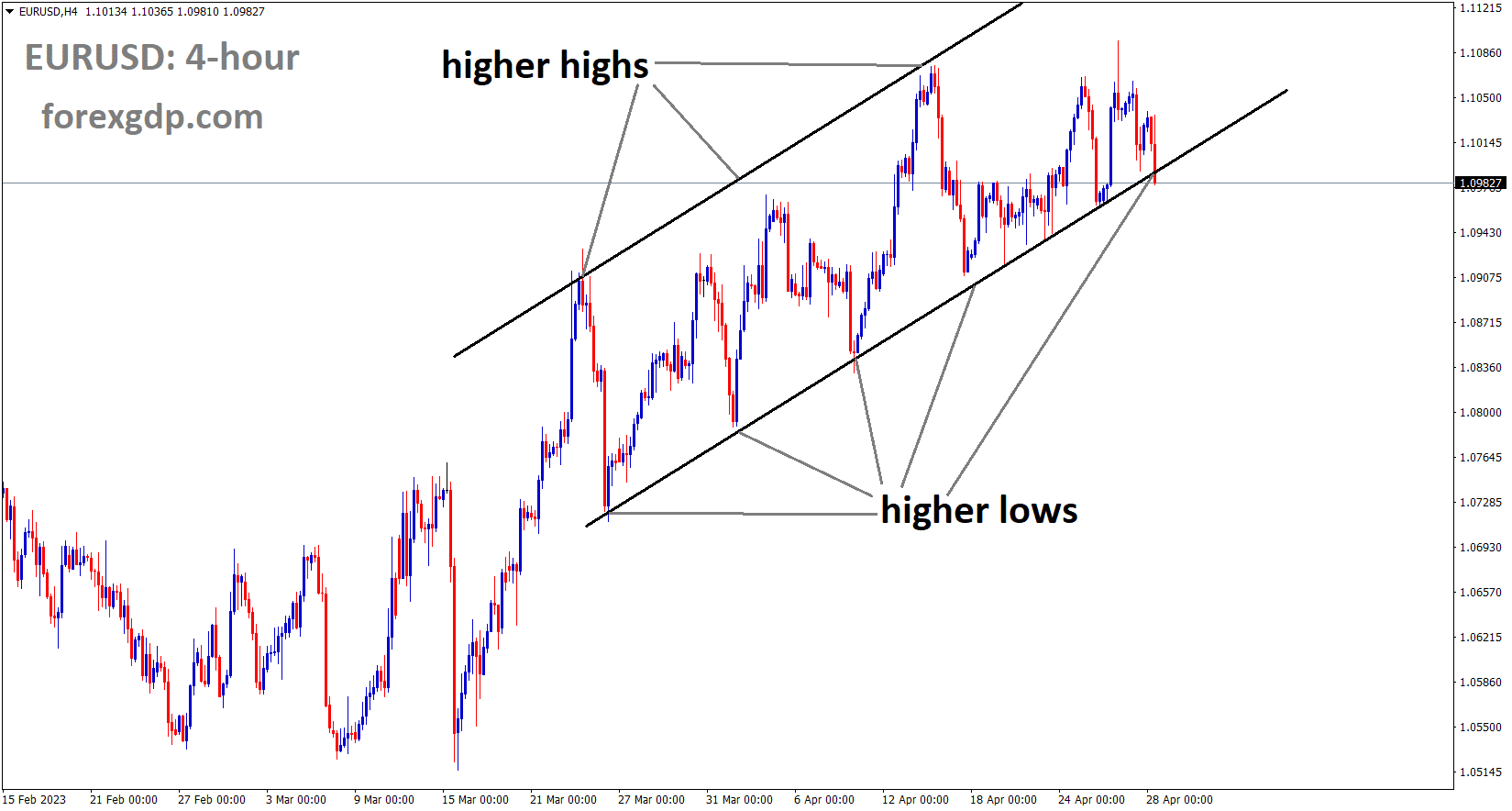

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The first quarter GDP for the Eurozone came in at 0.20%. On an annual basis, GDP is growing by 1.4% instead of the 1.8% forecast. The following information keeps ECB policymakers optimistic that a recession won’t occur in 2023. Additionally, a lack of labour drives up consumer spending in the Eurozone.

The cash rate forecast by Danske Bank is projected to increase by 50bps following the ECB meeting next week.

Following a steep sell-off on Thursday, the EURGBP pair has begun to gain momentum near 0.8820. As investors turn their attention to statistics on the German Harmonised Index of Consumer Prices and Eurozone Gross Domestic Product, the cross is beginning to show signs of recovery. The preliminary Eurozone GDP and German HICP releases have major significance because they will be the most recent economic statistics before the European Central Bank announces its interest rate decision, which will be made next week.According to consensus, first-quarter preliminary Eurozone GDP increased by 0.2% as opposed to a flat result. Preliminary estimates for GDP growth on an annual basis indicate a weaker rate of 1.4% growth than the 1.8% previously reported. Due to a labour shortage, ECB policymakers are optimistic that the Eurozone would avoid a recession and experience strong consumer spending.

Preliminary monthly inflation data for Germany, meanwhile, show an acceleration of 0.8% from the 1.1% pace registered in the previous month. The ECB’s policymakers will feel some relief as a result of this. The core Consumer Price Index (CPI) will, however, be the subject of more attention because, in the opinion of ECB policymakers, it has remained very tenacious. Danske Bank analysts predict that ECB President Christine Lagarde will raise interest rates by 50 basis points, without providing any precise forward guidance but instead sticking to her previous practise of basing decisions on facts. The lack of inflation-softening signs on the front of the pound sterling is supporting the Bank of England’s case for more rate increases. For its May monetary policy meeting, BoE Governor Andrew Bailey is expected to raise rates by a total of 25 basis points to 4.50%.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

First Republic bank in the US suggested selling half of its loan books to close a $100 billion deposit shortfall with investors in order to allay market concerns about US banks’ potential impact. Selling its assets, such as Gold and the US Dollar, causes Gold and the USD to turn positive. Today’s scheduled US Core PCE index data is predicted to decrease by 4.5% YoY as opposed to the prior reading’s 4.6%.

In the early hours of Friday’s Asian session, the price of gold declines to $1,986, reversing late Thursday’s corrective rally off the weekly low. As a result, the precious metal maintains the downside bias from the previous day, which was mostly supported by data on growth, inflation, and employment in the United States. However, the positive performance of the stock market, driven by the tech titan’s earnings, combines with the XAUUSD traders’ trepidation about the Fed’s preferred inflation gauge. Prior to the Federal Open Market Committee monetary policy meeting the following week, the gold price supports positive inflation indications from US statistics. The initial readings, sometimes referred to as advance readings, of the US gross domestic product for the first quarter (Q1) of 2023 showed conflicting results on Thursday. However, the GDP Price Index grew slightly to 4.0% on an annualised basis from 3.9% previously and 3.8% market consensus, while the headline US GDP Annualised eased to 1.1% from 2.0% expected and 2.6% prior. Additionally, the Personal Consumption Expenditure Prices for Q1 increased to 4.2% from 3.7% in earlier readouts, and the Core PCE figures also exceeded market expectations of 4.8% and the previous reading of 4.4% with a mark of 4.9% for the same period. It should be mentioned that the US Dollar was also able to stay firmer due to a drop in the weekly initial jobless claims.

Following the release of the data, the US Dollar Index was able to post a significant gain of about 30 pip before erasing some of its gains but still closing Thursday with a daily positive reading. The same originally drove the price of gold to probe the weekly low in the vicinity of $1,984 before cutting losses and retreating from $1,990 recently. However, it should be mentioned that Wall Street experienced its largest daily gain in a week thanks to the risk-on sentiment, which was mostly driven by the strong US technology giants’ profits and mixed US statistics. The same factor increased US Treasury bond yields and supported the price of gold.

SILVER Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The XAUUSD is weighed down by the hawkish Federal Reserve wagers and news that First Republic Bank aims to liquidate half of its loan book to close a $100 billion deposit flight gap, which in turn affects US banking fallout fears. The likelihood of a standoff in the US debt ceiling negotiations, where most policymakers have opposing viewpoints, may also be a factor impacting on the price of gold. Kevin McCarthy, the speaker of the House, recently declared, “I won’t pass a clean debt-limit increase. Moving on, the recent hawkish Federal Reserve (Fed) concerns, the market’s geopolitical concerns, as well as the banking FRB-led banking troubles, are expected to keep the gold price under pressure. The Fed’s favoured inflation indicator, the US Core Personal Consumption Expenditure (PCE) Price Index for March, which is predicted to decline to 4.5% YoY from 4.6% in February, is what determines how far lower the quotation can go. If the inflation indicators are weaker than expected, the gold price may recover some of its recent losses while supporting the risk-on attitude. Strong data readings, however, might allow the Fed to delay its shift in policy, which might then lead to the much-needed decline in the price of gold.

USDJPY Analysis

USDJPY has broken the Descending channel in upside.

Japan’s Bank No adjustments were made to the YCC policy settings or the monetary policy as of today. Japan will soon use ultra-accommodative policy measures to reach its 2% inflation target. After the BoJ expressed dissatisfaction with the Dovish approach on monetary policy, the Japanese Yen declined against counterpairs.

The Bank of Japan maintained its ultra-loose policy settings, including the closely monitored yield curve control policy, but eliminated its forward guidance that committed to maintaining interest rates at current or lower levels, which caused the Japanese yen to decline. After Nikkei reported that the BOJ would forgo revising YCC but was considering changing the expression in forward guidance regarding the possibility of further easing policy, USD/JPY had been volatile about an hour before the release of the BOJ rate decision. At his first press conference earlier this month, Japan’s new central bank governor Kazuo Ueda stressed that the bank is not in a rush to change the ultra-accommodative policy settings, including yield curve control. As a result, market expectations were muted going into the meeting. However, some were anticipating adjustments to the forward guidance as a way to get the markets ready for the end of the government’s massive stimulus programme. One-week USDJPY risk reversals have been substantially skewed in favour of JPY, indicating that the options market was set up for hawkish outcomes given that the BOJ is not unfamiliar with giving surprises. The YCC band’s upper limit was unexpectedly increased by the central bank in December, and in January, when some expected it to be further widened, the bank decided to hold steady.

Japan’s inflation rate is still above the BOJ’s 2% target; data from last week indicated that the CPI fell from 3.3% in February to 3.2% in March. The new governor’s justification for maintaining the ultra-easy policy is that recent inflationary pressures have been caused by cost-push and will therefore turn out to be temporary. Earlier this month, Ueda stated that significant adjustments to YCC should be considered by taking into account market, price, and financial trends. At the same time, he advised the BOJ to delay normalising monetary policy as little as possible to leave room for changes at the June meeting. The US PCE price index data that will be released later today, the US FOMC meeting on May 3, and the ECB meeting on May 4 will now draw attention. The Fed’s stance at its meeting next week will determine whether or not the USD/JPY surge is sustainable.

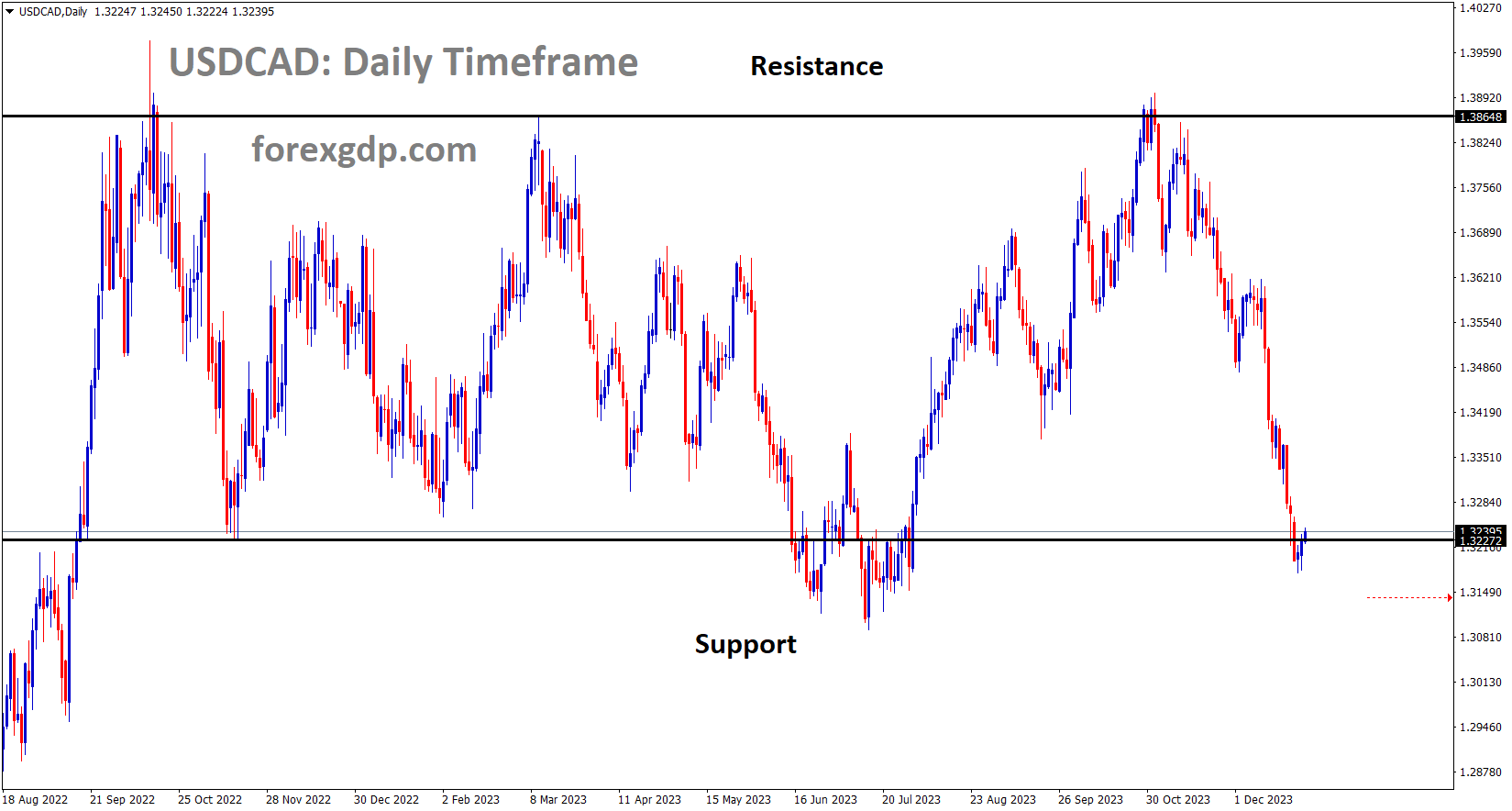

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

These data become true today and the Bank of Canada reconsiders for rate hikes in the next meeting, which will be a favourable tone for the the CAD. Today’s CAD GDP for February month is predicted to fall by 0.20% from the previous reading of 0.50%, which is positive for the Canadian Dollar.

After interrupting a six-day winning streak the day before, USDCAD grinds near intraday high during early Friday morning in Europe. Prior to the important data from Canada and the US, the Loonie pair makes predictions based on the general strength of the US Dollar. The current decline in WTI crude oil prices, Canada’s primary export good, is also probably to purchasers’ advantage. However, after retesting the monthly low on Wednesday, the WTI eases from an intraday high of $75.43 to $75.05 by press time, mildly bid for the second straight day. However, as negative sentiment joins hawkish Fed bets, the US Dollar Index continues the previous day’s recovery moves while refreshing intraday high above 101.80, up 0.30% on a day at the latest. Recent headlines involving First Republic Bank (FRB) and China are among the newest issues to test public opinion. According to unnamed sources cited by Reuters, representatives from the Federal Reserve, the Treasury Department, and the Federal Deposit Insurance Corporation (FDIC) are organising urgent discussions to save First Republic Bank.

The Taiwan problem, however, is a fine line that should not be crossed, according to China’s envoy to Japan. It should be noted that despite the change in governor, the Bank of Japan continued to support the ultra-easy monetary policy, which pushed on yields and helped the US Dollar to hold its stronger position. Additionally, positive readings for the first-quarter GDP price index and personal consumption expenditure prices revived demands for delaying the Fed’s policy turn from the day before. Future USDCAD traders are anticipated to applaud the most recent price run-up, supported by a risk-off mindset and widespread US Dollar strength ahead of the major data. Nevertheless, the monthly Canada GDP for February, which is predicted to fall from 0.5% to 0.2%, could strengthen the upward momentum for the Loonie pair. Any unfavourable surprise from the US Core PCE Price Index for March, which is predicted to ease to 4.5% YoY from 4.6% before, won’t hold back the sellers, though.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

The Federal Deposit Insurance Corporation, Treasury Department, and US FED organised a meeting for the rescue of First Republic Bank, according to the news, citing three sources. They also organised a meeting with banks and private equity firms to resolve the default and save public cash. The role of the US Government in this rescue attempt is unclear.

Officials from the Federal Deposit Insurance Corporation , the Treasury Department, and the Federal Reserve are coordinating urgent talks to rescue First Republic Bank as private-sector efforts led by the bank’s advisers have not yet resulted in a deal, according to three sources familiar with the situation. Recently, government agencies have begun arranging talks with financial institutions to discuss creating a lifeline for the struggling lender. The presence of the government is assisting in bringing more parties to the negotiating table, such as banks and private equity groups. It’s unclear if the US government is thinking about helping to save First Republic through the private sector.

On June 7, the antitrust agencies of the European Union will make a decision regarding UBS’ acquisition of Swiss Bank Credit Suisse. On April 26, UBS submitted a request for clearance under the European Commission’s policy on competition. The deadline was set for June 7. On March 19, UBS and Credit Suisse reached an agreement for UBS to acquire Credit Suisse’s stock worth over 3 billion Swiss Francs and losses of up to 5 billion Swiss Francs.

By June 7, European Union antitrust authorities will make a determination regarding UBS’ proposed acquisition of fellow Swiss bank Credit Suisse, according to a statement from the European Commission. According to the website for the Commission’s competition policy, UBS submitted its request for clearance on April 26. A preliminary deadline for a judgement was established for June 7. On March 19, UBS and rival Credit Suisse reached an agreement to merge for 3 billion Swiss francs ($3.23 billion) in stock and to take on up to 5 billion francs in losses. This shotgun merger was facilitated by Swiss regulators in an effort to prevent further market-shaking instability in the global banking industry.

USD Index Analysis

USD Index is moving in the Descending channel and the market has reached the lower high area of the channel.

Compared to the 2.6% reported in Q4 2022, the US Q1 GDP for 2023 came in at 1.1%. These lower figures resulted from a decline in private inventory investment and a slowdown in fixed non-residential investment in the US.

According to the most recent US Bureau of Economic Analysis figures, the US economy expanded by 1.1% in Q1, falling short of forecasts of 2% growth. In Q4 2022, the US economy expanded by 2.6%. “Compared to the fourth quarter, the deceleration in real GDP in the first quarter primarily reflected a downturn in private inventory investment and a slowdown in non-residential fixed investment,” the BEA reports. An increase in consumer expenditure, an uptick in exports, and a lower decline in residential fixed investment partially compensated these developments. Imports appeared. On May 25, the second Q1 GDP estimate for the US will be made public. The first look at Core PCE prices increased to 4.9% compared to a prediction of 4.7% and 4.4% in the prior quarter, as growth slowed and inflation increased.

The release of Core PCE Price Index (March), the Federal Reserve’s favoured indicator of US price pressures, will provide the latest look at US inflation on Friday at 13:30 UK. With the market now pricing in a 25 basis point increase to 500-525, tomorrow’s carefully expected inflation release and today’s growth and price data will play a significant role in how the FOMC decides to set interest rates next week. The US Federal Reserve will then stop rising interest rates before beginning a rate-cutting cycle at the end of the third quarter, according to current market pricing. The PCE statistics helped the US dollar advance, but it still has a medium-term downturn. The 20-day simple moving average is proving to be a strong resistance for the dollar, and it is likely to stay that way until Friday’s data release.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Due to lower inflation than anticipated by the UK Government and Bank of England, the Bank of England is anticipated to increase by 25 basis points in its May meeting. Higher consumer spending and higher labour demand on the UK labour market prevent the country’s inflation from declining.

In the early North American session, the GBPUSD pair draws some sellers near the psychological level of 1.2500 and descends to a new daily low after the release of the US macro data. However, spot prices manage to recover a few pip in the most recent hour and are currently trading with a slight negative bias, around the mid-1.2400s. This Thursday, the US Bureau of Economic Analysis revealed that between January and March, the economy’s growth slowed from a 2.6% annualised pace to 1.1%, falling short of forecasts for a reading of 2.0%. According to additional report information, the GDP Price Index increased marginally to 4% in the same period from 3.9%, versus expectations for a reading of 3.8%. The Personal Consumption Expenditures Prices increased to 4.2% from 3.7% on a quarterly basis, signalling an unanticipated escalation in price pressures.

Additionally, according to data released by the US Department of Labour, initial unemployment claims decreased to 230K in the week ending April 22 from 246K the week before and 248K predicted. The level is also the lowest it has been in three weeks. However, the positive macroeconomic data reinforces predictions for a further 25 basis point lift-off at the upcoming FOMC meeting in May and continues to support a rise in US Treasury bond rates, which supports the US Dollar and puts some pressure on the GBPUSD pair. The Bank of England is widely expected to raise interest rates by 25 basis points in May, so the downside is still cushioned, at least for the time being. This calls for considerable prudence before making strong bets against the GBP/USD pair and setting up for any significant fall. Additionally, traders are hesitant and now eagerly anticipate the release of the US Core PCE Price Index on Friday, the Fed’s favoured inflation indicator, which will have a significant impact on the short-term USD price dynamics.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Data for the Australian PPI (Q1) were less favourable than anticipated, indicating that the RBA will retain the cash rate at 3.60% at the next meeting. The Q1 PPI measurement was 1.0%, down from the previous figure of 1.7%. Annual PPI decreased from a release of 5.8% to 5.2%. Following the announcement of the news, the Australian dollar fell.

The AUDUSD pair has had a steep loss as its effort at a recovery during the Asian session failed to move over 0.6640. As investors moved their funds into the US Dollar Index out of concern over the Federal Reserve’s (Fed) decision on monetary policy, the Australian asset came under selling pressure. The S&P500 futures decline in the Asian session has persisted as pre-Fed policy concern affects market participants’ risk appetite. The protracted recovery action of the USD Index has overcome the immediate obstacle of 101.70. The market for US government bonds has drastically declined as another interest rate increase from the Fed is widely anticipated. The 10-year US Treasury rate has dramatically climbed and is now close to 3.53%.On Thursday, despite a steep decrease in the quarterly Gross Domestic Product data, the USD Index maintained its downward trajectory. GDP had a decline of 1.1% as compared to the prior expansion of 2.6%. Businesses lowered their inventory to offset consumer spending as a result of the gloomy economic forecast. Businesses will have the opportunity to restart the second quarter with little inventory, though.

The Australian dollar is under intense pressure as a result of predictions that the Reserve Bank of Australia will retain its neutral position on interest rates. The Reserve Bank of Australia’s governor, Philip Lowe, kept the Official Cash Rate at 3.60%, arguing that the current range of interest rates is adequate to tame stubborn inflation. The dramatic deceleration in Australia’s Producer Price Index strengthens the case for sticking with the existing interest rate plan. Quarterly PPI has risen by 1.0% at a slower rate than the 1.7% prior release and the 1.5% expectation. The annual PPI has been lowered from the estimates and the previous publication, which was 5.8%, to 5.2%.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Despite the US GDP coming in below projections yesterday, the New Zealand dollar remains normal. Readings for business activity and confidence in New Zealand reveal inconsistent data with earlier releases. The next catalyst for the NZDUSD today is the US Core PCE index data.

NZDUSD rises in the North American session after falling to a daily low of 0.6114, even though interest for the US Dollar was increased by recession worries triggered by US economic data. The NZDUSD is now down a negligible 0.09% at 0.6131. Wall Street is not displaying a dimmed view of the American economy. The US Department of Commerce reported that the Advanced Gross Domestic Product for Q1 in 2023 increased by 1.1% QoQ, below predictions of 2%, and lagged 2022 last quarter at 2.6%. Nevertheless, the antipodeans are making up for prior losses in the foreign exchange market. The US Core Personal Consumption Expenditure increased by 4.9% QoQ compared to projections of 4.8%, according to the study. As long as inflation keeps rising, the US Federal Reserve (Fed) would continue to tighten monetary policy.Initial Jobless Claims increased by 230K for the week ending April 22, which was less than expectations of 248K, according to the US Department of Labour, ending a streak of three weeks in a row in which they above expectations.

The NZDUSD oscillated between the day’s high and 0.6130 after the data release before falling into the 0.6120 region. The pair gained some distance afterwards and are currently at 0.6130s. The US Dollar Index, which measures the value of the dollar in relation to a basket of peers, increases 0.20% to 101.650. US Treasury bond yields increased as data supported the Fed’s rate increases in May. The odds of a 25 basis point hike in interest rates for the May meeting increased to 84.8%, up from 72.2% on April 26. The ANZ Activity and Business Confidence report for April in New Zealand revealed conflicting results, with the former increasing. However, it stayed negative while the latter fell below the reading from the previous period.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/