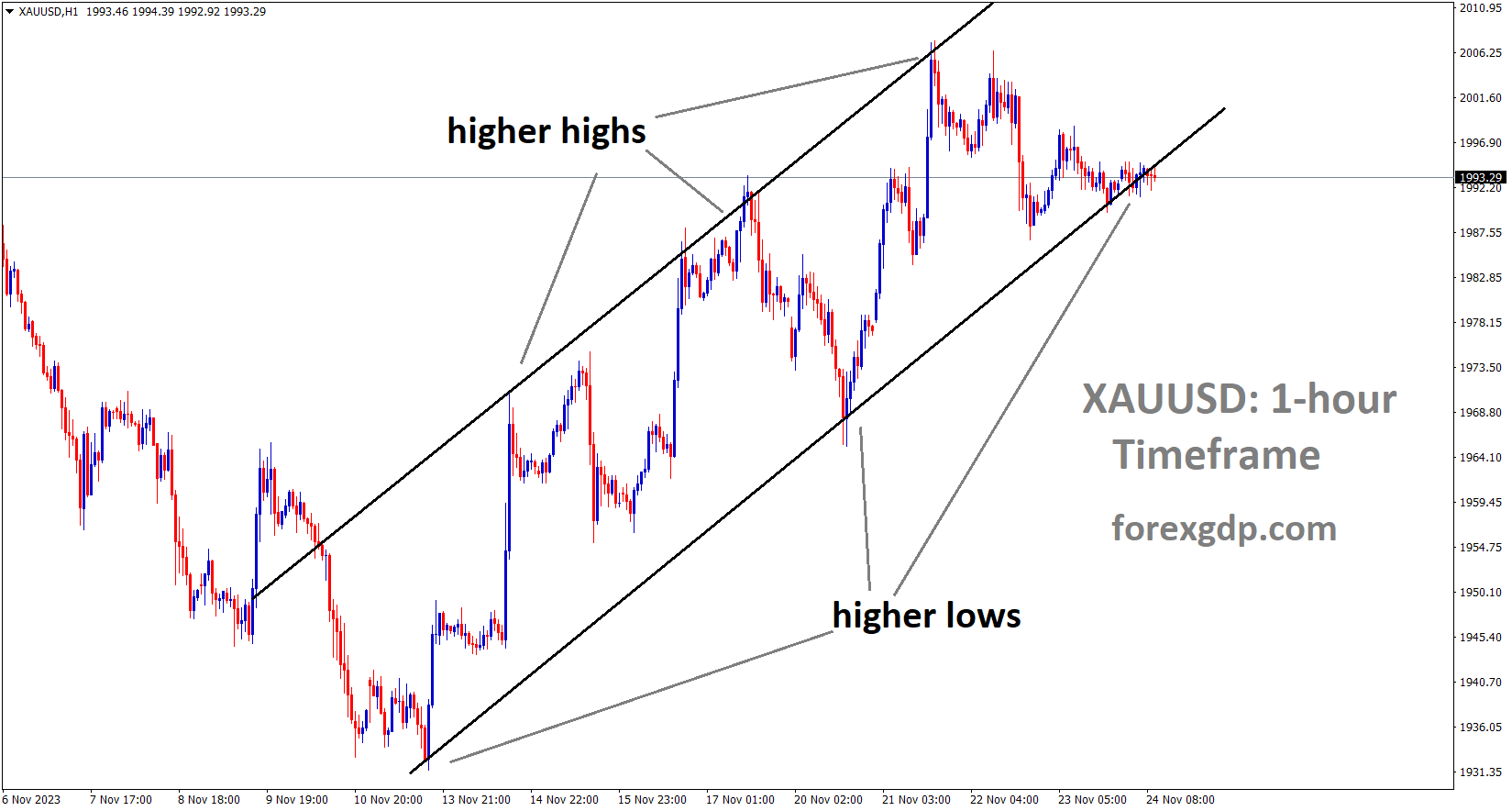

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices are experiencing a lack of significant movement during the current week due to US market holidays. With Thanksgiving Day on Thursday and an additional holiday on Friday, market volume is notably thin, resulting in minimal fluctuations in gold prices.

On Thursday, the price of gold experienced modest gains, influenced by a weaker US Dollar, yet it failed to sustain upward momentum and remained below the psychologically significant $2,000 mark. Despite indications of easing inflationary pressures, the recently released FOMC minutes on Tuesday conveyed a more hawkish tone. Furthermore, positive data on the US labor market and consumer sentiment on Wednesday could potentially empower the Federal Reserve to maintain higher interest rates for an extended period. This, coupled with a notable rise in US Treasury bond yields, emerges as a pivotal factor supporting the non-yielding gold price as the week concludes. However, prevailing market sentiment suggests a belief that the Fed is more likely to maintain steady interest rates rather than implementing hikes. Consequently, this sentiment does not contribute to any substantial buying of the US Dollar, preventing it from capitalizing on this week’s rebound from its lowest level since August 31.

In addition to these dynamics, a generally weaker tone in equity markets is reinforcing support for the safe-haven appeal of gold. Despite this, the XAUUSD is on course to register its second consecutive weekly gain as traders await potential market-moving insights from the flash US PMIs. As the Asian session unfolds on Friday, a confluence of divergent forces fails to impart significant momentum to the price of gold, resulting in subdued and range-bound price action. The disparity between the Federal Reserve’s hawkish stance and market expectations for rate cuts in 2024 is impeding traders from making decisive moves regarding XAUUSD. The FOMC meeting minutes from Tuesday underscored policymakers’ commitment to keeping interest rates higher for an extended period to mitigate inflation. However, the absence of expectations for a rate hike in December, as revealed by the October inflation report, and a market pricing in over a 25% chance of a rate cut as early as March 2024, are contributing to the uncertainty. While positive data on the US labor market and consumer sentiment, alongside rising US Treasury bond yields, support the US Dollar, dovish Fed expectations warrant caution among USD bulls. This cautious sentiment might persist and continue to provide some support to the commodity as traders await the flash US PMI releases for November.

SILVER Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Due to the observance of Thanksgiving Day in the US, the market was closed yesterday and remains closed today. Consequently, trading is occurring with limited volume. The release of US Global PMI data is scheduled for later this evening.

The US Dollar is trading sideways to lower. Despite the Greenback’s favorable position on Wednesday, poised to recover losses for the week, it experienced a significant reversal in the final trading hour before the US bank holiday. With no trading activity in the US, the Asian and European markets are exerting downward pressure on the US Dollar Index, making a weekly loss appear almost inevitable. The current day features a sparse economic calendar, devoid of any US data releases. European Purchase Managers Index numbers have already been disclosed, preceding the anticipated US PMI figures for Friday. Although the European PMI figures still indicate contraction, remaining below the 50 threshold, they exhibit a notable improvement compared to October. If Friday’s US PMI numbers show a decline, the changing dynamics between European and US PMIs may contribute to further depreciation of the Greenback. Preliminary readings for November indicate an uptick in European PMIs from the lower levels observed in October.

The ceasefire agreement in Gaza has been postponed by a day, set to take place on Friday. A car explosion on the Canada-US border has been deemed an accident with no terrorist motive involved. Chinese support and funding on Wednesday led to a nearly 7% surge in the Chinese property sector. Joachim Nagel, a member of the European Central Bank (ECB), expressed uncertainty in morning comments about whether the ECB has reached its peak rates. Nagel suggested that rates may need to stay higher for an extended period, considering the potential for a rapid resurgence of inflation in the coming months. Equities are experiencing mild gains on this US holiday, with the Chinese Hang Seng notably up 1% nearing its closing bell. European equities are seeking direction, while US equity futures show marginal gains in their half-day trading session due to the ongoing US holiday. The CME Group’s FedWatch Tool indicates a 97.8% likelihood that the Federal Reserve will maintain unchanged interest rates at its December meeting. Interestingly, a small percentage (2.2%) of the market is speculating on the possibility of a rate hike. The 10-year US Treasury Note yield has paused at 4.40%.

USDCAD Analysis:

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Canadian Dollar declined against its counterparts as oil prices remained subdued in the market, reflecting a decrease in tension related to the war conflict. Bank of Canada Governor Tiff Mackhlem stated that there is no necessity for rate hikes if concerns about demand decrease and inflation figures are reduced.

The OPEC+ Meeting originally set for November 26 has been rescheduled to November 30. This adjustment is attributed to increased divergence among OPEC+ nations regarding the agreement on supply cuts, necessitating more time to reach unified decisions.

The drop in the price of crude oil in the previous session put pressure on the Canadian dollar, and this could be explained by the unannounced postponement of an OPEC+ meeting. Nevertheless, by press time, the price of Western Texas Intermediate has recovered from its recent losses, trading higher at $76.50 per barrel and providing some minor support for the Loonie Dollar (CAD). This delay has added to market uncertainty by creating uncertainty about the OPEC+ alliance’s future decisions and actions.

In a recent speech, Governor Tiff Macklem of the Bank of Canada (BoC) indicated that policymakers might have taken enough action to control inflation and maintain economic equilibrium. Conversely, a risk-on attitude is encouraged by the growing probability that the Federal Reserve will not raise interest rates further, which could weaken the USDCAD pair. Encouraged by the improvement in US Treasury yields, the US Dollar Index recovers some of its recent losses and is now trading higher at 103.80. The yield on US 2-year and 10-year bonds has increased to 4.94% and 4.46%, respectively. Looking ahead on the economic calendar, Friday’s release of the US S&P Global PMI data is anticipated, with a slight expected decline in November. Investors will be closely observing these numbers in order to gain insight into how important US economic sectors are performing.

According to Reuters, the Organization of the Petroleum Exporting Countries (OPEC) and its allies are set to conduct their upcoming meeting virtually on November 30. The initially scheduled meeting to address discussions on oil output cuts, which was slated for November 26, has been postponed to November 30. This delay is attributed to the inability of producers to reach a consensus on production levels and potential supply cuts.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

The Swiss Franc has weakened against its counterparts following the announcement by the Swiss National Bank that foreign exchange reserves have decreased from 950 billion francs in 2022 to 657 billion francs. The employment level for Q3 in Switzerland is set to be released today.

The US Dollar is facing downward pressure as market participants express skepticism about the possibility of additional interest rate hikes by the Federal Reserve, potentially impacting the USDCHF pair.

Meanwhile, the Swiss Franc might encounter its own downward pressure following an announcement from the Swiss National Bank, revealing that the central bank’s currency reserves have hit a seven-year low of CHF 657 billion. This signals the ongoing efforts by the SNB to repatriate its foreign currency reserves, marking a gradual reduction from the peak of CHF 950 billion in 2022.

EURCHF Analysis:

EURCHF is moving in the Box pattern and the market has rebounded from the support area of the pattern

The US Dollar Index, which gauges the USD’s performance against six major currencies, is consolidating around 103.70, carrying a negative sentiment in anticipation of Friday’s release of US S&P Global PMI data. There’s an expected slight decline in the Services sector from 50.6 to 50.4 and in the Manufacturing sector from 50.0 to 49.8. Investors are keenly watching these figures for insights into the performance of key sectors in the US economy. US Treasury yields have shown improvement during the Asian session on Friday, following the Thanksgiving holiday in the United States, attempting to push the Greenback into positive territory. As of the current moment, the yields on US 10-year and 2-year bond coupons stand at 4.46% and 4.94%, respectively. Investors are closely monitoring these yield movements for potential impacts on the overall strength of the US Dollar.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The German Manufacturing PMI surpassed expectations by registering at 42.3, exceeding the forecast of 41.2. Similarly, the Services PMI came in at 48.7 compared to the forecasted 48.5, and the Composite PMI reached 47.1, surpassing the expected 46.5. Germany has successfully overcome the recession in 2023, as evidenced by the last quarter’s GDP figures remaining flat.

Preliminary data for German manufacturing PMI exceeded expectations, registering at 42.3, surpassing the consensus estimate of 41.2. This marks a partial recovery from a consistent contraction. The services sector also outperformed predictions, with a figure of 48.7 compared to the anticipated 48.5. While this slight improvement doesn’t significantly alter Germany’s economic outlook, it may indicate a less severe GDP contraction expected in Q4. There’s a possibility of a return to growth for the aggregated reading, the composite data point, before the second half of next year, although growth remains weak. Remarkably, Germany managed to avoid a technical recession in 2023, as prior quarterly GDP prints had indicated stagnant or even negative growth.

EURJPY Analysis:

EURJPY has broken the Descending channel in upside

The October Japanese Consumer Price Index recorded a 2.9% reading, slightly below the expected 3.0% but higher than the previous month’s 2.8%. Following the release of this data, the Japanese Yen appreciated.

The Japanese Yen has clawed back some of its recent losses, with ongoing support stemming from growing expectations of a shift in the Bank of Japan’s policy stance. Japan’s headline and core inflation rates have consistently exceeded the BoJ’s 2% target for the past 19 months. Anticipation of significant pay hikes in the coming year further bolsters the outlook for sustained and stable inflation, fueling speculation that the BoJ will likely abandon its negative rate policy in early 2024.

Friday’s government data revealed that Japan’s nationwide core Consumer Price Index, excluding volatile fresh food costs, rose 2.9% year-on-year in October, slightly below the anticipated 3.0%. However, this figure has consistently exceeded the BoJ’s 2% target for over a year, underscoring the persistence of inflationary pressures in the country. The core-core index, excluding fresh food and fuel costs, eased from 4.2% in September to 4.0% in October but remains close to a 40-year peak. The headline Consumer Price Index accelerated from 3% in the previous month to a 3.3% year-on-year pace in October.

Furthermore, expectations of another significant round of pay hikes by Japanese firms in the coming year could drive consumer spending and demand-driven inflation, potentially prompting the BoJ to reconsider its stance. The flash Japan Manufacturing PMI dipped to 48.1 in November from the previous 48.7, remaining below the 50.0 threshold that distinguishes contraction from expansion since June. Investors are now eagerly awaiting the release of the flash US PMI prints later in the North American session for potential short-term trading opportunities as the week draws to a close.

EURNZD Analysis:

EURNZD is moving in the Box pattern and the market has reached the support area of the pattern

A coalition government has been established in New Zealand comprising three parties. Their initial agenda involves amending the RBNZ Act of 2021 to eliminate the dual mandate related to immigration and employment changes, opting instead for the implementation of the price stability method of process.

Following over a month of discussions regarding ministerial positions and policy matters, the National Party of New Zealand has successfully reached an agreement with ACT New Zealand and New Zealand First to establish the nation’s upcoming three-party coalition government, as reported by Reuters. The coalition has unveiled a set of policy reforms, notably addressing the functions of the Reserve Bank of New Zealand. As part of these reforms, the government plans to modify the Reserve Bank of New Zealand Act 2021, eliminating the dual mandate related to inflation and employment and refocusing the bank’s objectives solely on ensuring price stability.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The UK experienced a surge in its Services PMI, Manufacturing PMI, and composite PMI figures, surpassing expectations and strengthening the GBP against its counterparts. The slowdown in inflation has provided support to both the manufacturing and services sectors. Economists anticipate that the GDP for the final quarter of 2023 is likely to remain flat.

It seems like the latest UK S&P Global PMIs (Purchasing Managers’ Index) have shown positive signs for the economy. The services sector, in particular, has contributed to this improvement, breaking a three-month sequence of decline. Tim Moore, the economics director at S&P Global Market Intelligence, mentioned that the UK economy “found its feet again” in November, and manufacturers reported less severe cutbacks to production schedules.

have shown positive signs for the economy")

Several factors are contributing to this positive trend. The pause in interest rate hikes and a slowdown in headline measures of inflation are providing relief and supporting business activity. However, it’s noted that the survey data suggests a broadly flat UK GDP in the final quarter of 2023. This could indicate that while there is improvement, there are still concerns about overall economic growth and inflation in the coming months.

Despite these concerns, the release of the data had a positive impact on Sterling traders, leading to an increase in the value of the Pound. This suggests that, at least in the short term, market participants are taking a positive view of the economic situation based on the latest PMI figures. It’s important to keep in mind that economic conditions can be influenced by various factors, and the situation may evolve over time.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Judo Bank witnessed lower-than-expected Manufacturing PMI and Services PMI figures yesterday. However, China’s positive outlook on the economy is bolstering Australian exports. The Reserve Bank of Australia is anticipated to implement the next rate hike in March 2024.

The morning saw a disappointing start for the Australian dollar due to underwhelming PMI data. Both Judo Bank’s manufacturing and services metrics hit yearly lows, pushing further into contractionary territory. Despite this, the impact of the Reserve Bank of Australia’s meeting minutes persists, as the board reiterated concerns about inflation and the potential for additional interest rate hikes.

Some positive news from China contributed to the upside for the Australian dollar, as Beijing announced financial aid for distressed property developers. Coupled with a lower trading greenback and the optimistic Chinese developments, key Australian commodity exports are on the rise, providing support for the Aussie dollar.

There’s been a noticeable shift in rate expectations, with a higher probability of a rate hike in 2024. On the flip side, from a U.S. dollar perspective, markets responded negatively to yesterday’s lower durable goods orders and Michigan consumer sentiment, despite a pullback in initial jobless claims. Considering that it’s Thanksgiving Day in the U.S., it’s anticipated that there will be minimal volatility and lower trading volume across financial markets. As a result, the currency pair is likely to remain relatively subdued.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/