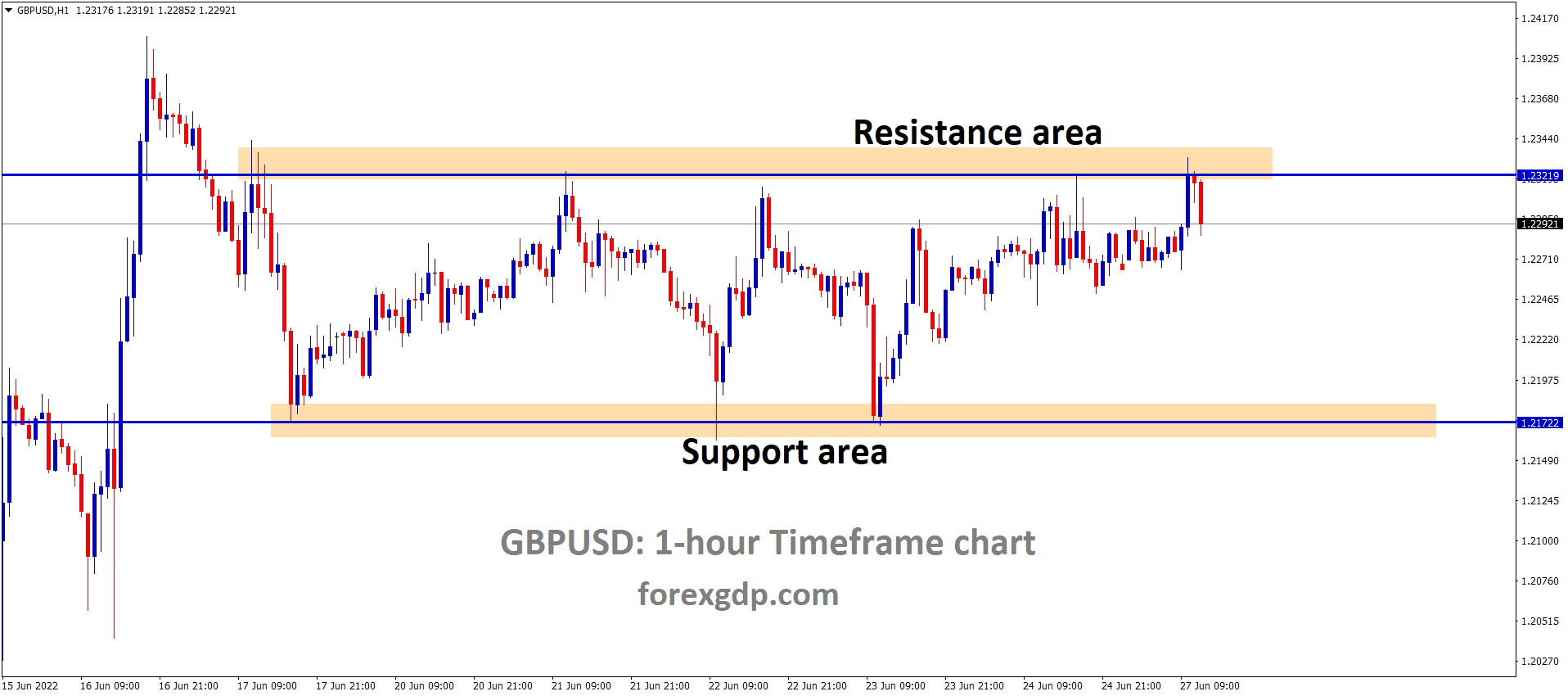

GBPUSD Analysis

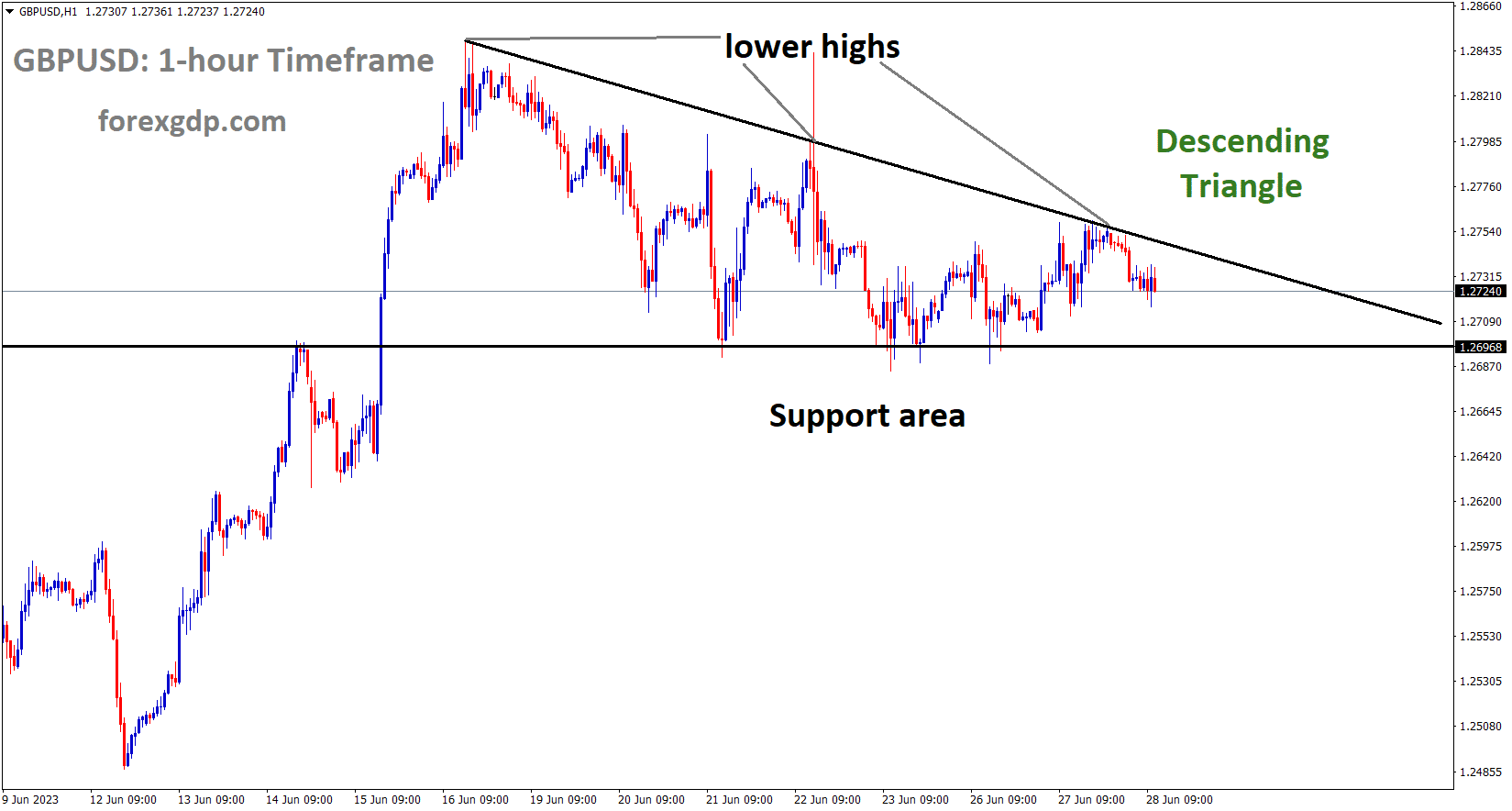

GBPUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

Bank of England’s concerns about an upcoming higher interest rate cycle and growing UK recession fears. At 8.7%, the inflation rate was higher than that of developed nations. Global demand is lagging due to ongoing tensions between the US and China over AI chip export disputes.

The GBPUSD currency pair is holding onto slight losses near 1.2730 as Wednesday’s London market opens, reversing the previous day’s recovery amid a variety of recent catalysts. However, rising concerns about the Bank of England (BoE) raising interest rates and the ensuing UK recession problems put pressure on the price of the pound sterling. On the other hand, mixed concerns about China and generally positive US data combine to nudge Cable sellers. The UK’s two-year Gilt, which also portrays the same, rises to its highest level in 15 years, reaching 5.24% at the latest, while also raising concerns about a 6.5% BoE peak rate in 2024. The GBP/USD bears are drawn in by expectations of more Chinese stimulus, which contrast with growing worries about a slower economic recovery in Beijing and worries about a Sino-American spat over the most recent AI restrictions on Chinese chip manufacturers. Additionally, a slew of US data allowed the US Dollar to reduce intraday losses and raise hawkish Fed bets, which in turn prodded the recent bulls of the Pound Sterling. The Durable Goods Orders, the Conference Board’s (CB) Consumer Confidence Index, and a few housing statistics stood out among them.

To illustrate the market’s shaky momentum, the S&P500 Futures pare the biggest daily jump in a fortnight with only minor losses, while the US Treasury bond yields remain low despite rising over the past two days. Future speeches by BoE’s Bailey and Fed Chair Powell will be crucial to monitor for the movements of the GBP/USD exchange rate immediately. However, the UK’s economic problems will receive a lot of attention, which could be good news for GBP/USD bears.

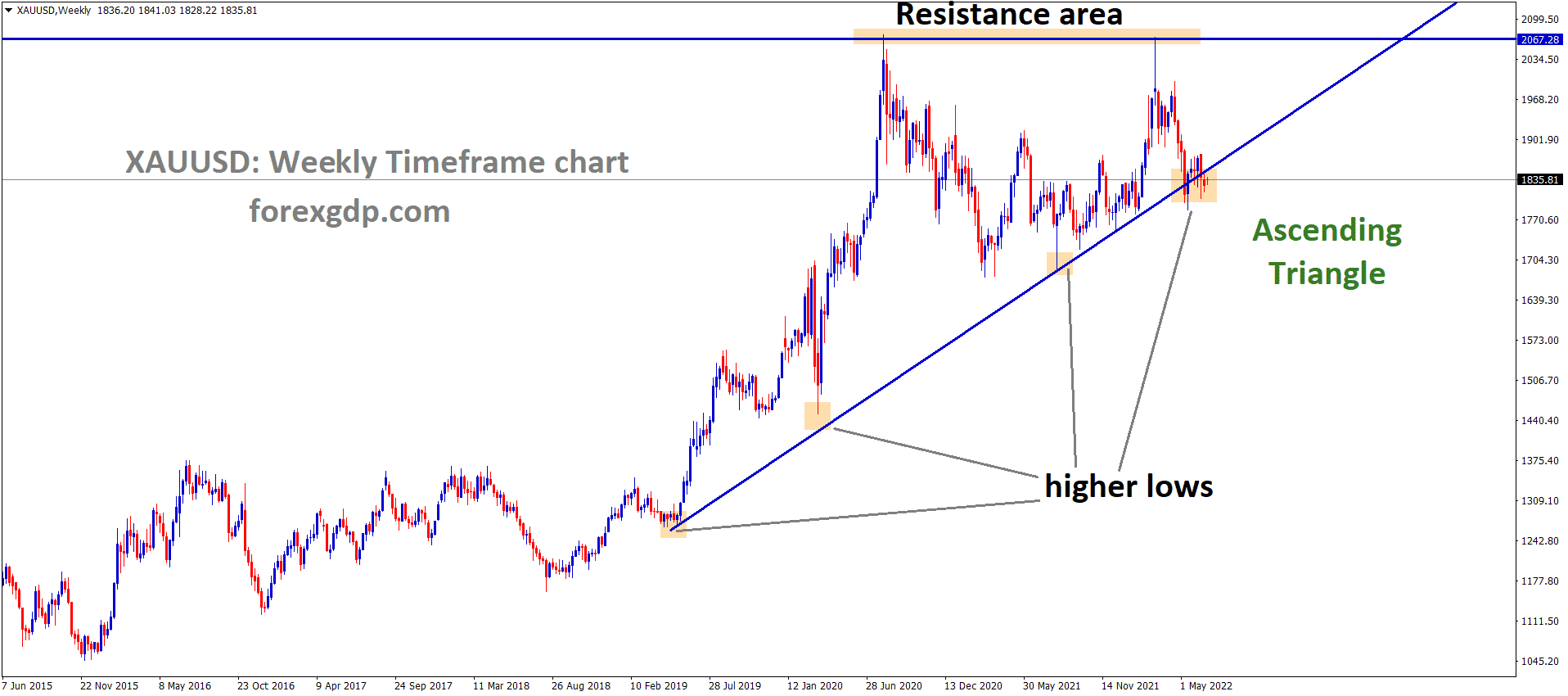

GOLD Analysis

XAUUSD Gold Price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Prior to the gathering of Central Bank Governors from around the world in Portugal, gold prices decline. Due to the strong US labour market and rising consumer confidence in June, US Jerome Powell reiterated a hawkish tone in upcoming meetings.

Going into the Wednesday session and ahead of Jerome Powell’s speech at the Federal Reserve later today, the price of gold is hovering around 3-month lows. The head of the Fed will participate in a policy panel discussion at the European Central Bank Forum on Central Banking in Sintra, Portugal. After the Federal Open Market Committee (FOMC) meeting in June saw a pause in rate hikes, he reaffirmed the bank’s tightening bias last week. The markets anticipated a rate cut in the near future as a result of the ‘hawkish hold’. Such expectations have been dispelled, and rates markets are now estimating that an easing in monetary policy will not happen until early 2024. The US Dollar registered some notable gains at the end of last week as the Fed’s rate path was readjusted, but this week has seen more range trading and sideways price action in many currency pairs. The 1-year US Dollar inflation swap has recently ticked up a little, which coincides with a slight reacceleration in inflation expectations. A period of easing in the first half of 2023 resulted in a flattening of the 2-year breakeven inflation rate as well. The market-priced inflation rate derived from Treasury inflation-protected securities is the breakeven inflation rate.

SILVER Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The breakdown of the CPI may be a potential source of justification for the market’s recognition that future inflation may be sticky. Looking closely at how energy prices affect the headline inflation gauge in particular, the Fed and the swap market may have concerns here. Russia has been dumping oil on all available markets to pay for the conflict in Ukraine. This week, it was reported that Russia surpassed Saudi Arabia as China’s top energy supplier. Headline Although the US CPI has been trending lower, this may only be temporary once the effects of lower energy prices are considered. The Fed has noted the continued strong price pressures in the services sector, and despite tightening policy, this area of the economy still appears to be tight with a robust labour market. The US CPI data released on July 12 will be closely scrutinised for hints about the Fed’s stance ahead of the July 26 FOMC meeting. The implications for US real yields may be a crucial aspect of the inflation outlook for the gold price. The market-priced inflation rate derived from Treasury inflation-protected securities (TIPS) for the same tenor is subtracted from the nominal yield to determine the real yield.

This might end up being a double-edged sword for the pricey metal. If CPI continues to rise, the Fed may be forced to adopt a more aggressive tightening stance, which could initially support the US Dollar. However, it might result in higher inflation expectations, which might cause real yields to decline, potentially making the yellow metal a desirable asset. The response in Treasury yields will be crucial to such a result. Real yields might nudge up, undermining the price of gold if they rise above the rise in market-priced inflation.

USD Index Analysis

USD index is moving in the Descending channel and the market has reached the lower high area of the channel.

Due to China being the US’s technological rival, US President Joe Biden stated that there will be a decrease in the export of AI chips to China. The dispute between the US and China boosts demand for the US dollar. According to data released yesterday, US consumer confidence increased to 109.7 in June from 102.5 in May. In light of Fed Powell’s speeches in Portugal today and tomorrow, the US dollar has strengthened.

Around 102.50, the US Dollar Index (DXY) begins to gain bids, breaking its two-day losing streak, as markets prepare for important data and events on Wednesday morning. Nevertheless, the US Dollar is under pressure from China’s risk-positive news and the economic optimism supported by positive US data. The gauge for the dollar against the six major currencies, however, is under downward pressure due to recent concerns about the US-China tension and a cautious attitude prior to Federal Reserve Chairman Jerome Powell’s speech at the European Central Bank Forum in Sintra. Late on Tuesday, Vice President Joe Biden of the US stated that China has serious issues. The Wall Street Journal (WSJ) news echoed his remarks when it reported that “the Biden administration is considering new restrictions on exports of artificial intelligence chips to China, as concerns rise over the power of the technology in the hands of US rivals, according to people familiar with the situation.” These headlines increased concerns about the escalating US-China dispute and supported the US Dollar Index. Tuesday’s headlines and remarks from Premier Li Qiang, along with the People’s Bank of China’s (PBoC) lower-than-anticipated fixing of the USDCNY rate in favour of the DXY bears, contributed to the perception that Asian lobbyists are pushing for looser regulations for Chinese stocks’ overseas listing. Furthermore, the Aussie pair was able to maintain its strength thanks to major Chinese state banks selling US dollars, according to Reuters.

It should be noted that despite optimism, a slew of US data late on Tuesday allowed the US Dollar to trim intraday losses but failed to stop the daily decline of the greenback. Despite this, US durable goods orders unexpectedly increased by 1.7% in May, compared to market expectations of -1.0% and 1.2% (revised). Additionally, the US Conference Board’s (CB) Consumer Confidence Index increased from 102.5 in May (revised from 102.3) to 109.7 for June. Similar to this, the US Housing Price Index increased in April from 0.5% in previous readings (revised) to 0.7%, exceeding the 0.3% forecast. The S&P/Case-Shiller Home Price Index reported a YoY decline of 1.7% for April, down from the prior month’s 1.1% but better than the -2.6% market expectations. The Richmond Fed Manufacturing Index improved to -7.0 in June from -15.0 in May and -10.0 expected, while New Home Sales increased 12.2% MoM in May from 3.5% prior and 0.5% anticipated. Despite the positive performance of Wall Street and the aforementioned catalysts, the S&P500 Futures print slight losses, and US Treasury bond yields continue to rise.

Looking ahead, news about China and the trajectory of global growth may amuse DXY traders prior to Fed Chair Powell’s important speech at the ECB Forum. According to analysts at the ANZ, the FOMC has made it very clear that in order to control inflation, there may need to be a period of sub-trend activity. However, so far, this does not appear to be the case. The same may combine with the most recent positive US data to support Powell’s continued hawkishness and fuel DXY bulls.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

This week’s price data for the Eurozone includes inflation data. The Portugal Economic Forum is scheduled for this week, and ECB President Lagarde is anticipated to strike a hawkish tone by pushing inflation readings down to the 2% range. Global gatherings of central bank leaders, with hawkish slants from the ECB, BoE, and FED, and dovish slants from the BoJ.

EURUSD is still fairly boring. Commerzbank economists evaluate the prospects for the two. It should come as no surprise that the Eurozone inflation data on Friday will be the next noteworthy event, with the data from the individual countries tomorrow possibly providing a first indication of what the overall data will look like. The high-profile panel at the ECB Forum this afternoon featuring Christine Lagarde, Jerome Powell, Andrew Bailey, and Kazua Uedo will be the previous interesting event. The Euro will remain strong if the price data for the Eurozone support the ECB’s tight policy. I think the Euro has more room to rise if it surprises to the upside. High inflation rates would imply that the ECB might act more because the market has confidence in its resolve to combat inflation. We are therefore pleased beyond belief with our prediction of 1.10 for the end of the quarter and sure that we will be able to deliver a precise landing.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Shunichi Suzuki, the finance minister for Japan, reaffirmed on Wednesday that he will, if necessary, take appropriate action in the case of excessive FX moves. FX levels are unremarkable. FX ought to move steadily. Current FX market has lopsided movements.

AUDUSD Analysis

AUDUSD is moving in the Descending Channel and the market has rebounded from the lower low area of the channel.

After the CPI data for May came in at 5.6% on the year, down from 6.8% in April, the Australian dollar declined. Due to CPI data coming in lower than anticipated in July, the RBA will be hesitant to raise rates by another 25 basis points.

The Reserve Bank of Australia may not need to raise interest rates as aggressively as previously anticipated, according to Australia’s monthly CPI indicator, which caused the Australian dollar to decline. Australia’s CPI for the month of May came in at 5.6% on the year, below the 6.1% forecast and significantly lower than the 6.8% recorded in April. After the release of the data, the likelihood of a rate increase by the RBA in July has slightly decreased. The RBA unexpectedly increased interest rates by 25 basis points earlier this month and stated that additional tightening may be necessary in order to bring inflation back to the target range. Undoubtedly, the monthly CPI numbers have fluctuated a lot, and they are frequently a poor indicator of the quarterly CPI, which is more important from the RBA’s perspective. The Australian retail sales due on Thursday and the US PCE data due on Friday are currently of utmost importance. Retail sales in May are predicted to have increased by 0.1% on a monthly basis. The resilience of global consumer spending would be strengthened by a higher-than-expected result despite the significant tightening of financial conditions. Data made public on Tuesday revealed that in June, US consumer confidence reached its highest level in almost one and a half years.

According to forecasts, the US Core PCE Price Index was unchanged in May at 4.7% annually but likely slowed down a little on a monthly basis to 0.3% from 0.4%. Compared to April’s 4.4%, the headline PCE Price Index is predicted to be 3.8% on a yearly basis. The US dollar, which increased significantly last week, could suffer if the on-month data is in line with or lower than expectations. While speaking at the European Central Bank Forum later on Wednesday, US Fed Chair Jerome Powell may not differ significantly from his testimony from last week. Andrew Bailey, Christine Lagarde, and Kazuo Ueda, the governors of the Bank of Japan and the Bank of England, will also be present. Powell is likely to keep using the hawkish language in light of the persistently high inflation. He could also reiterate what he said last week, which was that rates might rise gradually. The AUDUSD is testing a crucial converged cushion at the 89-day moving average and 0.6625, the 61.8% retracement of the early June rise, and the technical charts show that further downside may be constrained. However, for the immediate downward pressure to subside, the pair would need to move above the initial ceiling at Tuesday’s high of 0.6720. The March low of 0.6550 serves as the next point of support.

AUDCAD Analysis

AUDCAD is moving in the Descending Channel and the market has rebounded from the lower low area of the channel.

The RBA is expected to raise rates again in August, according to economists at Rabo Bank. The RBA set its interest rate at 4.10% in May, which is an 11-year high. By the end of the year, that rate will be reached, meaning that another 25 basis points will likely be added by the RBA in August.

In June, the RBA increased interest rates once more, pushing the cash rate to a new 11-year high of 4.10%. According to Rabobank economists, there will only be one more increase this year to bring the terminal cash rate up to 4.35%, and the August meeting is the most likely time for it to happen. We continue to advocate for an Australian terminal cash rate of 4.35%. We anticipate the upcoming (and last) rate increase to take place at the RBA Board meeting in August. Recent data on the labour market support raising policy rates, but overall, the economy is developing in line with RBA projections. The May monthly CPI figure’s softness gives us more confidence that the RBA is nearing the end of its cycle of rate hikes. One more increase would be in line with other central banks’ “least regrets” policies and take slowing private demand into account.

In May, the headline CPI for Canada was 3.4% YoY, which is less than the 4.4% recorded in April. As a result, the Canadian Dollar declines against other currency pairs. The Bank of Canada was on hold about raising rates due to lower inflation data.

The softer domestic data released on Tuesday, which showed that consumer inflation declined to its slowest pace in two years, has continued to weigh on the Canadian Dollar (CAD). In fact, according to Statistics Canada, the headline CPI slowed down in May from April’s 4.4% YoY rate to 3.4%. Additionally, the Core CPI of the Bank of Canada (BoC), which excludes volatile food and energy prices, fell short of consensus expectations and fell to 3.7% on an annual basis from 4.1% in April. In addition, the Loonie’s link to commodities is weakened by the overnight decline in Crude Oil prices.

AUDCHF Analysis

AUDCHF is moving in the Descending Channel and the market has rebounded from the lower low area of the channel.

Due to the significant financial loss of the company takeover and the support provided by SNB and Finance authorities, UBS plans to fire the Credit Suisse employees.

According to a Bloomberg report, 35000 people, or 30%, of the workforce, may be laid off. As a result of SNB restrictions on Margins and Losses, Credit Suisse already reduced more positions before merging with UBS.

UBS is about to start reducing employment at Credit Suisse. Traders and bankers in New York are some of the people most at risk from the chop. After layoffs at Goldman Sachs, Morgan Stanley, JPMorgan, and other companies, there are significant cuts. Deep cuts were expected at Credit Suisse, the bank that local rival UBS took over in an emergency rescue one weekend in March. The size of the anticipated reductions is still startling. Beginning in July, more than half of Credit Suisse’s global workforce will be reduced, according to Bloomberg, which cited unnamed people with knowledge of the situation. More than 20,000 people, in total. More people work there than at Blackstone, Jefferies, Lazard, and Moelis put together. According to Bloomberg, in addition to those in London and some Asian locations, Credit Suisse bankers, traders, and support personnel in New York will also be among those suffering the most from the layoffs.

Insiders and outside recruiters from Credit Suisse informed Insider in March that they anticipated many investment banking division employees, such as equity research analysts and traders, to lose their jobs. Founder of the London-based recruiting company Spartan International, Oliver Rolfe, stated at the time that the investment banking division at Credit Suisse was in serious trouble. “Credit Suisse and UBS overlap in so many ways. Such drastic cuts, which come after a series of culls on Wall Street, have a significant psychological impact. More than 3,000 jobs have been cut at Goldman Sachs, 3,000 at Morgan Stanley, and hundreds at JPMorgan Chase and Citigroup. The cutbacks come after a dry spell in deal-making and predictions of a wider US economic slowdown.

The fact that many of the Wall Street layoffs have been happening in waves since late last year is adding to the stress for financial professionals. According to Bloomberg, the reductions for UBS in July are just the first round; two more are anticipated in September and October. The intention is to reduce the combined workforce of UBS and Credit Suisse by about 30%, or 35,000 people, according to two of the people cited by Bloomberg. Before its problems compelled Swiss regulators to act, Credit Suisse had already been reducing its headcount. The Swiss bank’s customers withdrew $69 billion in the first three months. Despite the fact that Swiss authorities forced the two banks’ shotgun marriage in order to avoid a banking collapse, the outcome will still result in job losses there even though foreign financial centres will be hit harder. The bright side? Bloomberg reports that although many private bankers at Credit Suisse have already left, the majority will be encouraged to stay.

AUDNZD Analysis

AUDNZD has broken the Descending channel in upside.

According to China’s National Bureau of Statistics, corporate profits decreased by 12.6% in May compared to an 18.2% decline in April. As a major partner of China, New Zealand’s exports were negatively impacted by the slowdown in China.

The Kiwi asset is expected to continue to decline as China’s economic prospects worsen as a result of weak exports and weak demand. China’s National Bureau of Statistics (NBS) reported that due to weak household demand, corporate profits declined 18.2% in April and 12.6% in May. It is important to remember that New Zealand is one of China’s top trading partners, and the weak Chinese economic outlook would put pressure on the New Zealand Dollar.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/