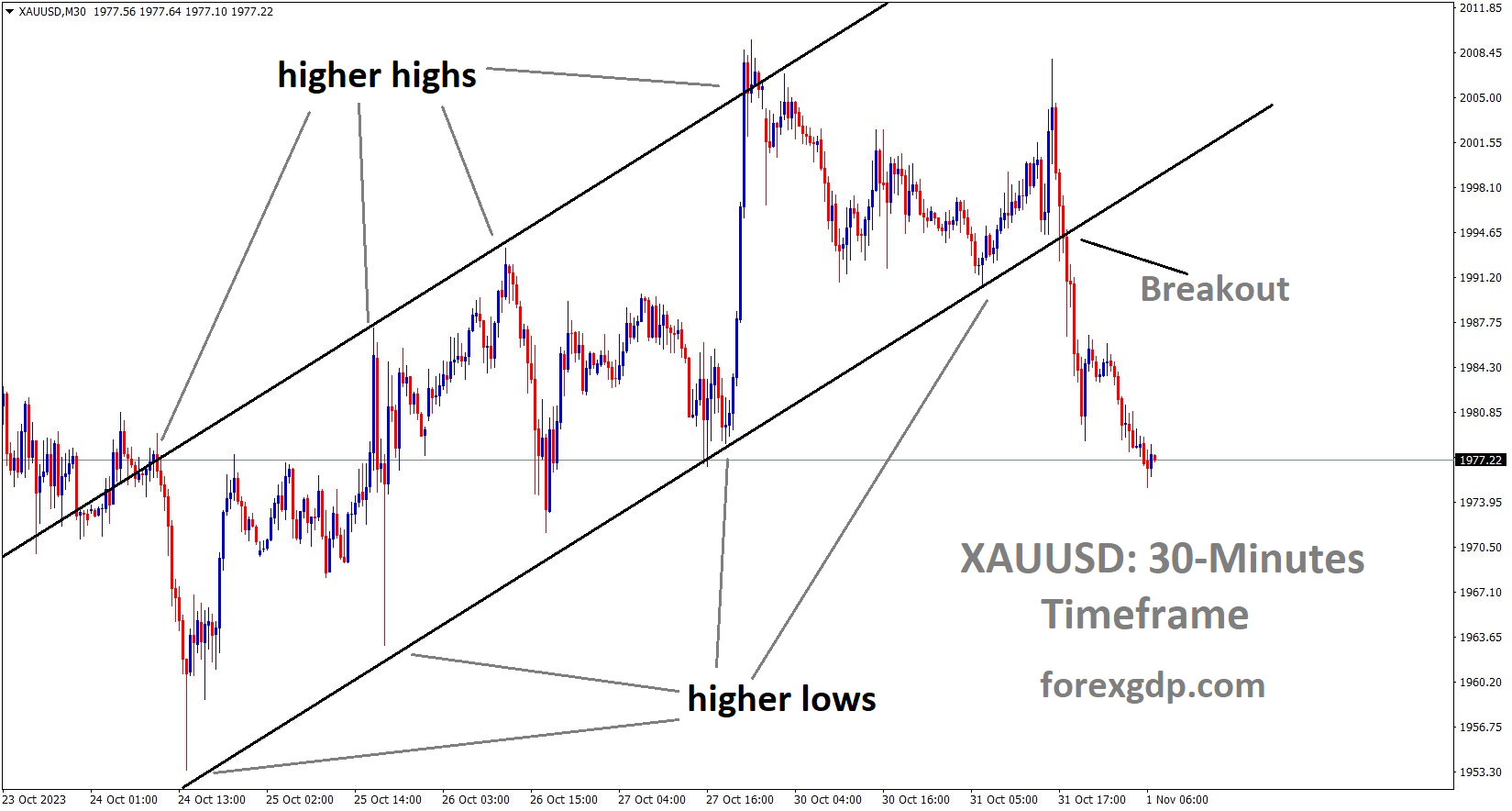

XAUUSD has broken the Ascending channel in downside

In today’s interconnected global economy, central banks play a pivotal role in shaping monetary policy, which in turn affects economic stability and growth. The Federal Reserve (Fed), as the central bank of the United States, holds a prominent position in this landscape. As we delve into the complex web of factors influencing the Fed’s monetary policy decisions, we will also explore the actions and policies of other major central banks across the world. These decisions collectively have a significant impact on the global economic landscape. In this comprehensive analysis, we will examine the current stance of the Federal Reserve, its reasons for maintaining interest rates, and the key indicators that will shape its future decisions.

Current Fed Policy

The Federal Reserve is at a critical juncture as it contemplates the path forward for its monetary policy. As of its upcoming meeting on November 1, 2023, the Fed is widely expected to keep its target interest rate range at 5.25% to 5.5%. This decision is in line with recent statements from Fed policymakers and the prevailing expectations of financial markets. However, the true intrigue lies not in the expected rate hold but in the signals the Fed may provide regarding the possibility of future interest rate increases and the potential trajectory for rate cuts in 2024.

Reasons for Maintaining Rates

Several key factors contribute to the Federal Reserve’s decision to keep interest rates unchanged at their current levels:

1. Bond Yields’ Impact

One critical consideration is the sharp increase in the 10-year U.S. Treasury Bond yield in recent weeks. At the time of the Fed’s September 2023 meeting, this yield stood at 4.5%, but it has since climbed to approximately 4.9%. Such a significant jump in this closely watched fixed-income benchmark has effectively tightened monetary policy.

Fed officials have even described this rise in long-term rates as being broadly equivalent to another interest rate hike. This development weighs heavily on the minds of policymakers.

2. Economic Data

Economic indicators, at least on the surface, have been fairly encouraging. Core Personal Consumption Expenditures (PCE) inflation, which is the Fed’s primary metric for inflation, has continued to cool off. In September 2023, core PCE inflation came in at a 3.7% annual rate, extending the pattern of disinflation witnessed throughout 2023. Additionally, the job market, while still running relatively hot, has shown signs of a better balance between supply and demand. Notably, wage growth has been slowing down.

3. Inflation Concerns

While a strong economy is typically a welcome development, it also carries the potential for inflationary pressures. For instance, the 4.9% GDP growth recorded for the third quarter of 2023 raises concerns that the economy might be running too hot, given the Fed’s objective of bringing inflation down further. The Federal Reserve has explicitly stated that if the economy fails to exhibit signs of easing back from its current robust growth levels, incremental interest rate hikes may become necessary.

Key Indicators for Future Decisions

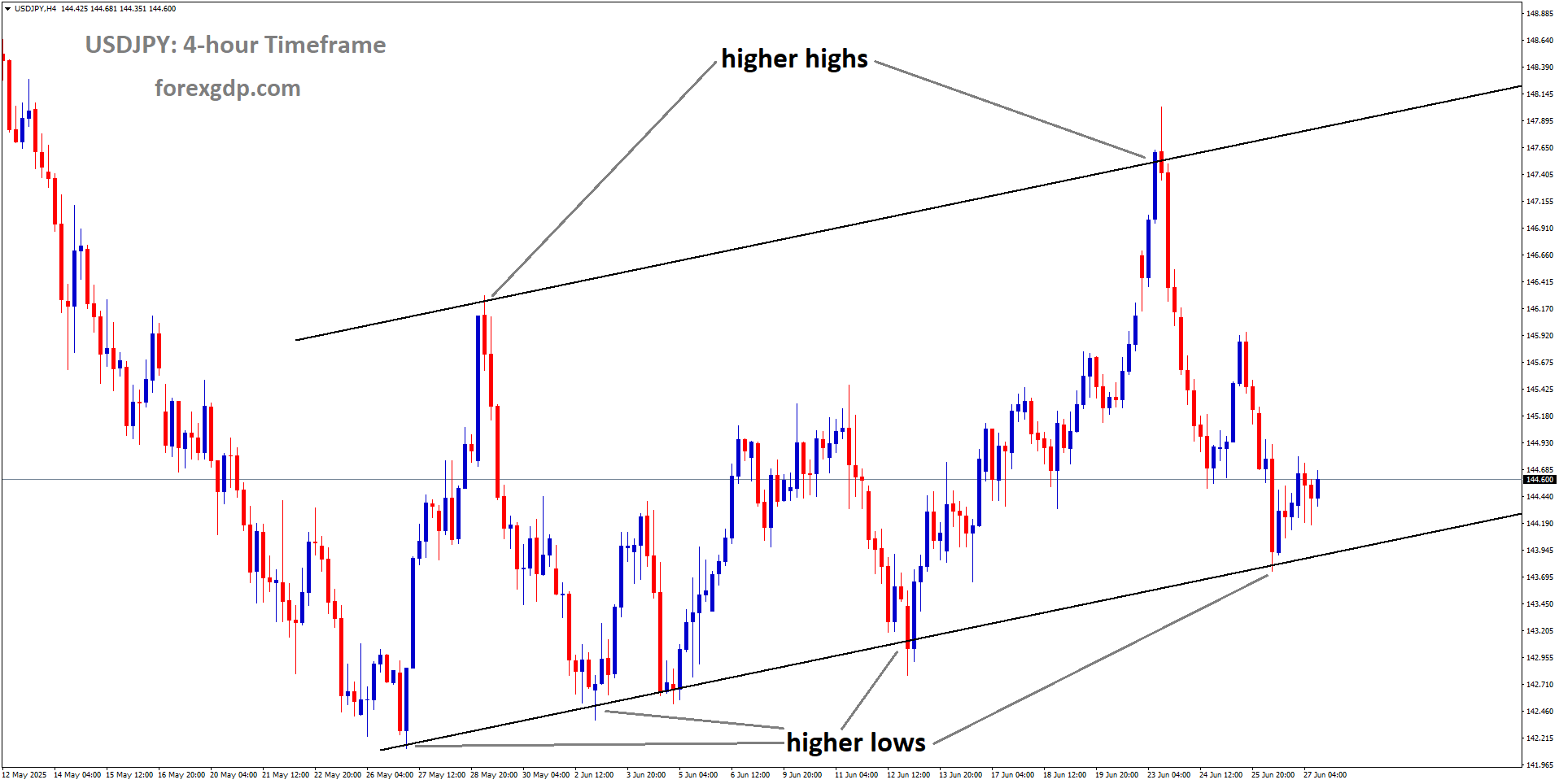

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

The November 1, 2023 meeting of the Federal Reserve is poised to provide important insights into the central bank’s future direction. Several key indicators will shape our understanding of where the Fed stands and where it might be headed.

Consensus Decision

One of the first aspects to scrutinize will be whether the decision to keep rates unchanged is a consensus decision among Fed policymakers. The presence of dissenting voices advocating for an interest rate increase could signal a higher likelihood of such hikes occurring in the coming months. Historically, Fed Chair Jerome Powell has demonstrated an ability to build consensus among policymakers, but the process may become more challenging now that the Fed is fine-tuning its policy.

Powell’s Statements

Perhaps the most eagerly anticipated element of the November 1 meeting is Fed Chair Jerome Powell’s press conference scheduled for 2:30 p.m. ET. In recent weeks, the prevailing sentiment within the Fed appears to have shifted towards holding rates at their current levels, with higher rates being viewed more as a contingency plan than an imminent action.

This is a notable shift from the prior perspective, where a rate increase was the more likely outcome. Therefore, it will be of great interest to observe how Powell discusses the various scenarios surrounding interest rates, including the potential for further hikes.

Interest Rate Cut Possibilities

Another aspect to watch closely is the extent to which Powell entertains questions related to interest rate cuts. Up until now, the Fed’s messaging has primarily revolved around maintaining elevated interest rates for an extended period, likely until the second half of 2024. However, any indication or elaboration from Powell on when and under what criteria rates might fall could have significant implications. As of now, the Fed’s focus has been on sustaining a restrictive policy stance. Nonetheless, the November Fed meeting remains significant, even if interest rates are almost certain to be held at their current levels. The primary focus will be on gathering clues regarding the likelihood of another interest rate hike and the potential trajectory for rates in late 2024.

Global Central Bank Actions

While the Federal Reserve’s monetary policy decisions garner substantial attention, central banks across the world are grappling with similar economic challenges.

USDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

Each central bank tailors its policy to the unique circumstances of its respective country. In this section, we examine the actions and policies of key central banks from various regions.

European Central Bank

The European Central Bank (ECB) is among the central banks that have closely mirrored the Federal Reserve’s policy actions. On a recent occasion, the ECB decided to keep its key interest rate at 4%. The central bank has reiterated its commitment to monitoring inflation trends and basing its future decisions on incoming data. Like the Fed, the ECB has stressed a data-dependent approach to its monetary policy.

Bank of England

The Bank of England (BoE) is set to make its own interest rate decision on November 2. The BoE faces a delicate balancing act between a relatively weak domestic economy, high levels of inflation, and the potential for energy price spikes due to geopolitical conflicts.

Interest rate futures suggest that traders believe the BoE will not cut rates until at least June 2024. The BoE, like its counterparts, must carefully weigh various economic factors in its decision-making process.

Bank of Japan

has maintained a dovish stance for many months, even as global interest rates have surged. To keep yields below its 1% cap, the BOJ has been intervening heavily in the nation’s bond market. However, mounting pressure on the BOJ to adjust its policy of suppressing domestic borrowing costs suggests the possibility of a tweak to the 1% yield cap in the future. The BOJ’s situation underscores the complexities central banks face in managing their respective economies and financial markets.

Bank of Canada

The Bank of Canada (BoC) held its key overnight rate at 5% on October 25. While inflation had peaked at over 8% the previous year, it dipped to 3.8% in September. However, the BoC indicated that price increases were unlikely to return to its 2% target until the end of 2025. The BoC’s approach to inflation management underscores the complexity of central bank decision-making in a changing economic landscape.

Reserve Bank of Australia

The Reserve Bank of Australia (RBA) has opted to keep rates steady at 4.1% for a fourth consecutive meeting in October.

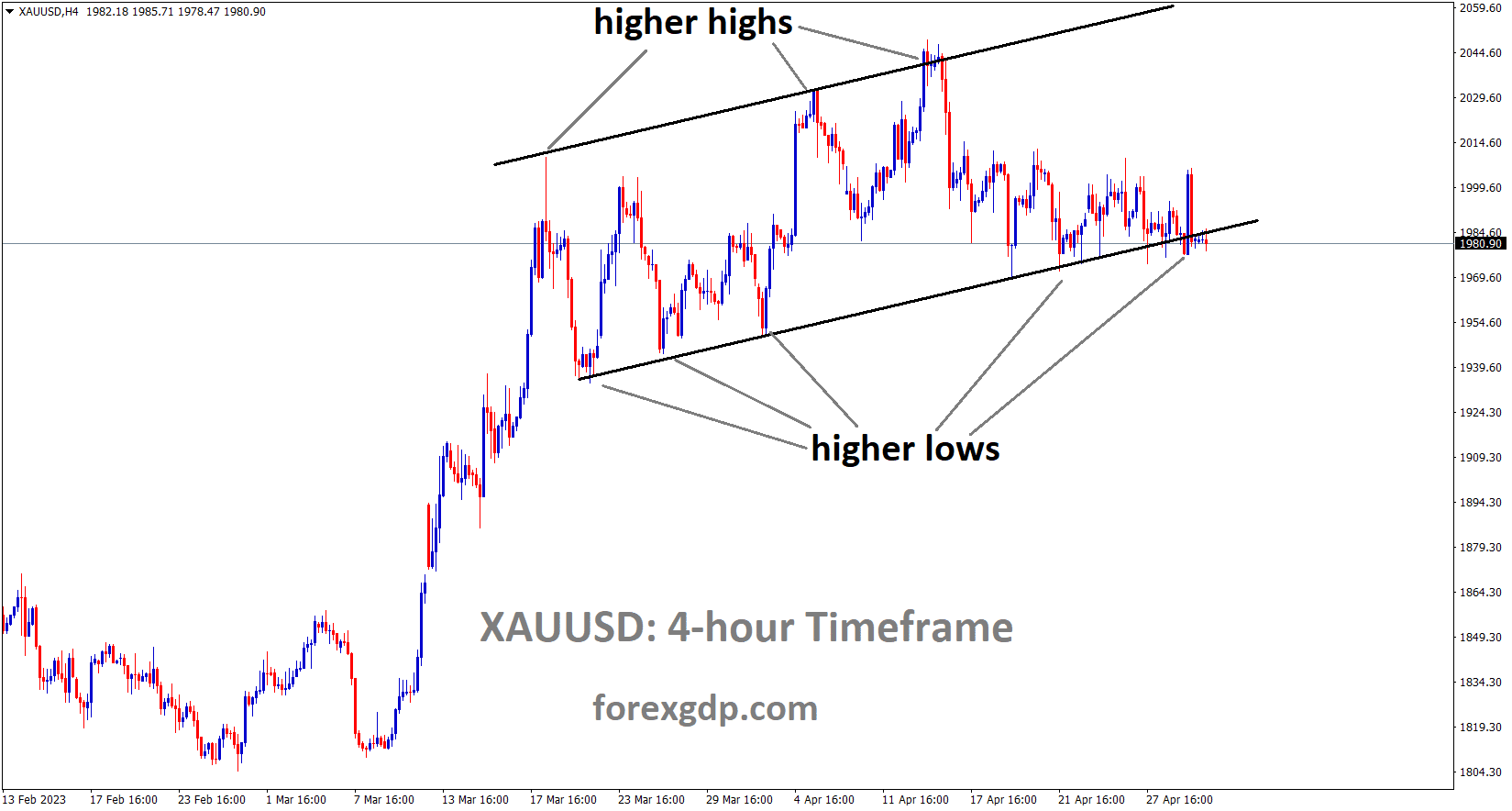

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The RBA’s decision followed surprisingly robust inflation figures in the third quarter. Markets are pricing in a roughly 60% chance of a quarter-point rate hike in the near future. Governor Michele Bullock has also issued warnings about the potential for further tightening if the inflation outlook worsens. Australia’s central bank must grapple with inflation pressures in its own unique context.

Reserve Bank of New Zealand

The Reserve Bank of New Zealand (RBNZ) faces a unique challenge as it decides on its monetary policy. The RBNZ kept its cash rate at a 15-year high of 5.5% in May. However, the New Zealand economy experienced inflation levels that reached a two-year low of 5.6% in the third quarter. Despite this, inflation remains well above the RBNZ’s target range of 1% to 3%. These dynamics make the decision to cut rates in November unlikely.

Swiss National Bank

The Swiss franc, a historically strong currency, reached its highest level against the euro since 2015 on October 19, 2023. This surge followed the outbreak of conflict in Gaza, which extended a long run of Swiss currency strength.

The SNB faces a dual challenge: controlling inflation, which stood at 1.7% year-on-year in September, comfortably within its target range, and safeguarding Swiss exports during a period of economic stagnation. Futures markets are tipping the SNB to hold its policy rate at 1.75% in December before assessing the next steps.

Sweden’s Central Bank

Sweden’s central bank raised its main interest rate to 4% in September. However, the country faces a unique challenge, as economists polled by Reuters predict a 0.7% contraction in the economy in 2023. Furthermore, Swedish inflation, excluding volatile energy costs, registered an uncomfortably high 6.9% in September. This presents the central bank with a complex dilemma as it seeks to balance growth and inflation.

Norges Bank

Norges Bank, the central bank of Norway, raised its key interest rate by 25 basis points to 4.25% in late September. This decision was made despite inflation data for that month coming in lower than expected. Prime Minister Jonas Gahr Stoere suggested that interest rates may have peaked. Norges Bank’s approach reflects the balancing act between economic data and political considerations that central banks must navigate.

The U.S. Economic Landscape

Amidst the backdrop of central bank decisions across the globe, the United States’ economic performance stands as a prominent example of resilience and growth.

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Understanding the dynamics of the U.S. economy is crucial in the context of the Federal Reserve’s monetary policy.

Strong U.S. Economic Performance

The U.S. economy has displayed impressive resilience and growth, despite the Federal Reserve’s series of interest rate hikes. The Commerce Department reported that the economy expanded at a robust rate of 4.9% in the last quarter. This pace exceeded expectations and marked the fastest growth rate in more than two years. The acceleration was primarily driven by robust consumer spending.

Factors Fueling Consumer Spending

Several factors have contributed to the strength of consumer spending in the United States:

1. Wage Increases

Despite persistent inflation pressures, wage increases have begun to outpace price hikes. In the April-June quarter of the latest available data, wages and salaries rose by 1.7% after adjusting for inflation.

This represents the fastest quarterly increase in three years. The improved purchasing power of consumers has been a key driver of spending.

2. Healthy Household Finances

Americans began the year with healthy financial conditions, according to a report from the Federal Reserve. The net worth of a typical household surged by 37% from 2019 through 2022. This increase was driven by rising home prices and strong gains in the stock market.

3. Historically Low Interest Rates

Low interest rates, which persisted from the pandemic recession of 2020 until late 2022, further bolstered consumer spending. The typical U.S. household, positioned between the richest and poorest, paid only 13.4% of its income to cover interest on debts. This proportion represented the lowest on record.

Potential Economic Slowdown

Despite the strong growth observed in the last quarter, some economists believe that it may represent a high-water mark for the U.S. economy.

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

They anticipate a gradual slowdown in the current October-December quarter, extending into 2024. This slowdown is expected to be driven by higher long-term borrowing rates and the impact of the Federal Reserve’s short-term rate hikes. As such, the future trajectory of the U.S. economy remains uncertain.

Conclusion

The monetary policy decisions of the Federal Reserve and other central banks hold immense significance for the global economic landscape. While the Fed is likely to maintain its current interest rate range in the upcoming meeting, the actions and policies of other major central banks worldwide will also shape the course of the global economy. The challenges faced by central banks are multifaceted, encompassing inflation control, economic growth, and geopolitical considerations. In this intricate web of monetary policy, each central bank must make decisions tailored to its unique economic circumstances.

The November 1, 2023 meeting of the Federal Reserve stands as a pivotal moment in shaping the future trajectory of the U.S. economy and, by extension, the global economy. As we closely monitor the statements of Fed Chair Jerome Powell and the indicators that inform the central bank’s decisions, we gain insights into the complex dance of monetary policy in a dynamic and interconnected world. The decisions made by central banks are not isolated events but rather threads woven into the fabric of the global economy, influencing markets, businesses, and individuals around the world.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/