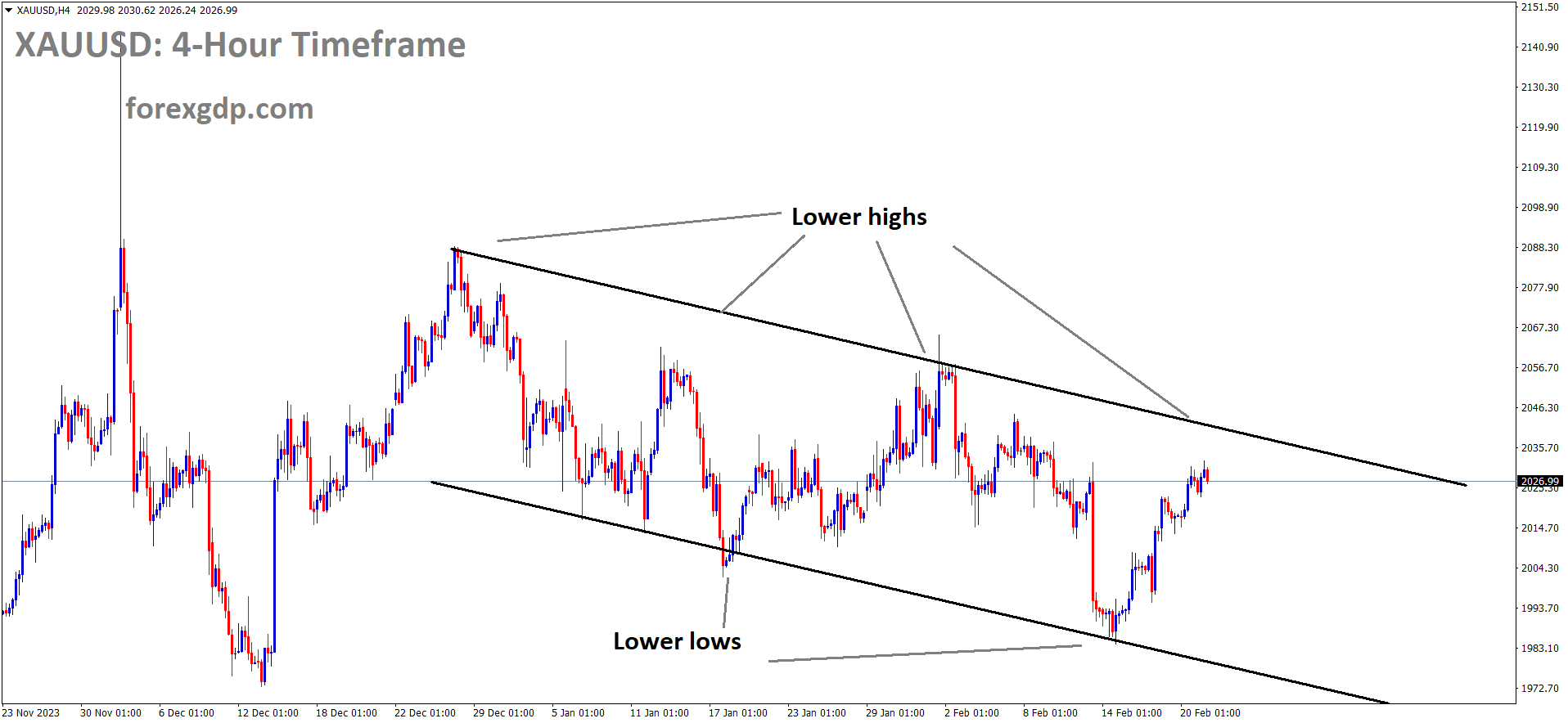

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Fed policymakers said inflation rates will be lowered in the longer term, so the rate of interest will be neutral or hold for some time. This news is positive for Gold because to holding of locker cost will remain the same at some times.

GOLD – XAUUSD Surges on Fed’s Long-Term Inflation Outlook

Fed policymakers said inflation rates will be lowered in the longer term, so the rate of interest will be neutral or hold for some time. This news is positive for Gold because to holding of locker cost will remain the same at some times.

Gold Outlook Strengthens as Fed Downplays Inflation Concerns

– Fed policymakers’ confidence in long-term inflation decline reduces the opportunity cost of holding non-yielding assets like Gold.

– Investors anticipate cues on three forecasted rate cuts in the FOMC minutes from the first 2024 monetary policy meeting.

– Preliminary S&P Global PMI data for February will influence Gold price and USD; US Manufacturing PMI expected to exceed the 50.0 threshold.

Market Update: Gold Price Rises ahead of Fed Minutes

– Gold extends gains, reaching over $2,023 amid concerns of prolonged higher interest rates by the Federal Reserve.

– Persistent fears stem from elevated core inflation data in the United States, nearly double the 2% target rate, dampening hopes for pre-June rate cuts.

– CME FedWatch indicates confidence in unchanged interest rates (5.25%-5.50%) until May; 53% chance of a 25 bps rate cut in June.

– Despite January’s inflation data, Fed policymakers downplay one-time high inflation, emphasizing the decline in the longer-run inflation trend.

– US Dollar Index hovers around 104.20 as investors await Wednesday’s release of FOMC minutes for insights into the January policy meeting.

– FOMC minutes expected to elaborate on the decision to maintain current interest rates; Powell emphasizes the need for continued positive data to ease price pressures.

– 10-year US Treasury yields, reflecting Fed policy expectations, see a slight increase to around 4.30%.

EURUSD – Surpasses 1.0800 on Surprise EU Current Account Surplus

The EU’s trade account surplus came at EUR 31.9 billion from EUR 22.5 billion in the December month. This surplus shows 1.8% of the bloc’s GDP from the deficit of 0.60% in the previous year.

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Wage settlement data announced from the ECB, Q4 2023 wage data dipped to 4.7% from 4.5% in the previous quarter.

EUR/USD Rises on Strong EU, Focus on Fed Minutes

– EU’s Current Account surplus in December exceeds estimates, rising to EUR 31.9 billion.

– ECB’s wage settlements indicator for Q4 2023 dips to 4.5% from 4.7% YoY; wage data crucial for ECB’s monetary easing decisions.

– Lagarde suggests monitoring wage data for timing of monetary easing; analysts point to June as likely for rate cut.

– US economic docket light, with the Leading Index for January expected to drop by 0.3% MoM.

– Wednesday brings the release of the FOMC minutes and Fed speakers.

USDCHF – Retreats to 0.8810 on Enhanced Swiss Trade Surplus, Weaker US Dollar

Swiss Trade balance data for January shows a trade surplus of 4738 million francs and it is higher than 1271 million Swiss francs. Exports data rose to 22804 million in January from 18788 in the previous month, Imports rose to 18067 million in January from 17517 in the previous month.

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

USD/CHF Declines on Positive Swiss Trade Balance and Weaker US Dollar

– Risk sentiment improves after positive Swiss Trade Balance figures on Tuesday.

– January trade surplus of 4,738 million, higher than December’s 1,271 million.

– USD/CHF dips near 0.8810 in the European session.

– Swiss Exports (MoM) rise to 22,804 million, Imports (MoM) increase to 18,067 million.

– Employment Level for Q4 to be released on Friday.

– Weaker US Dollar, attributed to declining US Treasury yields, adds to downward pressure on USD/CHF.

– Greenback attempts to halt losing streak amid fading expectations of Federal Reserve rate cuts in March and May.

Recent data indicates that both consumer and producer prices in the United States (US) continue to rise, potentially delaying the Federal Reserve’s early policy tightening. ANZ anticipates that the Federal Reserve (Fed) will commence rate cuts starting in July 2024.

The CME FedWatch Tool suggests a 53% chance of a 25 basis points rate cut by the US Fed in the June meeting. Traders are expected to closely monitor the Federal Open Market Committee’s (FOMC) minutes for the January meeting, set to be released on Wednesday.

USDCAD – Rebounds as Canadian CPI miss weighs on CAD

Canadian CPI data for January came at 2.9% versus 3.3% expected and 3.4% printed in December month. The Canadian Dollar moved lower after the data was printed. Core CPI printed at 2.4% versus 2.6%.

USDCAD is moving in the Ascending triangle pattern and the market has reached the resistance area of the pattern

Below-forecast Canadian inflation weakens CAD broadly.

Thursday brings Canadian Retail Sales data, with markets shifting attention to the Federal Reserve and the Federal Open Market Committee (FOMC). The latest FOMC Meeting Minutes will be released on Wednesday.

USD/CAD at 1.3500 as Canadian inflation dips; Investors eye FOMC and Retail Sales

– Canadian CPI drops to 2.9% in January, below the forecast of 3.3%

– Monthly CPI unexpectedly at 0.0%, missing the expected 0.4% rebound

– BOC’s CPI Core for January declines to 2.4% from 2.6%

– FOMC Meeting Minutes on Wednesday sparks expectations for Fed rate cuts

– CME’s FedWatch Tool indicates 60% chance of no May rate cut, 80% odds for a 25 basis point cut in June

– Thursday’s Canadian Retail Sales anticipated to bounce in December; MoM Retail Sales expected at 0.8% and Retail Sales Excluding Automobiles forecast to recover to 0.7% from -0.5%.

USD Index – Fitch Ratings: US GDP Growth Up, German Contraction in 2024

The Fitch rating agency used the new mixed-data sampling regression model and predicted the forecast of Global economies like the US, Japan, and Europe. The model shows the US GDP at 0.60% qoq compared to December 2023, and Germany contracted at -0.10% qoq.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

Fitch Ratings Updates ‘Nowcast’ Models: US GDP Growth Raised to 0.6% QoQ, German Growth at -0.1% QoQ

The improved framework introduces fresh nowcast models for the US, Japan, and the ‘Big4’ economies in the eurozone (Germany, France, Italy, and Spain).

Utilizing a mixed-data sampling (MIDAS) regression model, the new methodology employs monthly indicators to forecast GDP growth.

The updated models reveal an optimistic deviation for US GDP at 0.6% QoQ (non-annualized), in contrast to our Global Economic Outlook report from December 2023, and an adverse surprise for Germany at -1.0% QoQ.

AUDUSD – Retreats from 0.6580 Following RBA-Driven Surge

Australian Dollar gained after the RBA meeting minutes shows rate cuts will be delayed, rate hikes and neutral stance are more in the near term. Service inflation and tight labour growth cause the RBA to hold the rates in the near term.

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

RBA Keeps Rates Steady, Eyes on Fed’s Meeting Minutes

– RBA holds rates, but hints at possible future cuts if inflation progress is slow.

– Aussie (AUD) rises initially on potential rate hike, later retraces during US market hours.

– Focus shifts to Fed’s FOMC Meeting Minutes on Wednesday, with market anticipating potential interest rate cuts in June or July according to CME’s FedWatch Tool.

NZDUSD – NZ Producer Price Index Surpasses Expectations, Softens to 0.7%

NZ PPI data beat expectations but came below the previous quarter’s numbers. NZD PPI output came at 0.70% for the December month quarter versus a forecast of -0.40% and still down from 0.80% in the previous quarter. NZD PPI Input data came at 0.90% versus 0.40% expected and down from the previous quarter of 1.2%. NZ Dollar moved stronger against counter pairs after the result came.

NZDUSD has broken the Descending channel in upside

New Zealand’s Producer Price Index (PPI) surpassed expectations, exceeding forecasts for both Output and Input components, although it retreated from the previous quarter.

According to Stats NZ, the Output PPI increased by 0.7% in the quarter ending December, surpassing the predicted decline to 0.4%, but still lower than the previous quarter’s 0.8%. The Input PPI for the same period stood at 0.9%, exceeding the expected 0.4%, yet falling short of the previous figure of 1.2%.

Stats NZ highlighted that major contributors to Output PPI were dairy cattle farming, up by 7.3%, and real estate services, rising by 1.1%, partially offsetting a 4.5% decline in dairy product manufacturing.

On the Input PPI front, prices for dairy product manufacturing increased by 5.5%, while electrical and gas supply prices climbed by 5.8%. Basic chemical and chemical product manufacturing also contributed, adding a further 2.8%.

GBPJPY – Levels Off post BoE Bailey’s Remarks, Bullish Outlook Remains

GBP pairs moved stronger after the Bank of England Governor Bailey said rate cuts are possible this year even if inflation won’t come near our target. But Bank of Japan did not give a clear path for rate decisions. Most probably rate cuts are expected from the BoE in August month from the economists’ side.

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

Factors influencing the pair include ongoing shifts in the UK and Japanese financial and economic landscapes, impacting the monetary policy decisions of the Bank of England (BoE) and the Bank of Japan (BoJ).

The BoE expresses caution about the resilient local economy, with Governor Andrew Bailey suggesting the possibility of rate cuts before inflation reaches target levels. Currently, markets anticipate the first rate cut in the August meeting, but incoming data will determine the timing of the easing cycle. The BoJ, on the other hand, provides no clear signals on exiting its ultra-loose policy.

AUDJPY – Rises to 98.40 as Japan’s Total Trade Balance Declines Less Than Expected

The Ministry of Finance in Japan shows Japan’s trade surplus data, indicating a deficit of Yen 1758.3B in January from Yen 68.9B. Imports declined by 9.6% beating the estimate of an 8.4% decline. Exports surged by 11.9% beating the estimate of 9.5%.

AUDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

AUD/JPY Extends Winning Streak Amid RBA Optimism

– AUD strengthens against JPY after RBA meeting minutes, signaling reduced rate cut expectations.

– AUD/JPY trades around 98.40 in Asian hours on Wednesday.

– S&P/ASX 200 Index’s decline, influenced by mining stock and metal price losses, poses hurdles for the AUD.

– Mixed data on Australia’s Wage Price Index for Q4 has little impact on the AUD.

– Japan’s Ministry of Finance reports a Trade Balance figure better than expected, potentially supporting JPY and limiting AUD/JPY gains.

– Japan’s Merchandise Trade Balance Total shows a deficit of ¥1,758.3B in January, beating the anticipated ¥1,925.9B deficit.

– Imports (YoY) decline by 9.6%, exceeding the expected 8.4% drop, while Exports surge by 11.9% YoY, surpassing both the predicted 9.5% and the prior 9.7%.

– Japanese Finance Ministry official mentions discussions on FX intervention, providing some support for JPY.

XAGUSD – USD Hovers Near Multi-Week Low, Awaits FOMC Minutes for Momentum

Fed is expected to do rate cuts in Mid-2024 and four 25bps rate cuts in the year. The white House said the US is going to more sanctions against Russia due to the War progression of 2 years on Ukraine.

XAGUSD Silver price is moving in the Box pattern and the market has fallen from the resistance area of the pattern

USD Near Three-Week Low, Awaits FOMC Minutes for Direction

– USD under selling pressure, trades near lowest level in almost three weeks.

– USD Index (DXY) below 104.00 as traders await FOMC minutes for fresh impetus.

– Investors seek cues on Fed’s rate-cut path, impacting near-term USD trajectory.

– Growing acceptance of mid-2024 monetary policy easing and expectations of four 25 bps rate cuts in 2024 undermine the Greenback.

– Priced-out possibility of early rate cuts by the Fed, supported by signs of a healthy US economy and hawkish FOMC comments.

– Elevated US Treasury bond yields and a softer equity market tone may lend support to the safe-haven Greenback.

– PBoC’s decision to lower the five-year loan prime rate has short-lived market impact amid persistent geopolitical tensions.

– Attacks in the Red Sea raise risk of further military escalation in the Middle East.

– US plans major sanctions against Russia; DXY shows resilience below the 100-day SMA, cautioning against positioning for an extension of the pullback from a three-month top.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/