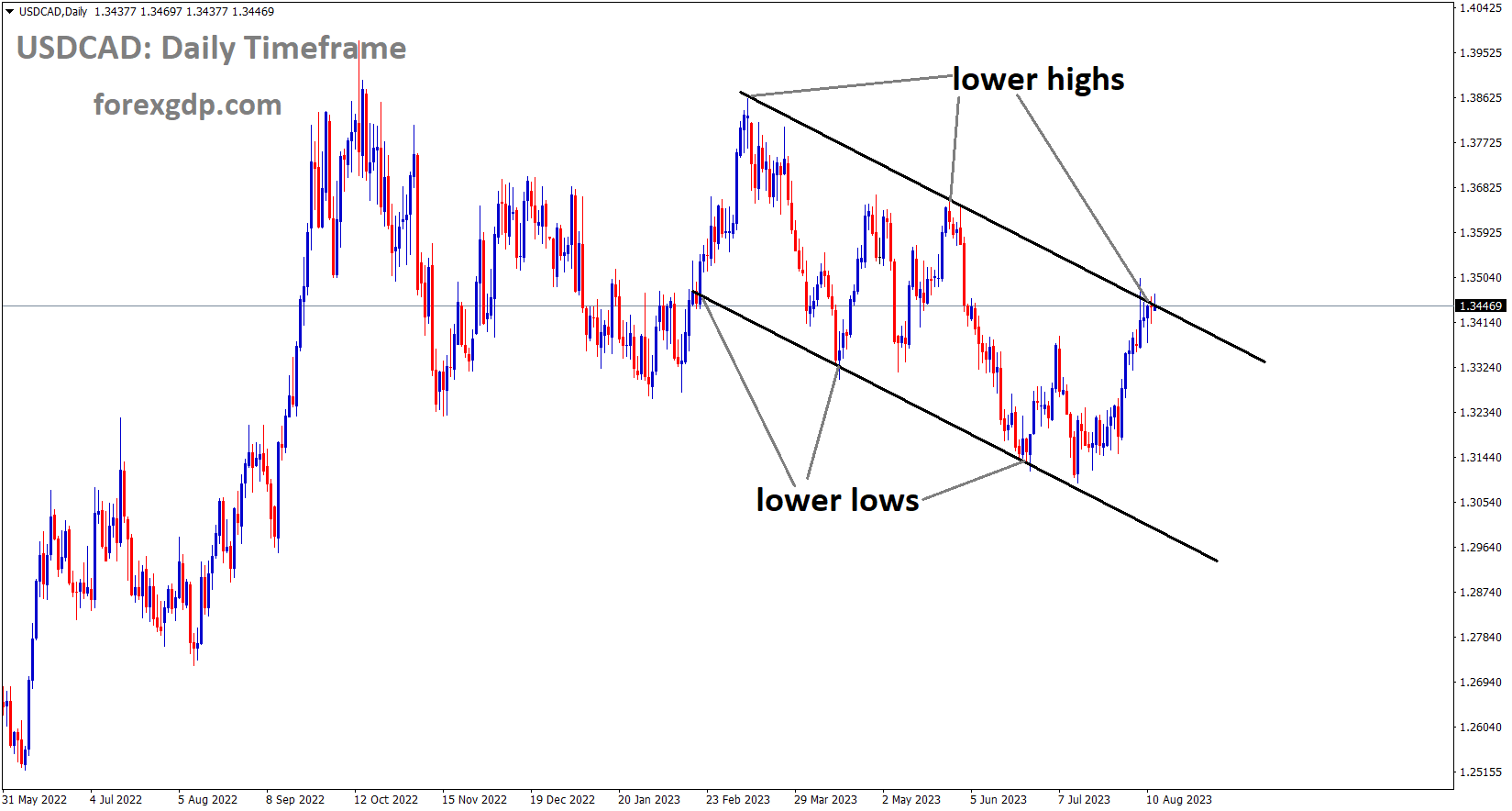

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

The Canadian dollar continues to benefit from rising oil prices, and this week’s scheduled 2.8% Canadian CPI data is expected to rise to 3.05 in July.

Crude Oil Analysis

Crude Oil is moving in the Box pattern and the market has reached the resistance area of the pattern

During Monday’s Asian trading hours, the USDCAD pair is trading higher. The rise in US 10-year Treasury bond yields and the mixed US economic data support the pair’s upswing. The Loonie is stronger than the US Dollar in the meantime due to the increase in oil prices. With a daily gain of 11%, the major pair is presently trading close to 1.3457. On Tuesday, traders will be watching the Canadian Consumer Price Index (CPI) YoY for July. On an annual basis, the percentage is anticipated to increase from 2.8% to 3.0%.

XAUUSD Analysis

XAUUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Pressure builds on gold prices when geopolitical tensions align. After China Country Gardens stopped paying the public, Russia began delivering hypersonic missiles to Ukraine via nuclear submarines.

Therefore, selling pressure from global tensions has caused a decline in gold prices.

After a four-week decline, the gold price XAUUSD maintains the bears’ lead at the monthly low as news out of China shakes investor confidence and supports the US dollar’s status as a haven. Geopolitical worries about Russia and rising US Treasury bond yields are contributing to the risk-off mood. This, in turn, enables the US Dollar Index DXY to hold onto its strength after rising for the past four weeks despite an impending Federal Reserve Fed policy pivot.

It is noteworthy that China’s debt problems are being exacerbated by the country’s suspension of its bond trading in addition to the non-receipt of payments from a Zhongzhi Enterprise Group subsidiary. The US-China trade war and Russia’s willingness to arm new nuclear submarines with hypersonic missiles are two other factors that add to the risk-off sentiment and influence the price of XAUUSD. In other news, largely positive indicators of US inflation run counter to dovish interest rate futures, implying that there will not be a hike in September, which puts pressure on the US dollar ahead of further indications of US price pressure and the Fed Minutes.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Rate cuts are anticipated by Goldman Sachs to range from 3.00 to 3.25% in the second quarter of 2024. The FED can only lower rates by 25 basis points every quarter, as Goldman Sachs predicted.

The most recent report from Goldman Sachs (GS) reveals dovish bias regarding the US Federal Reserve (Fed), with the analytical piece released over the weekend projecting a peak rate of between 3.0% and 3.25%. The GS also projects that beginning in the second quarter (Q2) of 2024, the Fed will begin reducing interest rates.

Carl Quintanilla, an analyst for the US bank, also tweets that the GS anticipates 25 basis points (bps) of rate cuts per quarter, with the option to cut rates more quickly if US policymakers believe the inflation issue is less likely to resurface.

The US FED policy makers’ resounding call for a rate hike in September to rein in US inflation is the reason why the US Dollar index rally did not end. Last week’s US CPI came in slightly higher than expected but lower than the previous reading. Due to the Covid-19 Crisis and the giant problem with country garden property, China’s economy is weak. Additionally encouraging for USD buyers is this news.

Again this week, the US dollar has performed well, mainly due to hawkish Federal Reserve policymakers and some early-week risk-off sentiment. Despite some weakness in US equities this week, markets do seem to have accepted the “soft landing” narrative. The markets continue to project an 88.5% chance that rates will stay the same in September, while the probability of a rate hike in December is currently at 30%. This is the only change in the Fed Funds probability over the course of the week. The weak data out of China this week, which saw a general sentiment of risk off, also helped the dollar. The Dollar has benefited from the market participants’ renewed concern over China’s uneven recovery due to its appeal as a safe haven. This week’s US inflation data did not reveal much: core inflation slightly decreased while headline inflation slightly increased but fell short of expectations. Numerous Federal Reserve policymakers, many of whom stated that the Fed still needed to work on inflation, cast a shadow over this. PPI data for July came in at 0.3% on Friday, up from a previously revised print of 0%. This represents a slight increase. As price pressures trickle down from production to the final consumer, PPI typically rises before CPI, which is probably another reason why the Dollar ended the week on the high note.

August University of Michigan Consumer Sentiment data declined, although much lie inflation came in above expectations on Friday as well. The report showed that the 1-year inflation expectations, which had previously been printed at 3.4%, had improved slightly to 3.3%. Although the current state of affairs improved, the expectations index decreased, from 68.3 to 67.3. After declining earlier in the week, US Treasury yields rebounded on Friday as well, with both the 2Y and 10Y yields expected to end the week higher. Treasury yields were unexpectedly rising during the first part of the week as the USD kept rising, but normalcy returned after the US CPI report on Thursday, which spurred a rise in yields.

As we approach the upcoming week, there could be some selling pressure on the DXY early on. Although the index has been rising rapidly over the last four weeks, it might be losing steam. Next week’s schedule is a little light, but the Federal Reserve minutes might keep the Dollar Index rising. This week, policymakers at the Federal Reserve said that there is still work to be done and that they have not even discussed a timeline for rate reductions. Given that the Fed is unlikely to exhibit any notable dovishness, I anticipate that this will be reflected in the minutes. We can learn more about the US demand side, which has moderated over the past few months, by examining retail sales data. Even though retail sales are positive for inflation, a further decline in sales could signal the possibility of a recession since lower prices should follow from decreased demand.

EURUSD Analysis

EURUSD is moving in the Descending channel and the minor Box pattern and the market has rebounded from the horizontal support area of the pattern

Georgia Meloni, the prime minister of Italy, stated that he will be in charge of increasing the windfall tax on banks. He said it will be a serious issue, and a meeting with the EU Parliament is anticipated.

According to Reuters, Italian Prime Minister Giorgia Meloni broke news early on Monday while speaking with La Repubblica, La Stampa, and Corriere della Sera.By characterising it as a serious matter, the Italian leader assumed full responsibility for the announcements of windfall tax on banks made earlier in the month.

Additionally, the policymaker dismissed rumours of alliances for the upcoming European Union (EU) parliamentary elections, stating that they were “Too early.” “No vetoes on Le Pen,” Meloni of Italy continued.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Data on industrial production in the UK was positive. June’s GDP was 0.50 percent, and manufacturing output was 2.4%. Mom last week made more GBP than USD. The economy will be concerned about the Bank of England’s rate hike because it is a 15-year high at 5.25%.

The investors are worried about the possibility of a further rate hike that would have an impact on the UK economy, the positive UK data is unable to strengthen the pound sterling. Friday saw an unexpected 0.5% MoM growth in the UK economy in June, above the 0.2% market estimate and down 0.1% from the previous month. Furthermore, June saw a 1.8% monthly increase in UK Industrial Production, exceeding projections of a 0.1% increase and a 0.6% decrease. The Manufacturing Output, which was expected to decline by 0.2% and 0.1% in the previous reading, instead came in at 2.4% mm. The likelihood that the Bank of England BoE will raise the additional interest rate is increased by the better UK economic data. Market players are wary of the BoE’s move, though, given the UK economy’s fragility and the interest rate’s 15-year high of 5.25%. The UK economy may suffer as a result of the aggressive monetary policy. Nonetheless, the UK’s inflation and wage data, which are anticipated later this week, will provide clues regarding the BoE’s decision at its upcoming meeting.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern

The lawsuit filed by Credit Suisse shareholders is being contested by UBS. The acquisition of Credit Suisse by UBS cost 3 billion francs, or half the value of the company’s shares. Shareholders suffered losses, and there was no voting procedure for this acquisition. Thus, a lawsuit was brought against UBS in the Swiss judiciary.

According to Financial Times, hundreds of individual shareholders, including former Credit Suisse employees, plan to file a claim in Zurich’s commercial court today, posing another legal challenge for UBS regarding its contentious takeover of Credit Suisse. About 500 Credit Suisse equity investors who suffered sizable losses when UBS took over the bank in March plan to file the claim on behalf of them, according to the Swiss Investor Protection Association SASV, which represents retail investors. The takeover, which was arranged by Swiss authorities, precluded shareholders from voting on the agreement. Credit Suisse was acquired by UBS for CHF 3 billion $3.4 billion, which was less than half of the bank’s market value the day before the deal was finalised. Bondholders who were impacted are pursuing multiple lawsuits, and this is the second class action lawsuit that Credit Suisse shareholders have filed against UBS.

Recently, UBS declared that it no longer needed government approval for the acquisition, potentially in an effort to quell public unrest ahead of October’s national elections. In order to meet the two-month deadline set by the Merger Act of Switzerland, SASV intends to file its case on August 14th. The deal was approved in June. Arik Röschke, the general secretary of SASV, proposed that UBS take into consideration settling the case, since a decision going against them might necessitate paying billions of dollars in compensation to all shareholders. But an out-of-court settlement would only provide the claimants with compensation. In a horse-trading transaction, UBS acquired one of the best capitalised banks in Europe for a pittance, according to Röschke. A portion of our claimants’ compensation was in stock; some of them worked at Credit Suisse for thirty years, he continued.

The parties bringing claims in this case are from a number of nations, including the US, the UK, Thailand, Austria, Germany, and Dubai. Many are former employees of Credit Suisse who were compensated with shares, according to a report by the Financial Times. Claimsants in the SASV case are required to pay a fee to cover the association’s costs, which may be partially refunded. The case is handled on a non-profit basis. Regarding the case, UBS declined to comment. The Swiss legal firm Niedermann Rechtsanwälte has been brought in to handle the case. This legal challenge comes after a comparable lawsuit filed by LegalPass, a legal services startup supported by Ethos Foundation, on behalf of institutional investors who hold roughly 5% of the stock in both banks. The Quinn Emanuel Urquhart & Sullivan and Pallas law firms are also defending bondholders who suffered when the transaction involved the write-down of $17 billion in additional tier 1 securities. Workers at Credit Suisse have also inquired about filing a lawsuit following the cancellation of their AT1-related bonuses.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The minutes of the RBA meeting are expected tomorrow. RBA Governor Lowe stated last week that the cost of building a home, rent, and services have increased inflation, even though the unemployment rate is at a 50-year low of 3.6%. Rate increases, conversely, result in decreased employment.

The US Dollar’s ascent into Monday’s trade is hindering the Australian Dollar’s ability to recover from its lows from last week, which is having an effect on riskier assets and commodities. Treasury yields, which have been rising steadily, seemed to be supporting the US dollar as the benchmark 2-year note surpassed 4.91% on Friday after touching 4.72% earlier in the week. The 10-year bond, which last week traded at 3.96%, is now preparing for a move above 4.20%. In order to maintain a relatively constant yield spread, Australian Commonwealth Government bonds (ACGB) saw a slight increase in yield at the same time. Commodity markets have been uneasy due to the strengthening US dollar; metals have seen some recent weakness in particular. To explore this facet of the Australian dollar’s weakness in more detail, see this article from our weekend publication. The Reserve Bank of Australia’s monetary policy meeting minutes, the wage price index, and the jobs report for the upcoming week are scheduled for tomorrow.

The Statement on Monetary Policy, which is made public the day the board meets, is usually not a source of surprise in the meeting minutes. The minutes contain more information, which occasionally reveals subtleties in the board’s reasoning. Philip Lowe, the governor of the Reserve Bank of Australia, addressed the House of Representatives Standing Committee on Economics last Friday. Regarding inflation, he reiterated that the primary drivers containing it were energy and the cost of constructing a house, while rents and other services kept driving up prices. It is anticipated that the wage price index will stay constant until the end of the second quarter, at 3.7% year over year. Given that several award-based wages have received 5% to 8% increases in the last few months, this gauge is receiving more attention than usual. According to a Bloomberg survey of economists, the unemployment rate will be 3.6%, which is not too far from 50-year lows. The Reserve Bank of Australia (RBA) has previously mentioned the tight labour market on multiple occasions as an obstacle to controlling inflation. Even though these domestic factors might influence the AUD/USD exchange rate, movements in the US dollar might still have the most influence.

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel

Japan’s government bonds were trading above the US dollar’s preferred rate of 0.60 percent. Typhoon Lan is predicted to make landfall in central Japan tomorrow; as a result of the natural disaster, there may be delays for flights and the rail system.

Japan’s government bonds JGB are stable at or above 0.60%, but the US dollar continues to benefit from the yield differential. Typhoon Lan is expected to make landfall in central Japan on Tuesday, causing major disruptions to rail and airline services. Tomorrow is the release date of the most recent GDP data from Japan. The Swiss Franc has been the least worst currency compared to the US Dollar thus far, with the high beta Aussie and Kiwi Dollars being the notable underperformers.

The week began with APAC equity markets in a sea of red, with Hong Kong’s Hang Seng Index HSI leading the decliners, down more than 2%.Chinese stocks have also suffered as worries about Country Garden persist despite Monday’s suspension of bond trading for the massive Chinese real estate company. Beijing declared that it intends to use tax breaks to promote foreign investment in specific sectors. On Tuesday, data on retail sales and industrial production in China will be made public. Wall Street futures suggest that their cash session will begin slowly, and European bourses might encounter some difficulties as well. The price of petrol has dropped this week after reaching all-time highs on Friday. Crude oil has also decreased today; the Brent contract is getting close to US$ 86 bbl, while the WTI futures contract is trading under US$ 82.50 bbl. The stronger dollar has resulted in decreased prices for base metals, especially nickel, copper, and aluminium. Although gold has dropped to its lowest point since early July, it is still stable at $1,910.

NZDUSD Analysis

NZDUSD is moving in the descending triangle pattern and the market has reached the horizontal support area of the pattern

The NZD Services index reading for this month was 49.4 from 50.1, and the reading for this month was 47.6, the lowest since January 2022. This week’s RBNZ meeting is planned, and economists are largely expected to exhibit a doveish bias.

For the fifth day in a row, there is some selling pressure on the NZDUSD pair, and on Monday during the Asian session, it falls to its lowest point since November 2022, near the mid-0.5900s. Antipodean currencies, such as the New Zealand Dollar NZD, are being undermined by growing concerns about China’s worsening economic conditions. The NZD loses more ground as a result of the negative domestic data. In fact, the Services Index for Business NZ fell to 47.8, the lowest level since January 2022, during July, entering contraction territory. Additionally, the reading from the prior month was revised downward from 50.1 to 49.6, indicating a slowing economy. The NZDUSD pair is still under pressure to decline due to this and the general bullish sentiment surrounding the US Dollar USD.

Indeed, as the Greenback is tracked against a basket of currencies, the USD Index DXY is up to its highest level since July 7 and is still being bolstered by expectations that the Federal Reserve Fed will maintain its hawkish stance. On Friday, the US PPI, which increased marginally more than anticipated in July, confirmed the wagers. In July, consumer prices increased somewhat, and the data indicated that the fight to return inflation to the Fed’s target of 2% is far from over. This supports a further increase in the yields on US Treasury bonds, which supports the USD, and leaves the door open for one more 25 basis point hike in Fed rates in 2023. In addition to the fundamental context already mentioned, Friday’s persistent breakdown below the psychological 0.6000 mark is thought to be another reason that triggers some follow-through technical selling in the NZDUSD pair. Consequently, this implies that the spot prices’ least resistance path is downward. Ahead of the important macro data dump from China on Tuesday and the Reserve Bank of New Zealand RBNZ monetary policy meeting on Wednesday, traders may choose to hold off on making large bets.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/