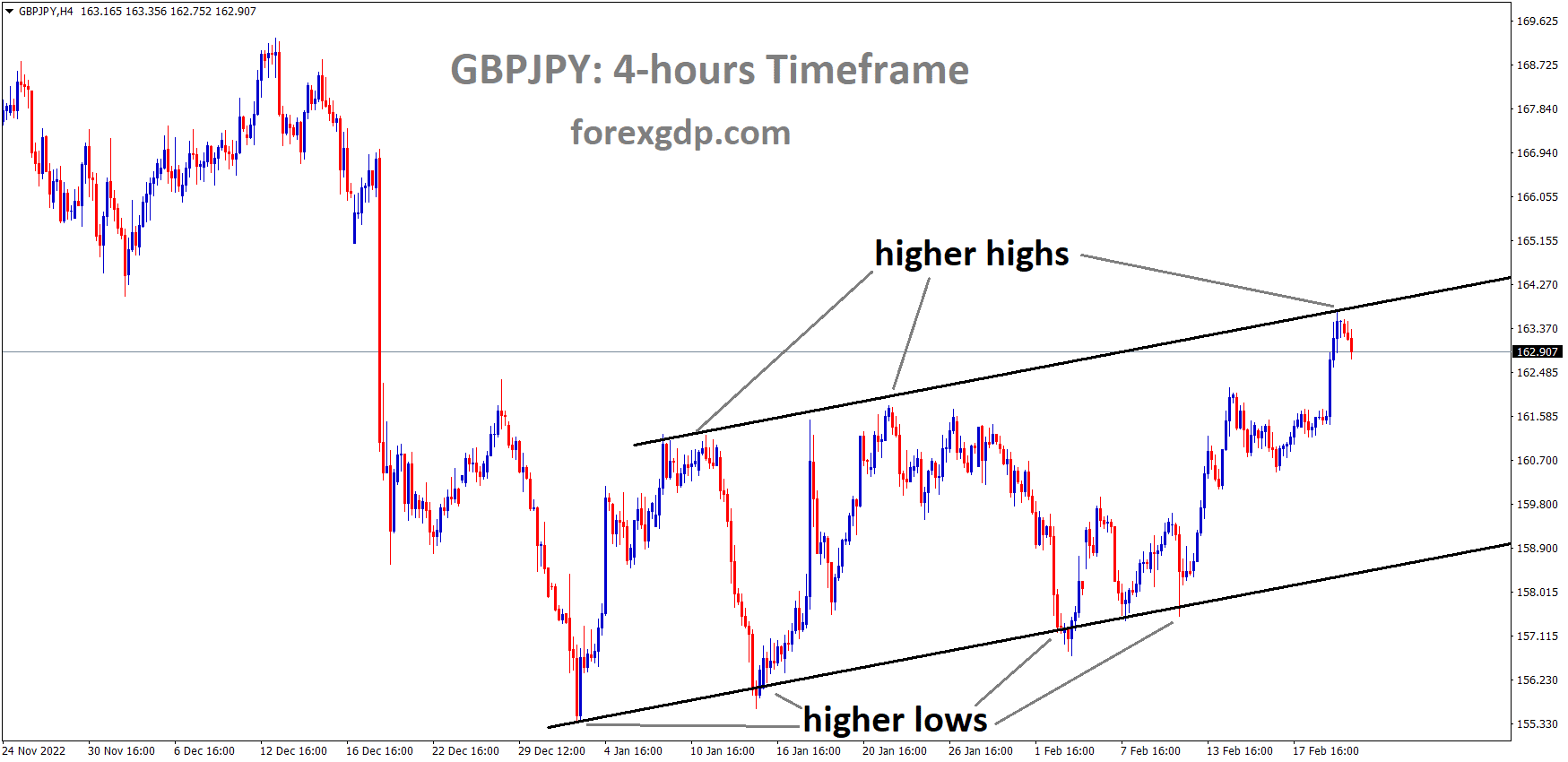

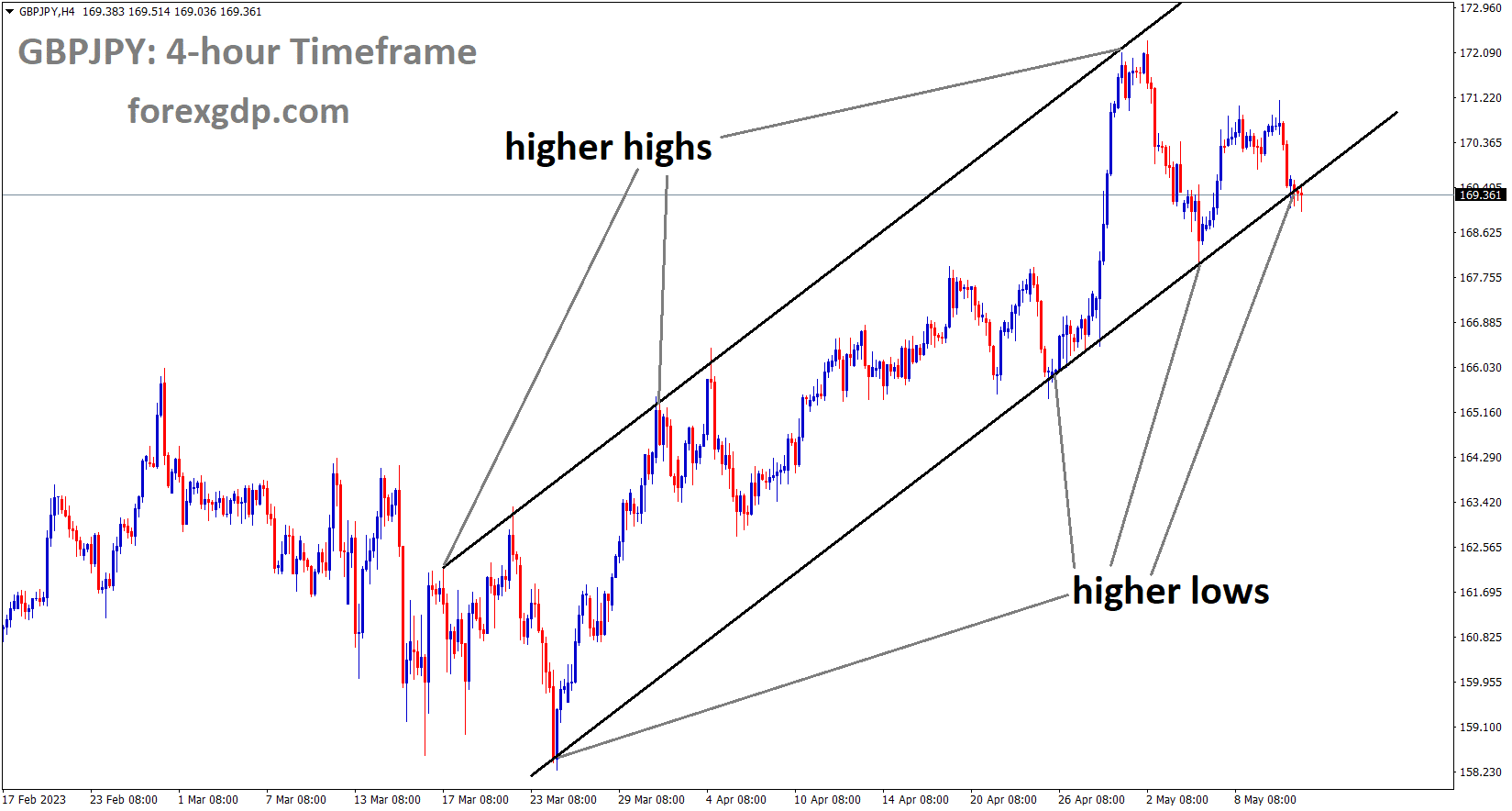

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Before the G7 meeting, Japan’s Finance Minister Shunichi Suzuki stated, “We will discuss Ukraine’s support for financial aid.” We will talk about financial regulation for banks, but not about the US debt ceiling because that is a single country’s policy. On May 13, we will meet with US Treasury Secretary Yellen to discuss financial regulations and credit policies.

Japanese Finance Minister Shunichi Suzuki comments on a variety of topics ahead of the G7 meeting.Following the financial support pledged thus far, the G7 will discuss Ukraine support. Will talk about how to strengthen global supply chains. When asked about US debt ceiling issues, he is unlikely to discuss individual countries’ policies. When asked about the US debt ceiling, the G7 is unlikely to reach a unified solution. On May 13, he will meet with US Treasury Secretary Janet Yellen. I am not going to say what I will talk about with Yellen right now. I would like to talk more about financial regulation.

GOLD Analysis

XAUUSD Gold price is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

Gold prices traded near all-time highs yesterday, while US CPI data came in lower than expected, and the US may enter a recession in the second half of 2023 due to tightening monetary conditions. The US debt ceiling limit issue is a major focus this week, and it has the potential to drive gold prices.

On Wednesday, gold was on a wild ride. The precious metal managed to rally nearly 0.85% in early morning trading after softer-than-expected US CPI data sparked a steep drop in US Treasury yields. The rally, however, was short-lived, with the XAUUSD pair back in the red by late afternoon in New York, falling about 0.2% to $2,035 at the time of writing. Bullion’s counter-intuitive reaction to the bond move suggests that the “slowing inflation” theme was pre-traded; after all, prices have risen more than 11% since early March, indicating that the rally was clearly stretched. This implies that nominal bond yields would need to fall much further in order to see higher highs and possibly a new record in gold. The prerequisite for gold to regain its lustre is unlikely to be a high hurdle to overcome. Growing headwinds for the US economy, such as tightening credit conditions for businesses and households in the aftermath of the US banking sector turmoil that began in March, could tip the country into a painful recession later this year.

SILVER Analysis

XAGUSD Silver price is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

With the economy worsening, forward-thinking traders will try to outpace the Fed by anticipating steep rate cuts, putting downward pressure on the Treasury curve. With this backdrop, it is only a matter of time before the 10-year yield drops to new multi-month lows below 3.25%, its April trough in 2023. The threat of a recession, combined with the ongoing debt ceiling saga in the United States, may soon drive increased demand for safe-haven assets. Gold, traditionally regarded as a defensive asset, stands to benefit from financial market flight-to-safety episodes. For these reasons, the XAU/USD remains bullish for the time being.

USDCAD Analysis

USDCAD is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

Building permits in Canada increased by 11.3% month on month in March, compared to -2.9% expected and up from 5.5% previously.

Oil prices have slowed after US CPI data came in lower than expected yesterday. Fears of a US recession reduce demand for oil from other countries. The Canadian dollar has a negative impact on oil prices, and the Bank of Canada has paused rate hikes until the end of 2023.

Early on Thursday, the USDCAD reverses some of the day’s losses inside the weekly trading range near 1.3400. By the time of publication, the intraday high had risen to near 1.3385. However, the recent gains in the USD/CAD pair may be explained by the weakening oil price and the US Dollar’s consolidation of losses brought on by inflation ahead of the release of the US Producer Price Index for April. Although the US Federal Reserve is being dovish, the pair sellers are still optimistic, especially in light of the day before’s discouraging US Consumer Price Index data. After retreating from a weekly high the day before, WTI crude oil is holding lower ground at $72.80. As a result, the price-negative Oil inventories and mixed sentiment are excused by the black gold, which also explains weaker inflation data from China and the US. It is important to remember that WTI crude oil is Canada’s top export, so any change in the price of oil can affect the USDCAD pair. At home, Canada’s Building Permits rose 11.3% MoM in March, outpacing market expectations of -2.9% and previously reported readings of 5.5% that had been revised downward. Recently, wildfires in Alberta forced the oil refineries to shut down before starting up again on Wednesday, which may have helped the Canadian Dollar hold its ground despite the recent USD recovery.

Speaking of the data, the Producer Price Index in China declines to -3.6% YoY compared to -3.2% market consensus and -2.5% previous readings, while the headline Consumer Price Index in China eases to 0.1% YoY from 0.7% prior, versus 0.3% expected. The US Consumer Price Index, on the other hand, eased to 4.9% YoY in April, below the market’s forecast of 5.0% inflation. This is the first reading below 5.0% in two years. The MoM figures, however, were in line with the optimistic 0.4% forecasts as opposed to the previous readings of 0.1%. In addition, the core CPI, also known as the CPI excluding food and energy, came in at 5.5% annually and 0.4% monthly, which was in line with market expectations, compared to 5.6% and 0.4% prior readings, respectively. In the midst of these manoeuvres, the US Treasury bond yields continue their negative trend and the S&P 500 Futures post modest gains, which weigh on the US Dollar Index. Looking ahead, the US PPI is a key catalyst to watch for USDCAD pair traders due to a light calendar in Canada, cautious sentiment ahead of the important Bank of England quarterly monetary policy report, mixed feelings for the US debt ceiling, and banking fallouts.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

Thomas Jordan, governor of the Swiss National Bank, stated that regional inflation in Switzerland is higher than the SNB’s target. With rate increases in the coming months, we will quickly return the Swiss franc to levels of 1-2% inflation.

Although it seems to be consolidating near the year-to-date lows at roughly the 0.8800 handle, the USDCHF continues its bearish downtrend after US data revealed that prices are beginning to decline. Additionally, USDCHF bears applauded the governor of the Swiss National Bank’s hawkish remarks. The USDCHF is currently trading in the 0.8890s range. The main topic of discussion on Wednesday was inflation. The US Bureau of Labor Statistics revealed the Consumer Price Index in April expanded as expected by 0.4% MoM, while annually based, the data showed an improvement with prices edging below estimates figures came at 4.9%, below projections of 5%. The core CPI data, which the US Federal Reserve monitors closely to assess inflation without the volatile items, jumped by 0.4% MoM. Core inflation increased by 5.5% on an annual basis, matching market expectations and remaining constant from the previous reading. Although inflation is still high, the USD/CHF major declined from its daily high of 0.8927 back towards the 0.8890 region, hurting expectations for higher prices. The 20-day exponential moving average at 0.8892 and the psychological 0.8900 level served as the upper limit of the USDCHF rally.

SNB Governor Thomas Jordan made a comment about recent events in Switzerland that inflation is still higher than desired by the central bank and above average for price stability. Jordan added that they do not foresee a wage-price spiral and emphasised that “at the moment” the monetary policy is not sufficiently restrictive. He claimed that international inflation was the cause of the nominal increase in the Swiss franc. Given the situation, the CME FedWatch Tool predicts that the Federal Reserve will leave interest rates unchanged at its meeting in mid-June, with odds of 93.6%. The US Treasury bond yields, specifically the 2-year note, which is most sensitive to changes in monetary policy, decreased by 11 basis points to 3.910% as a result. The hawkish language of the SNB may discourage USDCHF bulls from entering the market. Since Switzerland’s inflation rate continues to be higher than the SNB’s target, the SNB is anticipated to tighten monetary conditions even further.

USD Index Analysis

USD Index is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

Last day’s US CPI data of 4.9% in April month YoY causes the US Dollar to fall against counter pairs. The Fed may pause rate hikes at the next meeting, which is more likely due to CPI readings in the lower ranges.

The US dollar fell overnight after headline CPI came in at 4.9% year on year to the end of April, down from 5.0% expected and prior. Core CPI was 5.6%, which was in line with forecasts for the same period. Rates markets have increased their bets that the Fed will lower its target rate by the end of the year. The September Federal Open Market Committee meeting saw nearly 25 basis points shaved off monetary policy in the futures and overnight index swaps (OIS) markets. Treasury yields are lower across the yield curve compared to yesterday, with the benchmark 2-year bond currently trading near 3.90%. However, yields at all tenors are still comfortably above where they were in March following the collapse of SVB Financial.

Today, US Treasury Secretary Janet Yellen addressed the G-7 Finance Ministers meeting in Tokyo. She reiterated many of her recent comments about the importance of resolving the US debt ceiling issue. China’s inflation read was also soft today, with headline CPI coming in at 0.1% year on year to the end of April, down from 0.3% in March. PPI came in at -3.6%, up from -3.3% predicted and -2.5% previously. Chinese government bond yields fell today, with the 10-year note falling below 2.7% for the first time since November of last year. Markets are also expecting more dovishness from the People’s Bank of China as a result of easing price pressures.

EURUSD Analysis

EURUSD has broken the Ascending channel in downside.

German inflation data came in at 7.2%, down from 7.4% the previous day. This is the impact of the ECB’s rate hike on the Euro economy; lower inflation is good for Europe’s regions, and consumer spending will be tightened, as will business credit growth.

German inflation came in at the expected level. Over the last few days, comments from the European Central Bank’s Kazimir, Nagel, Schnabel, and dove, Stournaras have added to the debate. As is customary, those on the more hawkish end of the spectrum, such as Nagel and Schnabel, have stated that more needs to be done to reduce inflation and that rate cuts are unlikely in the near future. Stournaras, the ECB’s dove, chose to focus on a different message, stating that rate hikes will end in 2023. Nonetheless, markets continue to take into account what influential policymakers say.

To lower inflation, ECB officials have begun to accept interest rate increases through the September meeting. Some members of the ECB Board’s governing council believe that a rate increase of 25 basis points over the course of the next two meetings will not be sufficient to keep European consumer prices under control.

Bloomberg reported early on Thursday that European Central Bank officials are beginning to accept the possibility that interest rate increases will need to continue in September in order to fully control inflation. According to the sources, some members of the Governing Council of the European Central Bank are speculating that the two additional quarter-point increases that are anticipated may not be enough to control consumer prices.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

UK According to Reed recruitment job source, job wage growth increased by 10% when job changes occur in the United Kingdom. So the average wage is 6.6% higher without a bonus and 5.9% higher with a bonus in February statistics. Strong wage growth leads to higher inflation in the UK, so the Bank of England must raise interest rates by 25 basis points today, as expected.

According to a recent Bloomberg report based on Reed Recruitment Jobs data, the UK job market remains buoyant, with people changing jobs seeing a 10% increase in their wages on average. This is significantly higher than the official UK data from last month, which showed average earnings including bonuses (3Mnth/Year) rising by 5.9% in February, while average earnings excluding bonuses rose by 6.6% over the same time period.Tomorrow, the Bank of England will raise the UK Bank Rate by 25 basis points to 4.50%. Recent inflation data have shown that price pressures have remained stubbornly high, and today’s Reed Report, while not an official data point, will have many on Threadneedle Street concerned that a strong labour market will keep inflation higher for longer. Following the decision, BoE governor Andrew Bailey is expected to highlight the job market as an ongoing source of concern in his post-decision commentary and press conference.

The latest UK GDP data will be released this week on Friday, and it is expected to show that the UK avoided a technical recession in the first three months of this year. Preliminary year-on-year Q1 data show growth of 0.2%, compared to 0.6% in Q4 2022, with year-on-year growth slowing to 0.4% in March from 0.5% in February.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

China’s CPI data for April came in at 0.1% year on year, which was lower than the 0.30% forecast. PPI data came in at -3.6%, versus -3.3% expected and -2.5% in the previous reading.

China’s economic activity has slowed since the pandemic’s re-emergence; however, the Chinese government will boost the economy by providing additional stimulus, allowing it to recover to pre-pandemic levels.

China’s main imports from Australia are iron ore and coal; if China recovers, the Australian trade surplus will increase.

The Australian Dollar rose briefly after Chinese CPI came in at 0.1% year on year to the end of April, compared to 0.3% expected and 0.7% in March. PPI was -3.6%, up from -3.3% expected and -2.5% previously. According to the data, the People’s Bank of China may announce plans to stimulate the economy. The post-pandemic re-opening has not provided the boost to China’s economic activity that the government and market expected. A few mid-tier financial firms cut deposit rates last week, sparking speculation that lending rates will follow suit. It is possible that the PBOC is waiting for a clear Fed pause before cutting rates to re-ignite the economy. Government bond yields in China have been falling across the curve. For the first time since November of last year, the 10-year bond fell below 2.7% today. Many Australian exports are destined for China, and any stimulus measures that boost the Middle Kingdom’s economy could pave the way for a further boost to Australia’s trade balance, which is already at record levels.

If China’s economy returns to robust growth, demand for industrial metals such as iron ore and copper may rise. Market sentiment was already buoyed by expectations of a less hawkish Federal Reserve after US inflation gauges fell slightly overnight. Headline CPI was 4.9% year on year in April, down from 5.0% expected, and it appears to have emboldened the interest rate market to reinforce its view that the Fed will cut its target rate later this year. Treasury yields fell across the curve, with the largest moves seen in the 1 to 5-year segment. In the aftermath, the US Dollar lost ground and is still struggling to recover today. If the world’s two largest central banks adopt a dovish stance, the outlook for global growth may improve to some extent. The Australian Dollar has historically been sensitive to such shifts.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to Grant Robertson, the Minister of Finance for New Zealand, the government’s budget, which will be unveiled the following week, will focus on achieving fiscal sustainability and keeping inflation under control.

Food price index inflation for the month of April fell from 0.80% MoM to 0.50% MoM.

The inflation rate in New Zealand is 6.7%, which is higher than the RBNZ’s target range of 1-3%.

By lowering government spending to 30% less than New Zealand GDP, we hope to lower inflation.

According to Reuters, Grant Robertson, the finance minister for New Zealand, said on Thursday that the government’s upcoming budget would place a strong emphasis on fiscal sustainability as part of its efforts to keep inflation in check. New Zealand’s inflation rate is currently 6.7%, significantly higher than the central bank’s target range of 1% to 3%. Economists have cautioned that an increase in government spending could result in inflation remaining higher for longer.The food price index for New Zealand for April eases to 0.5% MoM from 0.8% in March and 0.4% in market expectations. We are determined to do our part to lower it, which includes lowering our spending as a share of the economy in the upcoming years. New Zealand’s economy is resilient, its fiscal position is solid, and spending was moving back towards the low to mid-30% range of GDP.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/