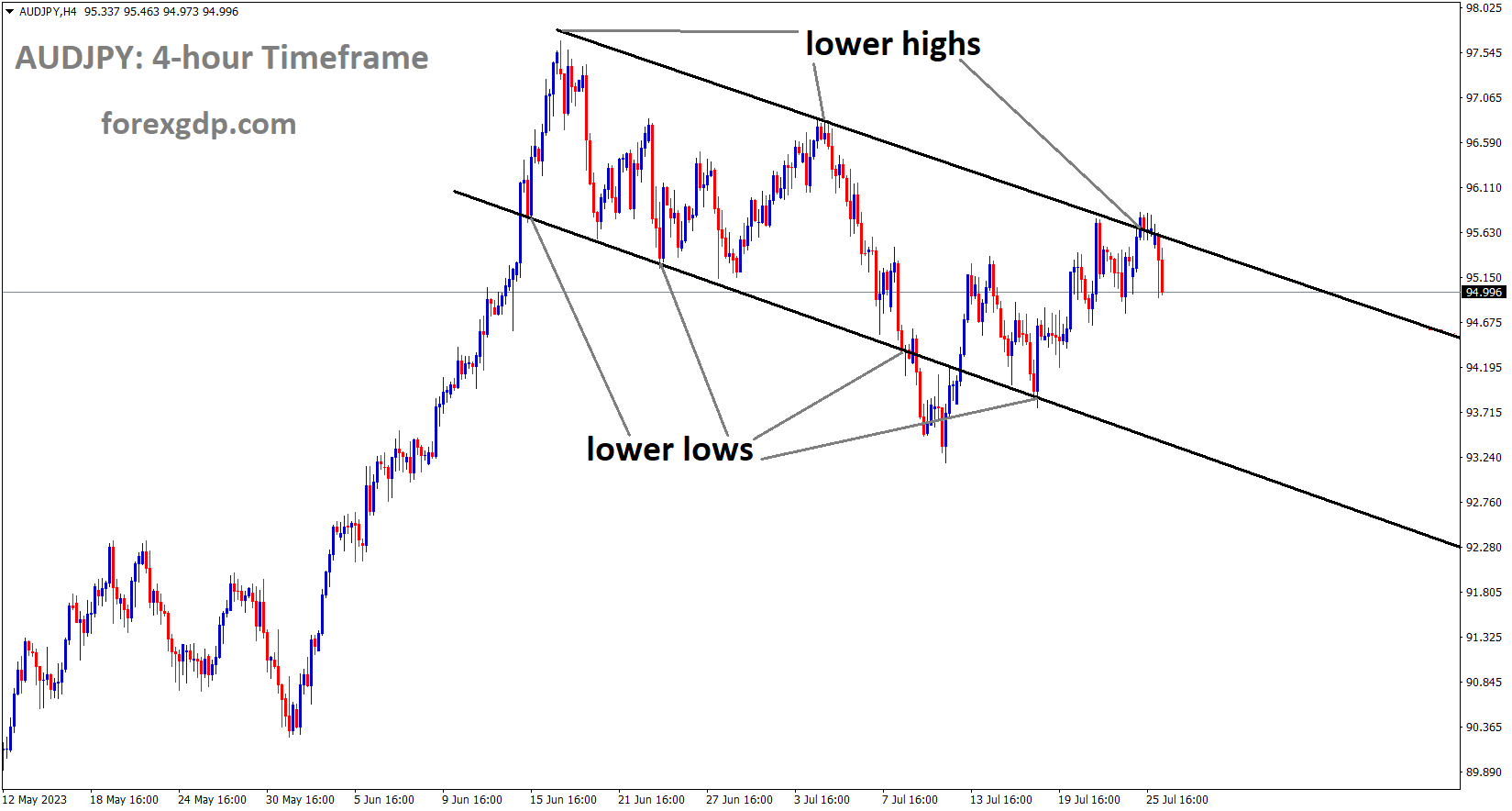

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel.

This week, the Bank of Japan is anticipated to maintain the policy at -0.10% and the YCC at 10 years levels of 0.50% or below 0%. Due to the Bank of Japan’s inaction and the rise in inflation on one side, the JPY is weak against counterpairs. The economy will not be as stable with lower interest rates and higher inflation.

On Friday, the BoJ will likely update its quarterly projections while maintaining its yield curve control ten years at 0.5% above or below 0% and policy rate -0.1%. The central bank’s quarterly inflation forecasts, which are anticipated to show a continued increase in consumer price inflation, are important to note. The central bank may need to adjust its current YCC levels if price pressures increase further or become persistent in order to prevent higher inflation from becoming entrenched.

The economic assessment reported by Japan’s cabinet office for July is more positive than those for the previous seven months. Capital spending, sales, and exports are increasing, and a moderate recovery is being observed. A rise in capital spending and a strong export report were both seen in July.

The Japanese Cabinet Office released its monthly economic assessment on Wednesday, just in time for the Bank of Japan’s (BoJ) policy announcements and revised economic projections on Friday. raises the impression of business sentiment for the first time in seven months in July. maintains a broad view of the economy. The government continued to believe that the economy was “recovering moderately” because exports, capital spending, and consumer spending all remained stable. Firms’ assessment of the state of the economy is becoming more accurate. The Cabinet Office continued to believe that capital spending was “picking up” and that exports were strong in July.

XAUUSD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Prior to today’s FED meeting, gold prices have stabilised; the anticipated 25 basis point rate hike causes gold prices against the USD to decline. Because of higher rates and China’s increased gold consumption as a result of the country’s economic recovery, gold prices are supported.

Due to a strong Dollar Index DXY, gold prices are still under pressure. As the FOMC meeting draws near, a number of factors may be contributing to the dollar’s strength. With a new range appearing to have been established between the $1950 and $1980 handles, gold prices currently seem to be in need of a catalyst. The Dollar Index DXY experienced some light selling pressure during the Asian session as the safe-haven US Dollar was pressured by expectations that China would implement a stimulus package. However, as the DXY surges higher ahead of the eagerly anticipated FOMC meeting, the European open has seen those losses reversed. Following last week’s selloff, repositioning and potential profit-taking may have contributed to the DXY’s strength.

XAGUSD Analysis

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel.

The FOMC meeting tomorrow might provide the impetus gold prices require to move forward. The majority of market participants are prepared for the Fed to raise interest rates by 25 basis points, which should not significantly affect the markets as it has already been priced in. As has been the case lately, the Fed Chair Powell’s press conference will likely be crucial for future market sentiment as well as any changes to the Fed’s outlook for the remainder of 2023. The good news regarding inflation does portend well for another Fed pause, which might cause the DXY to decline and support higher gold prices. In my humble opinion, for the DXY to maintain its current upward momentum, it would take extremely hawkish remarks from the Fed Chair, and my instinct is that the Dollar will weaken after the FOMC. With the release of Core PCE data, the Fed will end the week with yet another look at their preferred inflation gauge. The PCE data for 2023 have had an interesting ride, with 3 straight months of decline followed by an uptick in April. A decline in May will be followed by a decline this month, and the DXY will experience even more selling pressure if the print is below expectations.

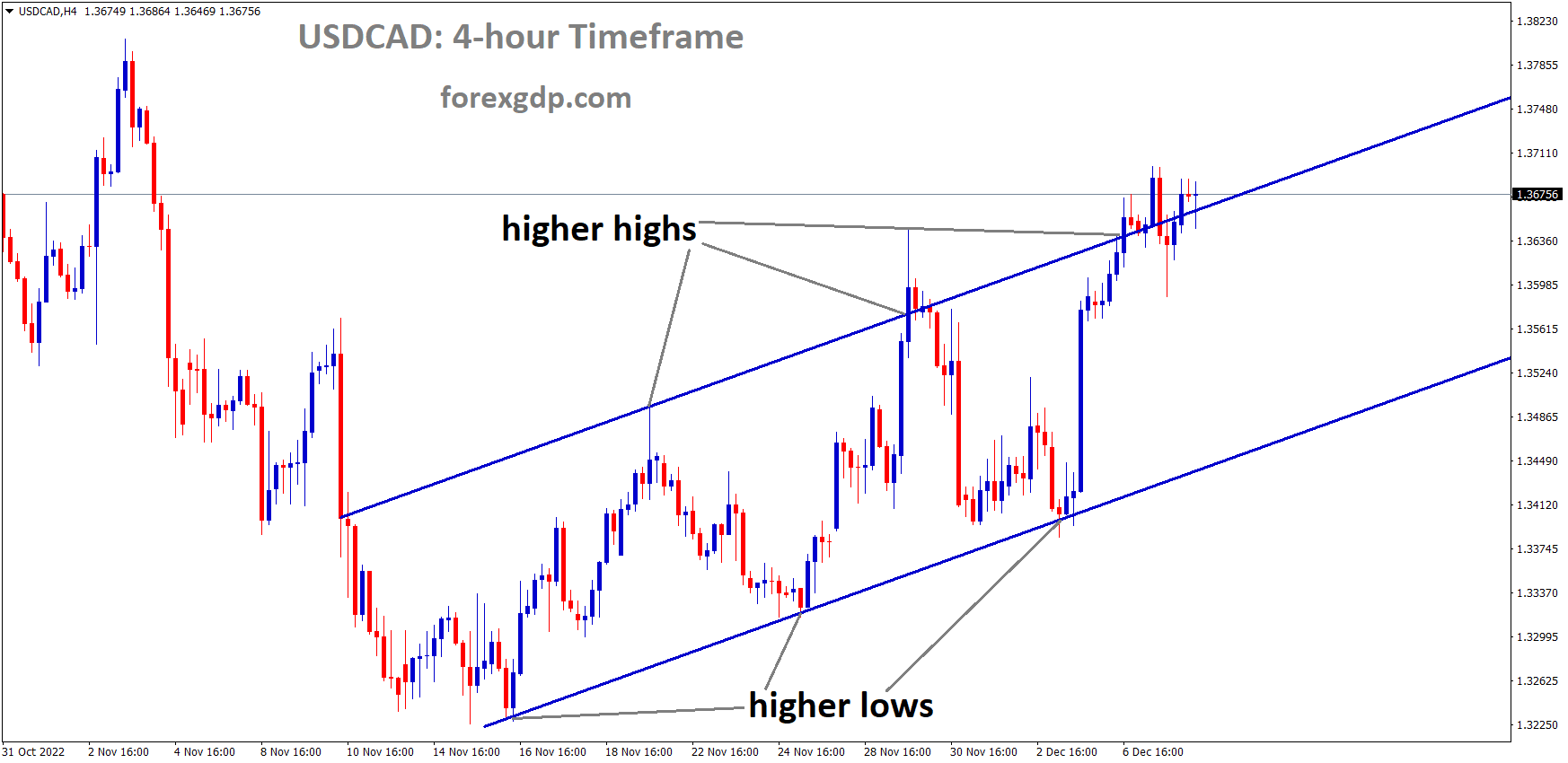

USD index Analysis

USD index is moving in an Ascending channel and the market has reached the higher low area of the channel.

In advance of today’s FOMC meeting, the US dollar is stronger against other currency pairs. There will be two more rate increases in 2023, one of which will take place at the July meeting and the other at the anticipated December meeting. Month-over-Month data show that US inflation is below the target of 3%, while demand is slowing and the labour market is still strong, prompting the FED to raise interest rates at this meeting.

Before the important US Federal Reserve interest rate decision later today, the US dollar has slightly recovered against its peers. A rate increase later on Wednesday seems inevitable given that inflation is still significantly higher than the Fed’s target, the process of disinflation is at best slow, and the labour market is still robust. The main concern would be whether and how much rate increases would occur following today’s meeting. The Fed’s statement and Powell’s remarks will be crucial in this regard.

A continuation of the June policy rate projections (two more rate hikes before the end of the year) could be justified by strong demand and loosening financial conditions, which would be a hawkish tack and boost the USD.The September meeting could be skipped if, on the other hand, the focus shifts to taming price pressures, particularly the significant decline in core inflation in June, and exercising more restraint while the disinflation process continues. The USD might suffer as a result of this. According to the CME FedWatch tool, rate futures are pricing in a slight possibility of one additional rate hike sometime in September or November.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

This week’s ECB monetary policy meeting is scheduled, and a rate increase of 25 basis points is anticipated to be announced in order to control the inflation reading. The manufacturing PMI and services PMI for the Eurozone were both published lower yesterday. In its upcoming meeting, the ECB is less likely to raise interest rates again.

The interest rate increase from the European Central Bank ECB, which will be announced on Thursday, the cross is predicted to continue its downward trend. ECB President Christine Lagarde is anticipated to announce a hawkish interest rate decision in an effort to curb the Eurozone’s persistent inflation, which is being driven by rising wages and service costs. It is anticipated that interest rates will rise by 25 basis points bps, bringing them to 4.25%. While the ambiguity surrounding the monetary policy guidance for September is the catalyst that is placing pressure on the euro. The economy in the eurozone is under stress as a result of higher interest rates, even though inflation has been steadily falling. The ECB may therefore decide to delay the policy tightening period in September, but this should not be combined with a pause at this time. However, ECB Lagarde’s advice would continue to be hawkish, giving the euro some support.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

However, the most recent Reuters poll revealed that only 20 economists predicted a half-point increase, while 42 out of 62 predicted a 25 bps increase to 5.25% in the Bank Rate during the upcoming BoE meeting on August 3. The Federal Reserve Fed is expected to make its monetary decision regarding the US dollar later in the North American session. It is widely believed that the Fed will increase interest rates by 25 basis points to 5.25–5.50%. Market participants will also be closely watching Fed Chairman Jerome Powell’s press conference because it could provide some information about the future course of monetary policy. A more dovish stance from the Fed may limit the Greenback’s upside potential and boost the GBPUSD pair. The value of the USD will probably continue to affect the movement of the pair in the absence of significant economic data released from the United Kingdom. Market participants will monitor the FOMC meeting and the press conference of Fed Chairman Jerome Powell. Aside from that, traders will use this week’s core Personal Consumption Expenditure PCE Price Index MoM and US Advance GDP QoQ as indicators. These statistics may have a significant effect on the US Dollar’s dynamics and provide the GBPUSD pair with a clear trend.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Worries for the GBP were raised when the Manufacturing PMI, Services PMI, and Composite PMI all came in worse than anticipated. According to economists, the Bank of England will likely increase interest rates again, with a 6.00% target. BoE has been raising interest rates for more than 30 years to reduce UK inflation.

Heading into the European trading hours, the GBPUSD pair oscillates within a constrained trading band between the 1.2875 and 1.2905 area. Due to traders’ preference to remain passive ahead of the Federal Open Market Committee FOMC meeting later in the day, the major pair struggles to gain. The price of GBPUSD is currently 1.2901, down 0.01% for the day. The information made public earlier this week demonstrated that the UK’s economic activity was weaker than anticipated. The Manufacturing PMI for July dropped to 45.0 from 46.5 in June, which was worse than the 46.1 expectation. The manufacturing sector experienced its 12th consecutive decline with this number. The preliminary Services PMI, meanwhile, dropped from 53.7 expected and 53.0 prior to 51.5. Markets quickly priced in a terminal rate of 6.50% after the Bank of England BoE unexpectedly increased its Bank Rate by 50 basis points bps to 5.00% in June. The BoE’s additional rate hike has pressured the pound sterling because it exacerbates worries about the Bank’s most aggressive rate increases in three decades and their effects on the UK economy.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Australian Q2 CPI data (June) were 0.80% higher than expected and 1.0% lower than the previous reading of 1.4%. Headline CPI data came in at 6.0% versus a forecast of 6.2% and a previous reading of 7.0%. After the data was flashed, the Australian dollar fell. After the CPI is brought down to the RBA’s target level, only a 40% chance of a rate increase in the August meeting is anticipated.

After the headline CPI of 6.0% missed expectations of 6.2% year-over-year to the end of June and against 7.0% previously, the Australian Dollar gave up overnight gains. Australia’s S&P ASX 200 equity index increased on expectations that the RBA’s tightening cycle might be coming to an end. In contrast to expectations of 1.0% and 1.4%, the headline CPI for the three months ending in June was only 0.8%. As opposed to earlier estimates of 6.0% and 6.6%, the RBA’s preferred measure of trimmed-mean CPI was 5.9% year-over-year to the end of June. The trimmed mean quarter-to-quarter CPI reading of 1.0% fell short of the forecasted 1.1% and Q1 reading of 1.2%.Prior to the release of today’s data, the interest rate futures markets assigned a 40% probability to the RBA raising interest rates by 25 basis points at their meeting on monetary policy next Tuesday. The post-CPI dial barely budged in the direction of less chance.

PPI and retail sales information will also be made public later this week. Another stellar jobs report was released last week, with the unemployment rate in Australia hovering around 50-year lows of 3.5%. In other news, the IMF increased its prediction for global GDP growth in 2023 from 2.8% to 3%. Due to the fact that many of Australia’s exports fluctuate in value based on global activity, the Australian economy and currency are closely tied to it. After China’s Politburo made a number of pro-growth statements earlier in the week, the IMF’s positive news added to the generally optimistic outlook for the region. The Australian Dollar gained during the first part of this week as the US Dollar declined ahead of the Federal Open Market Committee FOMC meeting later today. Most of those gains have been erased by the AUDUSD movement today. The main domestic focus for Australian Dollar financial products will be the RBA meeting on next Tuesday.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Data on US consumer confidence for July came in at 117, up from the predicted 112 and previous reading of 109.7. After the data projected a positive image, the NZD Dollar turned negative. NZD Dollar falls against USD due to RBNZ pausing rate hike this month and slower domestic demand.

Tuesday saw a rise in the NZDUSD despite the USD’s resilient performance against the majority of its trading partners. The US released strong data ahead of the Federal Reserve’s Fed decision on Wednesday, which might restrict the upside potential for the pair. On the side of the Kiwi, the NZD appears to be strengthening following China’s announcement of an economic assistance package for the Asian bloc. The US released impressive July housing and consumer confidence data. According to the Conference Board, people’s confidence in economic activity increased to 117, exceeding the predicted 112 and the prior reading of 109.7. While the Federal Housing Agency reported that its Housing Price Index increased by 0.7% in the same month, beating the consensus of 0.2%, the S&PCase-Shiller Home Price Index declined but was lower than expected in May, coming falling by 1.7% vs. -2.2% expected.

Markets anticipate a 25 basis point bps increase and a data-dependent approach from Chair Powell ahead of the Federal Reserve Fed’s two-day meeting because a strong economy and a tight labour market may lead the Federal Open Market Committee to consider another hike in September. While US Treasury yields traded in a range, with the 2-year rate slightly falling to 4.90%, the USD DXY Index kept rising, reaching 101.60 before falling back towards 101.40 while still holding gains.

CADCHF Analysis

CADCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

The rise in support for the Canadian dollar is caused by the recovery of oil prices on the global market. The unexpected rate increase by the Bank of Canada lowers manufacturing data, retail sales, and inflation due to higher rates.

European Private Bank By the end of September, according to Julias Baer, the assets and transactions of their Russian clients will be frozen. These customers are backing Russian President Vladamir Putin in the conflict in Ukraine. As a result, the freezing of the assets of Wealth elites’ Russian clients atones for illegal fund handling in Russia.

As wealth managers navigate an expanding web of sanctions and limitations related to Moscow’s invasion of Ukraine, Swiss private bank Julius Baer BAER.S informed its Russian clients in a letter obtained by Reuters on Tuesday that it would cease all business with them. The letter stated that wealth management activities, such as mandates managing clients’ investments, credit agreements, and credit card contracts, would be terminated by the end of September. Julius Baer will stop doing business with clients with addresses in Russia no later than December 31. The action comes as authorities have targeted Swiss banks, which serve as centres for offshore wealth, using sanctions, asset freezes, and criminal investigations to put pressure on Russia’s wealthy elite and weaken support for President Vladimir Putin.

Bloomberg reported in March that the two largest banks in Switzerland at the time, Credit Suisse CSGN.S and UBS UBSG.S, were being investigated by the U.S. Department of Justice (DOJ) to determine whether financial advisors assisted Russian oligarchs in dodging sanctions. Since Credit Suisse was later acquired by UBS, Julius Bär is now the second-largest of Switzerland’s publicly traded lenders. Switzerland moved in March 2022 to adopt the sanctions that the European Union (EU) imposed on Russian individuals and companies and to freeze their assets as retaliation for the invasion of Ukraine, departing from its traditional neutral position. Since then, it has expanded sanctions in line with EU initiatives. The agency in charge of sanctions reported in December that as of Nov. 25 2022, Switzerland had frozen about 7.5 billion Swiss francs ($8.63 billion) in related financial assets, as opposed to about 46.1 billion francs in current deposits held by Russian nationals and Russian-domiciled individuals. As European lenders worked to reduce their exposure to Russia’s elite, Julius Baer announced in March 2022 that it was ceasing all new business with wealthy Russians. According to a May article in Forbes Russia, Julius Baer informed clients in Russia and Belarus that their investment accounts would be frozen as a result of requirements from clearing house Euroclear.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/