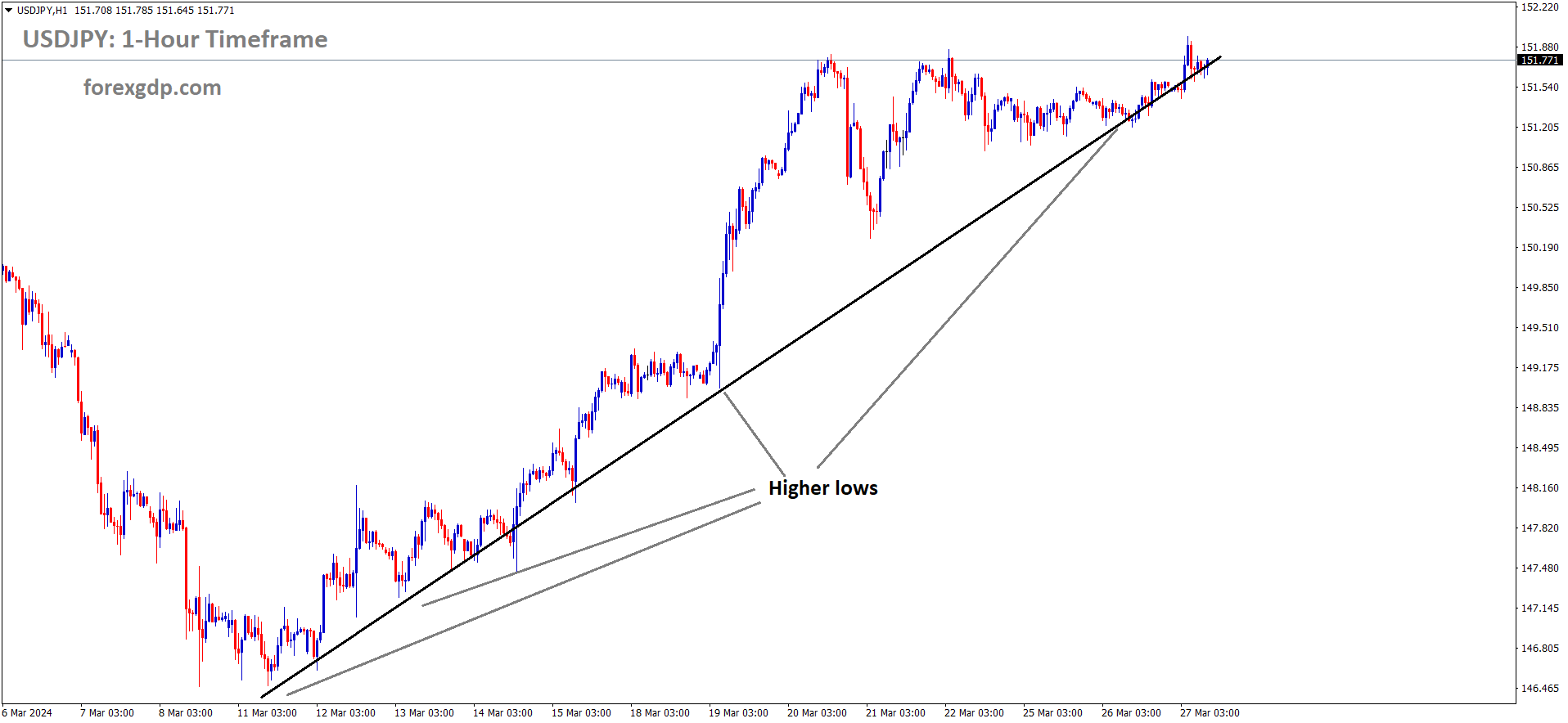

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

USDJPY – BoJ’s Ueda: Household sentiment brightens with wage hike expectations

The Bank of Japan Governor Ueda said House hold sentiment is going to improve on the expectations of wage hikes in the economy, we have to maintain accommodative policy for time period, when the Wage-inflation cycle turned positive we gradually cut the Bond buying operations and do rate hikes, it is purely based on Wages increases with price increase inflation in the Japan economy we expected. FX Levels is more impacted on the economy, prices, and business in the Japan.

BoJ Governor Kazuo Ueda remarked on Wednesday that “household sentiment is on the rise due to anticipated wage increases.” He refrained from discussing particular foreign exchange (FX) movements or levels but emphasized their substantial influence on the economy and prices. Ueda expressed the BoJ’s commitment to closely monitoring FX effects on the economy and prices, in collaboration with the government. Last week, he reiterated the intention to uphold an accommodative monetary policy, a statement that triggered significant selling of the Japanese Yen.

XAUUSD – Gold price holds steady despite robust US data and strong US Dollar

The Gold prices are steady in higher pace after the US Consumer confidence data came at104.7 from 104.8 from February month. US Core Durable goods came at 1.4% in February from -0.90% decline in January month , Even US Dollar doing stronger pace in the market, But Gold diminished the US Domestic data and rallying in the market due to Geopolitical tensions between Russia and Ukraine.

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Recent economic data from the United States indicates a notable rise in Durable Goods Orders, marking their highest level since 2022. However, Consumer Confidence shows a marginal decline in March, reaching its lowest level in four months. This decline is attributed to heightened prices and escalating borrowing costs.

Within the Federal Reserve, there exists a divergence of opinions regarding the prospect of interest rate cuts. While some members of the Federal Open Market Committee (FOMC) advocate for rate reductions, others express caution. Atlanta Fed President Raphael Bostic anticipates a single rate cut in 2024, diverging from the expectation of multiple cuts. Similarly, Fed Governor Lisa Cook echoes Bostic’s sentiment, emphasizing the risk of premature easing leading to entrenched inflation. Chicago Fed President Austan Goolsbee remains dovish, foreseeing the necessity for three rate cuts, contingent upon evidence of inflation moderating.

Market sentiment reflects a prevailing anticipation of a rate cut by the Federal Reserve, with money market traders assigning a 70% probability of a quarter-point reduction. This adjustment would set the federal funds rate (FFR) within the range of 5.00% to 5.25%.

Traders in the gold market await the release of the Core Personal Consumption Expenditure (PCE) Price Index, regarded as the Federal Reserve’s preferred measure of inflation. Projections suggest a year-on-year growth of 2.8% in February, with monthly figures expected to moderate from 0.4% to 0.3% month-on-month.

EURUSD – stays subdued despite robust USD, maintains position above 1.0800 level.

The ECB Policy Maker Madis Muller said there will be rate cut in June is more expected. ECB official Yannis Stournas said rate cuts most probably in June month. The rate cut in June month from ECB officials expected is down pressure for Euro currency against counter pairs.

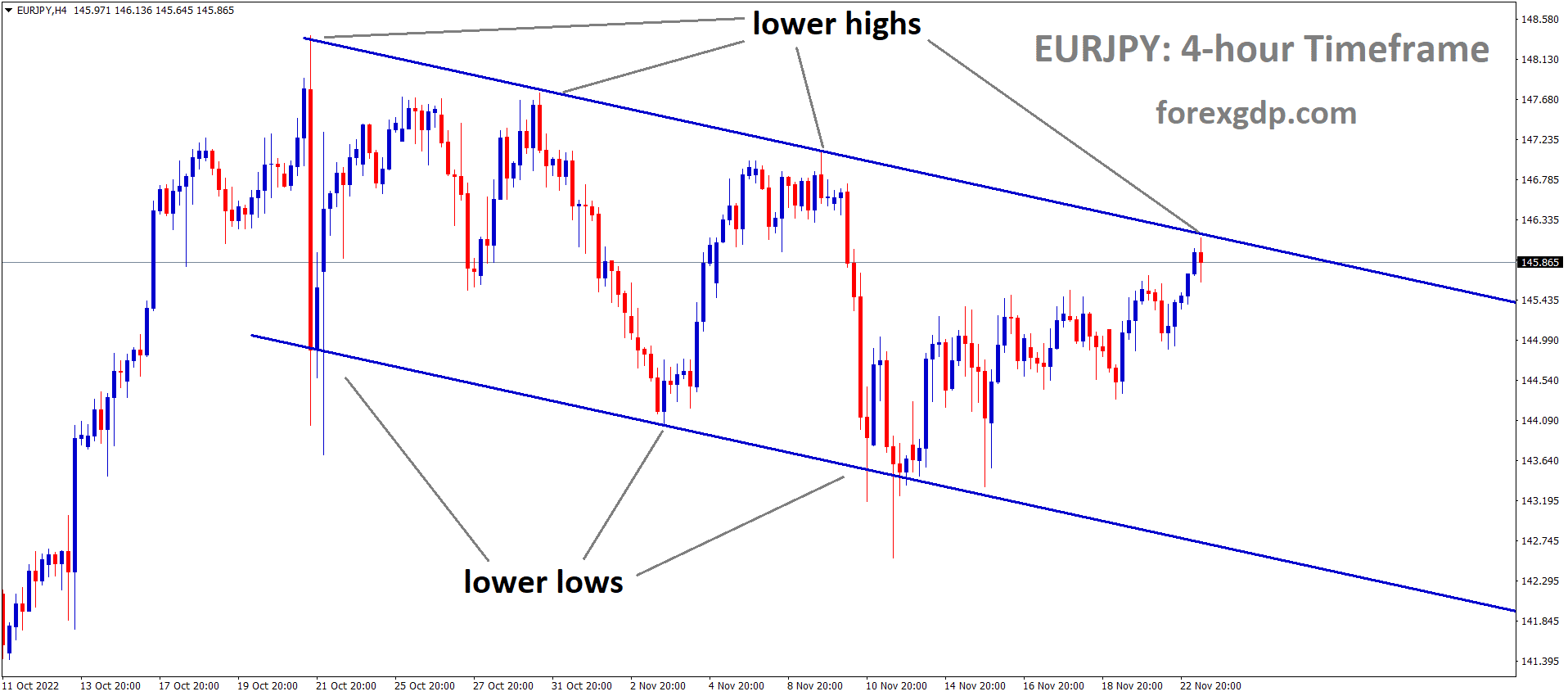

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

The USD Index (DXY), tracking the Greenback against a basket of currencies, approaches a multi-week high reached last Friday, supported by positive outlooks for the US economy. The slightly better-than-expected US Durable Goods Orders data on Tuesday reinforces this outlook, potentially leading the Federal Reserve (Fed) to maintain higher rates amidst persistent inflation concerns. This, coupled with a softer risk sentiment, boosts the safe-haven appeal of the USD and weighs on the EUR/USD pair.

Conversely, the euro faces downward pressure as expectations for a June rate cut by the European Central Bank (ECB) increase. ECB policymakers Madis Muller and Yannis Stoumaras both hinted at the possibility of rate cuts in June, contributing to the negative sentiment surrounding the EUR/USD pair and reinforcing its recent downtrend.

Looking ahead, the release of the Spanish Consumer Price Index (CPI) report on Wednesday could impact the euro and provide momentum in the absence of significant US data. However, all eyes remain on Friday’s US Personal Consumption and Expenditure (PCE) Price Index, which will offer insights into the Fed’s future policy decisions. This data will likely shape near-term USD dynamics and determine the next direction for the EUR/USD pair.

USDCHF – surges to 0.9000 on SNB’s unexpected rate cut, weakening Swiss Franc

The Swiss Franc is recent days depreciated against counter pairs after the SNB rate cut 25bps in last week. SNB goal of inflation is achieved in recent months to 0-2% and coming months rate cuts is possible based on inflation in control stage.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Despite the US Dollar experiencing a slight retreat from its recent monthly peak, the Swiss Franc remains under pressure, bolstering demand for the USD/CHF pair.

The Swiss National Bank (SNB) surprised markets by implementing a 25 basis points (bps) rate cut, reducing its interest rates to 1.50%. This unexpected move diverged from investors’ expectations of unchanged rates, marking the SNB as the first among developed nations’ central banks to initiate a rate-cutting cycle.

Meanwhile, S&P 500 futures indicate positive gains during the London trading session, indicating an improvement in market risk sentiment. The US Dollar Index (DXY) registers a decline to 104.10 as Federal Reserve (Fed) policymakers maintain confidence in easing underlying inflationary pressures, despite persistent price challenges observed in January and February. Concurrently, 10-year US Treasury yields dip to 4.25%, reflecting firm expectations of forthcoming interest rate cuts starting from the June policy meeting.

Rising house rents significantly contribute to US inflationary pressures. Nevertheless, policymakers express optimism that inflation will gradually recede to the targeted 2% level. Chicago Federal Reserve Bank President Austan Goolsbee, in an interview with Yahoo Finance on Monday, forecasted three rate cuts for the year as part of the March monetary policy outlook.

Looking ahead, market focus shifts to the US core Personal Consumption Expenditure price index (PCE) data for February, scheduled for release on Friday. This key economic indicator will likely shape the trajectory of the US Dollar in the coming days.

USDCAD – may reach 1.3600 on declining Crude oil rates and risk aversion.

The BoC Deputy Governor Carolyn Rogers said current inflation in Canada is more difficult than decades. The productivity has to increase in Canada from Skills, innovations and employments will be created more.

USDCAD is moving in the Box pattern and the market has reached the resistance area of the pattern

This movement marks a departure from the pair’s two-day consecutive decline. The shift is attributed to the relative strength of the US Dollar (USD) against the Canadian Dollar (CAD), propelled in part by the downward pressure exerted on the CAD due to declining Crude oil prices.

Specifically, the price of Western Texas Intermediate (WTI) oil experiences a decrease, hovering around $80.70 at the time of reporting. This dip in WTI prices is linked to the release of data indicating an increase in the API Weekly Crude Oil Stock for the week ending on March 22. The stockpile rose by 9.337 million barrels, contrasting with the previous week’s decline of 1.519 million barrels. This unexpected increase in crude oil inventories contributes to the overall bearish sentiment surrounding the CAD.

Furthermore, Bank of Canada (BoC) Senior Deputy Governor Carolyn Rogers voices concerns regarding Canada’s productivity levels. She points to factors such as insufficient investment, lack of competition, and underutilization of skills among new immigrants as key contributors to Canada’s low productivity. Additionally, Rogers highlights the potential threat posed by the current inflationary environment, suggesting that it may present more significant challenges than those witnessed in recent decades.

Meanwhile, the US Dollar Index (DXY) records its second consecutive day of gains, reflecting a broader strengthening of the USD. This trend is fueled by a prevailing risk-off sentiment in the market, driven in part by anticipation surrounding the release of the US Personal Consumption Expenditures (PCE) data scheduled for Friday. However, despite the overall bullishness of the USD, a decline in US Treasury yields serves to temper its advances. This decline is attributed to market expectations regarding potential rate cuts by the US Federal Reserve (Fed).

The divergent views among Fed officials further contribute to the market uncertainty. Atlanta Fed President Raphael Bostic advocates for a cautious approach, expressing his expectation for only one rate cut this year. He warns against prematurely reducing rates, citing the potential for increased economic disruption. In contrast, Chicago Fed President Austan Goolsbee aligns with the majority of the board, anticipating three rate cuts in the near future. These differing perspectives add complexity to the market dynamics surrounding the USD and its exchange rate with the CAD.

USD INDEX – USD gains continue as markets await catalysts

The US Dollar moving positive tone after the US Core Durable goods reading came at 1.4% in February from -0.90% decline in January month. US Inflation is sticky and Domestic data is came at higher than expected makes US Dollar more positive against counter pairs. FED Powell said There will be expected for June month rate cut based on incoming data will coincide with our goals.

USD Index is moving in an Ascending channel and the market has reached the higher high area of the channel

Following the release of Durable Goods and Housing market data, the USD maintains its stability as investors eagerly anticipate new catalysts to shape their positions, particularly in anticipation of upcoming decisions by the Federal Reserve (Fed).

The economic landscape of the United States is delicately poised, with inflation persisting at elevated levels while economic indicators exhibit signs of weakness. Fed Chair Jerome Powell reiterated the central bank’s commitment to a measured approach, emphasizing a reluctance to react aggressively to earlier inflation spikes. Despite this stance, the Fed’s interest rate projections remain unchanged for 2024, indicating a cautious approach to monetary policy adjustments. The expectation of easing measures commencing in June persists, although the timing will be contingent upon incoming economic data.

In the realm of economic updates:

– The S&P/Case-Shiller Home Price index, reported by S&P Dow Jones Indices, revealed a 6.6% year-on-year decline in home prices for January, slightly lower than market expectations.

– The Federal Housing Finance Agency’s (FHFA) House Price Index for January recorded a marginal 0.1% decline during the same period.

– According to data from the US Census Bureau, Durable Goods Orders experienced a notable 1.4% month-on-month increase in February, surpassing consensus estimates of 1.1% and signaling a significant improvement from the previous month’s decline of 6.9%.

Looking ahead, market participants eagerly anticipate the release of the Personal Consumption Expenditures (PCE) figures, a key metric favored by the Fed for measuring inflation. Projections suggest a 2.5% year-on-year increase in the headline PCE, with the core measure expected to show a 2.8% rise. The outcome of these figures is poised to influence the trajectory of the USD in the near term, as investors gauge the Fed’s response to inflationary pressures.

GBPUSD – slides to 1.2620; UK GDP data awaited

The BoE Hawkish Policy Maker Catherine Mann said there are too many rate cuts is expected in this year from BoE. Tomorrow, GBP Q4 GDP is expected to contract at -0.30% QoQ and 0.10% YoY is expected. The Reversal data will help the GBP to gain from lows.

GBPUSD is moving in the Descending channel and the market has fallen from lower high area of the channel

This movement occurs against the backdrop of Federal Reserve (Fed) policymakers maintaining their stance on interest-rate cuts amidst concerns regarding inflation. The Fed officials anticipate reducing rates three times in 2024, a factor that could potentially exert downward pressure on the value of the US Dollar (USD).

On the upcoming Thursday, both the United States and the United Kingdom are scheduled to release their Gross Domestic Product (GDP) data, adding to market anticipation.

Fed Chair Jerome Powell’s recent statements indicate that despite recent upticks in monthly inflation, pricing pressures are expected to ease. He suggests that it might be suitable to implement interest rate cuts later in the year. This dovish stance from the Fed, with the majority of officials projecting three rate cuts in 2024, contributes to the recent decline in the USD across trading sessions.

Regarding economic indicators, the US Conference Board’s Consumer Confidence metric sees a slight decrease to 104.7 from a revised 104.8 in February. However, Durable Goods Orders for February surpass market expectations, showing a 1.4% increase compared to the previous month’s 6.9% decline. Consequently, the US Dollar Index (DXY) consolidates around 104.30 as traders await insights from the US February Personal Consumption Expenditures Price Index (PCE) data scheduled for release on Friday.

In contrast, Catherine Mann, a prominent policymaker at the Bank of England (BoE), expresses caution regarding the excessive market anticipation of interest rate cuts in the UK. She suggests that markets may be expecting more cuts than warranted, and the BoE is unlikely to make any moves before the Fed. Mann’s remarks raise concerns about the market’s rate-cut projections.

Market participants are eagerly awaiting the release of UK GDP growth figures on Thursday. Projections estimate a contraction of 0.3% quarter-on-quarter and 0.2% year-on-year for the fourth quarter. Depending on the actual GDP figures, the performance of the Pound Sterling (GBP) could see fluctuations, potentially influencing the direction of the GBP/USD pair.

AUDUSD – AUD depreciates on softer Aussie CPI, stronger USD

The Australian CPI Data came at 3.4% in February month it is well below 3.5% expected in the market. Westpac Consumer confidence came at 84.4 in March month versus 86.0 in February Month. The RBA have chances to do rate cuts if inflation points continue to move in downtrend.

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Australian Dollar (AUD) continued its decline for the second consecutive session on Wednesday. This downward trend in the AUD/USD pair was driven by weaker-than-expected Australian consumer prices, potentially signaling a shift towards a more dovish stance by the Reserve Bank of Australia (RBA) regarding its interest rate trajectory. Consequently, this outlook has placed downward pressure on the AUD.

In February, Australia’s Monthly Consumer Price Index (YoY) increased by 3.4%, which, although consistent with previous levels, fell slightly below the anticipated 3.5%. However, this reading marked the lowest level since November 2021. The AUD faced additional downward pressure following the release of the Westpac Consumer Confidence index on Tuesday, which showed a decline of 1.8% to 84.4 in March 2024 from February’s 86.0, easing from its 20-month highs.

On the other hand, the US Dollar Index (DXY) recorded its second consecutive day of gains amidst a prevailing risk-off sentiment. This sentiment was largely fueled by expectations surrounding the forthcoming release of the US Personal Consumption Expenditures (PCE) report scheduled for Friday. However, the decline in US Treasury yields may be attributed to market expectations concerning potential rate cuts by the US Federal Reserve (Fed). Such sentiment could potentially limit the advances of the US Dollar.

Additionally, Australia’s Westpac Leading Index (MoM) increased by 0.1% in February, reversing the previous month’s decline of 0.09%. Furthermore, Australia’s government has pledged to support a minimum wage increase in line with inflation this year, acknowledging the ongoing challenges faced by low-income families amidst rising living costs.

According to a Bloomberg survey of economists, there is a consensus expectation for the People’s Bank of China (PBoC) to implement two additional Reserve Requirement Ratio (RRR) cuts in 2024, totaling a reduction of 50 basis points. Moreover, Chinese President Xi Jinping is scheduled to meet with US business leaders, following up on his November dinner with US investors in San Francisco.

Regarding US monetary policy, Atlanta Fed President Raphael Bostic expressed his expectation for only one rate cut this year, cautioning against reducing rates prematurely, which could potentially lead to greater disruption. Conversely, Chicago Fed President Austan Goolsbee aligns with the majority of the board in anticipating three cuts. However, Goolsbee emphasized the need for further evidence indicating a decrease in inflation before proceeding with rate cuts.

In terms of economic indicators, US Durable Goods Orders increased by 1.4% in February, surpassing the expected 1.3% and reversing the previous month’s decline of 6.9%. Similarly, US Durable Goods Orders excluding Defense rose by 2.2% in February, compared to the expected 1.1%, and the previous decline of 7.9%. However, the US Housing Price Index (MoM) decreased by 0.1% in January, following December’s increase of 0.1%.

NZDUSD – NZ Treasury slashes inflation forecast to 3.3% from 4.1%

NZ Finance minster Nicola Willis announced Nation Treasury cut the forecast of Inflation for the Year 2024 annually will be 3.3% from 4.1% predicted in the last time. NZ economy is slowdown than expected, FY 2024 GDP will be 0.10% from 1.5% forecasted in Half Yearly update. NZ Dollar moved down after the Nation opened CPI Forecasted to lower readings than expected.

NZDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

New Zealand Finance Minister Nicola Willis presented the nation’s Treasury semiannual update on Wednesday. The forecast for New Zealand’s annual Consumer Price Index (CPI) for the fiscal year 2024 has been revised down to 3.3%, compared to the previous forecast of +4.1%.

Key points from the update include:

– New Zealand is anticipated to experience slower growth than previously forecasted.

– The annual GDP for fiscal year 2024 is expected to be +0.1%, down from the earlier forecast of +1.5%.

– For fiscal year 2025, the annual GDP is projected to be +2.1%, up from the previous forecast of +1.5%.

")

– The forecast for the annual CPI for fiscal year 2024 has been revised down to +3.3% from the previous forecast of +4.1%.

– It’s important to note that this scenario is not a fiscal forecast as it does not incorporate all information from government entities.

CRUDE OIL – WTI below $80.85 amid strong USD, Russian supply concerns weigh.

The Crudeoil Prices are like to shoot up after the Russia Oil capacity down to 12% overall refineries output after the Ukraine did drone attacks on Russia.OPEC+nations like to cut the supply, it is major supply constraint for global countries for Energy demand.

XTIUSD Crude Oil Price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

WTI prices are experiencing a slight decline amidst a moderate rebound in the US Dollar (USD) value and a mixed market response to the recent disruption of Russian refinery operations due to Ukrainian drone attacks.

The disruption in Russian refineries has prompted concerns regarding global oil supply. Analysts estimate that these disruptions have impacted approximately 12% of Russia’s total oil processing capacity. Geopolitical tensions, particularly in the Middle East and the Russia-Ukraine region, are expected to exert significant influence on WTI prices, potentially leading to an upward trajectory.

Moreover, the Organization of the Petroleum Exporting Countries and its allies (OPEC+) are anticipated to reiterate their policy of production cuts against the backdrop of escalating tensions in the Middle East and Russia. Typically, when OPEC+ reduces oil supply during periods of declining demand, it tends to drive up WTI prices.

Additionally, the recent upward movement in WTI prices is supported by the weakening of the USD, which traditionally makes oil more affordable for buyers holding other currencies. Furthermore, expectations of interest rate cuts by the US Federal Reserve (Fed) throughout the year are providing additional support to WTI prices. Fed Chairman Jerome Powell reaffirmed last week that policymakers intend to implement rate cuts by the year’s end, contingent upon sustained economic growth.

Market participants are closely monitoring the release of the US February Personal Consumption Expenditures Price Index (PCE) data scheduled for Friday. Stronger-than-expected readings in the report could potentially postpone the anticipated rate cuts by the Fed this year and cap the upside potential of WTI prices. Federal Funds Futures, as indicated by CME Group’s FedWatch tool, currently imply a 74.5% likelihood of a rate cut during the June meeting.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/