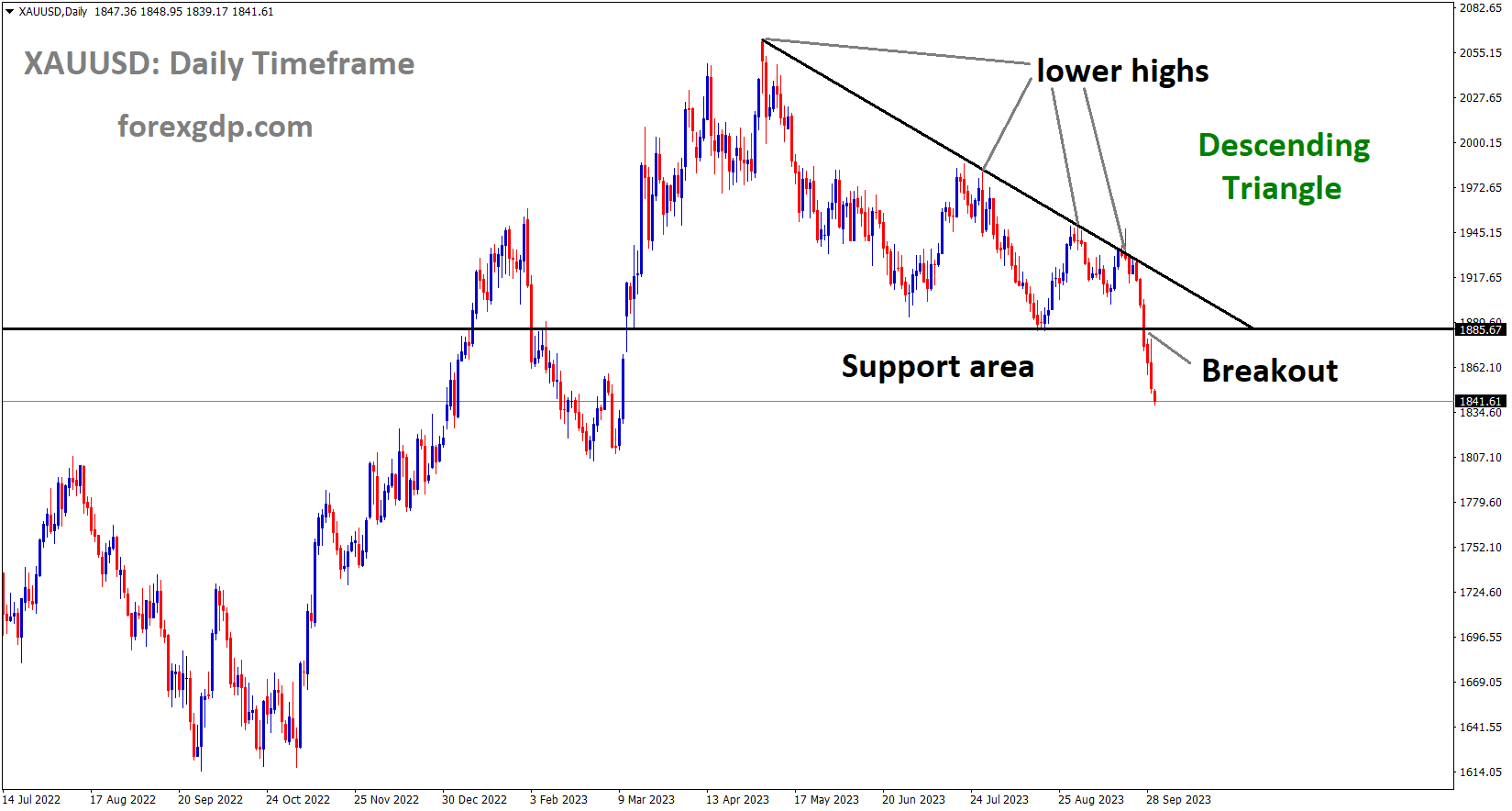

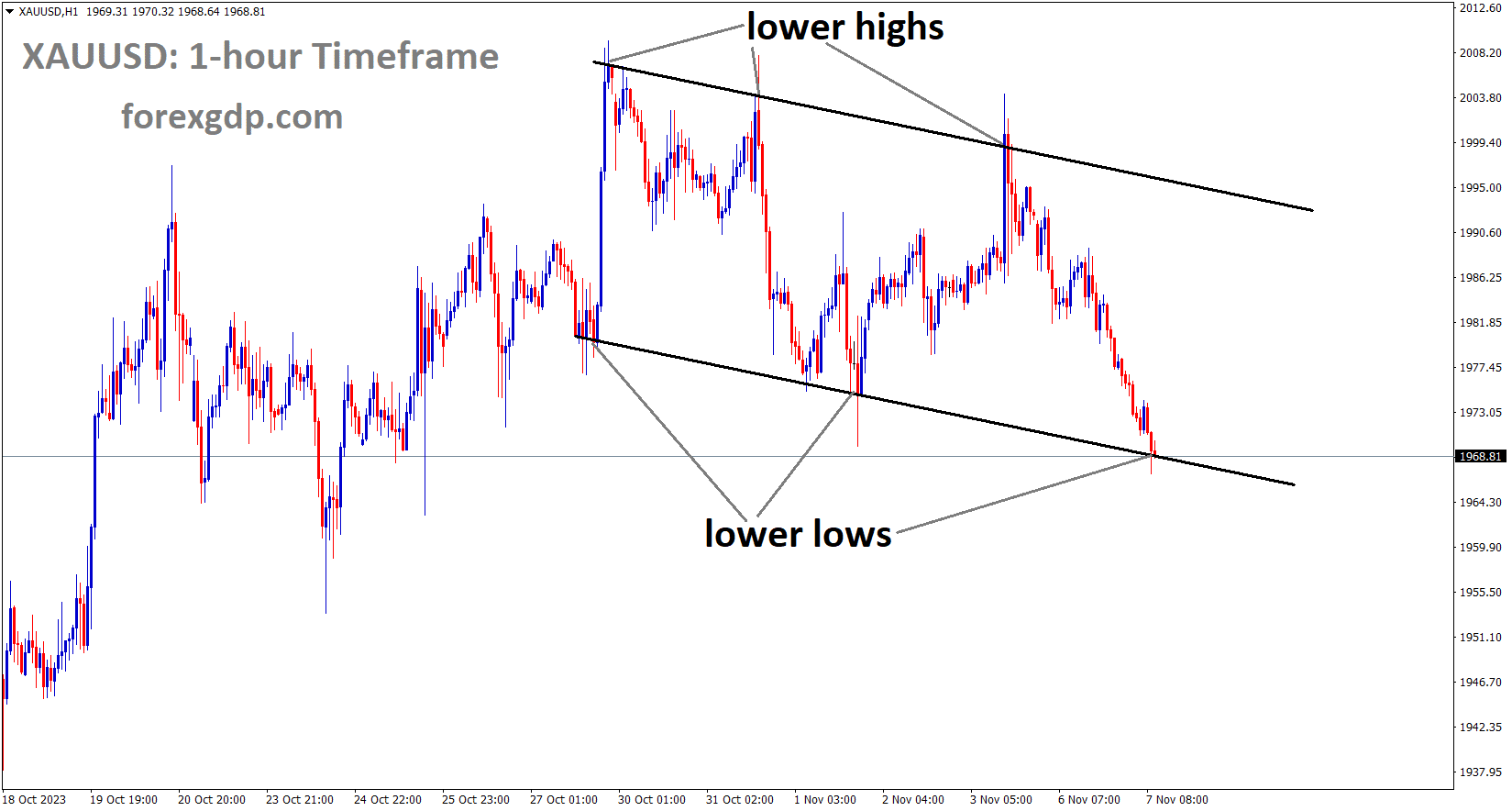

Gold Analysis:

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower low area of the channel

The recent de-escalation in the conflict in Israel and Gaza has led to a correction in Gold prices. Despite weak US domestic data last week, Gold prices did not see significant upward movement.

The price of gold faced selling pressure for the second consecutive day on Tuesday, maintaining a downward trend just above the monthly low as the European session approached. This decline can be attributed to several factors. Firstly, the ongoing recovery of the US Dollar from its lowest level since September 20, observed on Monday, has been exerting downward pressure on the precious metal. Furthermore, the absence of significant developments in the Israel-Gaza conflict has diverted investor attention away from the safe-haven appeal of gold. However, the persistent risk of a potentially expanding crisis in the Middle East, coupled with prevailing economic uncertainty, has left investors feeling cautious. This caution is evident in the somewhat subdued tone of equity markets, which, in turn, offers some support to the price of gold.

Additionally, a recent drop in US Treasury bond yields, driven by growing expectations that the Federal Reserve is nearing the conclusion of its policy tightening measures, is expected to limit losses for gold. As a non-yielding asset, gold tends to benefit from lower bond yields, making it an attractive investment option. Given the uncertainty surrounding the Fed’s future interest rate decisions, some investors may be inclined to wait for more guidance. Therefore, attention is likely to remain focused on speeches by influential members of the Federal Open Market Committee, with particular interest in Fed Chair Jerome Powell’s appearances on Wednesday and Thursday. These speeches will play a crucial role in influencing short-term USD price dynamics and determining the next direction for gold.

In the meantime, the release of US Trade Balance data on Tuesday could provide additional trading impetus during the early North American session. The uncertainty surrounding the Federal Reserve’s upcoming policy moves has prompted short-covering in the US Dollar, putting pressure on the price of gold. The softer US jobs report released on Friday has reinforced expectations that the central bank will maintain its current policy stance for the third consecutive meeting in December. Federal Reserve Governor Lisa Cook stated on Monday that the central bank’s current target interest rate is sufficient to bring inflation back to its 2% target. Minneapolis Fed President Neel Kashkari also noted that the US economy has demonstrated resilience, and under-tightening monetary policy will not expedite the return of inflation to the 2% target in a reasonable timeframe.

Furthermore, US Treasury bond yields, despite experiencing a rebound overnight, turned lower on Tuesday due to bets that the Fed’s rate hikes are coming to an end. This, coupled with the ongoing risk of an escalation in the Israel-Gaza conflict and overall economic uncertainty, is expected to provide support for the safe-haven appeal of gold.In terms of economic data, China’s trade balance has shown a significant decline from $77.71 billion to $56.53 billion in October, reaching its lowest level since May 2022. This decline is attributed to an unexpected surge in imports and a drop in Chinese exports, suggesting deteriorating overseas demand, particularly from major trading partners in Europe and the US.

Silver Analysis:

XAGUSD Silver Price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Minneapolis Federal Reserve President Neel Kashkari expressed the view that further tightening of monetary policy may not be effective in curbing inflation. He highlighted the resilience of the US economy, with steady job growth, improving unemployment rates, and GDP numbers. Kashkari also noted that the rate hikes implemented thus far have yielded positive results, considering the data from the US domestic front.

Minneapolis Federal Reserve Bank President Neel Kashkari, during an interview with the Wall Street Journal on Monday, expressed a preference for erring on the side of tightening monetary policy more than necessary rather than risking not doing enough to bring inflation down to the central bank’s 2% target. He emphasized that a conservative approach to policy tightening would not be effective in achieving the 2% inflation target within a reasonable timeframe. Kashkari noted that certain price and wage data suggest that inflation may be settling at a level above 2%. He highlighted the need for additional information to make well-informed decisions regarding future interest-rate adjustments.

Kashkari acknowledged the resilience of the economy and the positive developments in inflation, indicating that progress has been made in addressing inflationary concerns while maintaining a strong job market. However, he emphasized that there is still work to be done by the Federal Reserve to effectively control inflation. He also pointed out that American consumers continue to exhibit spending behavior. Despite these positive aspects, Kashkari remained cautious about prematurely declaring victory over inflation, as the U.S. economy appears to be ahead of foreign economies in terms of its economic performance and inflation control efforts.

USDJPY Analysis:

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Bank of Japan Governor Ueda has stated that the ultra-accommodative monetary policy will be maintained throughout the current year. The concern is that declining inflation may negatively impact the market, and thus, the policy aims to safeguard the Japanese economy from potential downturns. Japanese Yen persistently weakened by the Bank of Japan’s (BoJ) hyper-dovish policy stance. BoJ Governor Kazuo Ueda confirmed on Monday that the Japanese central bank would maintain its hyper-accommodative monetary policy approach. Despite increasing the upper limit on their Yield Curve Control mechanism, the BoJ reiterated its commitment to purchasing Japanese government bonds in whatever quantity necessary to tightly control the yield curve.

The BoJ also expressed concerns that inflation and wage growth would fall below the central bank’s target levels, vowing to keep the doors open to an easy monetary policy stance to support the Japanese economy.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc is experiencing a decline following last week’s relatively mild inflation data. Additionally, the situation in Israel has calmed more quickly than anticipated, leading to reduced demand for safe-haven currencies in the market.

The dynamics of USDCHF price movements have been primarily influenced by the rising US bond yields, which have provided support to the US Dollar, restricting the downside potential for the currency pair.On Monday, the US Dollar is regaining strength following a notable decline last week, driven by dovish expectations regarding the Federal Reserve (Fed) after its decision last Wednesday. The Fed chose to maintain interest rates at the range of 5.25-5.50%, with Chair Powell indicating that monetary policy might be nearing its endpoint. In response to this announcement, US Treasuries experienced a sharp drop, contributing to the downward trajectory of the USDCHF pair. The decline was further exacerbated by weak labor market data released on Friday, which included reports of a slowdown in US job creation in October and an increase in the unemployment rate.

During Monday’s trading session, the yields on 2-year, 5-year, and 10-year US Treasuries rebounded from multi-week lows, rising to 4.90%, 4.58%, and 4.64%, respectively. This increase in yields provided a boost to the US Dollar. Looking ahead, the focus for the rest of the week will be on various Fed officials who will be making public statements, allowing investors to continue forming their expectations for future Fed decisions. As of now, the CME FedWatch tool suggests that the probability of a 25 basis points rate hike at the upcoming December meeting has declined by nearly 10%. Chair Powell is scheduled to speak on Wednesday.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

In September, Germany’s industrial production saw a year-on-year decline of -3.7%, compared to a -2.0% drop observed in August.

According to official data released on Tuesday, Germany’s Industrial Production continued its downward trend in September, indicating a weakening manufacturing sector. The federal statistics authority, Destatis, reported a month-on-month decrease of 1.4% in industrial output for the Eurozone’s economic powerhouse, after adjusting for seasonal and calendar effects. This figure was significantly lower than the expected -0.1% and the -0.2% recorded in August. On an annual basis, German Industrial Production experienced a sharper decline of 3.7% in September compared to a 2.0% drop in August.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Economists at UOB have suggested that the ECB may opt to maintain the interest rate until the December meeting, taking into account the previous quarters’ CPI data and GDP growth trends.

Lee Sue Ann, an economist at UOB Group, analyzed the recent European Central Bank (ECB) monetary policy meeting. In October, the Consumer Price Index (CPI) saw a year-on-year increase of 2.9%, a notable decrease from the previous reading of 4.3%, and it was lower than the anticipated 3.1%. Core CPI also showed a decrease to 4.2% year-on-year, down from the previous 4.5%. On a month-on-month basis, inflation in the Eurozone registered at 0.1%, falling below the consensus forecast and the previous month’s 0.3%.

Looking ahead, we anticipate inflation to reach 5.6% in 2023 and then moderate to 2.7% in 2024. However, Eurozone GDP exhibited a slight contraction of 0.1% quarter-on-quarter in the third quarter of 2023, following a revised 0.2% gain in the second quarter (previously +0.1%). Compared to the same quarter in the previous year, seasonally adjusted GDP increased by 0.1%, down from the 0.5% gain seen in the second quarter of 2023. Our current outlook maintains expectations for the Eurozone economy to expand by 0.5% in 2023 and 0.8% in 2024.

Given the recent economic developments, including the growth and inflation figures, it appears that the ECB has solid reasons to maintain its current stance. During its October meeting, the ECB chose to keep its three key interest rates unchanged. The next significant decision point for the ECB will be on December 14th, which marks its final monetary policy meeting of the year. Given the already tight financing conditions and the slowing economic growth, our expectation is that the ECB will opt to keep interest rates at their existing levels for the time being.

GBPUSD Analysis:

GBPUSD has broken the Descending channel in upside

The Bank of England has indicated that there is an increased likelihood of the UK economy entering a recession in the coming year. This statement has led to a decline in the value of the GBP against the USD. It’s worth noting that the Bank of England’s decision to keep interest rates unchanged in last week’s meeting is also a noteworthy development.

The US Dollar is currently extending its recovery from a recent low, spanning nearly eight weeks, and is exerting pressure on the GBPUSD pair. Despite the prevailing belief that the Federal Reserve has concluded its interest rate hikes, less dovish remarks from Federal Open Market Committee members led to a notable uptick in US Treasury bond yields on Monday. Additionally, a somewhat pessimistic global risk sentiment, as evidenced by a subdued tone in equity markets, is bolstering the safe-haven appeal of the US Dollar.

In contrast, the British Pound is facing downward pressure due to the Bank of England’s gloomy economic outlook, which suggests a potential recession in the UK economy next year. However, the downside potential appears limited, as traders await fresh insights into the Fed’s future interest rate trajectory before determining the next direction for the pair.

As a result, market focus will remain on speeches by influential FOMC members, particularly Fed Chair Jerome Powell, scheduled for Wednesday and Thursday. Meanwhile, a further decline in US Treasury bond yields could cap additional gains for the US Dollar and help mitigate downside pressure on the GBPUSD pair. In the absence of significant market-moving economic data releases from either the UK or the US, the current fundamental landscape suggests it would be prudent to wait for strong follow-through selling before confirming that the pair has reached its peak.

CADCHF Analysis:

CADCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

The Canadian Ivey Purchasing Managers’ Index (PMI) data for October revealed a reading of 51.9, down from the September figure of 54.2. Subsequently, the Canadian Dollar depreciated following the release of this data.

The Canadian Dollar is retracing some of its gains from Friday as it enters a week with relatively sparse economic data. On Monday, Canada’s Ivey Purchasing Manager Index (PMI) figures fell short of expectations, but they continue to indicate growth, remaining above the 50.0 threshold for the time being. The non-seasonally-adjusted October Ivey PMI for Canada registered at 51.9, down from September’s 54.2. However, the seasonally-adjusted October Ivey PMI showed a firmer reading of 53.4, improving upon the previous month’s 53.1 but still missing the market’s median forecast of 54.0.

data for October revealed a reading of 51.9, down from the September figure of 54.2")

The economic calendar for the Canadian Dollar this week features limited data of significant importance. On Tuesday, there will be low-impact data on Canadian Trade Balance for September and a mid-tier speech from the Bank of Canada’s Deputy Governor Sharon Kozicki. Additionally, Canada Building Permits data for September will be released. In terms of commodities, Crude Oil is experiencing a modest increase on Monday, with West Texas Intermediate Crude Oil prices rising from the week’s opening level of $80.65 to reach $82.00 per barrel.

AUDCHF Analysis:

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

In the November RBA monetary policy meeting held today, there was a decision to raise the interest rate by 25 basis points, moving it from 4.10% in the previous meeting to 4.35%. This move was influenced by the increase in CPI data for the third quarter and a rise in retail spending, which prompted the RBA to implement the rate hike in this meeting.

Despite the Reserve Bank of Australia raising interest rates by 25 basis points on Tuesday, the Australian Dollar continues to weaken. After maintaining the benchmark interest rate unchanged for four consecutive meetings, Australia’s central bank has initiated a tightening of monetary policy by raising the Official Cash Rate from 4.10% to 4.35%. This move by the RBA may be in response to recent Consumer Price Index data, which revealed third-quarter inflation exceeding market expectations. Furthermore, Australia’s seasonally adjusted Retail Sales (MoM) for September surpassed predictions. Investors are closely monitoring RBA Governor Michele Bullock’s commitment to this recent hawkish stance, as it suggests potential future interest rate hikes. Additionally, major Australian banks, including ANZ, CBA, Westpac, and NAB, have adjusted their forecasts to anticipate an RBA rate hike in response to rising inflation and hawkish statements from RBA policymakers.

China’s Trade Balance data for October showed a decrease in the surplus balance, contrary to market expectations of an improvement. Exports experienced a more significant decline than anticipated, surpassing both expectations and the previous decline. The RBA has resumed its policy tightening by raising the Official Cash Rate from 4.10% to 4.35% after maintaining the benchmark interest rate unchanged for four consecutive meetings.

In terms of economic data, Australia’s TD Securities Inflation decreased to 5.1% in September from the previous 5.7%. Australia’s Retail Sales improved to 0.2% in the third quarter, rebounding from the previous reading of -0.6%. Aussie Trade Balance (Month-on-Month) fell to 6,786M in September, falling short of the expected 9,400M and lower than the previous figure of 10,161M. Over the twelve months leading up to September 2023, Australia’s monthly Consumer Price Index recorded a 5.6% increase. However, the quarterly inflation rate dipped to 5.4% year-on-year in Q3. China’s Trade Balance data for October revealed a decrease in the surplus balance to $56.53 billion, contrary to market expectations of an improvement to $81.95 billion from the previous $77.71 billion. Exports experienced a more significant decline of 6.4%, exceeding the expected decline of 3.1%.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market is rebounded from the lower low area of the channel

The Reserve Bank of New Zealand has decided to keep interest rates unchanged in response to the rise in the unemployment rate to 3.9% and the recent deceleration in labor growth. The New Zealand Dollar strengthened against the US Dollar primarily due to weakness in US domestic data.

US Treasury bond yields have risen, pulling the US Dollar closer to its Monday opening levels, as reflected in the US Dollar Index. The economic calendar for the United States (US) this week is relatively light, featuring updates on the Balance of Trade, IBD/TIPP Economic Optimism, unemployment claims, and consumer sentiment. In addition to economic data releases, several US Federal Reserve officials are scheduled to make statements, starting with Lisa Cook on Monday, followed by Michael Barr, Jeffrey Schmid, and Christopher Waller on Tuesday.

It’s worth noting that following last week’s Fed decision, there is anticipation of potential pushback from Fed officials against market expectations of a 100 basis points rate cut by the end of next year. One of the justifications for keeping rates unchanged in the previous Fed decision was the elevated yields at the longer end of the yield curve. Many Fed officials argued that these yields were tightening monetary conditions and serving their intended purpose. However, since the Fed’s decision, the yields on 20-year and 30-year US bonds have dropped by more than 30 basis points, suggesting that investors believe the Fed has completed its rate hike cycle.

It appears that market participants may have overreacted to last week’s US Nonfarm Payrolls report, which showed the addition of 150,000 jobs in October, falling short of the 180,000 forecast and revising September’s figure downward to 297,000. While the labor market is showing signs of easing, it’s essential to note that this report represents only the second instance in eleven months that job growth has missed expectations. On the New Zealand front, the direction of the New Zealand Dollar will be influenced by the New Zealand Business PMI data. However, it’s worth mentioning that a soft labor market and cooling wage growth may restrain the Reserve Bank of New Zealand from raising interest rates beyond the current 5.50% threshold.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/