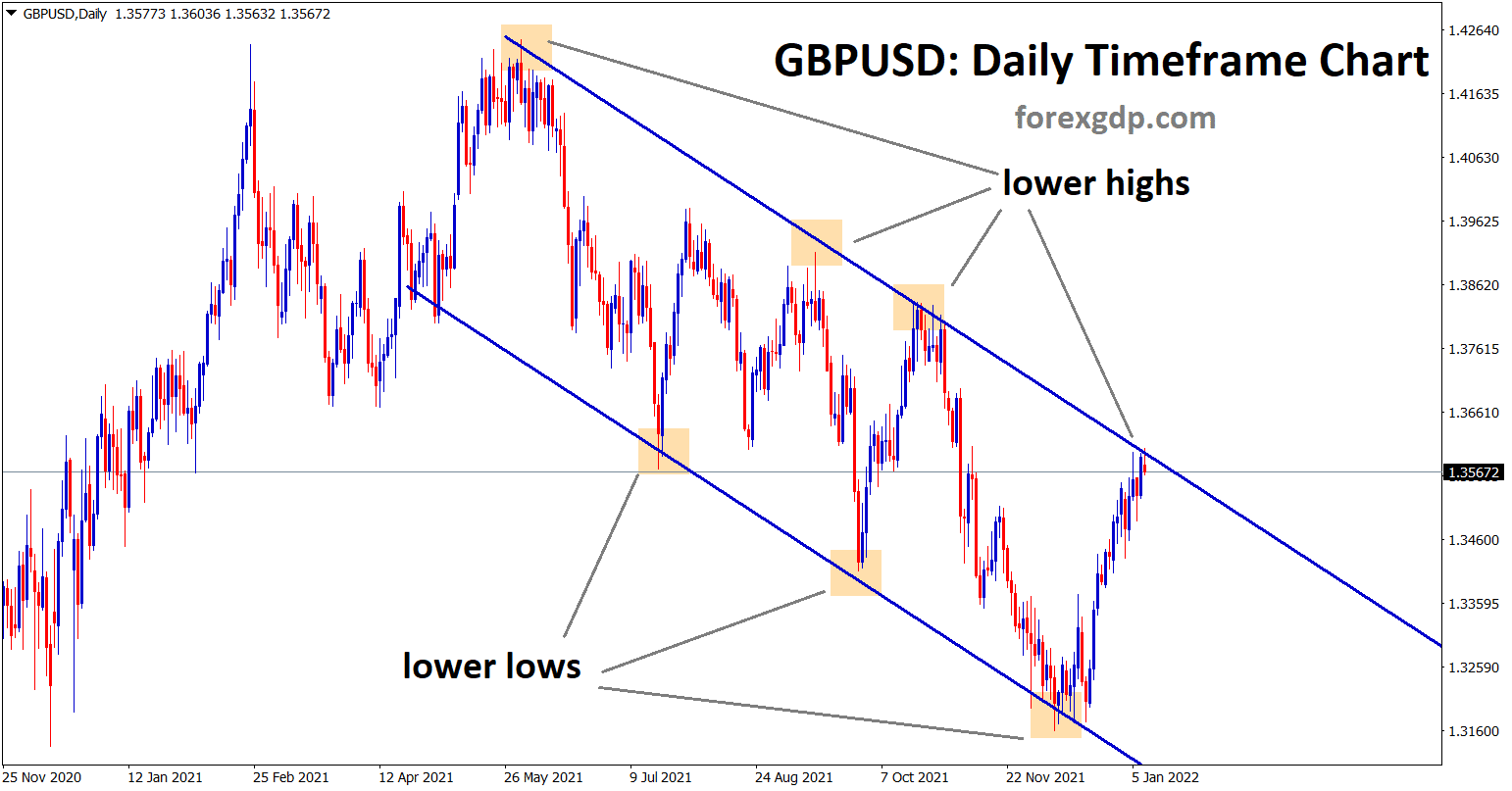

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

In the Hiking cycle of interest rate decisions, the Bank of England is more incensed than the ECB. The Euro region is not completely at peace with the UK’s low inflation reading. The inflation reading in the Eurozone appears to be slowing down because Germany has already entered a recession, but in the UK, employment and wages are rising along with inflation.

Even before the 50bps surprise delivered on June 22, the Great British Pound has been on fire recently. Recently, the Euro has experienced something of a renaissance, and as a result, EURGBP has risen; at the time of writing, the pair is trading near 0.8593. Following a record-breaking inflation reading in May, the Bank of England (BoE) has seen an increase in the likelihood of raising interest rates. On the other hand, the European Central Bank (ECB) has persisted in using hawkish language despite appearing to lose some steam as long as the economy is still a concern. I do anticipate the UK and its rate hike path to be more realistic than that of the ECB given that the UK economy is outperforming expectations, as stated by both Chancellor Hunt and PM Sunak following the June BoE meeting. Another indication that the BoE might need to be more aggressive than the ECB going into Q3 is the fact that UK inflation is still higher than that of the Euro Area.

Inflation in the UK is proving to be more persistent than anticipated, according to British Prime Minister Rishi Sunak, who also noted that the country is employing the proper tools to combat it. Whether it is monetary policy, sensible fiscal policy, or supply side reform, Sunak said, according to Reuters, that is the right toolkit to use when trying to bring inflation down.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to the New Zealand Institute of Economic Research, the Q2 business opinion survey result was -63.0%, down from the previous reading of -66.0. This report demonstrates that demand is decreasing and that the labour market for unskilled workers is more challenging than the survey indicates.

As traders from the United States US are still on vacation in observance of Independence Day, NZDUSD rises during a quiet North American session. However, the Reserve Bank of Australia’s RBA hawkish stance and the softening tone of the dollar helped to boost the NZDUSD. After reaching a daily low of 0.6140, the NZDUSD is trading at 0.6197, up 0.75%.Markets are still shut. After Durable Good Orders, Retail Sales, and Gross Domestic Product GDP for Q1 final reading justified the Federal Reserve’s Fed need for higher rates, the most recent round of US economic data painted an uncertain economic outlook. However, as concerns about a recession grew, a soft reading on the Fed’s preferred inflation gauge that was released on Friday along with a contractionary ISM Manufacturing PMI increased the likelihood of a hard landing. The New Zealand Institute of Economic Research’s quarterly survey of business opinion QSBO, which was conducted during the Asian session, showed an improvement in Q2 to -63.0% from -66.0 the previous quarter. The report noted that capacity utilisation among manufacturers and builders fell as demand weakened. Employers reported having trouble finding workers, particularly unskilled ones.

The New Zealand Dollar NZD was supported against the US Dollar USD as a result of this, along with the Reserve Bank of Australia’s RBA June monetary policy decision to maintain rates while tilting hawkish. The US Dollar Index DXY, which measures the value of the dollar in relation to a group of rival currencies, has partially given back Monday’s gains and is now down 0.02% at 102.941. US Treasury bond yields are increasing in the short term of the curve, while 20s and 30s print negligible losses.

AUDCHF Analysis

AUDCHF has broken the Descending channel in upside.

China’s Caixin Manufacturing PMI decreased to 50.5 in June from 50.9 in May, and the country’s Caixin Services PMI declined to 53.9 from 57.1 in May. Following the publication of poor domestic data for China, the Australian dollar declines.

On the back of negative China data, the AUDUSD declines to 0.6680, breaking a four-day uptrend. The Aussie pair also defends challenges to sentiment brought on by US-China tension and recession-related problems in doing so. The Caixin Services PMI for China for June decreased from 57.1 to 53.9. China’s Caixin Manufacturing PMI eased to 50.5 for the specified month earlier this week, down from 50.9 the previous month and 50.2 market expectations. It is important to note that the official PMIs for the country of the Dragon for June also seem less impressive. In addition to concerns about the US economy slowing down and the Sino-American trade war, the softer China data also put downward pressure on the AUD price.

Nevertheless, China abruptly announced restrictions on the export of a few products containing gallium and germanium, starting on August 1. The latest retaliation from the dragon country is in response to the US embargo on Beijing’s imports of AI chips. The news regarding the Reserve Bank of Australia’s RBA hawkish halt may be on the same vein. Further challenging the Australian pair sellers is Acting Treasurer Katy Gallagher’s denial of Australia’s recession problems.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/