XAUUSD – Gold Price Fluctuates After US NFP Data, Fed Officials’ Remarks

The Gold prices are higher against USD after the US Jobs report came at cooling than expected numbers. The ISM Services PMI contracted for First time Since December 2022 and came at 49.6 from 50.0 Level. The FED Rate cuts from September month is higher by economists view makes US Dollar down against counter pairs.

XAUUSD has broken Ascending channel in downside

Gold prices experienced a reversal of their earlier gains on Friday following the release of the US Bureau of Labor Statistics (BLS) Nonfarm Payrolls (NFP) data for April, which fell short of expectations, indicating a cooling job market.

The optimism prevailing on Wall Street is dampening the appeal of the safe-haven gold, with US Treasury yields declining, particularly the 10-year benchmark note, which is down by seven basis points. Consequently, US real yields, which have an inverse correlation with gold prices, have decreased from 2.219% to 2.146%.

A “Goldilocks” scenario appears to be shaping up for the US economy post the NFP report, as indicated by the Institute for Supply Management (ISM), which reported a contraction in business activity in the services sector for the first time since December 2022.

Meanwhile, several Federal Reserve (Fed) officials made significant statements. Fed Governor Bowman expressed a hawkish stance in an interview with Bloomberg Television, suggesting a willingness to hike rates if inflation stagnates or reverses. Additionally, the Chicago Fed’s Austan Goolsbee characterized the latest US employment report as solid, highlighting that the current monetary policy is restrictive.

Key highlights from the day’s market movements include:

– Gold prices being supported by lower US Treasury yields and a softer US Dollar.

– The US 10-year Treasury note yielding 4.506%, down seven basis points from its opening level.

– The US Dollar Index (DXY) dropping by 0.29% to 105.04.

– April US Nonfarm Payrolls revealing the addition of only 175,000 jobs, below the forecasted 243,000 and March’s upwardly revised 315,000.

XAUUSD is moving in Descending channel and market has fallen from the higher high area of the channel

– The Unemployment Rate slightly increasing from 3.8% to 3.9%, with Average Hourly Earnings (AHE) growing by only 0.2%, falling short of the expected 0.3%.

– The ISM April Services PMI falling below the critical 50.0 mark, indicating contraction, with a reading of 49.4.

– Fed rate cut probabilities increasing post-data release, with traders expecting 38 basis points of rate cuts by the end of the year.

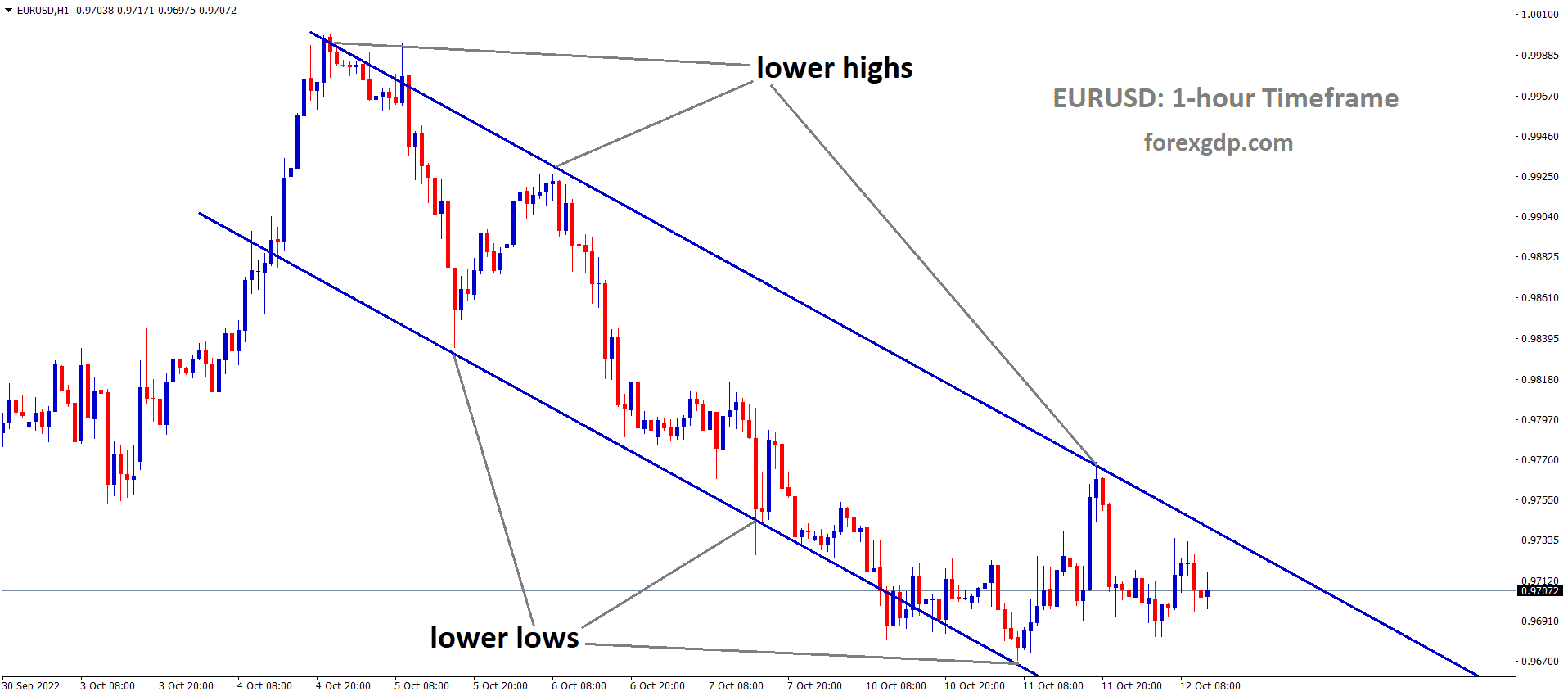

EURUSD – Stournaras of ECB: Likelihood of Three 2024 Cuts Increases

The ECB governing council member and Greece Governor Yannis Stournaras said there will be a 3 rate cuts in this year from 4 rate cuts previously forecasted. The Euro zone GDP numbers printed in the Q1 2024 and inflation rate probably come to 2% target in Mid -2025.

EURUSD is moving in Descending channel and market has fallen from the lower high area of the channel

Yannis Stournaras, a member of the European Central Bank (ECB) Governing Council and also serving as the Governor of the Bank of Greece, made remarks on Friday suggesting a potential adjustment in the ECB’s monetary policy stance. According to reports from Bloomberg, Stournaras indicated that instead of the previously speculated four rate cuts, the ECB is now more inclined towards implementing three rate cuts within the current year.

Stournaras elaborated on this stance with the following statements:

We now consider three rate cuts in 2024 as the more likely scenario.

He further commented on the economic outlook, stating:

If this pace of economic growth continues, then consumer-price growth is likely to be marginally higher than our March forecast, but without jeopardizing the 2% target in mid-2025.

Additionally, Stournaras highlighted the positive indicators observed in the most recent GDP figures for the eurozone, suggesting optimism regarding the economic trajectory.

GBPJPY – Hovers Around 192.00 Amid Possible BoJ Interventions

The Bank of Japan is overspent on this week in Uncategorised Financing operations nearly 9 trillion Yen. This news is not officially declared by BoJ but the markets shows strengthening of JPY against counter pairs.This week UK Q1 GDP is expected at 0.40% and BoE Interest rate decision scheduled this week.

GBPJPY is moving in Ascending channel and market has fallen from the higher high area of the channel

GBP/JPY is currently maintaining a steady trajectory near the 192.00 level, following suspicions of direct interventions by the Bank of Japan (BoJ) in the foreign exchange (FX) markets to support the weakened Japanese Yen (JPY). These suspected interventions occurred twice within the span of two days earlier this week. Recent disclosure reporting from the BoJ revealed an overspending of approximately 9 trillion Yen on uncategorized financing operations. This significant excess expenditure strongly suggests direct market intervention on behalf of the Yen, although no official statements have been issued by the BoJ to confirm or deny these actions.

Looking ahead to the upcoming week, the focus will shift to the Bank of England (BoE), which is scheduled to announce its latest rate decision and provide an update on the economic outlook. Additionally, late next week will bring a fresh update on UK economic growth through a quarterly Gross Domestic Product (GDP) report. Forecasts indicate a rebound in UK quarter-on-quarter (QoQ) GDP to 0.4% compared to the previous quarter.

Although Japanese markets resume normal operations following a series of holiday observations this week, data releases from Japan remain limited to low-tier prints. Investors will closely monitor any official statements from the BoJ regarding their market operations in the coming days.

USDCHF – Slips Below 0.9100, Awaits NFP Data

The Swiss Franc is appreciated against counter pairs after the Swiss CPI Data for the month of April came at 1.4% from 1.1% expected and 1.0% printed in the March month. The SNB have the chances to rate hold in the upcoming meeting is possible if inflation continuously in increasing mode.

USDCHF is moving in Ascending channel and market has reached higher low area of the channel

During the early European trading session on Friday, the USD/CHF pair continues its downward trend, marking its third consecutive day in negative territory.. This decline is attributed to the overall weakness of the US Dollar (USD) across the board.

Investors are eagerly awaiting the release of the US Nonfarm Payrolls (NFP) data for April, scheduled for Friday. Market analysts anticipate that the report will reveal an addition of 243,000 jobs to the US economy. The outcome of this data release is poised to have significant implications for market sentiment and may influence the trajectory of the USD/CHF pair in the short term.

The recent decision by the US Federal Reserve (Fed) to maintain its current monetary policy stance was announced during Wednesday’s press conference. Fed Chair Powell highlighted that while progress has been made on inflation, recent developments indicate a stall in this progress. As a result, the Fed is taking a cautious approach and will require more time to ascertain if inflation is moving towards the targeted 2% level. The expectation of sustained higher interest rates in the US is likely to support the US Dollar and limit the downside potential of the USD/CHF pair. Additionally, the Fed announced a deceleration in its balance sheet reduction program (Quantitative Tightening).

Meanwhile, in Switzerland, the annual inflation rate exceeded expectations in April, according to data released by the Federal Statistics Office. The Swiss Consumer Price Index (CPI) rose by 1.4% year-on-year in April, up from a 1.0% increase recorded in March, surpassing market forecasts of 1.1%. This accelerated inflation rate prompted a strengthening of the Swiss Franc (CHF), which in turn posed a headwind for the USD/CHF pair. Last week, Swiss National Bank (SNB) chairman Thomas Jordan expressed confidence that the central bank has effectively managed inflation, with projections indicating that price increases will remain within the SNB’s target range for the foreseeable future.

USDCAD – CAD Rises Against USD in Thursday’s Market Rebound

The BoC Governor Tiff Mackhlem said inflation is close to 2.9% sticky like this year. Rate cuts is the waited approach for the current stance and testimony before Canada House of Commons on this week. Canada Merchandise Trade balance data came at -2.28 Billion from 483 million in the previous month and 1.5 Billion is expected in the March. Hawkish speech from Governor makes Canadian Dollar moved higher against Counter pairs.

USDCAD is moving in Ascending channel and market has reached higher low area of the channel

The Canadian Dollar (CAD) staged a recovery alongside a broader improvement in market risk appetite on Thursday, following heightened investor tensions sparked by the US Federal Reserve (Fed) earlier in the week. S&P Global has revised its rate cut expectations for the year, now anticipating a single quarter-point reduction in December. However, consensus on Fed rate cuts appears increasingly inconsistent, with the CME’s FedWatch Tool indicating a reduced likelihood of a September rate cut, currently standing at 60%.

Bank of Canada (BoC) Governor Tiff Macklem made his second consecutive appearance, testifying before the Canadian government’s House of Commons Standing Committee on Finance alongside BoC Senior Deputy Governor Carolyn Rodgers. Meanwhile, Canadian International Merchandise Trade Balance figures for March unexpectedly declined, albeit with minimal impact on broader markets.

Key highlights from the day’s market movements include:

BoC Governor Macklem’s insights:

– Canadian inflation expected to remain close to 2.9% for several months, driven by gas prices.

– There are limitations to how much Canadian and US interest rates can diverge.

– Even if rates begin to decrease, the process is likely to be gradual.

– Consideration of potential CAD weakening is necessary when contemplating interest rate cuts.

Additionally:

– Canadian International Merchandise Trade declined by $2.28 billion in March, contrary to the forecasted improvement to $1.5 billion. The previous month’s figure was revised significantly downward to $480 million from $1.39 billion.

– US Q1 Unit Labor Costs rose to 4.7% quarter-on-quarter, surpassing the forecasted 3.2%, posing challenges for those anticipating rate cuts due to inflation concerns.

– Friday’s US Nonfarm Payrolls (NFP) labor report is anticipated to provide crucial insights into US employment figures, with median market forecasts projecting a print of 243K compared to the previous month’s 12-month peak of 303K.

USD INDEX – USD ends losing week after weak NFP

The US NFP Data for the month of April came at 175K versus 243K expected and 315K printed in the march month. The Unemployment rate came at 3.9% from 3.8% printed in the last month. The Average hourly earning index fell down to 3.9% in the April from 4.1% printed in the March month. So US Dollar fell down against counter pairs after the expected FED rate cuts in September month due to weak Job data.

USD Index Market Price is moving in Ascending channel and market has fallen from the higher high area of the channel

The US Dollar Index (DXY) has seen a notable decline, approaching the 105 level, marking significant losses as the trading week draws to a close. This downturn follows the release of disappointing US Nonfarm Payrolls (NFP) data for April on Friday, prompting a widespread sell-off of the USD in the markets.

The current state of the US economy presents a mixed picture of progress, characterized by robust demand and a tight labor market, alongside gradual yet noteworthy wage growth, which has contributed to inflationary pressures. Federal Reserve (Fed) Chair Jerome Powell has maintained a cautious stance regarding the uncertain trajectory of inflation, underscoring that the Fed’s prudent monetary policies have been instrumental in preventing economic overheating. However, the weak labor market data released on Friday has led market participants to increase their expectations of interest rate cuts by the Fed, particularly in September.

Key highlights from the daily market digest include:

– The US NFP report for April revealed an increase of 175K jobs, falling short of expectations set at 243K and indicating a decline from the revised 315K growth recorded in March.

– The unemployment rate experienced a rise from 3.8% to 3.9%.

– Wage inflation, as measured by Average Hourly Earnings, decreased to 3.9% year-on-year from the previous 4.1%.

– Market sentiment regarding a potential Fed rate reduction by September has strengthened following the release of weak labor market data.

Furthermore, US Treasury bond yields have witnessed a significant decrease, with the 2-year yield dropping to 4.80%, while the 5-year and 10-year yields declined to 4.50% and 4.58%, respectively.

GBPUSD – GBP Falls on Renewed US Services Price Concerns

The Bank of England Governor Andrew Bailey said inflation will come to our target in the April month numbers. There will be 3-4 rate cuts in this year is expected. US NFP Data makes GBP higher against USD. US Services paid readings came at 59.2 from 53.4 in the March month. Coming week, Uk Q1 GDP and BoE Interest rate meeting is scheduled.

GBPUSD is moving in Descending channel and market has reached lower high area of the channel

The Pound Sterling (GBP) experienced a reversal of its gains after rallying towards the round-level resistance of 1.2600 against the US Dollar (USD) during Friday’s early New York session. This retreat in the GBP/USD pair occurred as the US Dollar began to recover losses incurred following the release of the United States Nonfarm Payrolls (NFP) report for April. The report indicated weak labor demand and a slower-than-expected growth in wages.

The rebound in the US Dollar was prompted by the Service Prices Paid index, which advanced to 59.2 from 53.4, suggesting a further acceleration in price pressures during April. This development raised concerns about inflation and potentially dampened expectations for Federal Reserve (Fed) rate cuts, which were previously anticipated at the September meeting.

Conversely, the US ISM Services Purchasing Managers Index (PMI), representing the service sector, fell to 49.4, signaling contraction as it dipped below the 50.0 threshold separating expansion from contraction. This decline contradicted investor expectations of an improvement to 52.0 from March’s 51.4.

Earlier, the US NFP report revealed that nonfarm employers added 175,000 workers in April, below the consensus of 243,000 and the revised upward reading of 315,000 for March. The Unemployment Rate also rose to 3.9% from March’s 3.8%, while the Average Hourly Earnings softened to 3.9% from the expected 4.0% on a year-on-year basis. Monthly figures grew at a slower pace of 0.2% compared to the expected 0.3%.

In the broader market context, the Pound Sterling retreated from its position against the US Dollar as persistent US inflation pressures overshadowed the weak US NFP data. The rebound in the US Dollar Index (DXY) from a three-week low around 104.50 was attributed to easing labor market conditions, weak Q1 Nonfarm Productivity data, and the Fed’s less hawkish guidance on interest rates than feared.

Expectations of the Bank of England (BoE) potentially delaying interest rate reductions further strengthened the GBP/USD pair. Financial markets now anticipate the BoE to initiate rate cuts from the September meeting, aligning more closely with expectations of the US Federal Reserve’s similar move. Previously, investors were divided between expecting rate cuts at the June or August meetings.

The speculation surrounding the BoE’s stance on interest rate cuts has been deferred, with concerns persisting about robust wage growth in the United Kingdom, which fuels the core Consumer Price Index (CPI), the central bank’s preferred inflation measure. BoE Governor Andrew Bailey expressed confidence in the return of headline inflation to the desired 2% rate. The upcoming BoE monetary policy decision on May 9 is anticipated to maintain interest rates steady at 5.25%, with investors closely monitoring Governor Bailey’s adherence to previous statements regarding the possibility of rate cuts this year.

AUDUSD – Judo Bank’s Australian Services PMI Falls to 53.6 in April

The Australian Services PMI reading fell down in the April month as 53.6 from 54.4 printed in the March month. Economists at Judo Bank said this is the third straight month improvement in the Business index, Services from consumer is higher in the 2024, So rate cuts from RBA expected is diminish in the coming months.

AUDUSD is moving in box pattern and market has reached resistance area of the pattern

In April, Australia’s Judo Bank Services Purchasing Managers Index (PMI) experienced a slight decline, registering at 53.6, down from the previous month’s figure of 54.4. Despite this dip, there was notable growth in new services business, marking its fastest expansion since May 2022, driven by increased demand. However, the overall index performance was impacted as business charges decreased at a quicker rate, despite input costs rising at an accelerated pace.

Matthew De Pasquale, an Economist at Judo Bank, commented on the findings, stating, “The Australian Composite PMI for April confirms earlier ‘Flash’ PMI findings of an ongoing rebound in activity levels, continued employment growth, and improved business confidence.”

De Pasquale further elaborated, saying, “The services sector has been a key driver of the overall improvement in economic activity. Both the business activity and new order indexes have consistently remained in expansion territory over the past three months. Notably, the New Business Index recorded its highest reading since May 2022. While these indicators suggest a strengthening in consumption levels throughout 2024, official retail sales figures have yet to demonstrate clear signs of improvement, remaining subdued.”

NZDUSD – Approaches 0.6000 Before US NFP

The NZ Dollar moved higher after the RBNZ expected rate cuts in this year is delayed forecast, this is due to Wage growth and consumer spending is higher and in line with estimations. So Consumer spending higher then it moved inflation mark to ticked higher in coming months. US NFP Data and Services PMI came at below expected data last day is also supportive for NZ Dollar .

NZDUSD has broken Descending channel in upside

The NZD/USD pair continued its upward momentum for the second consecutive day on Friday, with the US Dollar dipping to a fresh three-week low. This movement occurred ahead of the release of two key economic reports in the New York session: the United States Nonfarm Payrolls (NFP) and the ISM Services Purchasing Managers Index (PMI) for April.

Investors closely anticipate these economic indicators as they provide insights into the current labor demand and overall economic health, crucial factors that influence the Federal Reserve (Fed) in its decision-making regarding interest rates. The reports will also fuel speculation about the timing of potential interest rate cuts by the Fed, with current expectations leaning towards a reduction starting from the September meeting.

Forecasts suggest that US nonfarm employers added 243,000 jobs in April, slightly lower than the robust 303,000 payrolls added in March. Additionally, attention will be on the Average Hourly Earnings data, a leading indicator of wage growth that impacts the inflation outlook. Analysts expect the Services PMI to show improvement, with a forecasted increase to 52.0 from the previous reading of 51.4.

Meanwhile, the New Zealand Dollar (NZD) has been strengthening amid expectations that the Reserve Bank of New Zealand (RBNZ) will commence interest rate reductions later this year. The recently released Labor Cost Index data, which reflects wage growth and its influence on consumer spending, met expectations in the first quarter of this year. This has bolstered expectations that the RBNZ may delay implementing rate cuts until later in the year.

CRUDE OIL – Oil Falls as Hamas Signals Ceasefire Potential

The Hamas Leader said Ceasefire Deal is completed with Good Sprit from Israel makes Oil prices down to $78 per Barrel. Ongoing war tensions in the Middle east is now eased after the Hamas- Israel stopped the War by smooth talks of Ceasefire deal. UAE announced it is going to up the production from 4.65 million barrels per day to 4.85 Million Barrels per day, Soon 5 Million Barrels per day by 2025 is planning. So Supply higher in Oil production makes Oil prices choppy market.

XTIUSD has broken Ascending channel in downside

Oil prices are relinquishing their gains on Thursday, potentially extending a four-day losing streak. This reversal occurred after initial gains turned into a slight loss following reports indicating that Hamas is open to considering the current ceasefire deal. Diplomatic efforts are intensifying in Gaza to broker a ceasefire, aiming to ease tensions in the region. Additionally, the US Energy Information Administration (EIA) released a report on Wednesday highlighting one of the largest crude stockpile increases in recent memory.

The US Dollar Index (DXY) is facing pressure around the 105.50 mark, after multiple attempts in the past two weeks to break below it. This level has held firm, particularly ahead of the US Jobs report for May, scheduled for release on Friday. The recent Federal Reserve rate decision brought no significant changes, with Fed Chairman Jerome Powell reiterating the Fed’s stance to wait for further inflation reduction before considering a rate cut.

As of the latest update, Crude Oil (WTI) is trading at $78.78, while Brent Crude stands at $83.53.

Key developments in the oil market include:

– Hamas spokesperson expressing openness to the current ceasefire deal.

– The UAE’s main oil company increasing production capacity from 4.65 million to 4.85 million barrels per day, aiming for 5 million barrels per day by 2027.

– The US EIA reporting a surprise increase in oil stocks of 7.265 million barrels, contrary to market expectations.

– India shifting from Venezuelan to Iraqi oil imports due to US sanctions.

– Citi’s commodity analyst predicting that OPEC+ will maintain supply curbs for the second half of the year.

– Shell’s CFO highlighting anticipated tightness in supply in the second half of the year, with OPEC+ policy playing a crucial role.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!