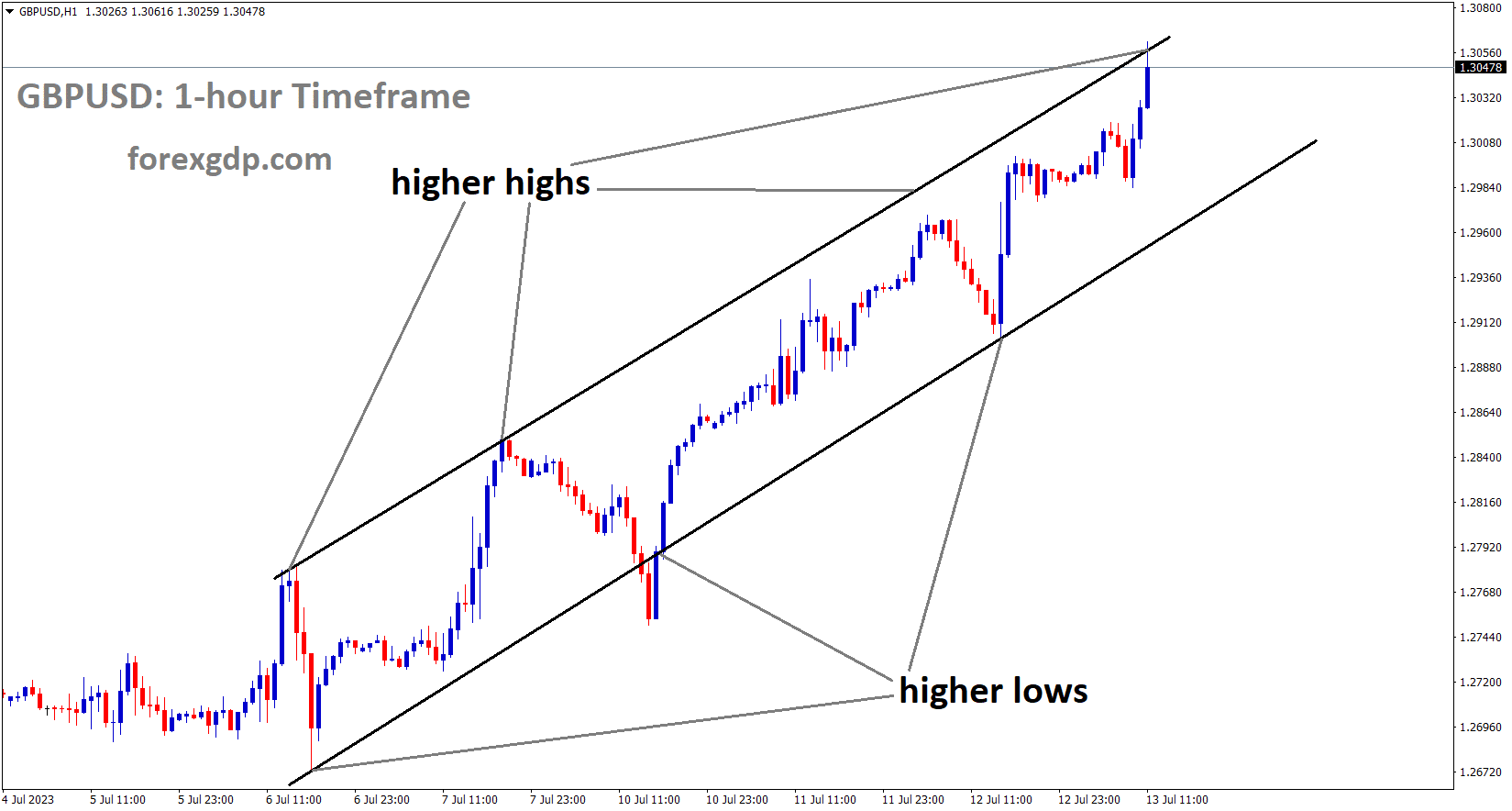

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

UK GDP MoM for May showed a 0.10% contraction compared to a 0.20% increase in April. The GDP data for the previous three months have not changed, and the services sector has not changed either. The increase in wages in the UK will help lower inflation in the second half of 2023, according to Bank of England Governor Bailey.

After growing by 0.2% in April 2023, the UK’s real GDP is projected to have decreased by 0.1% in May 2023. Looking at the data more broadly, the GDP did not increase in the three months leading up to May 2023. May 2023’s monthly GDP decreased by 0.4% from the corresponding month in the previous year. For comparison, between April 2022 and April 2023, the monthly GDP increased by 0.5%. The Platinum Jubilee, which resulted in an extra working day in May but two fewer days in June, according to ONS data, should be kept in mind as it may have an impact on the final data print when compared to the same period in 2022. The extra bank holiday, according to UK Chancellor Hunt, had an effect on growth in May, and inflation continued to be a hindrance to prospects for economic growth. Following an increase of 0.3% in April 2023, the services sector experienced no growth in May 2023. Overall, the services sector did not increase between the three months ending in May 2023 and the three months ending in February 2023. Human health and social work activities saw the biggest increase, 1.1%, which was largely offset by a 0.5% decline in wholesale and retail trade as well as auto and motorcycle repair.

From February 2020, the UK GDP is anticipated to be 0.2% higher than pre-covid levels.This week, Bank of England Governor Andrew Bailey gave a speech in response to rising wage expectations in the UK. Governor Bailey continues to maintain that the UK is fighting inflation in the right direction and that Q2 of 2023 will see a significant decline in inflation. The Governor added that despite the unprecedented rate increases over the previous 18 months, the economy and UK banks are currently doing okay. Even though the UK’s GDP is higher than it was in February of 2010 before the pandemic, there is still concern that the Bank of England will need to set a more stringent rate in order to reduce inflation. With Chancellor Hunt’s comments today reiterating the effects inflation is having on the economy, this could then cause the UK economy to enter a recession. As we approach the MPC meeting in August, all eyes will be on the BoE.

GOLD Analysis

XAUUSD Gold price has broken the Descending channel in upside.

When US CPI data (MoM) for June came in at 0.20% instead of the expected 0.30%, Gold appreciated against the US dollar. The likelihood that the FED will raise interest rates by 25 basis points at its July meeting is 92%, according to economists.

SILVER Analysis

XAGUSD Silver price has broken the Descending channel in upside.

The US Federal Reserve’s tightening cycle is about to come to an end, according to market expectations, which led to a rebound in gold after US inflation slowed down more than anticipated in June. The US CPI increased by 0.2% on a monthly basis in June, the smallest increase since August 2021, versus the 0.3% consensus. Core CPI moderated to 4.8% on-year, below the 5% forecast and the 5.3% recorded in May. However, the CME FedWatch tool indicates that there is a small chance of another hike before the end of the year, with rate futures indicating a 92% chance of a 25-basis point hike at the meeting on 25–26 July.

Rate reductions are anticipated by markets starting in H1-2023, with nearly 5 rate reductions by the end of the following year. The Fed is forecasting two rate hikes before the year ends and no rate cuts until 2025, which contrasts with the market’s expectations. The market’s dovish pricing has been further supported by the data from Wednesday. However, given that the labour market is still strong and inflation is still running well above the Fed’s target, a rate increase at the July meeting is still a possibility. Beyond that, it is still very unclear whether and by how much interest rates will increase.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Bank of Canada raised its interest rate by 25 basis points yesterday, and its governor claimed that this was because there was too much demand. Lower energy prices and a strong labour market support the Canadian economy. Readings of inflation are the basis for future rate increases.

In an effort to continue combating persistently high inflation, the Bank of Canada today concluded its July monetary policy meeting by voting to raise its benchmark interest rate by 25 basis points to 5.0%, the highest level in 22 years. After deciding to resume the tightening campaign and end the conditional pause announced in January, the institution raised rates for the second consecutive and back-to-back quarters of a point on Wednesday. The BoC stated that the economy has performed better than anticipated and that labour markets are still tight. It also mentioned that consumer spending has been surprisingly strong. Furthermore, the organisation led by Tiff Mcklen stated that recent data continue to show excess demand, a state of the economy that by definition tends to be inflationary.

Regarding the inflation outlook, the BoC acknowledged that price growth had slowed down, but added that lower energy prices, rather than underlying pressures, had largely been responsible for the general trend’s directional improvement. In this regard, the bank issued a warning that slower CPI progress will indicate that policy must remain restrictive for a longer period of time. The advice for the hiking cycle was a little bit hawkish. Although policymakers did not state it explicitly, “excess demand and core inflation” are proving to be more persistent than anticipated, which leaves the possibility of further hikes on the table.

The USD/CAD currency pair continued to decline on a daily basis after the Bank of Canada’s announcement hit the wires, reaching its lowest point since June 27. Although much will also depend on the Federal Reserve’s stance, the possibility that the Bank of Canada will increase borrowing costs once more later this year should be somewhat supportive for the Canadian dollar in the near term.

USD Index Analysis

USD index is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

US CPI data for the year came in at 3.0% instead of the expected 3.1%. which is less than the month before. The FED may raise rates by 25 basis points this month, which would be the final increase, with a pause for the remainder of the year. The main reason the US economy’s CPI is declining is because energy, food, and petrol prices are lower than they were in May.

In June, US headline inflation decreased year over year to 3%, beating forecasts of 3.1%. Core CPI YoY, which had been posing a challenge for the Federal Reserve, also outperformed expectations of 5%. The headline YoY inflation print marks the end of 12 months of declines and is the lowest reading since March 2021. The Core CPI, which had been rather stubborn recently, fell to 4.8%, its lowest level since October 2021. Energy costs plunged 16.7% vs. -11.7% in May, with prices falling by 36.6% for fuel oil, 26.5% for petrol and 18.6% for utility gas service. These factors were the biggest contributors to the decline in the headline figure. The Federal Reserve’s concern over food prices had been another source of surprise today, as prices rose by 5.7% rather than the 6.7% print from May.

The odds of a 25 bps hike were around 88% in the markets going into the July FOMC meeting, and the Fed was not expected to be swayed by today’s CPI reading. Even with a slight decline in last week’s NFP print and a rising trend of part-time workers over permanent ones, the US labour markets continue to show resilience. This week, Fed policymakers reiterated their hawkish outlook, with many believing it would be appropriate to keep up the rate hikes. In the June FOMC minutes, there were indications that Fed members disagreed on the best course of action, but I still anticipate a rate hike from the Fed in July. If there is any surprise, I think it might be in the size of the hike, with a potential hike of 10-15bps.

EURJPY Analysis

EURJPY is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

According to the Bank of Japan’s household survey, Japan’s inflation rate could increase to 10.5% in a single year. If inflation rises above the target range, the Bank of Japan will need to alter its monetary policy settings because wage prices have increased more over the past 20 years.

The average household expects inflation to be a staggering 10.5% over the next year, according to a central bank survey on the topic. Additionally, from 75.4% to 79% of respondents said they expect prices to rise in the next five years. In light of the most recent data and the fastest wage growth in nearly two decades, things in Japan seem to be looking up. Pressure is growing on the Bank of Japan (BoJ) to reverse years of ultra-accommodative monetary policy implemented to stoke a healthy level of inflation because actual inflation is above target and inflation expectations are at such extreme levels. The BoJ’s cap on longer-term yields makes the Japanese yen the release valve where markets bet on BoJ policy changes.

EURGBP Analysis

EURGBP is moving in the Descending channel and the market has reached the lower high area of the channel.

The US CPI data for June month decreased from the expected 3.1% annual rate to 3.0%. The last day saw the euro strengthening against the dollar due to the ECB’s two additional rate hike plans for 2023 and the FED’s upcoming rate hike.

The European Central Bank is expected to raise interest rates by 25 basis points at its meeting later this month. However, as President Christine Lagarde and other Board members have noted in previous remarks, the central bank is unlikely to reverse its bias towards rate hikes in the near future. In the larger scheme of things, the Fed’s and the ECB’s potential future actions in normalising their monetary policies are still being debated, particularly in light of growing worries about an economic slowdown on both sides of the Atlantic. In terms of regional data, the CPI in France’s final June figures increased by 0.2% MoM and 4.5% YoY, while industrial production in the euro zone increased at a monthly 0.2% rate and decreased by 2.2% from a year earlier. Producer Prices for June will be the main focus in the US, followed by the usual weekly initial claims for unemployment benefits for the week ending July 8.

More vacation time in May, according to UK Chancellor Jeremy Hunt, lowers the GDP rate that month, and as future growth rates rise, inflation will decrease.

Chancellor Jeremy Hunt commented on the UK Gross Domestic Product GDP data, stating that “high inflation remains a drag anchor on economic growth, even though an extra Bank Holiday had an impact on growth in May. Bringing inflation down as soon as possible is the best way to restart growth and relieve family stress. Hunt continued, “Our strategy will work, but we must follow it.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to the manufacturing sector’s contraction in June, the NZD Business PMI fell from 48.9 in May to 47.5 in June. Since November 2022, this reading is at its lowest level.

Contrary to expectations, the New Zealand Business NZ PMI fell in June to 47.5 from 48.9 in May. According to the data, the manufacturing sector continued to contract in June. It is below the long-term average of 53.0 and the lowest reading since November 2022. Production (47.5) and New Orders (43.8), two important sub-index values, dragged the June result further into contraction, while Employment (47.0) also slowed down. These sub-index values must return to positive territory for any long-term activity levels to be reached,” the report stated.

AUDCAD Analysis

AUDCAD has broken the Descending channel in upside.

As US domestic data came in at a slower pace, the Australian Dollar advanced. According to RBA Governor Philip Lowe, slower economic growth may be possible in the coming years if more tightening measures are taken. In a few months, the RBA Governor’s term will come to an end, and the RBA is preparing to change the number of monetary policy meetings from the current 11 to 8.

Despite Philip Lowe, the governor of the Reserve Bank of Australia, making hawkish comments, the Australian dollar is having trouble gaining traction. RBA Lowe has opened the door for additional policy tightening due to the complexity of the inflation picture and its outlook. According to Philip Lowe, the economy will continue to grow slowly over the coming years. The RBA has recently changed the organisation of its monetary policy. From the beginning of the following year, there will be eight rather than eleven policy meetings by the Australian central bank. As Philip Lowe’s term is about to expire, the Australian government is also looking for a replacement to oversee monetary policy operations. Investors’ attention will be drawn to the release of forward-year consumer inflation expectations on Thursday at 1:00 GMT. Compared to the previous release of 5.2%, the economic data is predicted to soften to 5.1%.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

The Swiss Franc increases as the SNB sells foreign assets as a result of the stronger currency. Due to SNB’s FX intervention, the Euro fell against the Swiss Franc.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/