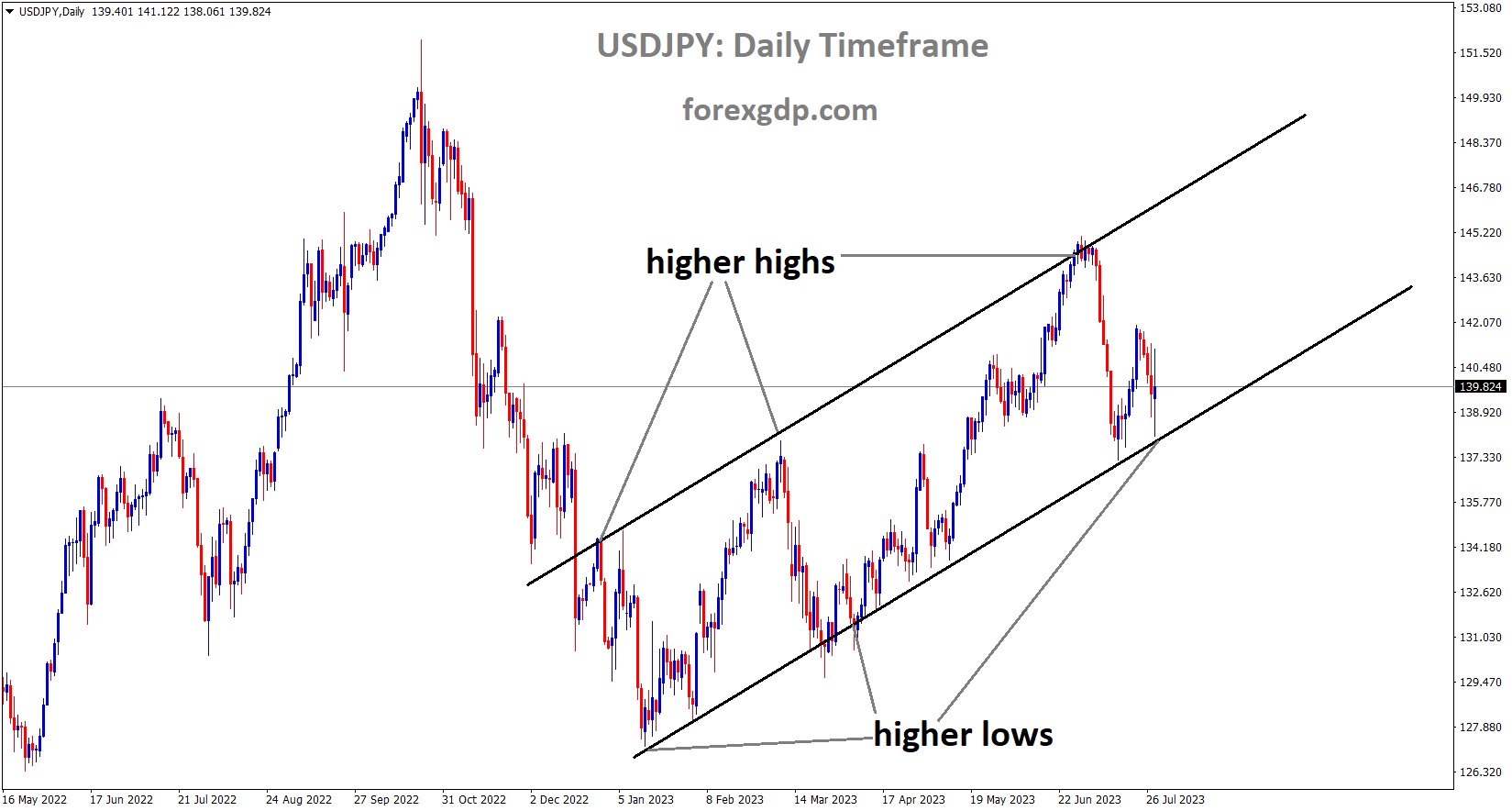

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

After the Bank of Japan decided to maintain its current policy settings at -0.10% at its meeting today, the Japanese Yen soared higher. No YCC settings were altered. According to BoJ Governor Ueda, corporate rate-setting behaviour has increased recently and the inflation reading will slow to 2% in the middle of the fiscal year.

There will not be a rate increase in monetary policy until the wage increase reaches our goal.

After the Bank of Japan BOJ kept its ultra-loose policy settings and the cap on the JGB 10-year yield, but stated that it would guide yield curve control more flexibly to respond to upside and downside risks, the Japanese yen fell against the US dollar. The BOJ maintained the yield target of roughly 0% and a band of +- 0.5% around the JGB 10-year yield band. The BOJ will reportedly discuss modifying its yield curve control policy at today’s board meeting by allowing long-term interest rates to rise beyond its 0.5% cap to a certain extent, according to a report published earlier on Friday by the Nikkei. The proposed modification would maintain the rate cap while allowing for modest increases above that point. Because of this, USDJPY declined significantly prior to the BOJ rate decision announcement, one-week 25-delta risk reversals continued to move in favour of JPY calls, and the Japan 10-year government bond yield hit increased above the BOJ’s cap of 0.5% in response to the report. After the policy announcement, the USDJPY exchange rate has gained ground. At its meeting today, the Japanese central bank was widely anticipated to maintain its current policy settings while waiting for additional proof of persistent price pressures. the controversial yield curve control YCC policy, which is being phased out, after a board member was quoted in the BOJ summary of opinions from the June policy meeting as saying the central bank should discuss changing YCC to improve market function and lessen its “high cost.”

Inflation is expected to slow to below 2% by the middle of the current fiscal year, according to BOJ Governor Kazuo Ueda, but the nation’s corporate price-setting behaviour is displaying changes that could cause inflation to rise higher than anticipated. Early Friday morning data revealed that in July, core inflation in Tokyo exceeded the 2.9% forecast by 3.0%. From 3.2% in May to 3.3% in June, the national core CPI increased. The so-called core-core inflation gauge, which does not include food or energy, decreased from 4.3% in May to 4.2% on a yearly basis. Future pressure on the yen may come from the still significant interest rate differences between Japan and the rest of the world. The downside in the JPY is likely to be supported, though, as the BOJ’s ultra-easy policy may be coming to an end.

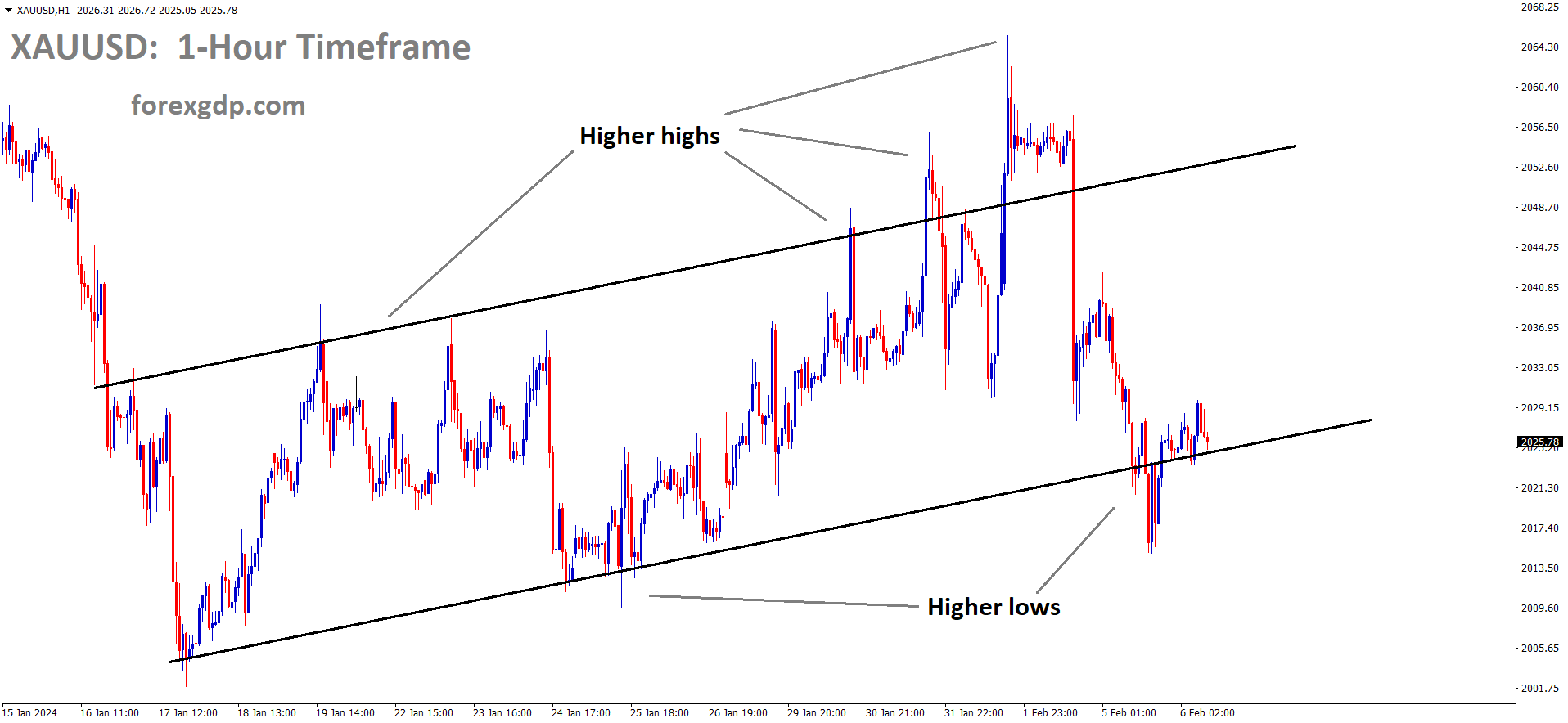

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Following the release of stronger-than-expected US GDP Q2 data, gold prices fell sharply from recent highs. Despite the fact that rate increases are higher in the US, the GDP data show that the country is progressing well. In contrast to the 1.8% decline anticipated, the most recent data, which had 2%, printed at 2.4%.

Since the most recent batch of US data showed the American economy to be in excellent shape, gold has lost more than $25 today. While jobless claims decreased and core PCE prices came in below market expectations, durable goods m/m outperformed expectations by a significant margin. The first estimate of Q2 GDP also outperformed expectations. Thoughts of a soft landing in the US will become more prevalent if tomorrow’s Core PCE Price Index and Michigan Consumer Sentiment continue in the same direction. The precious metal is being severely impacted by today’s increase in US Treasury yields, breaking through recent short-term support at $1,960/oz. With the current price action also appearing to drop below both the 20- and 50-day simple moving averages and towards a previous support zone between $1,940/oz. and $1,932.6/oz, the technical outlook is beginning to turn negative. The next level of support would be $1,900/oz if a confirmed break below this occurred.

USDCAD Analysis

USDCAD is moving in an Ascending triangle pattern and the market has reached the resistance area of the pattern.

The expected reading for Canadian GDP is 0.30%, up from the previous reading of 0%. A slowdown in the country’s manufacturing sector makes the CAD less competitive with other currencies. On July 12, the BoC increased the rate by 25 basis points, which is a 22-year high of 5.0%. Thus, no further rate increases are anticipated until the end of the year.

The USDCAD pair is currently trading at 1.3225, up 0.01% on the day, after retreating from 1.3248. The strengthening of the US Dollar is supported by the encouraging GDP figure. Prior to the start of the early European session, the US Dollar Index DXY, a gauge of the dollar against a basket of currencies used by US trading partners, remains above 101.70. For additional traction later in the North American session, market participants will keep an eye on the economic data. The US dollar has drawn some buyers across the board since the publication of positive US economic statistics on Thursday. Following the 2% growth reported in the first quarter, the US Bureau of Economic Analysis BEA first estimate showed that the US real Gross Domestic Product GDP increased at a rate of 2.4% annualised, exceeding the market expectation of 1.8%. On a monthly basis, orders for durable goods increased 4.7% to $302.5 billion. In the week ending July 22, initial claims for unemployment insurance fell by 7,000, to 221,000, the lowest level in five months. The information increased hope that the economy would be able to avoid a recession this year. In turn, this might strengthen the US dollar and limit the Loonie’s appreciation against a basket of commodities.

Jerome Powell, the chairman of the Federal Reserve, stated after the July policy meeting that another rate increase of 25 basis points bps could occur in September or November if the data support it. The Fed’s Fed more hawkish stance than the Bank of Canada’s BoC’s benefits the USDCAD pair. On July 12, the Bank of Canada BoC announced a 25 basis point rate increase to a 22-year high of 5.0%. Incoming data and the inflation outlook will be taken into consideration when making future policy decisions, according to Governor of the Bank of Canada Tiff Macklem. It is important to remember that the following policy meeting is set for September 6. The Bank of Canada BoC was not expected to raise rates further this year, according to market participants. A median of the participants in a market survey that the central bank released on Monday believe that the bank will keep interest rates at a 22-year high of 5.00% until the end of 2023 before lowering them in March.

Crude Oil Analysis

Crude Oil is moving in an Ascending channel and the market has reached the higher high area of the channel.

The Loonie has been supported by the rise in oil prices, which has also countered the decline in Canadian manufacturing. Since Canada is the top oil exporter to the United States, higher crude prices support the Canadian Dollar. Investors will closely monitor the Canadian Gross Domestic Product GDP data later in the day. From the previous reading of 0%, the figure is anticipated to increase by 0.3%. The US Core Personal Consumption Expenditure PCE report, the Fed’s preferred inflation indicator, will also be released during the North American session. It is anticipated that annual inflation will decrease from 4.6% to 4.2%. Prior to next week’s employment data, the data will be essential for determining a clear movement for the pair.

USD index Analysis

USD index is moving in the Descending triangle pattern and the market has rebounded from the horizontal support area of the pattern.

The US Q2 GDP data came in at 2.4%, up from 1.8% expected and 2.0% in the previous quarter. 70% of US GDP is made up of personal consumption expenditures, which increased by 1.6% from the previous quarter’s 4.0% growth. Therefore, the FED may raise rates again in upcoming meetings as a result of pockets of higher public spending in the US that are evident in GDP data.

Despite extremely high central bank interest rates, which are currently at their highest level in more than two decades, the U.S. economy gained momentum and expanded well above its long-term trend over the past three months. This was helped by consumer resiliency and robust capex spending. According to the U.S. Department of Commerce, the nation’s gross domestic product, the most comprehensive indicator of the goods and services it produces, expanded at an annualised rate of 2.4% in the second quarter, far exceeding forecasts of 1.8%. This is a strong result that might allay irrational fears of a recession.

Taking a closer look at the report’s specifics reveals that personal consumption expenditures, which make up about 70% of GDP, rose by 1.6% after previously rising by 4.0%, a glaring indication that households are still not prepared to stop spending, in part because of the robust and active labour market. While business fixed investment increased by 4.9% and residential investment decreased by 4.2%, gross private domestic capital formation overall increased by 5.7%. The housing market might remain weak given that mortgage rates are predicted to stay high, but there are other signs that suggest a bottoming out.

Overall, the strong GDP data indicate that, despite the FOMC’s aggressive measures to slow activity as part of its fight against inflation, the economy is still in excellent shape. This assessment is supported by final sales to domestic producers, which increased significantly at a rate of 2.3% (4.3% nominal) and show that the internal demand is holding up remarkably well. The U.S. dollar strengthened as a result of an increase in Treasury yields following the release of the GDP report by the U.S. Bureau of Economic Analysis. In order to prevent inflationary pressures from reaccelerating later this year, the Fed may be forced to deliver additional tightening if growth does not moderate. These anticipations may maintain an upward bias in yields, particularly if upcoming CPI and Core PCE results reveal price stickiness.

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to forecasts from last month, the ECB increased rates by 25bps. The interest rate was increased by the ECB from 4.00% to 4.25% yesterday. Further rate increases are less likely given the long-term need to control inflation and the ECB’s inability to predict how quickly it will decline. Inflation control policies are something we strive for.

The European Central Bank increased interest rates by 25 basis points in line with expectations, stating that despite recent declines, inflation is still anticipated to remain elevated for a longer period of time. The Central Bank also made the decision to set the minimum reserve compensation rate at 0%. By maintaining the current level of control over monetary policy stance and ensuring that interest rate decisions are fully transmitted to the money markets, the Central Bank claimed that this decision will maintain the effectiveness of monetary policy. In order to achieve a timely return of inflation to the 2% medium-term target, the ECB stated that moving forward policy rate decisions will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary. The Central Bank reaffirmed that developments since the last meeting support the expectation that inflation will decline even further, but the ECB is still concerned about the rate at which inflation is declining.

Regarding APPs, the ECB noted that the portfolio is deteriorating at a controlled and predictable rate. The Governing Council intends to reinvest principal payments from maturing securities purchased under the PEPP until at least the end of 2024.

Soon, the ECB Press Conference will start. When asked about the likelihood of a hike in September during her press conference, ECB President Lagarde remained evasive. Given that the President had previously been rather hawkish when pressed on potential rate hikes, this is a dovish indication. President Lagarde stressed that a September pause would not necessarily be for an extended period of time while also leaving the door open for quick policy changes should the need arise. She noted that the Central Bank may vary from one meeting to the next.

Lagarde confirmed the wording change in the statement was not random or irrelevant, which is a real mixed bag from the ECB. The European Central Bank’s (ECB) rate hike trajectory has become even more hazy going forward as a result of the Euro Area’s recent data performance. With different opinions on the future direction of monetary policy, this will undoubtedly lead to conflict among policymakers. Despite risks being skewed to the upside, inflation appears to be declining, as was previously mentioned. With the ECB stressing the length of time to bring inflation under control, the policy statement left the door open for future hikes. Recent economic indicators, particularly those related to PMI data and bank lending surveys, seem to have little influence at this point. The markets are still pricing in additional hikes from the ECB this year in the wake of the decision and before the press conference.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

The UK’s Royal Institution of Chartered Surveyors reported that 68% of respondents agreed that higher borrowing costs would hurt the housing sector. After chip shortages subsided, the annual growth rate for the automotive industry increased to 16%. After US GDP data yesterday exceeded expectations, the pound fell.

The fear of a UK economic recession is growing, and the Bank of England (BoE) is aggressively tightening monetary policy as a result. This has caused the Pound Sterling (GBP) to weaken. Although the GBP/USD pair was under pressure earlier, the outlook for the Pound Sterling is bullish as more interest rate increases from the UK central bank are possible in order to get inflation back on track.

Treasury of the United Kingdom Due to the aggressive policy tightening by the central bank, which has increased the burden on businesses, advisers expressed concerns about economic growth. In addition, the UK’s housing market is suffering from higher borrowing costs, and the number of first-time buyers has sharply decreased. Short-term pressure on the pound is present due to growing concerns about a UK recession and expectations of additional policy tightening by the Bank of England. As the BoE has sharply raised interest rates, advisers to UK Finance Minister Jeremy Hunt have expressed concerns about the risks of a recession becoming more severe. The central bank should slow down its rate-hiking spree, which is the fastest in three decades, according to the seven-member Economic Advisory Council, as some economic indicators point to a potential slowdown for the economy in the near future.

GBPNZD Analysis

GBPNZD is moving in the Box pattern and the market has reached the resistance area of the pattern.

Although the UK’s inflation dropped more than was anticipated in June, it was not enough to convince policymakers at the BoE to hold off on raising interest rates in August. The Consumer Price Index (CPI), which does not include volatile food and energy prices, fell to 6.9% in June while the headline CPI softened to 7.9%. These decreases, however, are not sufficient for the BoE to declare victory over inflation. Despite growing concerns about a recession and the growing burden on businesses, the BoE appears poised to increase interest rates again on August 3. The Bank of England is anticipated to announce a 25 basis point (bps) increase in interest rates, bringing them to 5.25%. This week, a Reuters poll indicated that the UK economy’s interest rates may reach a peak around 5.75%. According to a survey conducted by the UK’s Royal Institution of Chartered Surveyors (RICS), 68% of respondents think that the housing market has become vulnerable due to rising borrowing costs. Car production has increased for a fifth consecutive month despite rising interest rates as chip shortages have subsided.

The delivery of cars from factory gates increased by 16% annually, according to the Society of Motor Manufacturers and Traders (SMMT). The Federal Reserve (Fed) announced that it would take new data into account when deciding whether to raise interest rates further, which is boosting the market’s overall mood. Following a pause in June, the Fed raised interest rates by 25 basis points on Wednesday, bringing them to a range between 5.25% and 5.50%. Fears of a recession in the United States were significantly reduced by Fed Chair Jerome Powell’s failure to confirm further policy tightening. Powell added that no longer does the central bank’s staff predict a US recession. Investors are now focusing on the preliminary Gross Domestic Product (GDP) data, which will be released at 12:30 GMT, as they recover from the effects of the Fed’s policy meeting. The US economy is projected to grow at a rate of 1.8% on an annualised basis, which is slower than the 2.0% recorded in the first quarter.

The lack of noteworthy data released from the New Zealand docket this week makes it challenging for the Kiwi to develop a bullish thesis, and the offshore events will command attention. The Reserve Bank of New Zealand RBNZ, however, is expected to take a more hawkish stance by the market, which could increase the risk of a hard landing. This could consequently put pressure on the Kiwi.

AUDCAD Analysis

AUDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Retail sales data for June decreased by 0.80% compared to May’s 0.70% increase. PPI data for Q2 softened to 3.9%, down from 5.2% in Q1 but in line with expectations.

After today’s dismal data, the Australian Dollar is down.

According to the most recent data released by the Australian Bureau of Statistics ABS, consumer spending in Australia, as measured by retail sales, decreased by 0.8% over the course of the month in June as opposed to the 0% expected and May’s 0.7% increase. Separately, the Stats agency released data for the nation’s Q2 Producer Price Index PPI, which increased by 0.5% QoQ as opposed to the 0.9% forecast and 1.0% previous. Australia’s PPI inflation eased to 3.9% annually in the second quarter, down from a rate of 5.2% in the first quarter, and it was in line with market expectations of 3.9%.

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

In June, Swiss retail sales increased 1.8% year over year, compared to a contraction of 0.90% in May. Due to the improved data on retail sales, SNB may decide to raise rates at the upcoming meeting. After the US economy returned with better-than-expected Q2 GDP numbers, the US dollar increased in value relative to the Swiss franc.

The Swiss Franc CHF pair applauds the recently released domestic data while the US Dollar rises ahead of the superior data. In June, Swiss Real Retail Sales grew by 1.8% YoY, compared to the previous month’s contraction of 0.9%. This lends support to the Swiss National Bank’s SNB hawkish stance.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/