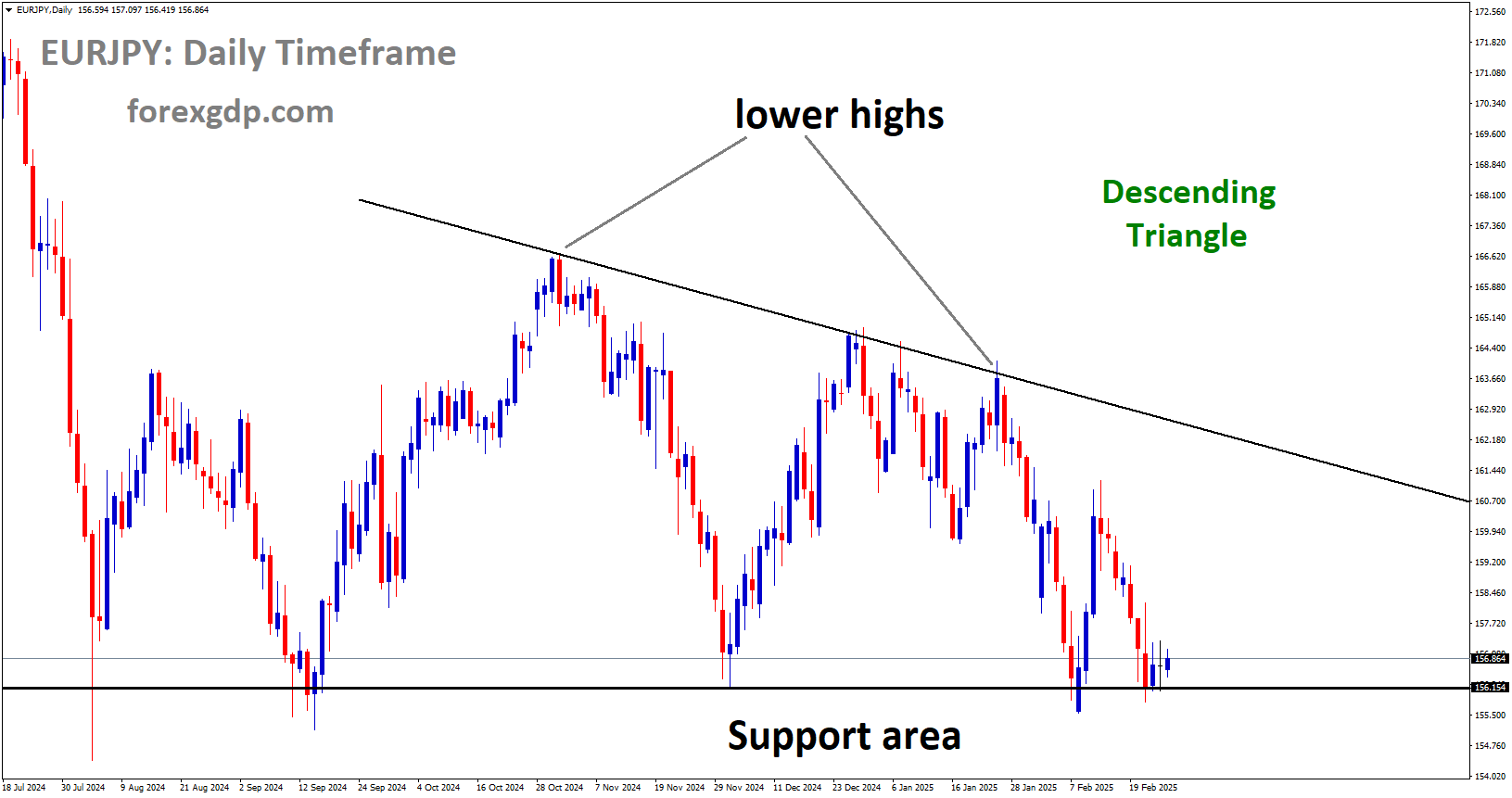

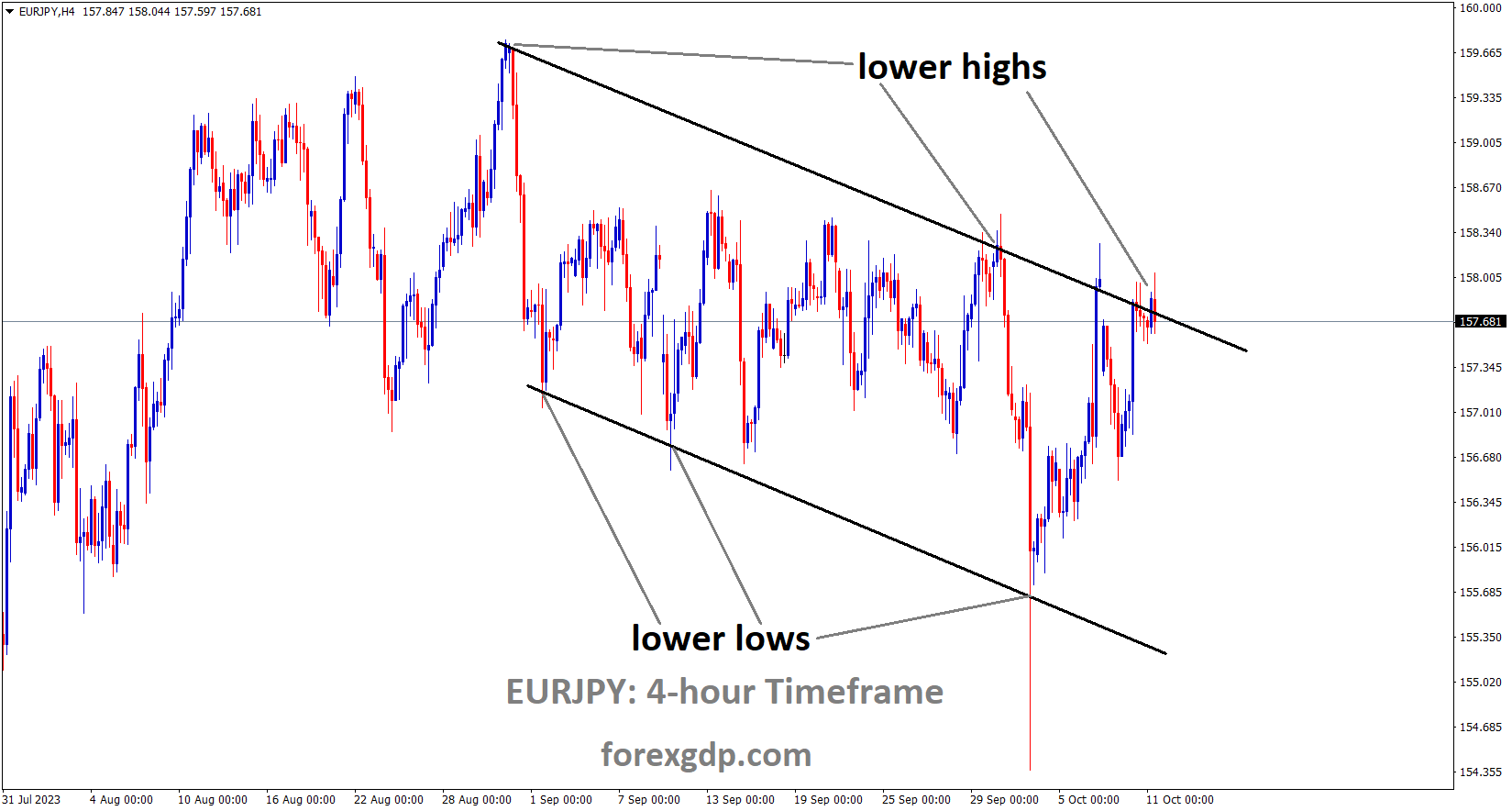

EURJPY Analysis

EURJPY is moving in the Descending channel and the market has reached the lower high area of the channel

The Bank of Japan has unequivocally expressed its commitment to maintaining an ultra-accommodative monetary policy, causing the yen to continue its slide against the US dollar.

Anticipations are high that the Bank of Japan BoJ will revise its 2023 core inflation forecasts upward to approximately 3% during the forthcoming October 30 and 31 meeting. Additionally, the BoJ is set to provide fresh projections for 2024 and 2025, and if these are revised upward, it could signal the beginning of a potential shift towards policy normalization.

Gold Analysis

XAUUSD Gold Price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Gold prices are experiencing a significant surge driven by concerns over the Israel-war conflict, while commodity prices are also on the rise due to increased demand. The possibility of the US Dollar weakening further next month as a result of additional rate hikes from the Federal Reserve is unlikely. The Gold price XAUUSD is maintaining its position at a recent weekly high, bolstered by a cautious market sentiment stemming from the escalating Israel-Hamas conflict. In response to Hamas’ incursion on Saturday, the Israeli army carried out airstrikes on the Gaza Strip. Additionally, the Federal Reserve Fed has provided a neutral outlook, indicating that it may have concluded its interest rate hikes. Fed policymakers have expressed concerns about the rising Treasury yields and the need for caution in further tightening monetary policy to avoid negatively impacting financial conditions. Despite tensions in the Middle East, the US Dollar has been unable to capitalize and is expected to remain under pressure, especially in anticipation of the Producer Price Index PPI data for September and the release of Federal Open Market Committee FOMC minutes.

Gold price is aiming to surpass the $1,860.00 mark, benefiting from increased demand for safe-haven assets due to heightened tensions in the Middle East and the Fed’s neutral stance.While the appetite for safe-haven assets has grown due to rising oil prices, there hasn’t been a significant sell-off yet. It appears that investors are monitoring the situation in Israel before making substantial moves. Israeli Prime Minister Benjamin Netanyahu stated that Israel’s response to Hamas’ multi-pronged attack would have a transformative impact on the Middle East. Gold price is performing well against the US Dollar as traders bet on an unchanged interest rate policy in the upcoming monetary policy meeting on November 1. According to the CME FedWatch Tool, there is an 88% likelihood that the Fed will keep interest rates steady at the current range of 5.25-5.50%, where they have been since July. The odds of another interest rate increase in the two remaining monetary policy meetings in 2023 have dropped to 28%. Dallas Fed Bank President Lorie Logan indicated that the Fed may not be inclined to raise interest rates further if long-term rates remain elevated due to higher Treasury yields. Regarding inflation, Logan mentioned that progress is encouraging but too early to confidently predict a sustainable path to the Fed’s 2% target.

Fed Vice Chair Phillip Jefferson emphasized the importance of considering higher Treasury yields before making any decisions on interest rates while speaking at the National Association for Business Economics conference. The 10-year US Treasury yield has reached nearly a 16-year high, approaching 4.8%, leading to a rise in 30-year mortgage rates to 7.5%. Jefferson cautioned that the central bank should exercise caution regarding further interest rate hikes. Last week, Cleveland Fed Bank President Loretta Mester and Fed Governor Michelle Bowman expressed support for one more interest rate increase in the remainder of 2023, citing the resilient US economy and the expectation that progress in reducing inflation to 2% may stall.The US Dollar Index DXY has found interim support around 106.00 after facing selling pressure due to the neutral guidance on interest rates from Fed policymakers. The future direction of the USD Index will depend on the US inflation data for September, set to be released on Thursday. According to estimates, monthly headline and Core inflation are expected to expand by 0.3%. The annual headline and Core Consumer Price Index CPI are projected to soften slightly to 3.6% and 4.1%, respectively. Before the release of US CPI data, the FOMC minutes for the September monetary policy and producer inflation data will be disclosed on Wednesday.

Silver Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The anticipated US inflation data for September is projected to come in at 3.6%, slightly lower than the 3.7% figure recorded in August. Consequently, the US Dollar is weakening against other currencies in anticipation of this data release.

The DXY Dollar Index is poised for a weekly decline leading up to the eagerly awaited Consumer Price Index CPI report. If these losses persist, it could mark the steepest five-day drop since mid-July. Additionally, there’s a growing bearish sentiment evident on the daily chart. Let’s analyze the current status of the currency in anticipation of the inflation report.

This Thursday, it’s expected that US headline inflation will weaken, with September’s year-on-year figure projected to be 3.6%, down from August’s 3.7%. This is referred to as disinflation, signifying a period where prices are still on the rise but at a slower rate compared to previous periods. It’s important to distinguish this from deflation, which involves prices falling. The Core CPI, which excludes volatile food and energy costs representing underlying inflation, is anticipated to decline from 4.3% to 4.1% year-on-year.

The Federal Reserve is likely to be more concerned with the latter figure. It’s worth noting that the lagging effect of decreasing rental property prices, as outlined in my fourth-quarter outlook, is expected to continue influencing core CPI. Consequently, this may exert downward pressure on core inflation in the coming months, aligning with my expectations for this upcoming report on Thursday.

Such an outcome is likely to validate the recent cautious statements from the Federal Reserve, which have been exerting slight downward pressure on Treasury yields. This, in turn, has been driving the US Dollar lower, particularly as stock markets rebound. As a result, there is reduced demand for the safety of the US Dollar, which works against the currency often associated with safe-haven characteristics.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

Global regulators praised the swift acquisition of Credit Suisse by UBS, noting that it was a decisive move that avoided the need for detailed procedural steps, thus preventing public panic concerning potential withdrawals.

Global regulators have come to the defense of Switzerland’s decision to support a rescue deal for Credit Suisse in March, rather than pursuing liquidation. This support was articulated in a report that underscored the limitations of a regulatory framework established post-global financial crisis.

The Financial Stability Board FSB, a highly influential collective of central bankers, regulators, and officials from leading global economies, released its report on “lessons to be learned.” It ultimately affirmed the overall success of the regulatory regime but exposed the tensions and conflicts inherent in a process that initially required Switzerland to financially back Credit Suisse’s emergency rescue by rival UBS.

Switzerland’s finance minister, Karin Keller-Sutter, emphasized that she had little choice given the potential economic repercussions, despite this move conflicting with a fundamental post-crisis reform principle that sought to shield taxpayers from bailing out distressed banks.

The report scrutinized Switzerland’s decision to support a takeover by the larger rival UBS instead of opting for the winding down or liquidation of Credit Suisse, as prescribed by a “resolution” mechanism designed after the 2008 financial crisis. The report’s conclusion was that the “resolution” rules, designed to handle the collapse of banks without causing market panic, could have been applied to Credit Suisse, albeit with the likely need for public funding. The FSB suggested that improvements in how these rules are applied might be required, rather than changes to their core principles.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

However, the practical challenges of implementing resolution or liquidation for a globally significant bank were evident, with legal feasibility differing significantly from economic realities. The report also contrasted with earlier criticism when UBS became Switzerland’s largest bank following the government’s rapid and partially funded takeover of Credit Suisse.

The report shed light on the events leading to Credit Suisse’s struggles. In mid-2022, Swiss regulator FINMA engaged in crisis discussions with international counterparts, considering options such as winding down the bank, nationalization, or a merger. U.S. authorities cautioned against liquidation due to the impact on bonds held by U.S. investors, citing legal obstacles.

The report refrained from directly criticizing Switzerland, although Bank of England Governor Andrew Bailey had previously expressed concerns about Switzerland’s deviation from the expected “playbook,” causing market uncertainty about the credibility of large bank resolutions.

Experts and consultants highlighted the limitations of resolution plans, noting their limited use in major failures. Spain’s Banco Popular was the only bank to have utilized them. The private nature of these “living wills” and the potential time-consuming nature of their implementation raised doubts about their effectiveness during times of crisis.

Overall, the report raised significant questions about the reliability and practicality of the regulatory framework, particularly in times of financial stress. Critics argued that further examination and enhancements were necessary, given the framework’s untested nature during a major crisis.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has rebounded from the support area of the pattern

ECB President Lagarde has stated that there is no immediate need for a further rate hike, expressing confidence that inflation will moderate until the next year. Additionally, she emphasized that the Euro region has ample energy reserves and reassured that the conflict in Israel will not significantly impact the region’s economic stability.

The currency pair is benefiting from an upward trend, largely driven by the ongoing correction in the US Dollar USD following dovish comments made by Federal Reserve Fed officials. A wave of dovish remarks from Fed policymakers has reverberated throughout the markets, with several expressing concerns that the elevated long-term US bond yields could hinder their willingness to raise interest rates in upcoming meetings.

Atlanta’s Fed President, Raphael Bostic, has taken a firm stance, stating that the current monetary policy is already restrictive, making additional rate hikes unnecessary. This perspective aligns with the dovish trajectory set by two fellow Fed colleagues earlier in the week, as Minneapolis Fed President Neel Kashkari echoed similar sentiments on Tuesday. Despite a minor recovery in US Treasury yields on Tuesday, the US Dollar Index DXY has faced losses and is currently trading lower around 105.70. Notably, the 10-year US Treasury bond yield stands at 4.64% at present.

Investors are closely monitoring economic data, particularly focusing on inflation figures. The Producer Price Index PPI is set to be released on Wednesday, followed by the publication of the FOMC meeting minutes and the Consumer Price Index CPI on Thursday. However, an increase in German bond yields may pose a constraint on the EURUSD pair’s upward movement, as market participants anticipate the European Central Bank ECB may halt its tightening cycle.

On Tuesday, Francois Villeroy de Galhau, a member of the European Central Bank ECB Governing Council and President of the Bank of France, expressed the viewpoint that “at this stage, further rate hikes are not the right course of action.” In an interview with the French newspaper La Tribune Dimanche, ECB President Christine Lagarde also voiced her confidence, stating that key ECB interest rates have reached levels that, if maintained over a sufficient duration, will significantly contribute to bringing inflation back to the target. President Lagarde remains optimistic about achieving the goal of reducing inflation to 2% and expressed confidence in Europe’s gas reserves.

Projections suggest a slowdown in Germany’s inflation, which could bolster the belief that the ECB will maintain unchanged interest rates.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In anticipation of the release of UK GDP and manufacturing production data, the GBP is showing a modest increase against the USD. Conversely, in the lead-up to key US domestic data such as the FOMC meeting minutes, the US Dollar is exhibiting slight weakness in comparison to the GBP.

The GBPUSD is experiencing an uptick in trading on Tuesday, reflecting a cautious rebound in market sentiment following the recent escalation of the Israel-Hamas conflict over the weekend. The Pound Sterling GBP is gaining strength, pushing it to fresh two-week highs, just below the 1.2300 mark.

This week holds significant importance for US inflation data, with the Producer Price Index PPI and Consumer Price Index CPI reports scheduled for release on Wednesday and Thursday, respectively. Concurrently, the Pound Sterling has its place on the economic calendar, with Gross Domestic Product GDP and Industrial & Manufacturing Production figures slated for Thursday. Federal Reserve Fed officials have been actively communicating on Tuesday, emphasizing the limited potential for further interest rate hikes. This stance has been keeping the US Dollar USD relatively subdued and providing an opportunity for risk assets to regain some lost ground.

The upcoming UK GDP data for Thursday is expected to reveal a modest recovery, with the monthly figure for August projected to show growth at 0.2%, a positive contrast to the previous month’s -0.5% contraction. In addition, the Industrial & Manufacturing Production numbers for the same period are also anticipated to improve, albeit with minor declines. The industrial component is forecasted to decline by -0.2%, an improvement from the previous -0.7%. Similarly, the manufacturing component is expected to record a decline of -0.4%, indicating a slight recovery from the previous -0.8% contraction.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The National Bank of Canada has reported that Canada is experiencing a shortage in housing supply, primarily driven by escalating rental and leasing costs in the country. The prospect of interest rate hikes is seen as advantageous for property owners, as it allows them to increase rental rates.

Deputy Prime Minister of Russia, Alexander Novak, has expressed concern that the ongoing conflict in Israel may have a global impact on oil prices.

The National Bank of Canada’s Stéfane Marion has released a report highlighting a concerning trend in Canada’s housing deficit, which reached an unprecedented low during the third quarter. The soaring costs of housing in Canada, coupled with supply limitations, are expected to further drive up mortgage lending rates and rents, posing a significant challenge as home and shelter expenses are already anticipated to exert a drag on the country’s economic growth in the coming years.

The September employment report unveiled a substantial increase in the working-age population, resulting in a remarkable cumulative gain of 267,000 during the third quarter. This surge, which stands as the largest on record, follows a gain of 238,000 in the second quarter and 204,000 in the first quarter. Setting three consecutive quarterly records for population growth is an unprecedented occurrence in modern Canadian history.

As a consequence of this robust population growth, the housing supply deficit has exacerbated to its most severe level ever recorded in the third quarter. Currently, there is only one housing start for every 4.2 individuals entering the working-age population individuals aged 15 and above. This stark contrast with the historical ratio of one housing start for every 1.8 new entrants to the working-age population underscores the magnitude of this imbalance. It is anticipated that this significant mismatch between housing supply and population growth will persist into the foreseeable future, pending a substantial slowdown in demographic expansion.

Before his meeting with Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, scheduled for later on Wednesday, Russian Deputy Prime Minister Alexander Novak stated that the agenda would include discussions on the oil market situation and oil prices, as reported by the TASS news agency. Novak also pointed out that the ongoing escalation of the Israel-Palestinian conflict could potentially have an impact on the oil market.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The Australian Dollar surged as the US Dollar weakened in anticipation of US inflation data. RBA Deputy Governor Kent emphasized that if the inflation rate does not align with the target, there may be a need for further interest rate hikes.

The Australian Dollar took a moment to reflect on its recent surge today, driven by signals that the Federal Reserve is adopting a cautious stance, while the Reserve Bank of Australia RBA is carefully assessing the outcomes of its recent series of interest rate hikes. Simultaneously, the ongoing situation in the Middle East has led to increased scrutiny of potential risks affecting various asset classes.

In the realm of commodities, crude oil prices remained relatively stable on Wednesday, with the WTI futures contract maintaining levels above $86 per barrel, while the Brent contract hovered near $88 per barrel.

Following the close of the North American trading session, San Francisco Fed President Mary Daly echoed sentiments expressed by other members of the Federal Reserve this week. The prevailing notion is that the rise in long-term bond yields in the Treasury market may be serving as an indirect tightening mechanism for the Fed. This has raised speculation that the central bank might signal a potential pause in its policy moves, both at its upcoming meeting this month and in the foreseeable future. Interest rate markets are currently assigning a low probability to an imminent rate hike. However, despite this shift being less hawkish, there are no indications in the Fed’s language thus far of any impending monetary easing.

Ms. Daly also suggested that the Fed’s “neutral rate” could potentially be higher than the widely accepted 2.5%. Nevertheless, she emphasized that the current Fed funds policy rate, ranging from 5.25% to 5.50%, is aimed at addressing high inflation and significantly exceeds the theoretical neutral rate. In terms of the US economy, Minneapolis Federal Reserve President Neel Kashkari expressed optimism about a soft landing scenario, stating that “It is looking more favorable.” On a positive note, Wall Street concluded its cash session on an upbeat trajectory, and Asian-Pacific equities followed suit. South Korea’s KOSPI index led the way with an increase of over 2.5%. Treasury yields remained relatively unchanged, with the 2-year note hovering around 5%, and the 10-year yield remaining at approximately 4.65%. Meanwhile, spot gold maintained its position near $1,860.

However, prominent investor Paul Tudor Jones expressed concerns about the current geopolitical environment, characterizing it as the most challenging he has witnessed. He also predicted a US recession in 2024 and noted that the US’s financial position is currently at its weakest since World War II. On another front, Reserve Bank of Australia RBA Assistant Governor Chris Kent raised concerns about the time lag in the transmission effects of monetary policy. He also highlighted the possibility of further tightening being necessary to bring down persistently high inflation to the target level. In response to Kent’s remarks, the AUDUSD pair exhibited a slight softening, and the NZDUSD pair also declined. This coincided with the upcoming national election in New Zealand scheduled for this weekend. Looking ahead, the economic calendar includes the German CPI figure, followed by US PPI data.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The Reserve Bank of New Zealand RBNZ decided to keep its interest rates unchanged last month, and the likelihood of future interest rate hikes by the Federal Reserve Fed is now less certain. These factors have contributed to the strengthening of the New Zealand Dollar NZD against the US Dollar .

The US Dollar continues to face downward pressure as market expectations for additional interest rate hikes by the Federal Reserve Fed have diminished. This shift is viewed as a supportive factor for the NZDUSD pair. Furthermore, relatively subdued US wage growth data, released last Friday, alleviated concerns about inflation. Coupled with dovish comments from various Fed officials, this suggests a more cautious stance from the US central bank.

According to reports from the Wall Street Journal WSJ, Fed officials are signaling that the recent increase in long-term interest rates could potentially serve as a substitute for another central bank rate hike. This development has led to a further decline in US Treasury bond yields, exerting additional pressure on the US Dollar. Additionally, an overall positive sentiment in the markets is weighing on the safe-haven status of the US Dollar, benefiting the riskier New Zealand Dollar Kiwi.

The NZDUSD pair has seen a substantial rally, gaining nearly 200 pips from its monthly low, which was around the 0.5870 level reached last week. However, this uptrend currently lacks strong momentum. Market participants are still factoring in the possibility of at least one more Fed rate hike before the year ends. This, coupled with concerns about escalating geopolitical tensions in the Middle East, may limit the downside potential for the USD and act as a restraint on the NZDUSD pair.

Traders are also awaiting the release of the US Producer Price Index PPI and the FOMC monetary policy meeting minutes, scheduled for later during the North American session. The focus will then shift to the release of the latest US consumer inflation figures on Thursday. These events will provide fresh insights into the Fed’s future rate hike path, ultimately influencing the price dynamics of the USD and offering a new directional impetus to the NZDUSD pair.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/