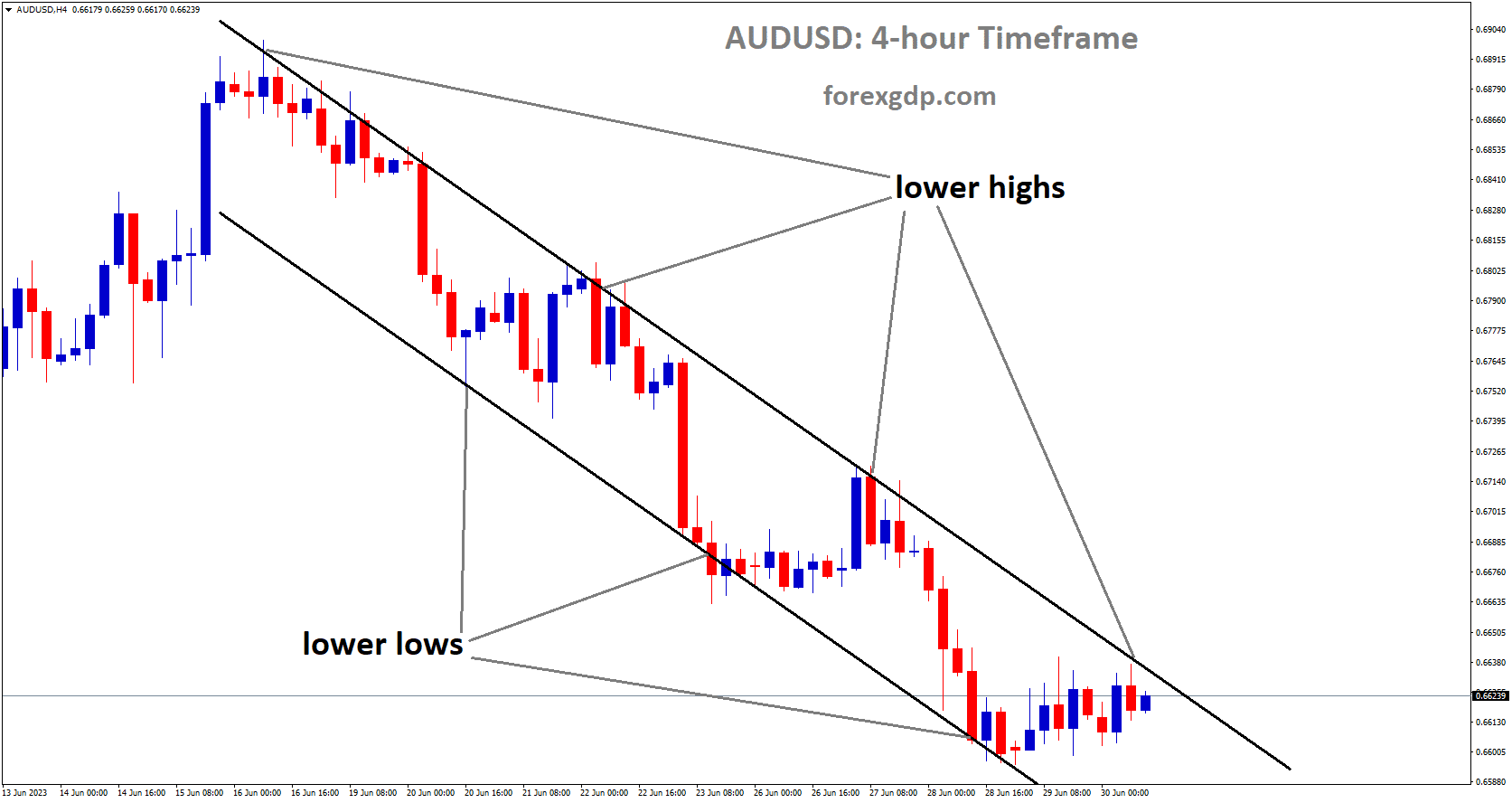

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

AUDUSD – AUD extends gains on strong CPI, weak USD

The Australian CPI Q1 (QoQ) came at 1.0% versus 0.80% expected and 0.60%printed in the Q4 2023. CPI (YoY) data came at 3.6% versus 3.4% expected and 4.1% printed in the previous quarter. Monthly CPI data came at 3.5% in the March month versus 3.4% printed in the previous month. Upbeat CPI Data makes Australian Dollar moved higher against counter pairs. This CPI Data favors for RBA to do hawkish tone in the upcoming months.

The Australian Dollar (AUD) continues its upward trend, marking its third consecutive day of gains following the release of unexpectedly positive Consumer Price Index (CPI) data on Wednesday. The robust inflation figures are seen as potentially bolstering a more hawkish stance regarding the monetary policy outlook of the Reserve Bank of Australia (RBA), thereby strengthening the Australian Dollar (AUD) and supporting the AUD/USD pair.

Additionally, the Australian Dollar (AUD) is boosted by gains in the ASX 200 Index, particularly driven by the technology and healthcare sectors. This positive momentum in Australian stocks mirrors the upbeat sentiment on Wall Street, propelled by strong corporate earnings reports.

Conversely, the US Dollar Index (DXY), which measures the US Dollar (USD) against a basket of major currencies, faces downward pressure due to declining US Treasury yields and disappointing Purchasing Managers Index (PMI) data from the United States (US). These factors contribute to the weakness of the US Dollar (USD) and further support the AUD/USD pair. However, despite the sluggish PMI data, reports indicate continued expansion in US business activity in April, albeit at a slower pace compared to March.

In the market update, the Australian Dollar appreciates following the release of upbeat consumer inflation data. Australia’s CPI rose by 1.0% QoQ in the first quarter of 2024, surpassing expectations, while the YoY CPI increase stood at 3.6%. Meanwhile, the US PMI data shows a decline, with the preliminary S&P Global Composite PMI dropping to 50.9 in April and Manufacturing PMI falling to 49.9, indicating contraction. Australia’s own PMI figures show mixed results, with the Composite PMI reaching a 24-month high but Services PMI declining.

Furthermore, reports suggest that the People’s Bank of China (PBoC) plans to lower the Medium-term Lending Facility (MLF) rate, which could impact the Australian market due to the countries’ close trade ties. Additionally, the probability of the Federal Reserve keeping interest rates unchanged in the June meeting has increased to 84.6%, according to the CME FedWatch Tool.

XAUUSD – Gold price steady above $2,300, awaits US macro data for momentum

The Gold prices are little rebounded from lows after the US Domestic data came at lower than expected last day. US Composite PMI reading came at 50.9 in the April month, Manufacturing PMI Data came at lower than expected, Services PMI reading came at 50.9 vs 51.7 printed in the March month. US Q2 GDP is expected lower due to Contraction in PMI data.

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

The price of gold, denoted as XAU/USD, struggles to build upon the rebound seen in the previous session from levels just below the $2,300 mark. As the market enters the European session on Wednesday, gold remains range-bound. The current global risk sentiment benefits from a reduction in concerns regarding further escalation of geopolitical tensions in the Middle East. This, coupled with some dip-buying of the US Dollar (USD), influenced by expectations of a hawkish stance from the Federal Reserve (Fed), poses a challenge for the non-yielding yellow metal.

Market expectations currently indicate that the US central bank will likely initiate its rate-cutting cycle in September, given the persisting inflationary pressures. This expectation supports elevated US Treasury bond yields, which, in turn, revives demand for the USD and restricts the upside potential for gold. Traders are likely awaiting key US macroeconomic data scheduled for release this week, particularly the Advance Q1 GDP report and the Personal Consumption Expenditures (PCE) Price Index, to gauge the Fed’s stance on future rate cuts before taking fresh directional positions on XAU/USD.

Meanwhile, the release of US Durable Goods Orders on Wednesday could impact USD price dynamics and offer short-term trading opportunities for gold. The current price action suggests that traders may wait for a sustained breakthrough and acceptance below the $2,300 level before considering further downside momentum for the precious metal, following its recent retreat from the all-time peak achieved earlier this month.

Furthermore, easing concerns over geopolitical tensions in the Middle East continue to support a generally positive risk tone, acting as a deterrent for safe-haven assets like gold. Additionally, hawkish comments from Federal Reserve officials have bolstered expectations of prolonged higher interest rates, undermining gold’s appeal. The weaker-than-expected US Purchasing Managers Index (PMI) prints released on Tuesday have kept USD bulls cautious, providing some support to gold.

Traders are also exercising caution ahead of this week’s significant US macro data releases, which could influence the Fed’s future policy decisions and provide fresh momentum to XAU/USD. Wednesday’s economic calendar includes Durable Goods Orders, although attention remains focused on the Advance Q1 GDP report and the Personal Consumption Expenditures (PCE) Price Index.

EURUSD – ECB’s Nagel: Single June rate cut doesn’t imply consecutive cuts

The ECB Policy maker and Bundesbank Chief Joachim Nagel said June month rate cut is not necessary and services inflation still higher in the Euro zone, Wage growth is also higher. We do not pre-commit to rate cuts based on the incoming datas, we wait for inflation to move to the target of 2% then only we do rate cuts. Hawkish remarks from Chief Nagel makes Euro stronger against counter pairs.

EURUSD has broken the Descending triangle pattern in downside

European Central Bank (ECB) policymaker and Bundesbank Chief Joachim Nagel addressed on Wednesday the potential for a June interest rate cut, emphasizing that such a move might not automatically lead to a sequence of subsequent rate reductions.

Nagel also noted that services inflation continues to stay elevated, primarily due to ongoing robust wage increases. However, he expressed reservations about whether inflation would indeed return to the target level in a timely and sustained manner.

Highlighting the prevailing uncertainty, Nagel emphasized the ECB’s stance of not committing in advance to a specific path for interest rates.

USDJPY – JPY hits multi-decade low against USD, hovers near 155.00 level

The Japanese Yen moved lower after the BoJ Ueda commented there is no rate hike in the April month due to inflation will be sustained at the target of 2% in the next three years.Labor hike done by 70% companies and remaining companies worry for labour shortages even wage hikes done.

USDJPY is moving in an Uptrend line and the market has rebounded from the higher low area of the trend line

US Dollar moved higher against JPY after the Middle east tensions are eased down.

The Japanese Yen (JPY) descends to a fresh multi-decade low against the US Dollar (USD) as Tuesday’s European session commences. Bears are eyeing a breakthrough below the pivotal 155.00 level before initiating new positions. Market sentiment leans towards a prolonged divergence in interest rates between the US and Japan. Additionally, the improved market sentiment, buoyed by easing tensions in the Middle East, dampens demand for the safe-haven JPY.

Conversely, the USD sees some buying interest, rebounding from the previous day’s decline driven by disappointing US Purchasing Managers’ Index (PMI) data. This recovery supports the USD/JPY pair. However, the sustainability of JPY bearishness is in question amid speculation of potential intervention by Japanese authorities to strengthen the domestic currency. Moreover, anticipation mounts ahead of the Bank of Japan (BoJ) decision on Friday. The outcome of the crucial BoJ meeting, along with key US economic data releases—such as the Advance Q1 GDP report and the Personal Consumption Expenditures (PCE) Price Index—will likely shape the near-term trajectory of the currency pair.

In related news, despite verbal intervention warnings from Japanese officials and positive indicators regarding pay scale hikes and labor shortages in Japan, JPY bulls struggle to gain ground. Investor focus remains on the BoJ’s monetary policy stance and its implications for interest rates. Additionally, weaker US PMI figures contribute to USD pressure, keeping the USD/JPY pair in check. Traders await further cues from upcoming US economic data releases, particularly the Durable Goods Orders, as well as the GDP and PCE Price Index reports later in the week.

USDCHF – Steady at 0.9150, Matching Six-Month Highs

The Swiss annual inflation rate came at 1.0% in the March month, SNB has the chances to rate cut in the June month. Business confidence indicators lower than expected, Retail sales also lower reading in the recent months. So Swiss Franc is depreciated against counter pairs in the market.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

During early European trading hours on Wednesday, the USD/CHF currency pair hovered near the 0.9140 level, maintaining its position close to the six-month high of 0.9152 reached on April 15. The Swiss Franc (CHF) is facing challenges due to notable disparities in expected monetary policy trajectories between the US Federal Reserve (Fed) and the Swiss National Bank (SNB).

Swiss annual inflation dropped to a more than two-year low of 1% in March, emphasizing the SNB’s assertion that underlying inflation has moderated. This, coupled with pessimistic Business Confidence indicators and a decline in Retail Sales, has strengthened market expectations that the SNB may implement another rate cut in June.

The CHF had already experienced significant depreciation after the Swiss National Bank unexpectedly reduced its main interest rate by 25 basis points to 1.50% in March, becoming the first major central bank to reverse course on tighter monetary policy.

In the United States (US), the probability of the Federal Reserve maintaining interest rates unchanged in the June meeting has risen to 84.6%, up from the previous week’s 82.7%, according to the CME FedWatch Tool.

The US Dollar Index (DXY), which measures the US Dollar (USD) against six major currencies, has rebounded due to a higher 10-year yield on US Treasury bonds, standing at 4.62%, up by 0.54% at the time of writing. However, disappointing US Purchasing Managers Index (PMI) data is weighing on the Greenback, thereby limiting the advance of the USD/CHF pair.

In April, the preliminary S&P Global Composite PMI for the US declined to 50.9 from the previous reading of 52.1. Additionally, the Manufacturing PMI fell to 49.9 from 51.9 in the previous reading, below the estimated 52.0. Similarly, the Services PMI decreased to 50.9, compared to the prior 51.7, falling short of the expected 52.0.

USDCAD – muted near 1.3650 on oil gains, weak US PMI

The Canada Industrial produce price index came at 0.80% in the March month versus 1.1% printed in the 1.1% previous month. House price index came at 0.10% and inline with expected reading. Now retail sales data is scheduled today. US Domestic data came at lower than expected last day makes USD weaker against Canadian Dollar.

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

The USD/CAD pair extends its downward trajectory that commenced on April 17, hovering around 1.3660 amid the Asian session on Wednesday. This decline is primarily attributed to the weakening US Dollar (USD), which suffered from disappointing Purchasing Managers Index (PMI) data from the United States (US) released on Tuesday.

In April, the preliminary S&P Global Composite PMI for the US dropped to 50.9 from the previous reading of 52.1. Additionally, the Manufacturing PMI declined to 49.9 from 51.9 in the prior reading, falling below the estimated 52.0. Similarly, the Services PMI decreased to 50.9 from the prior 51.7, missing the expected 52.0.

Meanwhile, the Canadian Dollar (CAD) gains support from the uptick in crude oil prices, given Canada’s status as the largest exporter of crude oil to the United States (US). West Texas Intermediate (WTI) oil price trades around $83.20 per barrel at the time of reporting.

Crude oil prices have risen following industry data indicating an unexpected decrease in US crude stocks last week, signaling positive demand dynamics. Attention has shifted away from tensions in the Middle East. The American Petroleum Institute (API) reported a decline of 3.23 million barrels in weekly crude oil stocks for the week ending April 19, contrary to the expected increase of 1.80 million barrels and the previous week’s increase of 4.09 million barrels.

Furthermore, the Canadian Industrial Product Price Index rose by 0.8% in March, meeting expectations but slightly lower than the previous month’s upwardly revised figure of 1.1%. Additionally, the New Housing Price Index remained unchanged in March, against forecasts of a 0.1% increase, with the year-over-year NHPI declining by 0.4%. Investors are awaiting Canadian Retail Sales data scheduled for release on Wednesday.

USD INDEX – USD falters on disappointing S&P PMI data

The US Composite PMI reading came at 50.9 in the April month versus 52.1 expected, Manufacturing PMI reading at 49.9 from 50.9 in the previous month, Services PMI reading shows 50.9 from 51.7 printed in the last month. Economists said Second quarter shows tepid start in the Manufacturing, Services and Private sector Businesses. US Dollar moved down after the downbeat data readings printed in the April month.

USD Index is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The US Dollar Index (DXY) experiences a softening trend, hovering around 105.70, marking a decline in its value during Tuesday’s trading session. This downtrend comes as the Federal Reserve (Fed) maintains a consistently hawkish stance, which could potentially mitigate the Greenback’s losses, as market participants postpone expectations for the onset of an easing cycle.

Investors are closely monitoring crucial economic indicators scheduled for release this week, particularly the preliminary data on the Gross Domestic Product (GDP) Growth Rate for Q1 and the Personal Consumption Expenditures (PCE) Price Index for March. These reports are anticipated to provide valuable insights into the overall health of the economy and further influence market sentiment.

The latest session witnessed S&P Purchasing Managers’ Index (PMI) figures falling below market expectations, prompting selling pressure on the US Dollar. Despite this, the US economy continues to demonstrate resilience overall.

The Fed’s hawkish tone suggests reduced probabilities of imminent rate cuts, with expectations now leaning towards such actions occurring no earlier than September. The forthcoming PCE and GDP data releases are poised to introduce additional volatility into the markets, as they contribute to shaping expectations regarding future Fed policy decisions.

Daily Digest Market Movers:

– The S&P Global Composite Purchasing Managers Index (PMI) for April’s flash estimate dipped to 50.9, indicating a slower pace of private sector growth in the US compared to March’s figure of 52.1.

– April’s S&P Global Manufacturing PMI showed a more pronounced decline, dropping from 51.9 in March to 49.9, suggesting a contraction in manufacturing sector activity.

– Similarly, the Services PMI for April declined from 51.7 to 50.9, reflecting a moderation in services sector growth.

– Despite the dovish sentiment surrounding the Fed’s monetary policy, the first rate cut is now projected to occur in September, although it has not been fully priced in by the market.

– US Treasury bond yields also exhibit a downward trend, with the 2-year yield at 4.93%, the 5-year yield at 4.61%, and the 10-year yield at 4.58%.

GBPUSD – inches up past 1.2450; BoE official quells summer rate cut hopes

The BoE Chief economist Huw Pill said inflation easing in the UK is not enough to cut rates in the June month, So GBP Jumped against USD after the comments from Economists. Readings from the US domestic data came at lower than expected last day in this April month makes worry for USD against GBP.

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

GBP/USD exhibits a modest recovery above the 1.2450 level during the early Asian trading hours on Wednesday. The recent US data, showing a slowdown in April’s business activity, along with an increased risk appetite, exerts downward pressure on the US Dollar (USD). Later today, investors anticipate the release of US Durable Goods Orders and weekly Mortgage Applications.

The S&P Global report released on Tuesday indicated a decline in business activity in the United States in April, marking a four-month low due to reduced demand. The flash Manufacturing PMI dropped to 49.9 from the previous reading of 51.9, while the Services PMI slipped to 50.9 from 51.7, both below market expectations. Consequently, the Composite PMI, reflecting both sectors, fell to 50.9 from March’s 52.1. This data prompts some selling in the Greenback.

As the Federal Reserve (Fed) evaluates signs of economic deceleration to address inflation concerns, markets anticipate the central bank to maintain its policy rate within the current 5.25%–5.50% range in the upcoming monetary policy meeting. Despite some policymakers suggesting potential rate cuts, the general tone suggests a prolonged restrictive policy, bolstering the USD and restraining GBP/USD’s upside potential.

Conversely, speculation regarding a summer interest rate cut by the Bank of England (BoE) diminishes as the UK’s chief economist underscores the necessity of maintaining a “restrictive” monetary policy stance. BoE Chief Economist Huw Pill emphasized that easing headline inflation alone does not warrant policy easing and highlighted the risks associated with premature rate cuts. These remarks provide support to the Pound Sterling (GBP) against the USD.

NZDUSD – maintains elevated levels near mid-0.5900s, reaching over one-week highs amidst upbeat risk sentiment

The Middle east tensions are calm down in the markets, So NZ Dollar moved higher against USD. Yesterday US PMI readings are more down against expected readings, So US Dollar moved down against NZD. This week US Core Durable Goods orders and GDP data is scheduled, based on the readings NZDUSD further movements in the market.

NZDUSD is moving in the Symmetrical triangle pattern and the market has reached the bottom area of the pattern

The NZD/USD pair extends its upward momentum for the third consecutive day into Wednesday’s Asian session, climbing to levels around the mid-0.5900s. This surge brings the pair to over a one-week high, propelled by a slight weakness in the US Dollar (USD).

The recent release of weaker US Purchasing Managers Index (PMI) data on Tuesday suggests a loss of momentum in the economic recovery at the beginning of the second quarter. Additionally, diminishing geopolitical tensions in the Middle East contribute to a positive market sentiment, which reduces demand for the safe-haven USD and supports risk-sensitive currencies like the New Zealand Dollar (NZD).

Despite the USD weakness, expectations of a hawkish stance from the Federal Reserve (Fed) act as a deterrent to the NZD/USD pair’s upside potential. Investors increasingly believe that the Fed is unlikely to initiate interest rate cuts in June and anticipate fewer rate cuts in 2024 compared to previous expectations. This outlook supports higher US Treasury bond yields and prevents a significant decline in the USD, thereby limiting the NZD/USD pair’s gains.

Looking ahead, market participants await the release of US Durable Goods Orders later in the North American session for potential market-moving catalysts. However, the main focus remains on Thursday’s Advance US Q1 GDP report and Friday’s release of the US Personal Consumption Expenditures (PCE) Price Index. These data releases will shape market expectations regarding the Fed’s future monetary policy decisions, influencing demand for the USD and determining the short-term direction of the NZD/USD pair.

CRUDE OIL – WTI steadies near $83.25, supported by optimistic demand projections

The Crudeoil prices are lower against USD due to Israel- Iran conflict eased down in the market.Iran said no retailiation on Israel and no missle attack for Israel. Oil demand slumped and supply concerns makes Oil prices moved lowered against USD.

XTIUSD Crude oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

West Texas Intermediate (WTI) crude oil prices are struggling to gain momentum after bouncing off the 50-day Simple Moving Average (SMA) support around the $80.75 level. As of the Asian session on Wednesday, the commodity is hovering around the $83.25 mark, showing minimal change for the day. Several factors are influencing WTI crude oil prices at the moment.

Firstly, concerns regarding a potential escalation of geopolitical tensions in the Middle East have eased slightly following indications from Iran that it does not plan to retaliate against Israel’s recent limited-scale missile strike. While this reduction in geopolitical risk premiums is pressuring crude oil prices, the ongoing conflict between Israel and Hamas continues to keep concerns alive, providing some support to oil prices.

Additionally, expectations of interest rate cuts by major central banks to stimulate economic growth, which would lead to increased fuel consumption, coupled with a surprise decline in US crude inventories reported by the American Petroleum Institute (API) last week, are helping to mitigate downward pressure on crude oil prices.

Furthermore, the US dollar is trading near its lowest level in over a week following disappointing US Purchasing Managers’ Index (PMI) data for April. This weakness in the dollar is offering support to crude oil prices. However, expectations of the Federal Reserve maintaining higher interest rates for an extended period may prompt some dip-buying in the dollar, warranting caution in predicting further short-term gains in crude oil prices.

Traders are awaiting official US crude inventory data for confirmation of the significant drawdown reported by the API, which could provide further momentum. Additionally, the release of US Durable Goods Orders data may impact the dollar and present short-term trading opportunities for crude oil prices. Looking ahead, market focus will be on the Advance US Q1 GDP report and the Personal Consumption Expenditures (PCE) Price Index later in the week.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!