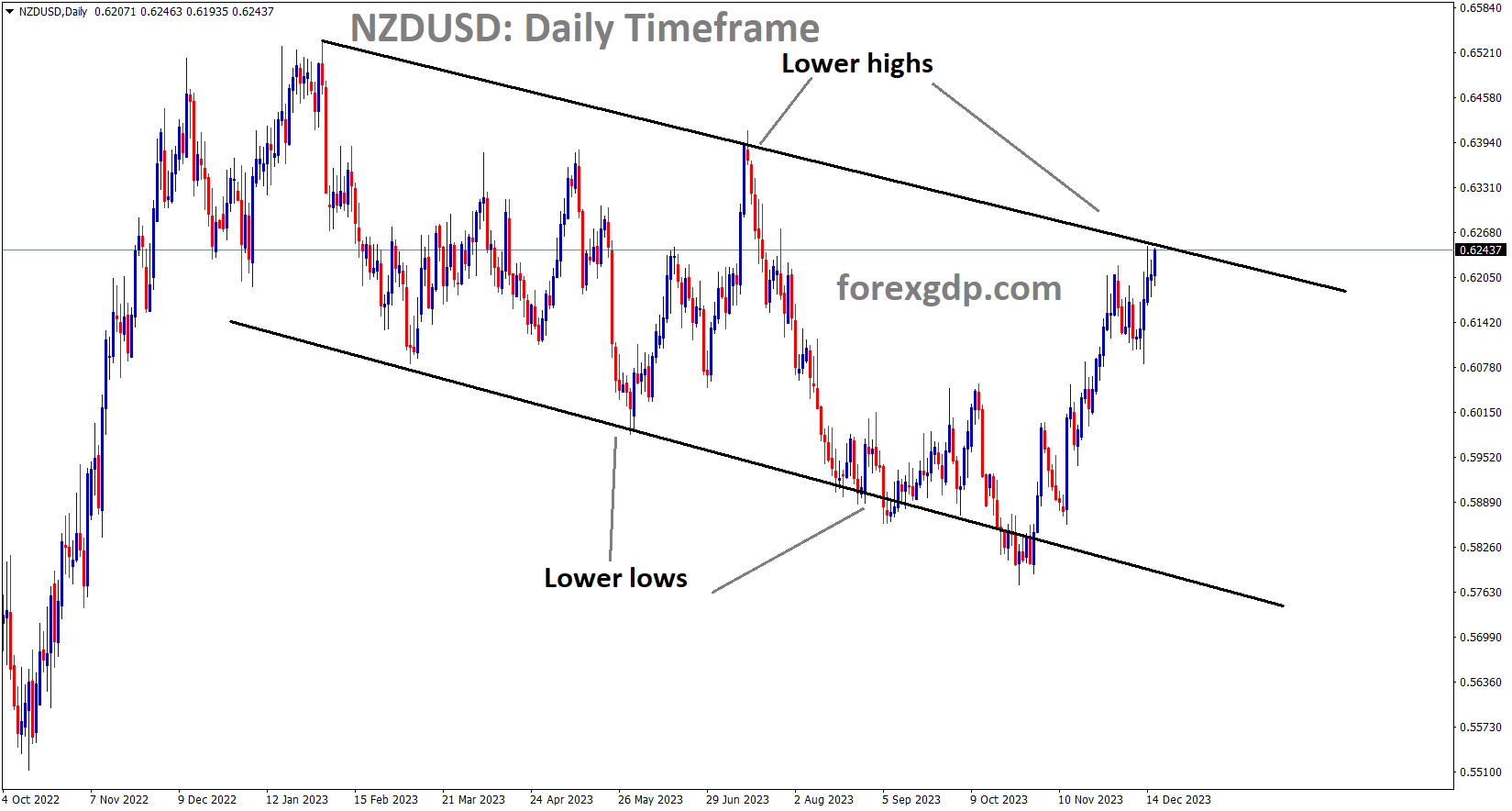

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The NZD Services index for the current month stands at 51.2, a notable increase from the November figure of 48.9. Additionally, the NZ Westpac consumer confidence reading for Q4 has surged to 88.9, marking its highest point in two years. As a result of these positive developments, the NZDUSD received a boost on Monday following the release of these readings.

Business NZ released the latest data, revealing that New Zealand’s Business NZ Performance of Services Index made a significant move into expansion territory, rising to 51.2 in November from the previous reading of 48.9. Additionally, the New Zealand Westpac-McDermott Miller Consumer Confidence Index for the fourth quarter of 2023 surged to 88.9, marking its highest level in two years. These positive developments have provided a boost to the New Zealand Dollar (NZD) and are serving as a favorable factor for the NZDUSD pair.

Conversely, Federal Reserve Bank of Chicago President Austan Goolsbee cautioned on Sunday that it is premature to declare victory in the battle against inflation, emphasizing that decisions regarding rate cuts will depend on economic data. Furthermore, Atlanta Fed President Raphael Bostic mentioned that the Fed could initiate interest rate cuts in the third quarter of 2024 if inflation behaves as anticipated. Looking ahead, New Zealand is scheduled to release Trade Data and the NZ Business Confidence survey on Tuesday. Additionally, the United States will release housing data, including Building Permits and Housing Starts on the same day. Traders will closely monitor these data releases to identify trading opportunities in the NZDUSD pair.

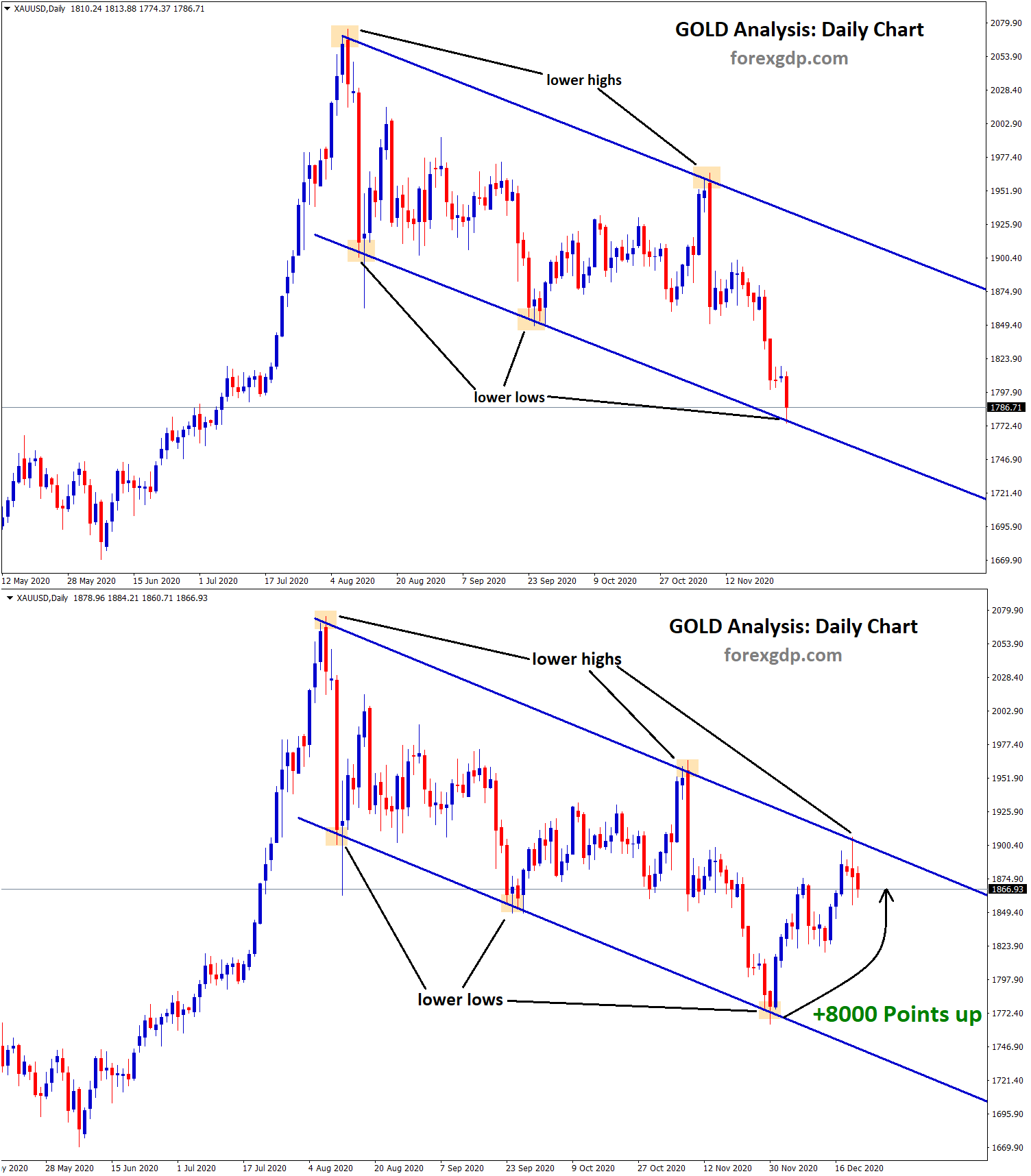

GOLD Analysis:

XAUUSD Gold price has broken the Box pattern in downside.

Gold prices are holding steady in anticipation of this week’s release of US inflation and US GDP data. There is an expectation in the market of potential 75 basis points rate cuts by the Federal Reserve in 2024.

The price of gold showed positive momentum at the beginning of the new week, maintaining its modest intraday gains during the European session. However, it struggled to sustain significant upward movement. The Federal Reserve’s recent announcement signaling the end of its tightening cycle and the projection of 75 basis points in rate cuts for 2024 acted as a cap on the US Dollar’s rebound from a four-month low reached on Friday. This development provided support for the precious metal, which is considered a safe-haven asset. Additionally, concerns about geopolitical risks and fears of a deeper economic downturn, particularly in China and the Eurozone, added further backing to gold’s appeal. Despite these factors, a couple of Federal Reserve officials attempted to push back against market expectations for early interest rate cuts. Furthermore, the recent strong rally in global equity markets, fueled by the Fed’s more dovish stance and expectations of additional stimulus from China, limited any substantial upward movement in the price of gold. Traders also remained cautious, awaiting the release of the US Core PCE Price Index, the Federal Reserve’s preferred gauge of inflation, on Friday.

This critical US inflation data will shape market expectations regarding the timing of the Fed’s policy adjustments and influence the next direction for gold, which doesn’t provide yield. In the absence of significant economic data from the US on Monday, broader market sentiment and USD dynamics will likely continue to impact demand for XAUUSD. New York Federal Reserve President John Williams, in a recent CNBC interview, emphasized that rate cuts are not currently under discussion, and it’s too early to speculate about them. He mentioned that economic data can surprise, and the central bank should be prepared to tighten policy further if inflation progress falters. Atlanta Fed President Raphael Bostic echoed a similar sentiment, suggesting that rate cuts are not imminent and might occur sometime in the third quarter of 2024. However, markets appear convinced that the Fed will ease its policy by the first half of 2024, which limits the US Dollar’s rebound from its four-month low and supports the price of gold.

On the economic front, the flash PMI data released on Friday indicated a deterioration in business activity in Germany in December, raising concerns about a possible recession in the Eurozone’s largest economy. Additionally, North Korea conducted missile tests, and China expressed optimism about its economic outlook for 2024. China’s favorable conditions, low prices, manageable government debt levels, and policies to strengthen monetary and fiscal measures, in conjunction with the Fed’s dovish stance, bolstered positive sentiment in global equity markets, thus restraining further gains in the safe-haven gold market.

SILVER Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The US Dollar saw an upward trajectory following the release of favorable US Services PMI data. The Services data rose to 51.3 in December, up from 50.8 in the previous month of November. Additionally, the Composite PMI increased to 51.0 from 50.7 in the preceding month. US policymakers have stated that rate cuts would only be considered if inflation remains within our target range in the coming months.

During the early European session on Monday, the US Dollar Index, which measures the value of the US Dollar against a weighted basket of currencies representing US trade partners, experienced a loss of momentum. The DXY rebounded from its multi-month lows at 101.77 and is currently trading near 102.45, showing a 0.15% decline for the day. While the stronger US Services PMI released on Friday provided some support for the Greenback, its upside remains constrained by expectations of three rate cuts from the Federal Reserve (Fed) in the upcoming year. On Friday, data indicated that the flash reading of the US S&P Global Services PMI for December climbed to 51.3 from November’s 50.8, surpassing market expectations of 50.8. However, the Manufacturing PMI dropped to 48.2 in December, down from 49.4 in November and below market expectations of 49.3. The Composite PMI for December increased to 51.0, up from the previous reading of 50.7.

The Fed’s dovish stance prompted a rally in US equities and placed downward pressure on the US Dollar. Currently, money markets are reflecting a nearly 75.0% probability of at least a 25-basis point rate cut in March 2024, up from around 64.5% before the latest policy decision, according to CME Group’s FedWatch tool. Federal Reserve Bank of Chicago President Austan Goolsbee stated on Sunday that it is too early to declare victory in the battle against inflation, emphasizing that decisions regarding rate cuts will depend on upcoming economic data. Atlanta Fed President Raphael Bostic also noted that the central bank can commence interest rate cuts in the third quarter of 2024 if inflation behaves as anticipated.

The prospect of potential Fed rate cuts in the coming year is also weighing on US Treasury bond yields, with the US 10-year Treasury note yields reaching multi-month lows and currently standing near 3.90%. This development follows the Fed’s indication that it plans to implement three interest rate cuts in 2024 after its recent meeting. Traders will closely monitor the release of US Building Permits and Housing Starts on Tuesday. Later in the week, attention will turn to US Consumer Confidence and Existing Home Sales data scheduled for Wednesday. Additionally, the US Gross Domestic Product Annualized for Q3, which is expected to remain steady at 5.2%, will be released on Wednesday.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The Swiss National Bank currently has no intention of selling foreign reserves to maintain the strength of the Swiss Franc. Instead, they plan to sell reserves before implementing any rate cuts. The Swiss Franc experienced a depreciation against other currencies after the SNB reduced its emphasis on foreign exchange sales.

The Swiss National Bank finds itself in a challenging position, opting to maintain interest rates unchanged for the second consecutive rate decision. This decision comes as inflation gradually approaches the SNB’s targets, while the projection for Swiss Gross Domestic Product (GDP) growth points to a slowdown. SNB Chairman Thomas Jordan remarked on Thursday that the SNB has shifted its focus away from direct forex operations aimed at preventing further appreciation of the Swiss Franc. Despite market expectations increasing for potential rate cuts as early as March, Chairman Jordan emphasized that, in terms of monetary policy, the SNB is more inclined to resume selling currency reserves directly before considering rate reductions.

On the economic front, US data on Friday showed a mixed picture. The S&P Global Manufacturing Purchasing Managers’ Index for December fell short of expectations, registering at 48.2 compared to November’s 49.4, missing the median market forecast, which had anticipated a slight decline to 49.3. Conversely, the US Services PMI exceeded expectations, posting a robust figure of 51.3, surpassing the market’s projection of a drop to 50.6 from the previous month’s 50.8.

Looking ahead to the coming week, the SNB is set to release its Quarterly Bulletin for the fourth quarter of 2023 on Wednesday, followed by US GDP figures on Thursday. The Federal Reserve’s policy shift and the updated dot plot of interest rate expectations will face their first test with the release of US Personal Consumption Expenditure data for November next Friday. The annualized US GDP for the third quarter is expected to remain stable at 5.2%, while median market forecasts suggest a slight decline in PCE for the year up to November, from 3.5% to 3.4%.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The Eurozone appears to be heading towards a technical recession, as indicated by the December data, which shows lower readings in Services, Composite, and Manufacturing PMI. If inflation continues to decline in the upcoming months, the ECB may initiate rate cuts earlier than anticipated, given the consistent decrease in Eurozone GDP and domestic data over recent months.

According to ECB Policymaker Robert Holzmann, interest rates have currently reached their highest point, and any potential further rate cuts will be determined solely based on inflation remaining at lower levels for an extended period.

The Euro Area’s economic challenges persist, with an impending entry into a technical recession expected in the coming weeks. Data from HCOB, a prominent data provider, reveals that business activity in the Euro Area declined even more sharply in December. This marks the conclusion of a fourth quarter characterized by the most rapid output decline in 11 years, with exceptions only for the early months of the 2020 pandemic. Dr. Cyrus de la Rubia, Chief Economist at HCOB, commented on the data, expressing dismay at the Eurozone’s inability to exhibit any clear signs of recovery. Instead, it has contracted for six consecutive months, heightening the likelihood of the Eurozone remaining in a recession since the third quarter.

During Thursday’s ECB meeting, the central bank pushed back against the market’s aggressive pricing of approximately 150 basis points in rate cuts for 2024. President Lagarde emphasized the intention to maintain interest rates at sufficiently restrictive levels for as long as necessary to bring inflation back to the target rate of 2%. She also noted that the governing council had not discussed a specific timetable for rate cuts. However, if the Euro Area does indeed slip into a recession, as currently appears likely, and inflation continues to decline, the ECB may need to reconsider its stance on interest rates and prepare the market for a series of cuts in the upcoming year. Financial markets are already factoring in nearly five 25 basis point rate cuts in 2024.

The persistent weakness of the US dollar gained momentum late on Wednesday following the Federal Reserve’s decision to keep rates steady for the third consecutive month. Fed Chair Jerome Powell sent a strong signal that interest rates would be reduced in 2024, with the possibility of a 75 basis point cut next year. However, the market viewed this as a conservative estimate. After the conclusion of the FOMC press conference, market expectations for US rate cuts in 2024 surged to 150 basis points, with the first 25 basis point cut anticipated in March. These heightened expectations, coupled with the sell-off in US bond yields, further contributed to the decline of the US dollar.

During a news conference on Friday, European Central Bank policymaker Robert Holzmann expressed the view that it is increasingly probable that interest rates reached their highest point last month, according to Reuters. Holzmann further clarified that there have been no deliberations regarding interest rate reductions among policymakers. Additionally, he mentioned that a majority of policymakers perceive upside risks to inflation.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

This week, we are expecting the release of Q3 GDP data for GBP and November’s inflation figures. The Bank of England will base its decision on potential further rate cuts on the data presented in its 2024 meetings.

In a week marked by significant central bank policy decisions, the Federal Reserve adopted a more cautious stance, contrasting with the Bank of England and the European Central Bank, which remained committed to a prolonged period of elevated interest rates. This divergence introduced increased volatility to the USD, Euro, and British Pound, as discussed in the articles above. The pivotal event of the week was the Fed’s decision and accompanying statement on Wednesday, which resulted in a sharp decline in the US dollar and US Treasury yields.

The British Pound experienced a subsequent rise but is currently in a holding pattern, awaiting the release of crucial inflation and GDP data, representing the final high-importance UK releases before the seasonal break.

While the UK’s economic growth remains sluggish at best, the Bank of England will closely monitor the latest inflation figures. Last month witnessed a notable drop in inflation, and the UK central bank is anticipating further progress in their efforts to combat persistently high price pressures when the ONS data is unveiled on Wednesday. Should inflation fall below expectations, it will increase pressure on the Bank of England to consider implementing rate cuts sooner, potentially exerting downward pressure on the British Pound in the weeks ahead.

GBPJPY Analysis:

GBPJPY is moving in the Box pattern and the market has reached the support area of the pattern

In anticipation of the Bank of Japan’s monetary policy announcement tomorrow, JPY pairs have shown limited movement. Economists are anticipating that this meeting will likely provide further hints about potential rate hikes.

The China’s Central Finance Office expressing an optimistic outlook, is boosting investor confidence. Consequently, this is regarded as a significant factor undermining the safe-haven appeal of the JPY

The risk-on sentiment in the market is undermining the safe-haven status of the Japanese Yen, alongside a moderate recovery in the US Dollar from its recent four-month low. State media Xinhua, citing a government statement, reported that China’s economy is expected to encounter more favorable conditions and opportunities than challenges in 2024

On a different note, North Korea conducted a missile launch, including at least one unidentified type of ballistic missile on Monday, following a separate short-range missile launch late Sunday night. The flash PMI data released on Friday indicated a deterioration in German business activity in December, heightening the risk of a recession in Europe’s largest economy. Meanwhile, the S&P Global Composite PMI showed a slight increase to 51.0 from 50.7, suggesting that business activity in the US private sector continues to expand at a modest pace in early December. And market participants increasingly anticipate the possibility of the Bank of Japan exiting its negative interest rate policy early next year.

GBPCAD Analysis:

GBPCAD is moving in the Descending channel and the market has reached the lower low area of the channel

Bank of Canada Governor Tiff Macklem’s speech on Friday indicates that rate cuts are not imminent; these remarks have encouraged the Canadian Dollar to strengthen against its counterparts. Although inflation and GDP data have declined as anticipated, the possibility of rate cuts in early 2024 is not currently under consideration.

Bank of Canada Governor Tiff Macklem, speaking at the Canadian Club of Toronto, emphasized that it is still premature to consider or discuss rate cuts. Macklem’s remarks at this event represent the most notable item on the Canadian Dollar’s economic calendar for the week. New York Fed President John Williams also tempered the enthusiasm in the markets on Friday, stating that market expectations of rate cuts as early as March are premature. He revealed that rate cut discussions have not even been on the Fed’s agenda yet.

The Canadian Dollar was among the top performers on Friday, gaining ground against all major currency counterparts. It rose by over one percent against the Euro, a full percent against the British Pound, and a quarter of a percent against the US Dollar. BoC Governor Macklem: Premature to consider rate cuts.

Crude oil markets faced some pressure following Fed President Williams appearance on CNBC, causing WTI crude to dip towards $70.50 before stabilizing below $72 per barrel. This limited support for the Canadian Dollar on Friday. Overall, the Canadian Dollar ended the week on a positive note against the US Dollar, with a gain of 1.6% from Monday’s opening levels.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Positive data for China’s factory output and retail sales in November has led to a rise in the Australian Dollar against other currencies. Despite stimulus measures being injected into the property sector, their impact has yet to materialize; however, once the property sector picks up, it can significantly boost the Chinese economy. This week, we are anticipating the release of the RBA Meeting minutes.

The prospect of rate cuts by Federal Reserve officials is putting downward pressure on the US Dollar across the board, offering some support to the AUDUSD currency pair. Atlanta Fed President Raphael Bostic’s recent remarks on Friday indicated that the central bank could potentially initiate interest rate cuts in the third quarter of 2024 if inflation follows the anticipated path. Additionally, Chicago Fed President Austan Goolsbee mentioned that he did not rule out the possibility of a rate cut at the Fed’s meeting in March.On the economic front, US business activity expanded at the quickest pace since July, as indicated by the data from the US S&P Global Purchasing Managers’ Index released on Friday. The preliminary Composite PMI for December rose to 51.0 from November’s 50.7. However, the Manufacturing PMI declined from 49.4 to 48.2, while the Services PMI increased from 50.8 to 51.3.

AUDCHF Analysis:

AUDCHF is moving in the Box pattern and the market has reached the resistance area of the pattern

Meanwhile, the Chinese economy displayed signs of modest growth in November, with factory output and retail sales registering increases, according to the National Bureau of Statistics of China’s report on Friday. However, the property market remained sluggish, despite the government’s promise of additional policy support. Market expectations include the implementation of further stimulus measures to stimulate demand in the property sector, as well as potential lending rate cuts in the first half of 2024. Positive developments related to the Chinese economy could have a positive impact on the Australian Dollar, given that China is Australia’s largest trading partner.

In the upcoming days, investors will be closely monitoring the release of the Reserve Bank of Australia’s meeting minutes on Tuesday, as well as US housing data, including Building Permits and Housing Starts. The highlight of the week will be the Core Personal Consumption Expenditure Price Index report, scheduled for release on Friday.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/