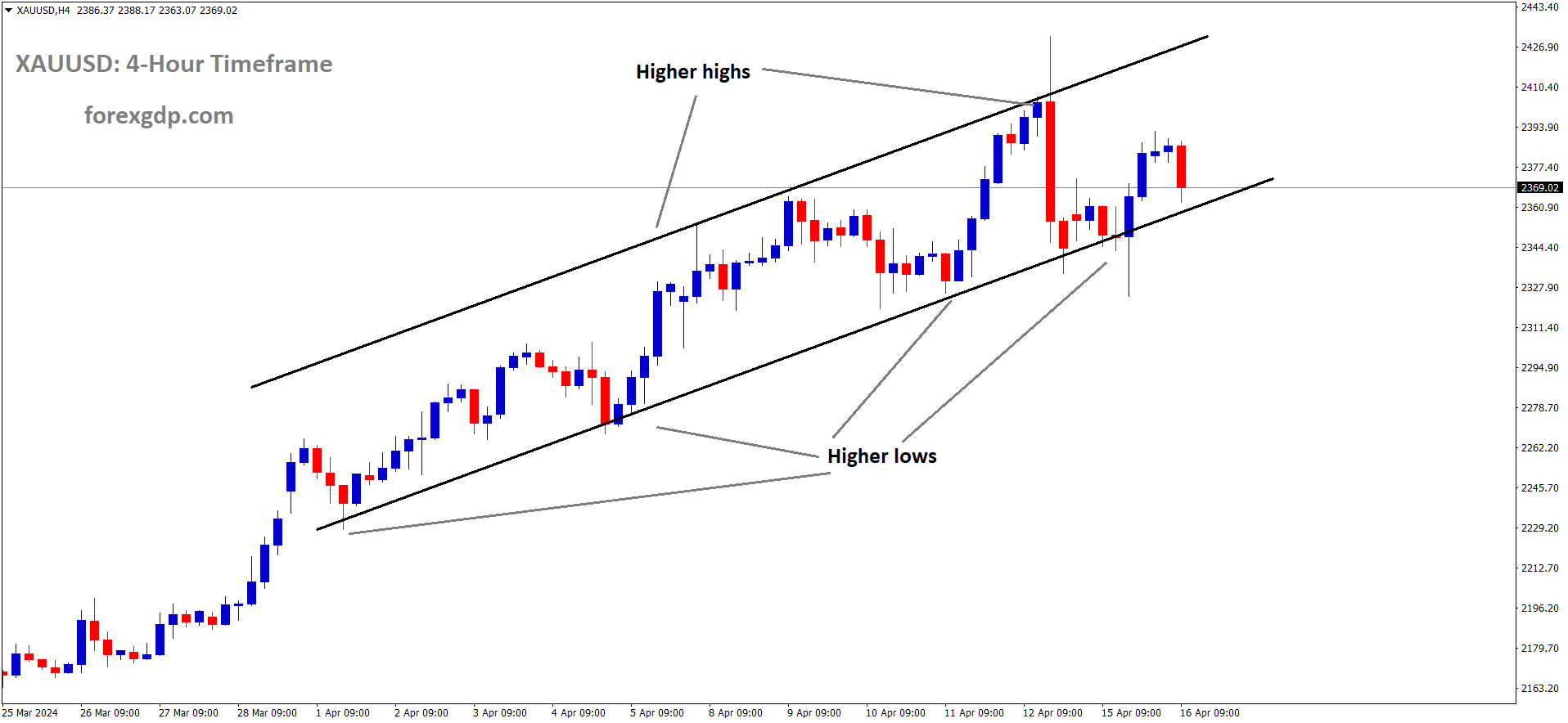

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD – GOLD Price Trades Lower Amid Strong USD, Limited Downside Likely

The Gold prices are moving higher after the Middle east tensions slowdown. Iran side further escalations is not come as per Iran Foreign minister said. Now Israel and Gaza remains conflicts going on, US Retail sales rose to 0.70% in March month versus 0.90% printed in the last month.

Gold prices struggle to maintain their upward momentum on Tuesday as they face selling pressure. The strengthening US Dollar, fueled by reduced expectations of a Federal Reserve rate cut, weighs on the precious metal. Despite this, the escalating crisis in the Middle East is expected to support gold prices and prevent significant losses.

During the early European session, the price of gold (XAU/USD) retreats slightly from its recent highs near the $2,325-2,324 range, marking a temporary reversal from a multi-day low. The ongoing anticipation that the Federal Reserve will maintain higher interest rates for a longer period due to persistent inflation and a resilient US economy contributes to the sustained buying of the US Dollar. Consequently, this exerts downward pressure on gold, which is denominated in USD, although a substantial corrective decline remains elusive.

Investor sentiment remains cautious amidst geopolitical tensions in the Middle East, evident from the overall weakness in equity markets. Additionally, the belief that major central banks may delay interest rate cuts later in the year could help mitigate downward pressure on gold, given its status as a safe-haven asset. Market participants are now closely monitoring US macroeconomic data and speeches by influential Federal Open Market Committee (FOMC) members, including Fed Chair Jerome Powell, for fresh cues on the future direction of XAU/USD.

In the broader market context, ongoing concerns about the Middle East crisis and speculations surrounding the Fed’s monetary policy stance are supporting gold prices. Investors have adjusted their expectations for the timing of the first Fed rate cut, pushing it back to September from June, due to concerns about inflation and the robustness of the US economy. This sentiment was reinforced by stronger-than-expected US Retail Sales data released on Monday, indicating robust consumer spending that could fuel inflation in the coming months.

Furthermore, the yield on the benchmark 10-year US government bond has surged to its highest level since November, although gains were capped by the disappointing release of the Empire State Manufacturing Index. The continued upward trajectory of the US Dollar, reaching over a five-month high, may discourage bulls from entering new positions and restrain further upside potential for gold.

Tuesday’s US economic calendar includes the release of housing market data and Industrial Production figures, alongside speeches by Federal Reserve officials, which could provide additional direction for gold prices in the absence of significant geopolitical developments.

USDJPY – JPY continues downward trend against USD, hits new multi-decade low

The JPY moving 34 year low against USD due to More policy divergence from BoJ and FED.

BoJ Do small rate hike in the March month but BoJ Governor Ueda said we stay with more bond purchasing programs and stay with accommodative stance. Whenever inflation adjusted wage hike seen in the market we do proper rate hikes thereafter. So Dovish message from BoJ side makes weakness persists in the market.

USDJPY has broken the Ascending triangle pattern in upside

The Japanese Yen (JPY) continued its downward trajectory against the US Dollar (USD) on Tuesday, reaching a fresh 34-year low in the early European session. This depreciation comes amidst the Bank of Japan’s (BoJ) dovish stance, as the central bank refrained from providing clear guidance on future policy steps or the pace of policy normalization after ending negative interest rates in March. A report on Monday indicated that the BoJ might adopt a more discretionary approach, shifting away from a focus on inflation to let various data guide its future rate hike path. This lack of clarity from the BoJ, combined with ongoing USD strength, pushed the USD/JPY pair above the mid-154.00s.

Furthermore, incoming US macroeconomic data suggesting persistent inflation and a resilient economy have led investors to delay expectations for the first interest rate cut by the Federal Reserve (Fed) to September, instead of June. This delay indicates that the interest rate differential between the US and Japan will persist, potentially driving flows away from the JPY and supporting further appreciation of the USD/JPY pair. However, JPY bears remain cautious due to recent warnings from Japanese authorities about potential market intervention to bolster the domestic currency. Additionally, the worsening Middle East crisis has limited losses for the safe-haven JPY, providing some support to the currency pair.

In the daily market movements, the Japanese Yen continues to be weighed down by the BoJ’s dovish stance, while bullish US economic indicators keep the USD/JPY pair near a 34-year high. Strong US retail sales data, coupled with less aggressive interest rate cut expectations by the Fed, have boosted the US Dollar and acted as a tailwind for the USD/JPY pair. Japanese officials have reiterated their vigilance on FX movements and readiness to take measures to stabilize the currency, though this has done little to alleviate pressure on the JPY. Geopolitical risks and expectations of prolonged US rate hikes continue to weigh on investor sentiment, supporting the safe-haven appeal of the JPY and limiting gains for the USD/JPY pair. Traders are now awaiting further impetus from US macroeconomic data and speeches by key Fed officials later in the day.

USDCAD – nears 1.3800, highest since November ahead of Canadian CPI

The Canadian Dollar moved lower against USD after the US Domestic retail sales data came at higher than expected last day. Further escalations from Israel Military chief on Iran makes worry for Oil supply and Oil prices rebounded from the lows. Canadian CPI is scheduled on this week.

USDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

The USD Index (DXY), which measures the USD against a basket of major currencies, reaches a five-month high, driven by expectations that the Federal Reserve (Fed) will postpone interest rate cuts due to persistent inflation. Additionally, robust US Retail Sales data released on Monday indicates strong consumer spending, supporting inflation and suggesting a longer period of higher interest rates. This optimistic outlook supports higher US Treasury bond yields, bolstering the USD further.

Furthermore, a general risk-off sentiment prevails in equity markets amid geopolitical tensions, particularly in the Middle East. Israel’s military chief’s statement regarding a potential response to Iran’s recent missile and drone attack adds to the uncertainty, potentially favoring safe-haven assets like the USD. The possibility of further escalation in Middle East conflicts supports crude oil prices, which could indirectly boost the Canadian Dollar (CAD) due to its correlation with oil prices.

Investors eagerly await the release of Canadian consumer inflation data later in the North American session, which could influence the CAD’s performance. Additionally, US housing market data and Industrial Production figures, as well as speeches by key Federal Reserve officials including Fed Chair Jerome Powell, will impact USD dynamics. Oil price movements will also be closely monitored, shaping short-term trading opportunities for the USD/CAD pair.

USDCHF – remains above 0.9100, approaching highs since October

The Swiss Import and export prices data shows 0.10% increase in the March month. YoY data shows contraction of 2.0% in the March month from 2.1% printed in the previous month. Swiss Franc remained weaker against USD after the data printed.

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

The pair is being supported by the strength of the US Dollar (USD), driven by upbeat Retail Sales figures from the United States (US). These data have raised expectations that the Federal Reserve (Fed) may maintain higher interest rates for a longer duration.

Furthermore, the US Dollar Index (DXY) is extending its gains, reaching around 106.30, while yields on US Treasury bonds, particularly the 2-year and 10-year bonds, stand at 4.93% and 4.62%, respectively, at the current time. Heightened geopolitical tensions in the Middle East have prompted investors to seek refuge in the safe-haven US Dollar (USD).

In remarks made on Monday, Federal Reserve (Fed) Bank of San Francisco President Mary Daly acknowledged progress on inflation but stressed the need for further assurance before any policy action is taken.

On the Swiss side, March saw steady growth in Swiss Producer and Import Prices (MoM), rising by 0.1%. However, on a year-on-year basis, Producer and Import Prices (YoY) experienced a more significant decline, contracting at a rate of 2.1%, compared to the previous contraction of 2.0%.

The Swiss Franc (CHF) had already undergone significant depreciation following the surprise rate cut by the Swiss National Bank (SNB) in March. With inflation showing signs of moderation in March and business sentiment remaining pessimistic, there is speculation in the market that the SNB might opt for another rate cut at its upcoming June meeting.

USD INDEX – Yellen: US to Employ Sanctions, Ally Cooperation Against Iran’s Destabilizing Activity

The US Treasury Secretary Janet Yellen warned Iran we will use more sanctions on Iran, if Iran doing Destabilising activity in Israel. Already 500 Individuals and firms linked to Iran has been doubtful from our side. Iran actions on Israel will disrupt whole world and must be avoided.

USD INDEX is moving in an Ascending channel and the market has reached the higher high area of the channel

During a statement on Tuesday, US Treasury Secretary Janet Yellen issued a warning, emphasizing the United States’ commitment to employing sanctions and collaborating with its allies to counteract Iran’s “malign and destabilizing activity.” Yellen underscored the necessity of taking decisive action to disrupt Iran’s actions, which pose a threat to regional stability in the Middle East and have the potential to trigger economic repercussions.

EURGBP – Vulnerable Near 0.8530 Despite UK Employment Weakness

The Euro currency moving weaker against USD after the ECB makes no policy changes in the last week meeting. ECB Governing council members expected rate cuts from ECB is June month.Inflation for the March month is 2.9%, Declining of straight eight months in CPI reading gives confidence to 2% target will be come in near term.

EURGBP is moving in the Box pattern and the market has reached the support area of the pattern

The currency cross faces downward pressure as the Euro weakens, driven by expectations that the European Central Bank (ECB) may follow suit with other central banks in developed nations and pivot towards rate cuts.

ECB policymakers are aligning with market expectations that the central bank could begin reducing borrowing rates as early as the June meeting. This sentiment stems partly from the annual core Consumer Price Index (CPI) figures, which, excluding volatile food and energy prices, decreased significantly to 2.9% in March. The consistent decline in Eurozone core CPI over the past eight months suggests a sustained move towards the ECB’s 2% inflation target.

During the previous week, the ECB opted to maintain its Main Refinancing Operations Rate at 4.5%, meeting market expectations. ECB President Christine Lagarde indicated in a monetary policy conference that if policymakers become more confident that inflation is on track to meet the target, it would be appropriate to consider interest rate cuts.

In contrast, the Pound Sterling has exhibited resilience against the Euro but weakness against the US Dollar. This divergence is driven by strong speculation that the ECB may implement rate cuts sooner, while the UK faces economic challenges reflected in weak labor market data.

The United Kingdom Office for National Statistics (ONS) reported a sharp increase in the Unemployment Rate to 4.2%, surpassing expectations of 4.0%, with employers laying off 156K workers in February, up from 89K in January.

Looking ahead, investor attention will turn to the UK Consumer Price Index (CPI) data for March, scheduled for release on Wednesday. This inflation data will play a crucial role in shaping market expectations regarding potential rate cuts by the Bank of England (BoE), currently anticipated to begin from the August meeting.

GBPUSD – Pound Sterling Hits Five-Month Low on Weak UK Employment Data

The UK Pound moved down after the UK Unemployment rate rise to 4.2% in February month from 3.9% in Previous month and 4.0% expected. Employers laid off 156K workers in February month when compared to 86K printed in January month.

GBPUSD is moving in the Descending channel and the market has reached the lower low area of the channel

Labor market cooling down makes UK CPI is expected to cool down in the coming months and BoE may be do soon rate cuts in this year.

The Pound Sterling (GBP) faced a downturn during Tuesday’s London session following the release of concerning labor market data by the United Kingdom’s Office for National Statistics (ONS). The report revealed a notable cooling in labor market conditions for the three months ending February, with the Unemployment Rate surging to 4.2% and a total of 156,000 workers being laid off.

This downturn in labor market conditions has stirred uncertainty regarding the economic outlook, potentially prompting Bank of England (BoE) policymakers to consider earlier-than-expected interest rate reductions. When labor market conditions deteriorate, job seekers and current employees often accept lower wage increases, resulting in sluggish wage growth that could hinder the sustainable achievement of the desired inflation target.

Further volatility is expected in the Pound Sterling as the UK ONS prepares to release consumer and producer inflation data for March on Wednesday. Forecasts suggest that the headline Consumer Price Index (CPI) may increase by 3.1%, a slight decrease from the previous reading of 3.4%. Additionally, the core CPI, excluding volatile food and energy prices, is projected to rise by 4.1%, down from 4.5% in February. A potential decline in inflation data could fuel speculation about the BoE’s initiation of interest rate reductions starting from the August meeting.

In light of these developments, the Pound Sterling extended its decline to 1.2410. The weak labor market data revealed an unexpected rise in the ILO Unemployment Rate to 4.2%, surpassing expectations of 4.0%. Additionally, employers shed 156,000 jobs in February, a significant increase from the previous reading of 89,000.

Meanwhile, the Claimant Count Change for March, indicating the change in the number of individuals claiming jobless benefits, was lower than anticipated at 10.9K, compared to expectations of 17.2K. However, the Average Earnings including bonuses for the three months ending February rose by 5.6%, slightly surpassing the consensus of 5.5%. Conversely, Average Earnings excluding bonuses slowed to 6.0%, down from the previous reading of 6.1%.

The weak labor demand underscores the repercussions of the BoE’s decision to maintain higher interest rates. With rising jobless rates and subdued labor demand, the economic outlook appears vulnerable, potentially prompting the BoE to consider earlier rate cuts than previously anticipated.

Market sentiment remains cautious amidst concerns of escalating tensions in the Middle East and uncertainty surrounding the Federal Reserve’s timeline for interest rate adjustments. Strong demand for safe-haven assets has propelled the US Dollar Index (DXY) to 106.30.

Recent events, including Iran’s attack on Israeli territory on April 13 and robust US Retail Sales data, coupled with strong labor demand and higher consumer price inflation in March, have bolstered arguments for potential delays in Fed rate cuts later this year.

San Francisco Fed Bank President Mary Daly emphasized on Friday that there is no immediate urgency to initiate interest rate reductions, emphasizing the need to maintain restrictive interest rates for a prolonged period to ensure inflation returns to the desired rate of 2%.

AUDUSD Breaking: China’s Q1 2024 GDP Growth Surpasses Expectations

China Q1 GDP Increased at 5.3%YoY versus 5.2%YoY printed in the last quarter. Quarterly basis increased at 1.6% versus 1.0% printed in the previous quarter. Retail sales at March month increased at 3.1% versus 4.5% expected and 5.5% printed last month. Industrial production came at 4.5% YoY versus 5.4% estimate and Previous month at 7.0%. Fixed asset investment came at 4.5% in March month versus 4.3% expected and 4.2% previous month. Overall all sides of China Data shows well strength versus previous quarters, So Australian Dollar moved mild higher against counter pairs.

AUDUSD has broken the Box pattern in downside

In the first quarter of 2024, China’s economy expanded by 5.3% year-over-year, compared to the 5.2% growth recorded in the final quarter of 2023, according to official data released by the National Bureau of Statistics (NBS) on Tuesday. Market expectations for this period were pegged at 5.0%.

On a quarterly basis, China’s Gross Domestic Product (GDP) saw a 1.6% increase in Q1 2024, up from the 1.0% growth registered in the previous quarter.

For March, China’s year-on-year Retail Sales climbed by 3.1%, falling short of the anticipated 4.5% and trailing behind the 5.5% recorded previously. Industrial Production in the country reached 4.5% year-on-year, below estimates of 5.4% and lower than February’s 7.0%.

Additionally, Fixed Asset Investment saw a year-to-date increase of 4.5% in March compared to the same period last year, surpassing expectations of 4.3% and exceeding the previous figure of 4.2%.

Yellen further stressed the importance of addressing the ongoing suffering endured by the Palestinian people, particularly emphasizing the responsibility of all participants at IMF-World Bank meetings to actively contribute to ending this plight.

Moreover, Yellen highlighted the US Treasury’s ongoing efforts in combatting terrorism associated with Iran and its proxies. She noted that since 2021, the Treasury has targeted over 500 individuals and entities believed to be linked to terrorism sponsored by Iran and its affiliated groups.

NZDUSD – drops on geopolitical concerns, trades under 0.5900

The NZDUSD moving down due to Middle east tensions of Iran over Israel. US retail sales data came at 0.70% in the March month makes NZ Dollar down against USD. China Q1 GDP rose to 1.6% from 1.0% printed in the previous quarter. But War tensions only impacted NZ Dollar moving downward pressures sustaining in the market.

NZDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

NZD/USD faces depreciation, nearing 0.5880 during the Asian trading session on Tuesday, as investors flock to the US Dollar (USD) amidst heightened geopolitical tensions in the Middle East. The recent escalation in conflicts between Israel and Iran, triggered by Iran’s airstrike over the weekend, prompts traders to seek safety in the USD. Market sentiment remains cautious as the world awaits Israel’s response to Iran’s attack.

Meanwhile, attention turns to New Zealand’s upcoming release of the Consumer Price Index (CPI) data for the first quarter of 2024, scheduled for Wednesday. Expectations hover around a slight uptick to 0.6% quarter-on-quarter, compared to the previous period’s 0.5%.

Recent diplomatic developments between China and Iran, where the Iranian foreign minister conveyed Iran’s restraint intentions, have failed to sway the New Zealand Dollar (NZD). Mixed Chinese economic data also influences the NZD, as China is a significant trading partner. China’s GDP rose by 1.6% quarter-on-quarter in Q1 2024, surpassing previous growth of 1.0%. Year-on-year GDP surged by 5.3%, exceeding expectations and the previous period’s figures. However, China’s Industrial Production in March fell short of market forecasts.

Conversely, the USD strengthens following robust US Retail Sales data, dampening hopes for potential Fed monetary policy easing. March’s Retail Sales surpassed forecasts, rising by 0.7%, with February’s figures revised upwards. Investors keenly await US housing data and Fed Chair Jerome Powell’s speech for further market cues.

CRUDE OIL – WTI trims gains post Iran attack, holds above $85.00

The Crude oil prices are remaining flat, Israel PM Benjamin NetanYahu called for War meeting and said we will do retailiation for Iran attack, Israel Military chief said we are marking sites on Iran for attacks. This fears the 3 million barrels per day will be problem for Global supply from Iran if Iran and Israel war begins.

XTIUSD Crude oil price is moving in the Box pattern and the market has reached the support area of the pattern

WTI crude oil prices climb to nearly $85.30 per barrel in Asian trading on Tuesday, driven by concerns over escalating tensions between Israel and Iran following Iran’s missile and drone attacks on Saturday. Israeli Prime Minister Benjamin Netanyahu convened his war cabinet for the second time in less than 24 hours to strategize a response to Iran’s direct assault, with Israel’s military chief indicating retaliatory measures targeting strategic sites in Iran.

Iran, a significant member of OPEC and a major crude oil producer, generates over 3 million barrels per day. Any escalation between Israel and Iran could potentially ignite a broader conflict in the Middle East.

Despite mixed data from China, the world’s largest oil importer, crude oil prices remain resilient. China’s first-quarter GDP expanded by 1.6% quarter-on-quarter and 5.3% year-on-year, surpassing expectations. However, industrial production in March grew by 4.5% year-on-year, missing forecasts and the previous reading of 7.0%.

Additionally, OPEC+ is considering Namibia for potential membership, given its projected status as Africa’s fourth-largest oil producer by the next decade. Namibia aims to join OPEC+’s Charter of Cooperation, a coalition focused on ongoing discussions about energy market dynamics.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!