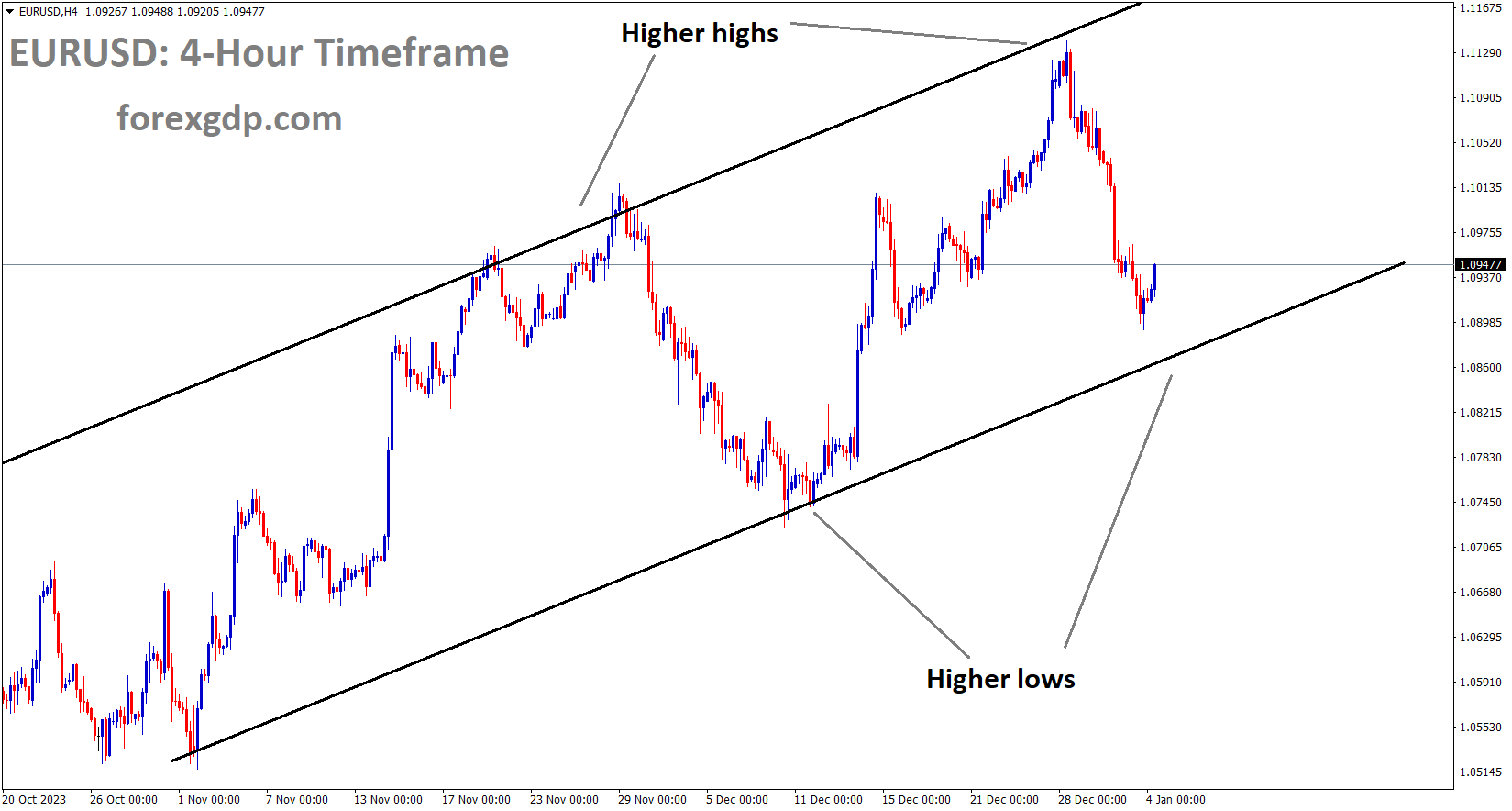

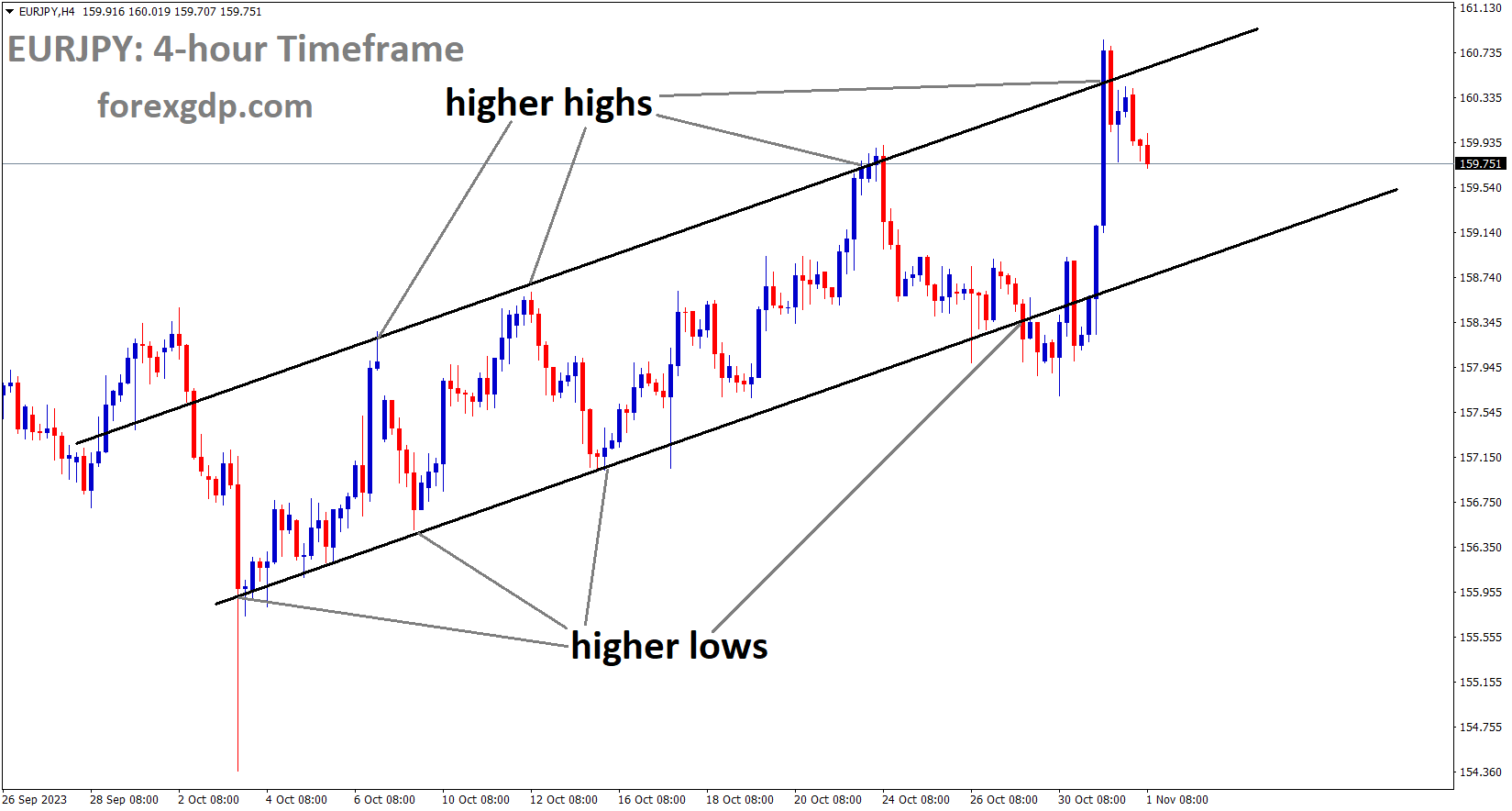

EURJPY Analysis:

EURJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The Japanese yen faced significant depreciation against both the U.S. dollar and the euro in response to the Bank of Japan’s monetary policy announcement. During early afternoon trading in New York, the USDJPY exchange rate surged by approximately 1.5%, reaching 151.35, a level not seen since October of the previous year. Simultaneously, the EUR/JPY rate experienced an increase of around 1.2%, surpassing the 160.00 threshold and achieving its highest point in 15 years.

The Bank of Japan opted to maintain its benchmark interest rate at -0.10% while making adjustments to its yield curve control program. This move indicated a shift towards a more flexible approach to managing long-term interest rates. Under this new framework, the institution would permit the 10-year government bond yield to rise above 1.0%, defining this level as a reference point rather than an inflexible cap, as was previously considered.

Although the Bank of Japan’s actions signaled a departure from its controversial accommodative stance of the past decade, they fell short of expectations generated by a media leak on Monday. This leak had suggested that, under the leadership of Kazuo Ueda, the institution was prepared to implement a more substantial and meaningful change to its current strategy.

The yen’s decline was exacerbated by reports that the Ministry of Finance had refrained from intervening in foreign exchange markets recently. Traders had believed that the government had taken steps to support the currency earlier in the month, but official data contradicted this claim. Consequently, the heightened volatility experienced a few weeks ago, when the USDJPY rate exceeded 150.00, was likely the result of trading algorithms. With the Bank of Japan not yet ready to fully abandon its ultra-dovish stance and the Japanese government taking limited action to curb the yen’s weakness, speculative trading activity could continue to drive both the USDJPY and EURJPY rates higher in the near term. This could potentially lead to fresh multi-year highs for both currency pairs as we head into November.

GOLD Analysis:

XAUUSD Gold price has broken the Ascending channel in downside.

XAUUSD Gold price has broken the Ascending channel in downside.

Gold prices initially dipped to approximately $1,990 per ounce during the Asian session, but a rebound occurred during the European session, bringing the precious metal back above the $2,000 per ounce threshold. However, there is noticeable selling pressure hovering above the $2,000 per ounce mark, coinciding with the Dollar Index (DXY) showing signs of a recovery during the upcoming U.S. session.

U.S. economic data continues to exhibit strength, with today’s Consumer Confidence figure surpassing expectations by registering 102.6 in October, surpassing the anticipated 100. The September reading was also revised upwards from 103 to 104.3, signaling an improving consumer outlook despite recent challenges. A noteworthy concern in the data is the persistently high 1-year consumer inflation expectations, remaining at 5.9%, alongside the 4-year inflation expectation, which also stands at 5.9%. This is causing apprehension for the Federal Reserve and market participants, as it suggests that the Fed may need to take further action. It could partially explain the resurgence of the U.S. Dollar Index (DXY).

As the FOMC meeting scheduled for tomorrow approaches, market expectations lean towards a pause from the Federal Reserve. However, if the Fed receives another round of robust data, there is speculation about whether Fed Chair Powell might adopt a more hawkish stance. Mere comments about the possibility of another interest rate hike may not suffice to extend the recent DXY rally beyond the 107.00 mark. Therefore, the language used by the Fed Chair during tomorrow’s meeting holds paramount importance, as the rate decision itself is unlikely to generate substantial market movement.

Turning attention to the Middle East, there has been an escalation in attacks on U.S. bases in the region, coupled with Israeli airstrikes on Hezbollah targets in Lebanon overnight. These developments could further intensify tensions and reignite safe-haven demand. This geopolitical backdrop continues to influence the financial markets, particularly impacting the price of Gold, and should not be disregarded.

SILVER Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has reached the support area of the pattern

On Tuesday, the US Dollar (USD) demonstrated strength, with the DXY index reaching a daily high of approximately 106.85, in close proximity to last Thursday’s monthly high of 106.90 before settling at 106.70. Several factors contributed to this uptick in the Greenback, including a cautious market sentiment ahead of the Federal Reserve (Fed) decision scheduled for Wednesday and positive mid-tier economic data. Additionally, the ongoing conflict between Israel and the Gaza group weighed on market sentiment.

Despite the Federal Reserve’s tightening measures, the US economy has shown remarkable resilience, bolstering the USD’s performance. However, the likelihood of a 25-basis-point interest rate hike in December, as indicated by the CME FedWatch Tool, remains low, limiting significant upward movement for the USD. Nevertheless, investors will closely analyze the policy statement and the words of Fed Chair Jerome Powell for insights into forward guidance, which will help shape their expectations for the upcoming meetings.

The US DXY Index rebounded to 106.70 after briefly dipping below 106.00 earlier in the day. Economic data for the day included the US Conference Board Consumer Confidence Index for October, which exceeded expectations by registering 102.6 versus the anticipated 100.5. Additionally, the S&P Dow Jones Indices reported that the S&P/Case-Shiller Home Price Index for August surpassed expectations, recording a 2.2% year-on-year increase compared to the expected 1.6% and a notable improvement from the previous reading of 0.2%. On the downside, the Chicago PMI for October disappointed, coming in at 44, below the consensus of 45, and declining from its previous reading of 44.1.

Meanwhile, US government bond yields displayed a mixed performance, with the 2-year, 5-year, and 10-year yields at 5.07%, 4.81%, and 4.86%, respectively. These varying yields could potentially limit the momentum of the USD. Looking ahead to Wednesday, the CME FedWatch Tool suggests that a pause in November is largely priced in, while the odds of a 25-basis-point rate hike in December remain relatively low, around 20%.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Investors are eagerly anticipating the upcoming Federal Open Market Committee (FOMC) policy meeting scheduled for Wednesday, with expectations of no change in interest rates. Key economic data releases include the US Chicago Purchasing Managers’ Index for October, which dipped slightly to 44.0 from 44.1 in September. In contrast, the CB Consumer Confidence Index for October exceeded expectations, reaching 102.6. Furthermore, the US S&P/Case-Shiller Home Price Indices showed improvement, rising by 2.2% YoY in August, compared to the previous reading of 0.2%, surpassing the estimated 1.6%. Lastly, the House Price Index for the month registered a 0.6% increase MoM, down from 0.8% in the previous month.

The FOMC is poised to announce its interest rate decision on Wednesday, with no surprises expected in terms of rate changes. Market participants will closely scrutinize the FOMC’s press conference for insights into the committee’s stance on future interest rate hikes. Hawkish comments from Fed officials could potentially strengthen the US Dollar (USD) and exert pressure on the Swiss Franc (CHF). According to the CME Fedwatch tool, the market has priced in a 97% likelihood of a rate hold in the November meeting, while the odds of a rate hike for the November meeting have increased to 29.1%.

On Tuesday, the Swiss Real Retail Sales for September reported a YoY decrease of 0.6%, a notable improvement from the previous reading of a 2.2% decline and surpassing the market consensus of a 1.2% decrease. Despite the positive figure, it failed to provide a significant boost to the Swiss Franc (CHF). However, heightened tensions in the Middle East may bolster the CHF, which is traditionally considered a safe-haven currency, and limit the upside potential of the USDCHF pair.

Looking ahead, the highlights include the FOMC policy meeting and a speech by Swiss National Bank Chairman Thomas Jordan. Additionally, key US economic reports, including the ADP employment report, JOLTS Job Openings, and the ISM Manufacturing PMI, are due later on Wednesday. Later in the week, the Swiss Consumer Price Index (CPI) will be released on Thursday, followed by US employment data, including Nonfarm Payrolls and Average Hourly Earnings, on Friday.

EURCHF Analysis

EURCHF is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

The euro zone’s economic growth contracted in the third quarter, following in the footsteps of Germany’s contraction reported yesterday. This 0.1% decline from the previous quarter underscores the challenges posed by the global economic slowdown, which is gaining momentum. Surprisingly, this downside miss did not add to the euro’s troubles; in fact, the currency showed some strength. Even in the wake of Germany’s economic contraction reported yesterday, the euro managed to gain some ground, albeit starting from a relatively low point.

The European Central Bank (ECB) has indicated its satisfaction with the current interest rates, and inflation is displaying signs of improvement, temporarily easing concerns about stagflation. Additionally, recent stimulus measures announced by Chinese authorities in Beijing have helped stabilize Chinese and China-related assets in recent days. Given China’s significant role as a trading partner, these stimulus measures may assist in mitigating the euro’s declines.

Looking ahead, the focus turns to upcoming events such as the Federal Open Market Committee (FOMC) meeting, Non-farm payrolls data, and U.S. services PMI figures. Germany, the economic powerhouse of Europe, also saw a quarter-on-quarter and year-on-year contraction, resulting in discouraging figures, although the data was not as dire as initially feared.

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The British Pound Sterling (GBP) displayed limited movements on Wednesday as investors awaited monetary policy decisions from both the US Federal Reserve (Fed) and the Bank of England (BoE). The GBP/USD pair remained in a state of uncertainty, with investors anticipating that the BoE would maintain its current interest rates. In the near term, the demand for the Pound Sterling appears fragile, as investors believe the BoE will opt to hold rates steady due to concerns about a slowdown in the UK economy, despite persistent inflationary pressures. Aside from the monetary policy decision, market participants will seek guidance on future interest rates and the inflation outlook. UK Prime Minister Rishi Sunak pledged in January to reduce inflation to 5.4% by year-end, a commitment that appears challenging as annual price growth remained at 6.7% in September, largely unchanged since July.

The Pound Sterling remains under pressure as the appeal for risk-associated assets diminishes ahead of the Federal Reserve’s monetary policy meeting and ongoing tensions in the Middle East. Gaza announced its intention to release hostages in the coming days, but a ceasefire is not anticipated as the Israeli Defense Forces (IDF) contemplate a full-scale ground offensive in Gaza. Apart from geopolitical tensions, the cautious stance of market participants ahead of the BoE meeting is keeping the Pound Sterling in suspense.

displayed limited movements on Wednesday as investors awaited monetary policy decisions from both the US Federal Reserve (Fed) and the Bank of England (BoE)")

The BoE is expected to maintain its interest rates at 5.25% on Thursday, marking the second consecutive occasion that policymakers have left rates unchanged after 14 consecutive rate hikes. There is skepticism regarding whether UK Prime Minister Rishi Sunak will fulfill his commitment to halve inflation to 5.4% by year-end.

GBPCHF Analysis:

GBPCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Consumer inflation in the UK economy is the highest among G7 nations, primarily due to robust wage growth. Despite persistent inflationary risks, the BoE is anticipated to maintain the status quo due to the economic slowdown driven by declining labor demand. The UK Office for National Statistics (ONS) reported that employment contracted for the third consecutive time in August, suggesting potential upward risks to the Unemployment Rate. Other economic indicators, such as weak consumer spending and declining business investment, support the expectation of a steady interest rate decision from the BoE. While robust wage growth continues to exert upward pressure on prices, there has been a significant drop in food price inflation in October. High inflation and reduced labor demand have prompted households to curtail spending and increase savings amid a volatile economic environment. According to the British Retail Consortium (BRC), food inflation has declined for the sixth consecutive month, with the food price index easing to 8.8% in October from 9.9% in September.

Meanwhile, the US Dollar Index (DXY) has stabilized around 106.80 after a sharp rebound, as investors await the Fed’s monetary policy decision, private payroll data, and the ISM Manufacturing PMI for October. The Fed is expected to maintain interest rates in the range of 5.25%-5.50% but may provide a hawkish outlook, as inflation above 2% remains persistent due to strong consumer spending, a robust labor market, and expectations of a revival in business activity. A positive report on private payrolls and factory activity would bolster the US Dollar, allowing the Fed to prolong its elevated interest rates. The Manufacturing PMI for October, as surveyed by S&P Global, stood at the threshold of 50.0, signifying the boundary between expansion and contraction in factory activity.

GBPNZD Analysis:

GBPNZD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The NZD pair is experiencing losses as market sentiment tilts in favor of the US Dollar (USD) ahead of the upcoming monetary policy decision by the US Federal Reserve (Fed) scheduled for Wednesday. Furthermore, the Kiwi pair faces headwinds due to moderate employment data from New Zealand. In the third quarter, Employment Change declined by 0.2%, falling short of expectations for a 0.4% increase. The Unemployment Rate also rose as anticipated, climbing from 3.6% to 3.9%, indicating that the Reserve Bank of New Zealand (RBNZ) is likely to maintain its policy rate in November. This expectation is placing downward pressure on the NZD pair.

")

In addition, the unexpected drop in China’s Caixin Manufacturing Purchasing Managers’ Index (PMI) revealed in the latest data on Wednesday has raised concerns about deteriorating economic conditions in the world’s second-largest economy. This adds to the pressure on the New Zealand Dollar (NZD), as the PMI for October recorded a reading of 49.5, below the expected 50.8 and lower than September’s 50.6, which indicated expansion.

CADCHF Analysis:

CADCHF has broken the Box pattern in upside

US Dollar Index saw a boost driven by rising US Treasury yields, maintaining a position near 106.70, while the 10-year US bond yield reached 4.90% as of the latest data. Market sentiment leans towards the expectation that the US Federal Reserve will keep the current interest rate steady at 5.5% in their Wednesday meeting. Any hawkish statements from the Federal Open Market Committee regarding the future direction of interest rates could potentially strengthen the US Dollar.

The ongoing conflict between Israel and Gaza has raised concerns about potential disruptions in oil supply from the Middle East. Despite these worries, crude oil prices have dropped to two-month lows, exerting downward pressure on the Canadian Dollar (CAD). As of the current writing, Western Texas Intermediate is trading below $81.00 per barrel.

Furthermore, on Tuesday, disappointing data on monthly Canadian GDP may have weakened the commodity-linked Loonie Dollar and acted as a supporting factor for the USDCAD pair. Statistics Canada’s release of Gross Domestic Product data for August revealed that the Canadian economy exhibited no growth, remaining flat at 0.0%. This outcome contradicted market expectations, which had anticipated a 0.1% expansion during the same period. In addition to this, market participants will closely watch the S&P Global Manufacturing PMI for further insights into Canada’s economic situation.

AUDUSD Analysis:

AUDUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

The Australian dollar has declined against the US dollar this morning due to disappointing Chinese PMI data This deceleration in economic activity has caused a drop in most soft commodities, precious metals, and base metals, exerting downward pressure on the AUD. Australia is a significant commodity trading partner with China, and its currency tends to be sensitive to Chinese economic performance. While the manufacturing PMI had recently re-entered expansionary territory for the first time since April, it has now slipped back below the critical 50-mark. Despite falling short of expectations, the Chinese government’s efforts to stimulate the economy could still have a positive impact in the future.

Assistant Governor Brad Jones of the Reserve Bank of Australia (RBA) addressed the public earlier today, but his remarks provided little insight into the central bank’s monetary policy stance. However, his statement emphasized the uncertainty surrounding interest rates, citing factors such as geopolitical tensions, global trade disruptions, cyberattacks, and climate change, which could contribute to increased interest rate volatility.

One positive development for the AUD came from the monthly housing credit figure, which reached its highest level in a year at 0.4%. Nevertheless, inflation remains relatively stable, supporting the likelihood of a 25-basis point rate hike at the RBA’s upcoming decision on November 7th. Later today, attention will shift to the US CB consumer confidence data and labor cost figures, ahead of Friday’s Non-Farm Payroll (NFP) report.

In its annual assessment of the Australian economy, the International Monetary Fund (IMF) emphasized the economy’s resilience, while noting that inflation continues to be persistent. The IMF argues that the Reserve Bank of Australia (RBA) should implement further policy tightening measures. Despite experiencing a robust post-pandemic recovery, Australia’s economy is currently undergoing a slowdown, albeit maintaining its resilience. Inflation, though gradually decreasing, remains considerably higher than the RBA’s target, and economic output continues to surpass its potential. As a result, the IMF recommends additional monetary policy tightening to ensure that inflation returns to the target range by 2025 and to minimize the risk of inflation expectations becoming unanchored.

The IMF also suggests that the Commonwealth government, along with state and territory governments, should implement public investment projects at a more measured and coordinated pace. This approach is necessary due to supply constraints and can help alleviate inflationary pressures while supporting the RBA’s efforts to combat disinflation.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/