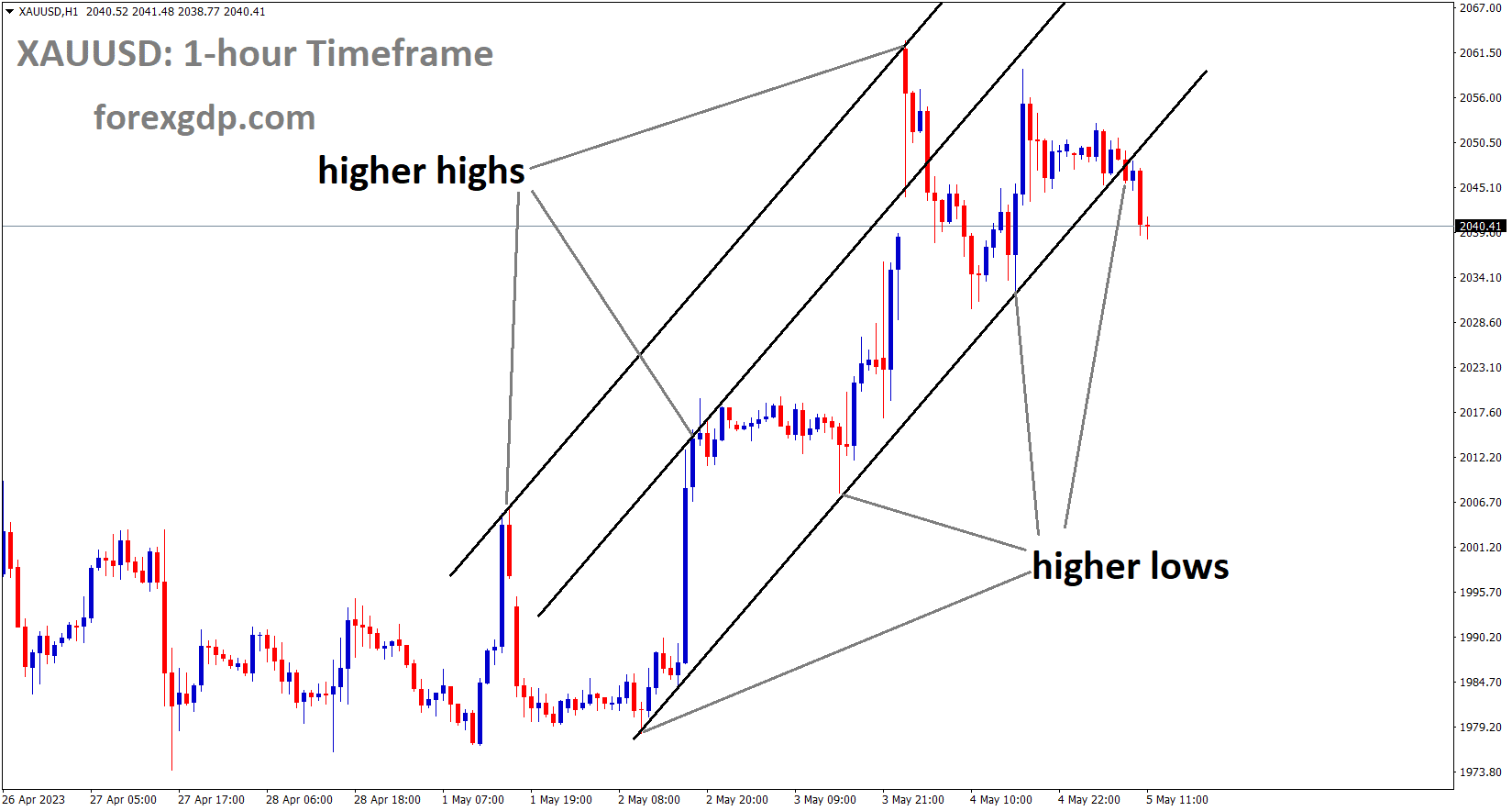

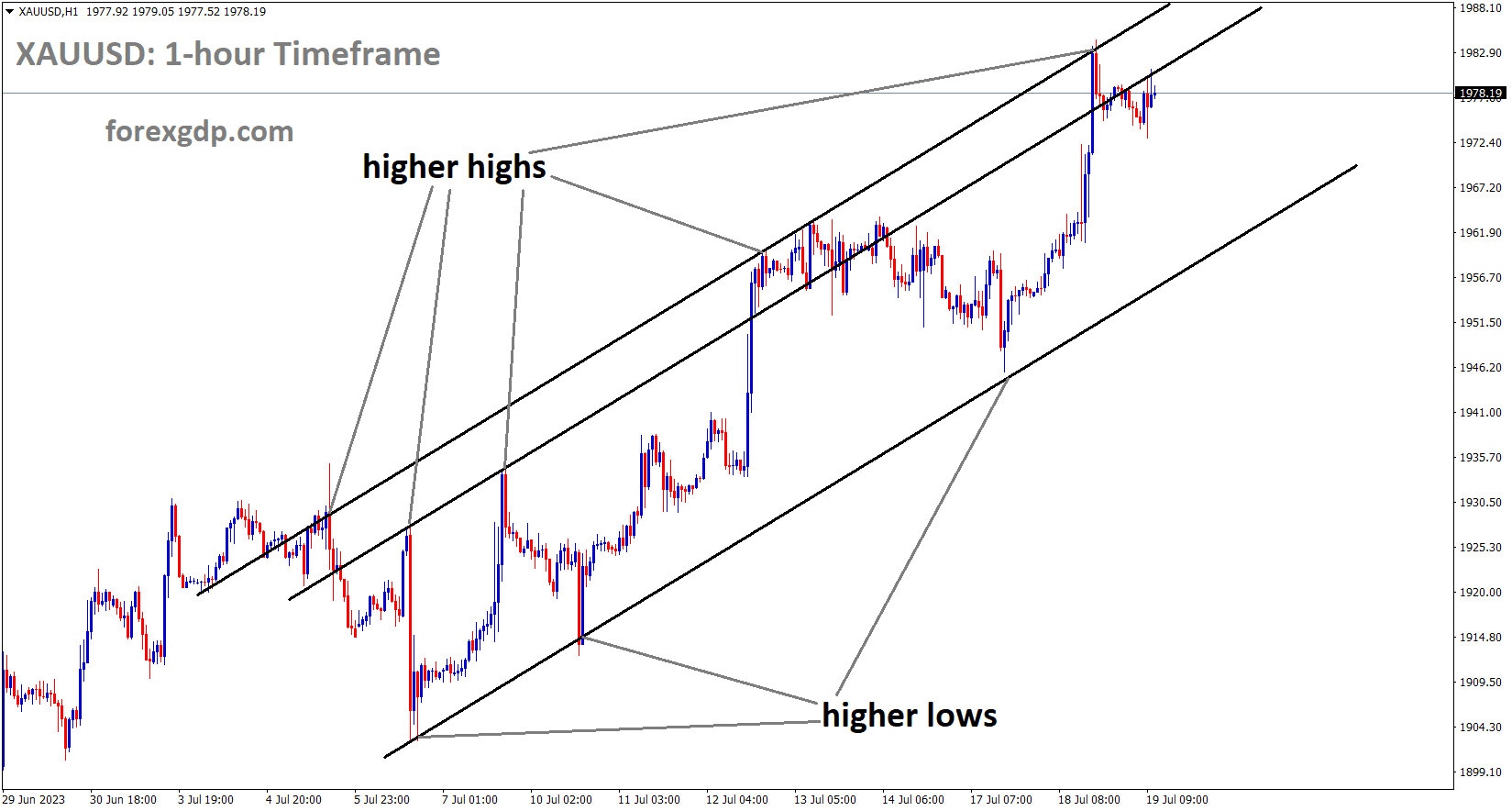

XAUUSD Analysis

XAUUSD Gold Price is moving in an Ascending channel and the market has reached the higher high area of the channel.

Following the release of less-than-expected US retail sales numbers for the month of June, gold prices have increased.Last week’s US CPI and PPI data were lower than anticipated, indicating lower US consumer spending and tight labour market concerns. There is a 99% chance that the FED will raise interest rates at its July meeting.

Gold increased after US retail sales in June increased less than anticipated, which hurt the US dollar and US Treasury yields. Despite disappointing headline retail sales, underlying consumer spending seemed to be strong because of a tight labour market. Following weaker US CPI and PPI data comes the mixed retail sales report. The Economic Surprise Index, which measures broader economic data, continues to show strong performance; the US ESI reached a two-year high earlier this month before reversing course slightly. The US dollar’s disproportionate reaction to lower retail sales and inflation, which nonetheless showed a robust economy, suggests the market is not in the mood to buy the dollar as there is an increasing belief that the Fed’s tightening cycle is about to come to an end.

According to the CME FedWatch tool, there is a 99% chance that rates will increase by a quarter of a percentage point at the meeting on July 25–26. However, the market is already pricing in rate reductions beginning in the middle of 2024 and reaching nearly 5 by the end of the following year. The Fed is forecasting two rate hikes before the year ends and no rate cuts until 2025, which contrasts with the market’s expectations.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Due to the anticipated increase in core inflation in the coming months, the Bank of Japan is anticipated to alter its ultra-loose monetary policy at its meeting next week. The Bank of Japan will support the yen and may soon alter its policy parameters.

For the second straight day, the Japanese Yen is losing ground against the US dollar. According to Commerzbank economists, it is important to monitor the JPY, especially on Friday when new inflation data for June will be released. Expectations that the BoJ might alter its ultra-expansionary monetary policy in some way next week are likely to rise if the overall rate falls only slowly while the core rate stays stubbornly high, which would support the Yen.

However, the BoJ would need to be more transparent than it was the last time, in December 2022, when it ‘only’ increased the yield range and briefly caused a lot of drama, but ultimately made it clear that it had not altered its monetary policy. The anticipated reversal was not started in the spring either by the new governor of the central bank, Kazuo Ueda. But perhaps the moment is finally here.

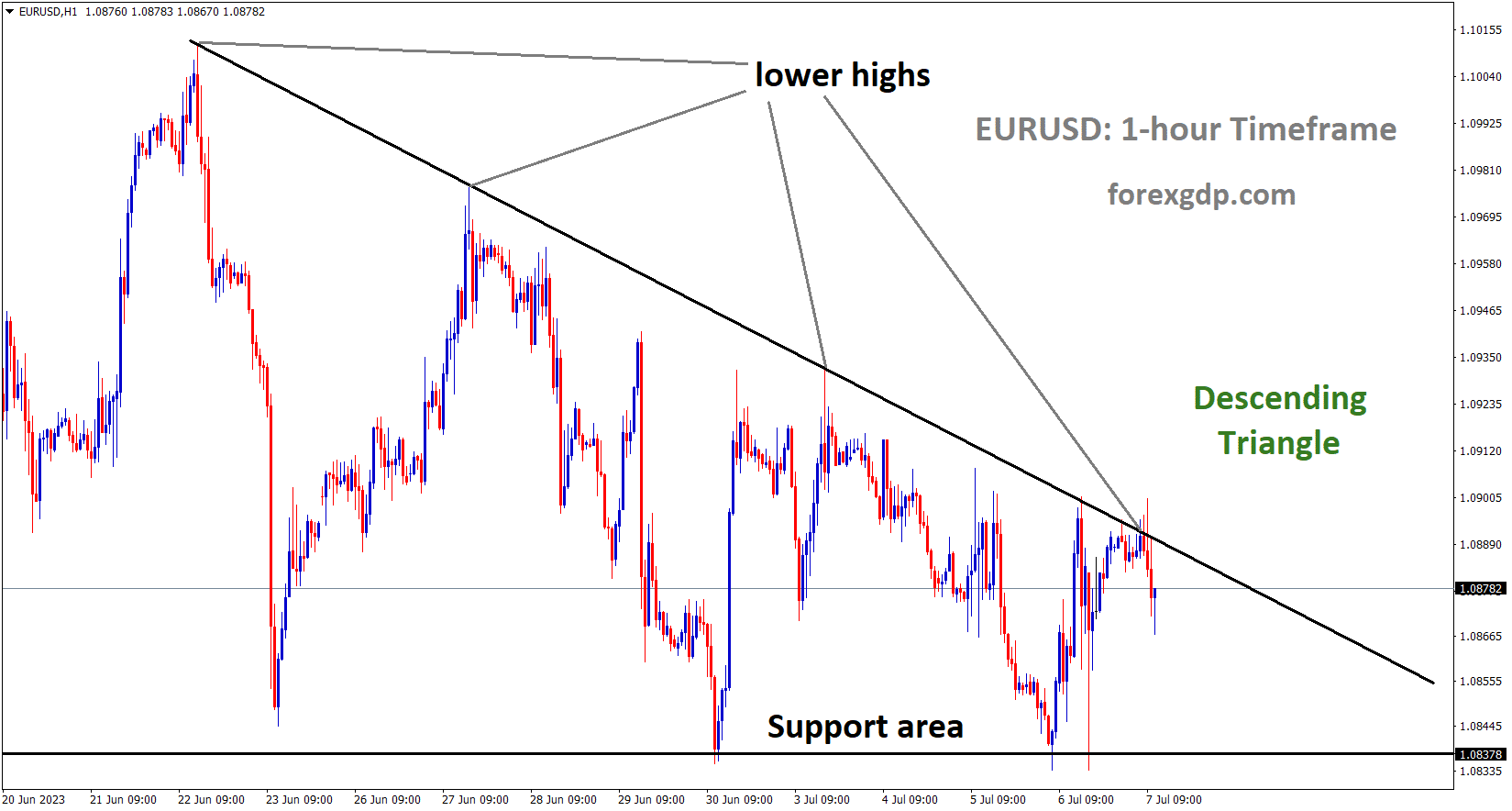

USD index Analysis

USD index is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

Negative US domestic data published after the rate hike was paused at the meeting last month prevented the US Dollar’s decline from recovering. According to economists, this month’s 25 bps rate increase will be the last one until the second half of 2023. After the FED overtightened, CPI, PPI, and retail sales data show sluggish numbers.

The DXY index, which measures the strength of the US dollar, experienced a significant decline during the first half of the month, but has since stalled at technical support near the psychological 100.00 level and lost momentum. While traders search for new market catalysts, consolidation may continue in the ensuing days. However, next week may bring about a clear change in trend as the Federal Reserve announces its July monetary policy meeting.

After a brief pause, the FOMC is expected to resume its normalisation cycle by raising rates by a quarter point to 5.25%–5.50%. Traders should put their main attention on forward guidance because the upcoming change in the policy stance has already been fully priced in. The U.S. central bank stated last month that it was prepared to implement an additional 50 basis points of tightening in the second half of the year, but the economy’s weakening price pressures may call for a softer stance. The U.S. dollar is likely to continue its recent decline as traders start to position for a full-fledged pivot if policymakers adopt a less hawkish stance or show any signs that their hiking campaign has ended. The DXY index could suffer significant losses as a result.

EURGBP Analysis

EURGBP is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

The Euro area Economic Surprise Index is at its lowest point since mid-2020 as a result of recent underwhelming Euro area data. The uneven post-Covid recovery in China is one factor contributing to the worsening outlook for the Euro area. Due to weak domestic demand and a slowdown in the real estate market, analysts have lowered their estimates for the Chinese economy.

Both the US Fed and the ECB may move forward with a 25-basis point increase in monetary policy next week. Beyond that, both central banks are uncertain as to whether and how much more rate increases will be made. From a fundamental standpoint, the EUR’s path of least resistance is currently sideways due to the limited relative monetary policy advantage.

Inflation will decline, according to UK Finance Minister Jeremy Hunt, and there is still time. However, today’s slower inflation readings are the first tangible results of the Bank of England’s difficult decision.

We can win the war against inflation, UK Finance Minister Jeremy Hunt said in response to the inflation data. The Bank of England (BoE) has made challenging choices. There is still a long way to go, but we are already beginning to see the results of the difficult choice.

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Euro Core CPI is anticipated to increase to 5.4% from 5.3% in May, but headline CPI is anticipated to decline to 5.5% from 6.1% in May. If the CPI reading for today was higher than anticipated, the ECB may raise interest rates by 25 basis points. Since the Bundesbank has already stated that Germany is currently entering a recession, the following increase will likely occur in September.

Before the important central bank meetings next week and the key Euro area inflation data later on Wednesday, the euro is testing the upper end of its recent range against the US dollar. In contrast to May’s 5.3% increase, the euro area core CPI is predicted to have increased by 5.4% in June. Although the headline CPI is predicted to have moderated from 6.1% to 5.5% on an annual basis, it will still have increased by 0.3% from May’s flat rate. Although a stronger-than-anticipated CPI print could guarantee a rate increase by the ECB next week, the inflation data alone might not be enough to drive the EUR significantly higher. Money markets predict that the ECB will raise interest rates by 25 basis points next week, with a 70% chance of doing so again in September. However, a bleak economic outlook seems to be raising the threshold for action in September. The German economy may contract more this year than anticipated, according to the Bundesbank’s statement on Monday. Additionally, ECB officials have recently sounded relatively dovish with regard to a move in September.

GBPCAD Analysis

GBPCAD has broken the Ascending channel in downside.

In contrast to the expected 8.2% and the 8.7% recorded in May, the UK CPI data for June came in at 7.9%. After additional rate hikes, the reading is more calming for the Bank of England this time.In his election platform, UK Prime Minister Rishi Sunak stated that due to the likelihood of a 2024 election, inflation must be under control by the end of 2023.Following the release of today’s data, GBP fell against the USD.

The UK’s June inflation report came in much softer than anticipated, which draws significant offers for the Pound Sterling GBP. Following the release of the data, the GBPUSD pair quickly fell below the psychological level of 1.3000, and more weakness is predicted. As households and businesses deal with the impact of higher interest rates from the Bank of England BoE, the monthly headline Consumer Price Index CPI increased at a negligible rate of 0.1% in June. More so than the markets had anticipated, the UK’s inflationary pressures have subsided thanks to lower factory gate prices for goods and services as well as aggressively restrictive monetary policy from the BoE. Investors are still unsure, though, whether UK Prime Minister Rishi Sunak will keep his promise to cut inflation in half by year’s end in advance of what is likely to be an election in 2024. As the Consumer Price Index for June weakened more than anticipated, the pound fell. According to the UK’s Office for National Statistics, monthly headline inflation increased by 0.1% in June, which was less than the 0.4% anticipated and the 0.9% increase seen in May.

In comparison to the consensus estimate of 8.2% and the 8.7% increase seen in May, the headline CPI slowed to 7.9% on an annual basis. Investors were expecting core inflation to rise at a steady 7.1% rate, but it slowed to 6.9% because it excludes volatile food and oil prices. The UK’s persistent inflation has been largely attributed to labour shortages and high food prices.

According to Reuters, UK grocery inflation eased for a fourth consecutive month in June to 14.9%, posting the biggest drop since its peak in March. Additionally, according to a Lloyds Bank survey, producers have reduced their prices for the first time in more than three years as a result of easing cost pressures, which is expected to reduce food inflation. Although the burden on households will likely be lessened by the synergistic effects of soft PPI and CPI, they are insufficient to permit the Bank of England to cut interest rates.

Interest rates are predicted by the markets to increase by another 100 basis points bps this year, reaching a peak of about 6.5%. The BoE’s burden of high inflation and higher interest rates is shifting from domestic firms to household consumers. According to the UK’s insolvency services, due to loan defaults, England and Wales are expected to report the highest quarterly number of company insolvencies since early 2009.The US Dollar Index DXY is attempting to maintain above the 100.00 psychological resistance level. Despite the fact that US retail sales growth fell short of expectations, the USD Index gained ground.

US retail sales increased 0.2% in June, which was less than the 0.5% increase that markets were anticipating. The Federal Reserve Fed may decide to raise interest rates only once more this year as a result of softening US inflation, loosening labour market conditions, and moderating retail demand. According to US Treasury Secretary Janet Yellen, a slowing labour market is assisting in containing inflation. Yellen added on Monday that she does not anticipate a recession and that the economy is doing well in bringing inflation back to 2%.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

After the Q2 CPI reading, which was printed at 6.0% instead of the expected 5.9%, came in slightly higher than the forecast reading, the NZD Dollar is slightly higher against the USD. Much lower than the 6.7% in the previous quarter.

Following the release of unexpectedly stronger local inflation data on Wednesday morning, the New Zealand Dollar increased. In contrast to the consensus estimate of 5.9%, New Zealand’s headline CPI rate for the second quarter came in at 6% y/y. In the meantime, inflation was 1.1% q/q instead of the expected 0.9%. Each reading decreased from its previous values of 6.7% and 1.2%. In response, financial markets started to factor in a Reserve Bank of New Zealand that was more hawkish. The financial markets were barely anticipating another hike by the end of this year prior to the data. Currently, a further increase of 25 basis points to 5.75% is largely priced in. Government bond yields in New Zealand increased following the negative data.

The central bank maintained its official cash rate at 5.5% last week as was predicted. The confidence of policymakers in the ability of restrictive rates to bring inflation back to target was noted. The governor also emphasised that homeowners have not yet fully benefited from the tightening cycle. Early next year, the average mortgage rate on outstanding loans is predicted to increase to 6% from 3%. Being a central bank is challenging because monetary policy has lags. As a result, even if the RBNZ raised interest rates once more, the market pricing would still be constrained by the possibility of just one more increase.

AUDCAD Analysis

AUDCAD is moving in the Descending channel and the market has reached the lower low area of the channel.

Following the release of June CPI data that came in at 2.8% versus a forecasted 3.0% and a prior reading of 3.4%, the Canadian Dollar experienced market weakness. The Bank of Canada raised interest rates by 25 basis points in response to inflation data.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

In a meeting with US diplomat Henry Kissinger, China’s defence minister Li Shangfu stated that the US must exercise sound strategic judgement when dealing with China. This week, there will be a change in Australian employment, and the data will affect the AUD.

The Reserve Bank of Australia’s (RBA) minutes, which were made public in Asia, hinted that additional policy tightening might be required. At the policy meeting in August, the decision-makers will, however, change their minds. China’s defence minister, Li Shangfu, said that the US should use sound strategic judgement in dealing with China during a meeting with top US diplomat Henry Kissinger on Tuesday in Beijing. Market participants will monitor the progress of Sino-US relations in search of new dynamism.

Australia will publish its Employment Change and Employment Change reports on Thursday. Participants in the market will also follow US housing starts and unemployment claims as indicators. These statistics would significantly affect the AUD pair.

The current risk-on environment is thought to be decreasing demand for the safe-haven. CHF, the Swiss Franc Speculations about the possibility of additional government stimulus measures increased as a result of this week’s weaker economic data from China. This, in part, assuages worries about China’s slowing economic growth and increases investor confidence, which sparked the recent rally in global equity markets.

Crude oil Analysis

Crude oil Price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In Canada, headline inflation YoY fell to 2.8% in June, beating expectations of 3%. Petrol prices were the main factor in the decrease in inflation, which was fairly widespread. With petrol excluded, headline inflation would have been 4.0% in June after rising by 4.4% in May. Food prices continue to be a problem, as seen throughout much of the developed world, with the UK struggling in particular with high food prices. The CPI increased by 0.1% on a monthly basis in June after increasing by 0.4% in May. Travel tours put downward pressure on the monthly all-items index in June after helping to increase it in May. The CPI increased 0.1% on a monthly basis after season adjustment. In June 2023, Canadian annual core inflation—which excludes the cost of food and energy—slowed to a 2-year low of 3.2%, down from 3.7% in May and below 3.5% market expectations. Another encouraging development for the Bank of Canada (BoC) is that the PPI MoM decreased significantly, coming in at -0.6%, suggesting that further relief from price pressures is still possible. Money markets now predict a 22% chance of a Bank of Canada rate hike in September, down from a 25% probability before the inflation data.

All eyes were on the Bank of Canada (BoC) going into the July 12 meeting because it was the central bank setting the example for other central banks in the tightening cycle. The 25 bps increase in July, which had surprised everyone at the previous meeting, was merely a formality because the market had already largely priced it in. Have rates reached a peak from the BoC in light of the inflation data from today? That is a challenging question, especially in light of Governor Macklem’s cautionary statement that a slowdown in inflation may start to stall and take longer than initially anticipated. The Governor will probably be pleased with today’s print, which could mean that rate increases from the BoC are coming to an end.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/