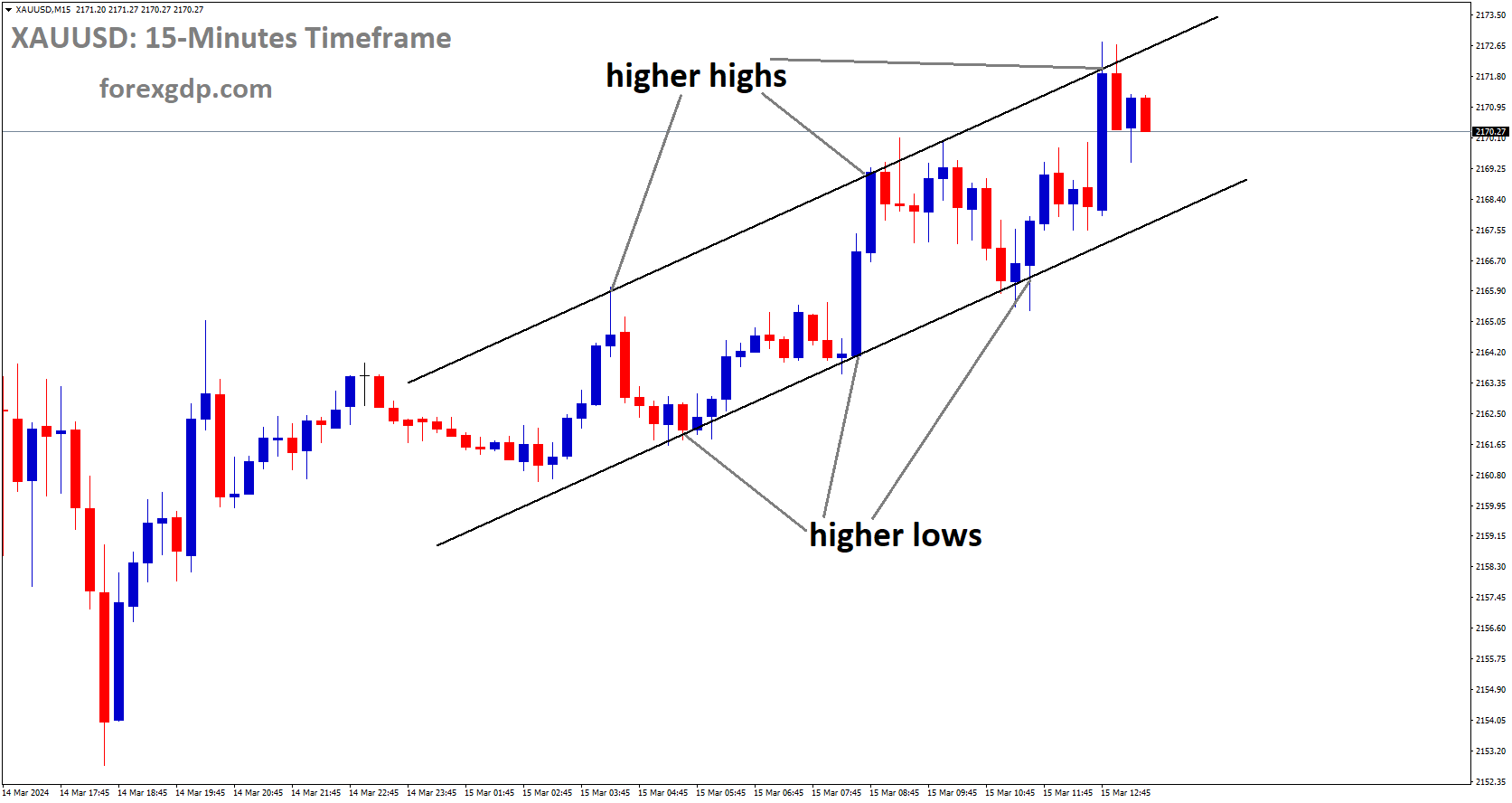

XAUUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

XAUUSD – Gold Price Dynamics Amid Fed Rate Cut Speculation

Amid expectations of a June Fed rate cut and a subdued risk sentiment, the allure of gold prompts buying interest. However, this upward movement lacks sustained momentum due to uncertainty surrounding the Fed’s rate decision. Traders await US macro data to gain momentum before the upcoming FOMC meeting.

Despite this, gold remains range-bound as traders await clarity on the Fed’s rate cut stance. Attention is centered on the impending FOMC meeting, while speculation persists regarding the timing of rate cuts. The recent uptick in Producer Price Index fuels speculations, although the market still anticipates rate cuts in June.

US economic indicators, coupled with bond yields, will influence USD dynamics and, consequently, gold prices. Short-term trading opportunities hinge on broader market sentiment. Nonetheless, gold may see modest losses after a prolonged winning streak.

Recent data, including higher-than-expected Producer Price Index and lower Initial Jobless Claims, have implications for Fed policy. Despite softer Retail Sales figures, the market maintains expectations of a rate cut in June, albeit with caution due to geopolitical tensions.

Investors grow wary amid geopolitical tensions, supporting gold’s safe-haven status. Developments such as Russia’s strategic maneuvers further influence market sentiment.

As traders await key economic releases, attention remains fixed on the upcoming FOMC meetings for insights into the Fed’s policy direction and its impact on gold prices.

EURUSD – Near Key Level Amid Fed Rate Cut Speculation

EUR/USD is on the brink of a significant threshold as it approaches, a level that could potentially determine the short-term direction of the pair. This proximity to such a critical level suggests heightened sensitivity to market dynamics, with further downward movement potentially favoring bearish sentiment.

EURUSD is moving in Ascending channel and market has reached higher low area of the channel

The recent trajectory of EUR/USD has been influenced significantly by developments in US macroeconomic indicators, particularly those released on Thursday. Of notable impact was the US Producer Price Index (PPI) data, which showed an unexpected 1.6% year-on-year increase in February, surpassing both the previous month’s figure and market consensus estimates. This robust performance in PPI, coupled with lower-than-anticipated Initial Jobless Claims and a moderate uptick in Retail Sales, indicates a stronger-than-expected resilience in the US economy. Consequently, this data implies a reduced likelihood of early interest rate cuts by the Federal Reserve (Fed) to stimulate economic activity, thus exerting downward pressure on EUR/USD.

The European Central Bank (ECB) has also contributed to market uncertainty surrounding EUR/USD through divergent statements from its policymakers. While ECB President Christine Lagarde has indicated a review of interest rates in June, other members have expressed differing opinions regarding the timing of rate cuts. For instance, Governor of the Bank of France Francois Villeroy de Galhau suggested the possibility of an interest-rate cut as early as April, while others like Governor of the Bank of Austria Robert Holzmann have aligned with a June timeframe. This divergence within the ECB reflects varying outlooks on the economic landscape, with some advocating for immediate policy action while others prefer a more cautious approach.

Looking ahead, the economic calendar for Friday includes key US data releases such as the Empire State Manufacturing Index, Industrial Production figures, and the Michigan Consumer Sentiment Index. These indicators are expected to provide further insights into the health of the US economy and could potentially influence short-term movements in EUR/USD.

Additionally, market participants will closely monitor speeches from influential figures such as Bundesbank President Joachim Nagel and ECB chief economist Philip Lane. Any remarks pertaining to ECB policy direction or economic outlook could offer valuable guidance to traders navigating the current uncertainty surrounding EUR/USD dynamics.

USDJPY – JPY Recovers Amid BoJ Policy Uncertainty

The Japanese Yen (JPY) sees a slight rebound from its recent lows against the US Dollar (USD), but gains are limited due to uncertainty surrounding the Bank of Japan’s (BoJ) policy stance. Market sentiment is influenced by Japan’s corporate response to wage hike demands and a cautious outlook from BoJ Governor Kazuo Ueda. Additionally, a moderate USD uptick, fueled by expectations of sustained interest rates from the Federal Reserve (Fed), keeps pressure on USD/JPY. Traders await US economic data for short-term cues while eyeing next week’s BoJ and FOMC meetings for potential market direction. Despite uncertainties, the USD/JPY pair remains on track for weekly gains.

USDJPY is moving in Ascending channel and market has reached higher high area of the channel

BoJ’s Policy Uncertainty Weighs on Japanese Yen Amid USD Strength

The Japanese Yen (JPY) experiences a modest recovery against the US Dollar (USD) but struggles to gain momentum as uncertainty looms over the Bank of Japan’s (BoJ) policy decisions. Comments from BoJ Governor Kazuo Ueda hint at a cautious approach towards monetary stimulus withdrawal, contrasting with speculation of an imminent policy shift. Meanwhile, the USD gains support from hotter-than-expected US Producer Price Index data, tempering expectations of a June interest rate cut and boosting Treasury bond yields. Traders await US economic releases while keeping a close watch on the upcoming BoJ and FOMC meetings to gauge the USD/JPY pair’s near-term trajectory.

USD INDEX – US Dollar Gains on Strong PPI, Soft Retail Sales Data

US Dollar Index (DXY) surged by 0.55% to 103.36, buoyed by robust Producer Price Index (PPI) figures and a consequent rise in US Treasury yields. However, soft Retail Sales and Jobless Claims data tempered the Dollar’s gains.

USD Index is moving in Descending channel and market has reached lower high area of the channel

The US Bureau of Labor Statistics revealed that February’s PPI surpassed expectations, with a year-on-year (YoY) increase of 1.6%, outperforming the consensus of 1.1%. Moreover, the core PPI, excluding volatile items, rose by 2.8% YoY, surpassing the previous figure of 2.6%.

In contrast, February’s Retail Sales saw a modest 0.6% monthly increase, falling short of the expected 0.8%. Similarly, Initial Jobless Claims for the week ending March 9 were reported at 209K, below the predicted 218K but higher than the prior week’s 210K.

Despite signs of persistent inflation, market expectations regarding the Federal Reserve’s (Fed) monetary policy remain stable. Forecasts indicate a less than 15% chance of a rate cut in May and a 60% likelihood for June, aligning closely with the Fed’s projection of three cuts this year.

US Treasury yields soared to two-week highs, with the 2-year yield at 4.70%, the 5-year yield at 4.29%, and the 10-year yield at 4.28%. This mixed economic outlook in the US underscores the delicate balance between inflationary pressures and tepid economic activity.

USDCHF – USD Gains on Yield Rise; SNB Worried about CHF

The recent upward movement in US Treasury yields has acted as a significant driving force behind the strengthening of the US Dollar (USD) across currency markets. This increase in yields has boosted investor confidence in the US economy and its currency, contributing to the appreciation of the USD against other major currencies, including the Swiss Franc (CHF).

USDCHF is moving in Ascending channel and market has rebounded from the higher low area of the channel

At the same time, Thomas Jordan, the Chairman of the Swiss National Bank (SNB), has raised concerns regarding the strength of the Swiss Franc and its potential adverse effects on Swiss businesses. The appreciation of the CHF can negatively impact Swiss exporters by making their products more expensive in international markets. As a result, Jordan’s remarks underscore the importance of managing currency valuations to support the competitiveness of Swiss industries.

Adding to the USD’s strength is the robust performance of US economic indicators, notably the Producer Price Index (PPI) data. The PPI measures the average change over time in the selling prices received by domestic producers for their output and serves as a key indicator of inflationary pressures in the economy. Stronger-than-expected PPI figures indicate rising prices for goods produced in the US, which can bolster the USD by signaling potential inflationary pressures and increasing the likelihood of the Federal Reserve maintaining its current monetary policy stance, including higher interest rates.

Furthermore, the US Dollar Index (DXY), which measures the value of the USD against a basket of other major currencies, benefits from the hawkish sentiment surrounding the Federal Reserve. Market expectations that the Fed will continue to pursue a policy of higher interest rates to combat inflationary pressures provide additional support to the USD, attracting investors seeking higher yields.

Amid these developments, the USD/CHF currency pair has experienced notable movements, with the USD gaining ground against the CHF. The combination of rising US Treasury yields, strong economic data, and concerns over the strength of the Swiss Franc has contributed to the USD/CHF pair’s upward trajectory. This dynamic underscores the interconnectedness of global financial markets and the impact of central bank policies and economic indicators on currency valuations.

EURGBP – ECB and BoE Rate Cut Outlooks Shape Market

The upcoming monetary policy decisions of the European Central Bank (ECB) and the Bank of England (BoE) are anticipated to shape market dynamics, with the ECB likely to initiate rate cuts in June, followed by a similar decision by the BoE in August.

EURGBP is moving in box pattern and market has reached support area of the pattern

The Pound Sterling’s trajectory hinges on the UK’s inflation data scheduled for release on Wednesday, serving as a crucial indicator for investors. Despite expectations of a potential rate cut by the BoE following the ECB’s move, the EUR/GBP pair displays resilience, bouncing back during Friday’s European session.

Market sentiment heavily leans towards the ECB implementing rate cuts during its June policy meeting, supported by a notable decrease in inflationary pressures within the Eurozone economy. Core inflation figures decelerated to 3.1% in February, signaling limited upward price pressures amidst a subdued economic outlook.

Key ECB policymakers, including Klaas Knot and Yannis Stournaras, express support for an early rate cut, highlighting the possibility of multiple rate reductions throughout 2024. Their remarks reinforce market expectations of an imminent monetary policy adjustment by the ECB.

Meanwhile, investor attention turns towards the BoE’s interest rate decision, slated for announcement on Thursday. Although the BoE is expected to maintain its interest rates at 5.25%, market focus remains on the UK’s inflation data for February, which is poised to influence expectations regarding potential rate cuts by the BoE. Presently, market sentiment anticipates the first rate cut by the BoE to occur in August.

AUDUSD – Australian Dollar Falls on Stronger US Data

The Australian Dollar (AUD) faces continued downward pressure on Friday, marking its second consecutive day of losses and hitting weekly lows against the US Dollar (USD). The AUD/USD pair depreciates as the USD gains strength, fueled by robust Producer Price Index (PPI) data from the United States. The outlook for interest rate cuts by the Federal Reserve becomes more uncertain in light of this data, contributing to the USD’s momentum.

AUDUSD is moving in Descending channel and market has reached lower high area of the channel

In the Australian stock market, the S&P/ASX 200 Index experiences significant losses, dropping to its lowest levels in three weeks. This decline mirrors the downturn on Wall Street, with major banking and mining shares leading the sell-off. The Reserve Bank of Australia (RBA) maintains its stance on the potential for further rate hikes, with its policy decision looming next week. Investors will be closely monitoring the release of the preliminary US Michigan Consumer Sentiment Index for further market cues.

The US Dollar Index (DXY) benefits from the hawkish sentiment surrounding the Federal Reserve, which is considering maintaining its higher interest rates in response to ongoing inflationary pressures. Additionally, US Treasury yields have been on the rise for the past four consecutive sessions, further supporting the USD and weighing on the AUD/USD pair.

In Australia, the NAB Business Confidence Index decreases while the Business Conditions Index improves. Analysts anticipate the RBA to maintain its official cash rate at 4.35% for the third consecutive meeting, with no expected changes until at least the end of September. RBA Governor Michele Bullock attributes inflation in Australia to strong labor market conditions and increasing wage inflation, foreseeing no significant changes until 2026.

The People’s Bank of China (PBOC) maintains the 1-year Medium-term Lending Facility (MLF) rate at 2.5% and continues injecting cash via MLF for the 16th consecutive month. However, the amount injected this time is slightly lower than the maturing amount.

US Treasury Secretary Janet Louise Yellen remarks on the unlikely return to pre-pandemic interest rate levels and considers the interest rate assumptions in President Biden’s budget plan reasonable. According to the CME FedWatch Tool, the probability of a rate cut in March remains low, with expectations decreasing for May and beyond.

Meanwhile, US Core PPI remains consistent, exceeding expectations, while US Retail Sales show modest growth but fall short of forecasts. These economic indicators contribute to the overall market sentiment and impact currency valuations.

NZDUSD – Strong US Data and Weak NZ PMI Impact NZD/USD Pair

During the early Asian session on Friday, the NZD/USD pair exhibits weakness, trading below the mid-0.6100s. The pair’s decline is attributed to robust US Producer Price Index (PPI) data, which exerted downward pressure.

NZDUSD is moving in Ascending channel and market has reached higher low area of the channel

On Thursday, US February Retail Sales figures showed a 0.6% month-on-month (MoM) increase, although below expectations of a 0.8% rise, signaling weaker consumer spending momentum. The Retail Sales Control Group remained stagnant at 0% MoM, contrasting with the previous month’s 0.3% decline. Additionally, February’s PPI surpassed estimates, rising by 0.6% MoM compared to January’s 0.3% increase. The Core PPI also showed growth, climbing by 0.3% MoM, albeit slower than January’s 0.5% gain.

These upbeat US economic indicators follow a surprise rise in the CPI inflation report earlier in the week, raising concerns about disinflationary trends in the US. The data suggests the Federal Open Market Committee (FOMC) may adopt a cautious stance and await further data before considering interest rate cuts. This potential delay in the Fed’s monetary easing cycle bolsters the US Dollar.

Meanwhile, recent data from Business NZ reveals that New Zealand’s Business NZ Performance of Manufacturing Index (PMI) for February improved to 49.3 from 47.3 previously. Although showing signs of progress, the index remains within the contraction zone, contributing to the Kiwi’s struggle against the US Dollar.

Looking ahead, traders will closely monitor US Industrial Production and the preliminary Michigan Consumer Sentiment index on Friday. Additionally, the upcoming FOMC monetary policy meeting next week will be a focal point, with traders seeking guidance from data releases and exploring trading opportunities around the NZD/USD pair.

USDCAD – Rises on Strong US PPI and WTI Prices

The USD/CAD pair continues its upward trend following the release of robust US Producer Price Index (PPI) data. The US Core PPI, which remained steady with a 2.0% year-over-year increase and rose by 0.3% month-over-month in February, surpassed expectations. This positive data, coupled with higher West Texas Intermediate (WTI) oil prices, has implications for both the US Dollar and the Canadian Dollar.

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

The US Dollar Index (DXY) benefits from a hawkish sentiment surrounding the Federal Reserve, with considerations of maintaining higher interest rates amid persistent inflationary pressures. This sentiment is reinforced by a four-session increase in US Treasury yields. The DXY remains strong, hovering around 103.40, with notable corrections in the 2-year and 10-year yields on US Treasury bonds.

Meanwhile, the rise in WTI oil prices, now in its third consecutive day, is driven by signs of robust demand in the US and an optimistic global consumption outlook for 2024. As Canada is a major oil exporter to the US, the positive trend in crude oil prices could lend support to the Canadian Dollar (CAD). Consequently, this could potentially limit the upside potential of the USD/CAD pair.

In the Canadian economic landscape, Manufacturing Sales showed a rebound to 0.2% in January, though falling short of the forecasted 0.4%. Nevertheless, it marks a recovery from the previous month’s decline. Investors are now awaiting the release of Housing Starts and Wholesale Sales data, which may offer further insights into the Canadian economic outlook.

Overall, the USD/CAD pair’s movements are influenced by a combination of strong US economic data, including the PPI figures, and the dynamics of the oil market, with implications for both currencies involved.

XTIUSD – WTI Pauses Amid Hawkish Fed Outlook and Supply Concerns

WTI Crude Oil hesitates after recent rally to year-to-date highs, as concerns over hawkish Fed stance and Chinese economic slowdown linger. However, anticipated increase in demand serves as a buffer against significant price declines.

XTIUSD is moving in Ascending channel and market has rebounded from the higher low area of the channel

The unexpectedly high US Producer Price Index (PPI) raises speculations that the Federal Reserve may maintain its current interest rate strategy to combat inflation. This outlook, coupled with apprehensions regarding a slowdown in China, creates a challenging environment for Crude Oil prices. Despite this, factors such as a notable reduction in US inventories, drone strikes on Russian refineries, and optimistic energy demand projections help support prices.

The Energy Information Administration’s (EIA) report revealing an unexpected decrease in US crude stockpiles, alongside Ukraine’s significant drone attacks on Russian energy infrastructure, including a fire at Rosneft’s largest refinery, contribute to market dynamics. Furthermore, the International Energy Agency’s upward revision of oil demand growth for 2024, amid supply disruptions caused by Houthi attacks in the Red Sea, bolsters confidence.

In continuation, OPEC+ members’ decision to prolong production cuts throughout the second quarter further underpins the potential for Crude Oil prices to continue their upward trajectory. Despite prevailing uncertainties, the market’s attention now turns to the imminent two-day FOMC monetary policy meeting commencing next Tuesday, which is poised to influence further market movements.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/