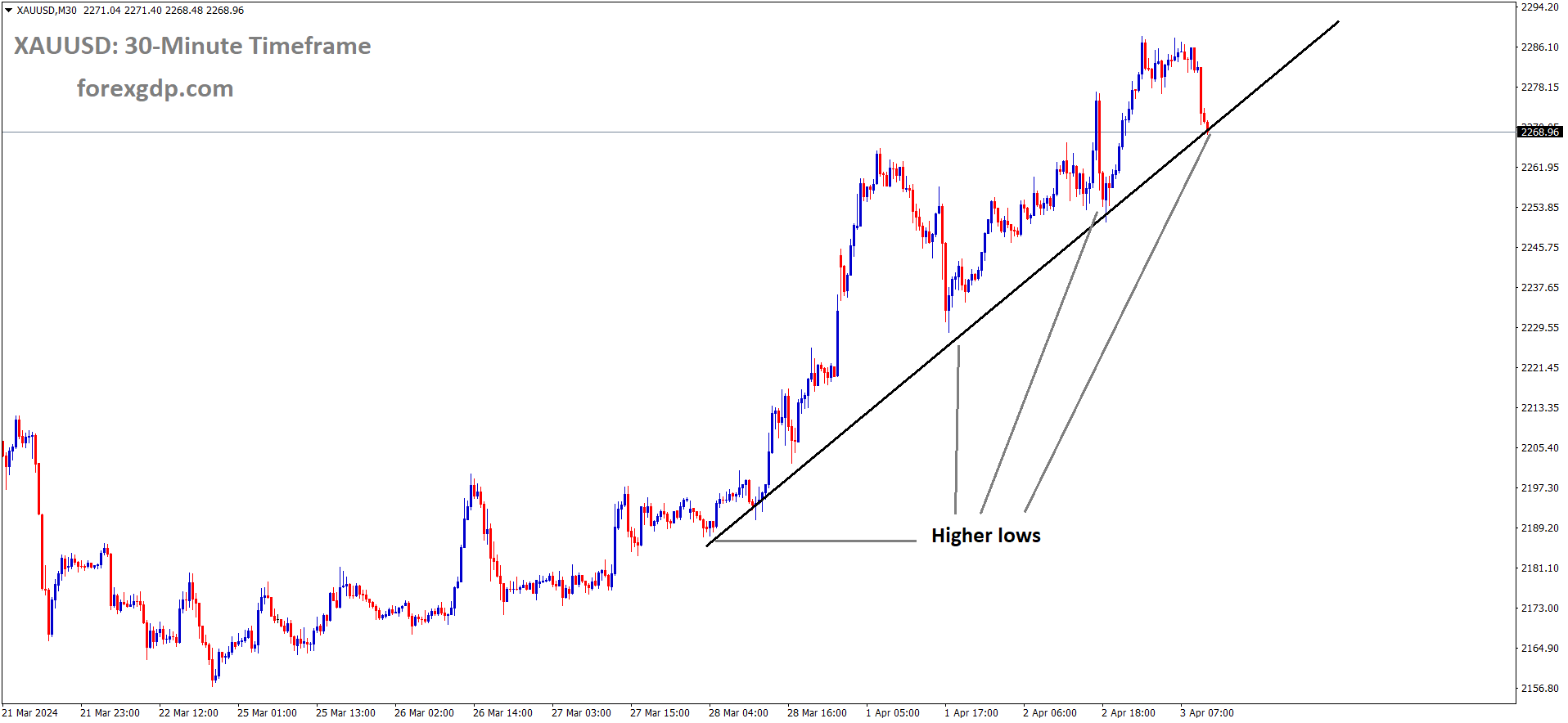

XAUUSD Gold price is moving in an Ascending trend line and the market has reached the higher low area of the trend line

XAUUSD – Gold price retreats from record high amid Fed rate cut uncertainty, prompting profit-taking.

The Gold prices are moving higher after the Israel attacked Iran Embassy in Syria, Senior official killed in this attack, any retailiation from Iran will create war fear increased in the middle east.

US Domestic data supporting US Dollar, rate cut in June month is slightly vanishing due to strong domestic data of US economy.

The price of gold (XAU/USD) slightly declines as the European session begins, with some investors engaging in profit-taking after the recent surge that led to a new record high earlier on Wednesday. The retreat comes amid a reassessment of expectations for a June interest rate cut by the Federal Reserve (Fed) following robust US macroeconomic data, indicating the resilience of the economy. This has bolstered US Treasury bond yields, providing support to the US Dollar (USD) and restraining the demand for gold, especially as conditions on the daily chart appear somewhat overextended.

Despite the profit-taking, significant downward movement in the gold price is constrained by ongoing geopolitical tensions, such as the prolonged conflict between Russia and Ukraine and recent Israeli strikes on Iran’s embassy in Syria. These events maintain a risk-off sentiment among investors, favoring traditional safe-haven assets like gold. Additionally, uncertainties surrounding the Fed’s rate-cutting plans and the impact of a devastating earthquake in Taiwan contribute to global risk aversion, suggesting that any decline in gold may be limited until further confirmation of a market shift.

In the context of market movements, recent data releases indicate an expansion in the US manufacturing sector for the first time since September 2022, alongside persistently high job openings. However, Federal Reserve policymakers, including San Francisco Fed President Mary Daly and Cleveland President Loretta Mester, have expressed differing views on the necessity and timing of interest rate cuts. This uncertainty is reflected in market expectations, with current pricing indicating a reduced likelihood of rate cuts and a yield increase in the benchmark 10-year US government bond.

Investor focus now turns to upcoming US economic data releases, including the ADP report on private-sector employment and the ISM Services PMI, as well as speeches by influential FOMC members. These events are expected to provide further insights into the economic outlook and potential monetary policy adjustments, influencing gold prices and market sentiment.

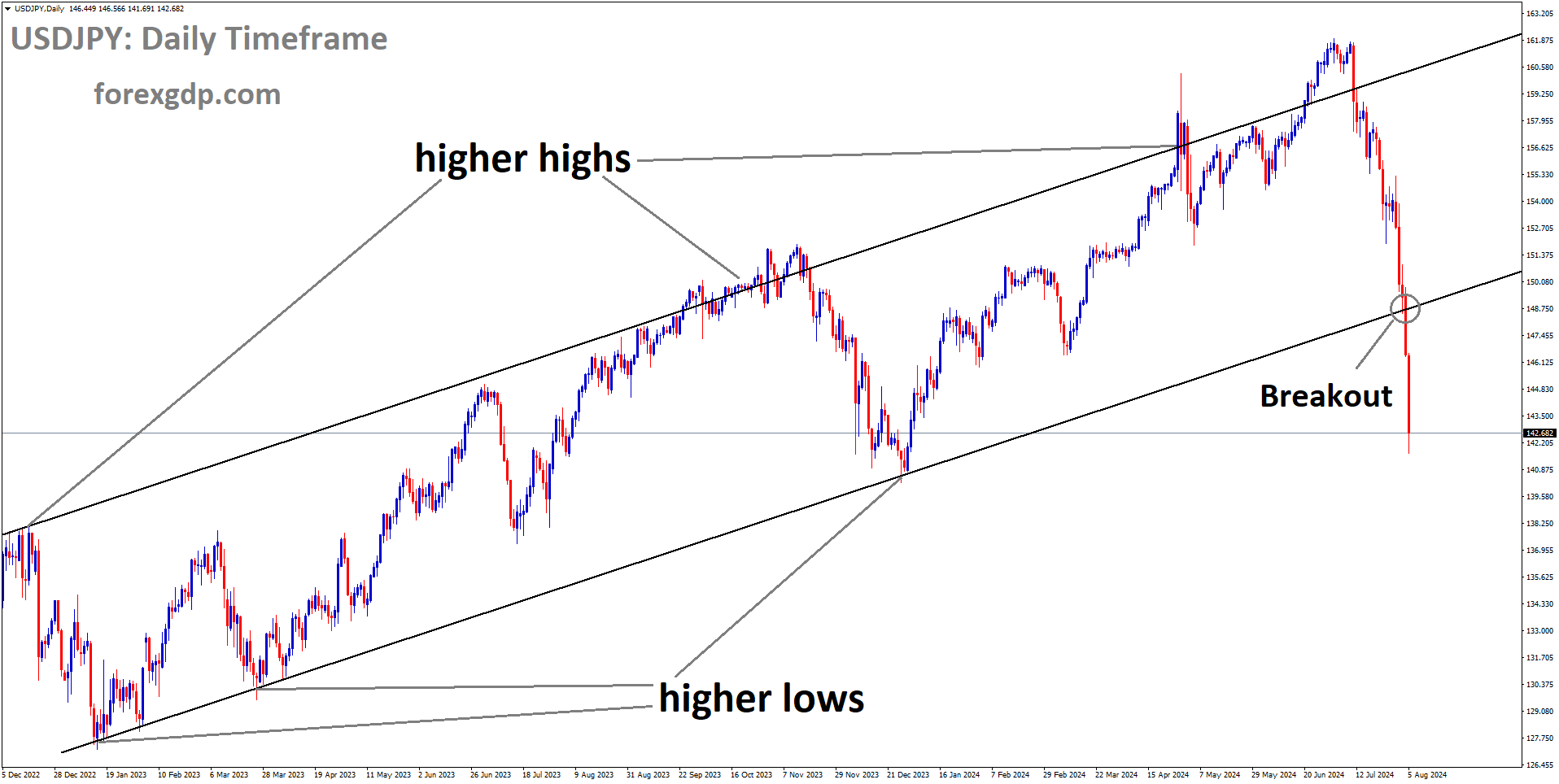

USDJPY – BoJ maintains JGB purchases at previous level

The Bank of Japan said today they are going to buy Japan Government bonds unchanged from the previous offer. 150 billion Yen in 1 year, 375 billion Yen in 1-3 Years, 425 Billion in 3-5 years, 150 billion Yen in 10-25 years. After the rate hike in last month, Buying operations of Bonds is negative for JPY in the market against Rivals.

USDJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

Bank of Japan (BoJ) made an announcement confirming its decision to maintain the purchase of Japanese Government Bonds (JGBs) at the same level as the previous offer. Specifically, the BoJ’s purchase plan includes 150 billion yen for up to 1-year JGBs, 375 billion yen for one to three-year JGBs, 425 billion yen for three to five-year JGBs, and 150 billion yen for 10 to 25-year JGBs.

EURJPY – nears 163.30 before Eurozone HICP data

The Eurozone CPI is scheduled today, Last day German inflation data came at 2.3% in March month versus 2.4% in previous month. ECB Policy Maker Robert Holzmann said he has no objection on rate cuts in June month, but we have to wait for inflation come to our target of 2%.

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Despite a modest uptick in the Japanese Yen (JPY) observed yesterday, its strength struggles to persist as investors remain wary of potential intervention by Japanese authorities to prevent significant depreciation of the currency.

The cautious sentiment, compounded by subdued risk appetite, offers some support to the safe-haven JPY. However, the Bank of Japan’s (BoJ) reluctance to pursue further policy tightening fails to instill bullish sentiment or generate substantial momentum in the market.

Japanese Finance Minister Shunichi Suzuki reiterated concerns regarding excessive exchange-rate volatility and reaffirmed authorities’ readiness to take appropriate action, providing additional backing to the Japanese Yen.

On the other hand, European Central Bank (ECB) policymaker Robert Holzmann expressed a reserved stance in a Reuters interview on Wednesday, indicating openness to a rate cut in June but emphasizing the need for more supportive data before making a decision.

In Germany, inflation moderated slightly more than anticipated in March, reaching its lowest level in almost three years. The preliminary German Harmonized Index of Consumer Prices (HICP) rose by 0.6% month-on-month (MoM) in March, slightly below the forecasted 0.7% increase. The year-on-year rate of HICP climbed by 2.3%, falling short of the market consensus of 2.4%.

The softer inflation figures suggest Germany is inching closer to the European Central Bank’s (ECB) target of 2%, fueling market expectations of a potential interest rate cut in the near future. Consequently, this exerts selling pressure on the Euro (EUR) and presents a headwind for the EUR/JPY cross. Investors are now eagerly awaiting the release of advanced Eurozone Harmonized Index of Consumer Prices data for March on Wednesday for further insights.

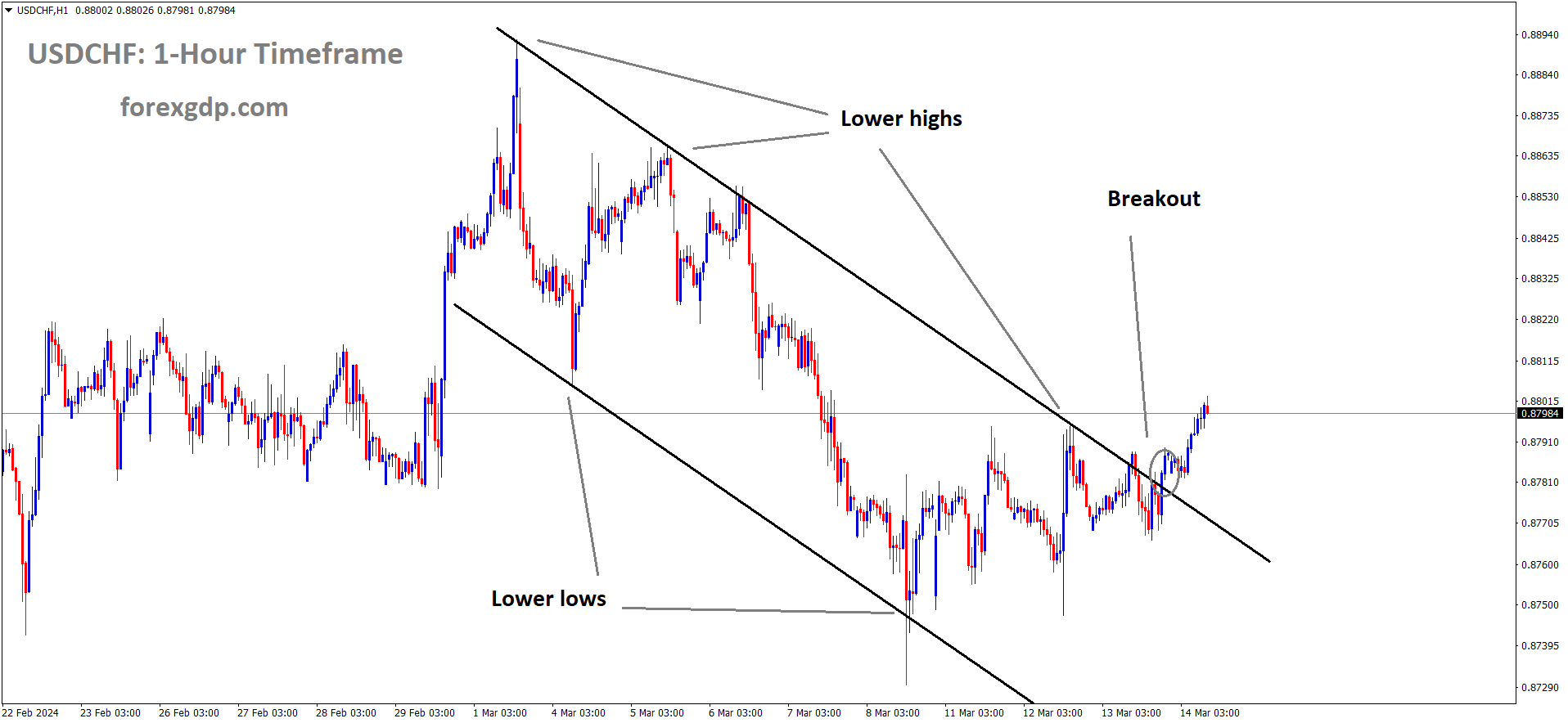

USDCHF – Stays Below 0.9100 Amid Risk-Aversion, Bulls Hold Advantage Near Year-to-Date High

The Swiss Franc is depreciated against counter pairs after the Swiss Retail sales last day printed at lower than expected. Rate cut in March month makes weaker for Swiss Franc in the market against counter pairs. US Domestic data performed well compared to Swiss economy.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc (CHF) remains pressured by the unexpected interest rate cut implemented by the Swiss National Bank (SNB) in March. This decision came amidst a quicker-than-expected slowdown in inflation and economic growth within Switzerland. Conversely, the Federal Reserve (Fed) has seen a shift in market expectations regarding rate cuts, as signs of resilience persist within the US economy. This dynamic supports the US Dollar (USD) bulls, reinforcing a positive stance on the USD/CHF currency pair.

Recent data reveals a notable expansion in the US manufacturing sector during March, marking the first growth since September 2022. Additionally, demand for labor remains robust. However, remarks from influential members of the Federal Open Market Committee (FOMC) have cast doubt on the likelihood of the Fed implementing three rate cuts throughout the year. Present market assessments suggest a total rate cut of 65 basis points (bps) for 2024, which falls short of the Fed’s projection of 75 bps announced in March.

This evolving outlook is bolstering US Treasury bond yields, which helps contain the ongoing corrective pullback in the USD from its recent peak reached on February 14th. Despite this, the prevailing risk-off sentiment typically favors traditional safe-haven assets like the CHF, potentially impeding the upward momentum of the USD/CHF pair. Consequently, traders are closely monitoring US macroeconomic data releases and speeches by key FOMC members for potential market direction cues.

USDCAD – near 1.3560, biased lower on Crude oil gains

The Canadian Dollar moving lower against USD after the higher Oil prices and higher US Domestic data. Canada Imports and exports data is scheduled this week. Domestic data performed well in Canadian economy, exports are also doing well by rising oil prices after the middle east conflicts.

USDCAD is moving in the Box pattern and the market has reached the resistance area of the pattern

This uptick in WTI price is primarily supported by two factors: the weakening US Dollar and concerns surrounding global oil supply due to ongoing geopolitical uncertainties.

The depreciation of the US Dollar Index (DXY) exerts downward pressure on the USD/CAD pair. The DXY faces challenges following dovish remarks from Federal Reserve (Fed) officials. Cleveland Fed President Loretta Mester stated her expectations for rate cuts later this year, while San Francisco Fed President Mary Daly considered three rate cuts in 2024 as “reasonable,” pending further convincing evidence.

On the economic front, Tuesday’s release of US February JOLTS Job Openings showed a modest increase to 8.756 million from the previous figure of 8.748 million, surpassing market expectations. Additionally, Factory Orders in February rebounded by 1.4% month-on-month following a 3.8% decline in the prior reading.

Looking ahead, market participants are keenly awaiting the release of Canadian Import and Export data on Thursday, alongside labor data scheduled for release on Friday. In the United States (US), focus will be on the ADP Employment Change and ISM Services PMI data on Wednesday. Additionally, Federal Reserve Chairman Jerome Powell is scheduled to deliver a speech on the US economic outlook at the Stanford Business, Government, and Society Forum in Stanford.

USD INDEX – stalls under 105.00, attention on US data and Fed’s Powell

US Dollar index climbed up higher after the US Jolts Job Openings came at 8.756M from 8.748M in Previous month. Factory orders climbed up 1.4% MoM in February than 3.8% decline in Previous month. US FED Policy makers said rate cut in June month is possible if inflation rate comes down, three rate cuts in this year is possible according to data. June month rate cut is 65% chances from 70% chances in previous poll.

USD INDEX is moving in an Ascending channel and the market has reached the higher low area of the channel

The US Dollar Index (DXY) has pulled back from its weekly peak of 105.10, influenced by the dovish sentiments expressed by Federal Reserve (Fed) officials on Tuesday. Attention now turns to forthcoming US economic indicators, notably the ADP Employment Change and the ISM Services PMI, slated for release on Wednesday.

Cleveland Fed President Loretta Mester remarked on Tuesday her anticipation of rate cuts by the US central bank this year, with the possibility of action as early as the June policy meeting, contingent upon supportive data. Similarly, San Francisco Fed President Mary Daly advocated for a baseline of three rate cuts in 2024 but emphasized the robustness of the labor market and ongoing growth, suggesting no immediate necessity for rate adjustments. Market probabilities of a rate cut by June have slightly decreased to approximately 65%, down from about 70% post the Fed’s March meeting, as indicated by the CME FedWatch Tool.

Recent data from the US Bureau of Labor Statistics revealed an increase in February JOLTS Job Openings to 8.756 million, surpassing market projections. Furthermore, Factory Orders demonstrated a month-on-month improvement of 1.4% in February, rebounding from the prior month’s 3.8% decline.

Conversely, escalating geopolitical tensions in the Middle East and the Russia-Ukraine conflict may spur demand for safe-haven assets, bolstering the US Dollar’s appeal. Recent events include airstrikes on a building within Iran’s consulate complex in Syria, resulting in casualties among Iran’s Revolutionary Guard leadership, alongside reported attacks on commercial vessels in the Red Sea.

Market participants await Fed Chair Jerome Powell’s speech later on Wednesday, anticipating insights into monetary policy and interest rate trajectories. Any inclination towards a hawkish stance by Powell could potentially uplift the Greenback against its counterparts in the immediate future.

GBPUSD – stays below 1.2600, watching US data and Fed’s Powell speech

The GBPUSD pair is moving down due to rate cut expected from BoE than FED this year. Inflation is easing more in the UK in recent months makes rate cut hopes increasing in the UK in recent days. US ADP data is scheduled today and US Domestic data performed well in this week makes US Dollar stronger against GBP.

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The GBP/USD pair continues to face pressure due to various factors, including sluggish UK inflation data and a generally negative market sentiment. Investors are closely monitoring the remarks from Federal Reserve officials on Wednesday, hoping for insights into the central bank’s stance on interest rates and future monetary policy decisions.

Several Fed policymakers expressed their views on Tuesday regarding the outlook for monetary policy. Cleveland Fed Bank President Loretta Mester indicated her expectation for interest rate cuts this year but suggested that the upcoming May policy meeting is unlikely to see any changes. Similarly, San Francisco Fed Bank President Mary Daly echoed the sentiment of anticipating rate cuts but emphasized the need for further evidence of inflationary pressures easing before any action is taken. Daly described three rate cuts in 2024 as a reasonable scenario but cautioned against assuming it as a certainty. Market indicators, such as the CME FedWatch Tool, currently suggest a reduced likelihood of a rate cut by June compared to previous estimates following the Fed’s March meeting.

In terms of economic data, the US February JOLTS Job Openings surpassed expectations, indicating strength in the labor market, while Factory Orders rebounded in February after a decline in the previous month.

Conversely, market sentiment regarding the Bank of England (BoE) cutting interest rates before the Fed this year has increased, adding downward pressure on the British Pound (GBP). Additionally, weak UK inflation figures and overall market pessimism are weighing on the GBP, limiting any potential upside for the GBP/USD pair.

Traders are awaiting key US economic indicators, including the ADP Employment Change, final S&P Global Composite PMI, and ISM Services PMI, for further direction. Furthermore, speeches from Fed officials Bowman, Goolsbee, Barr, Kugler, and Powell later in the day could impact the Greenback’s performance, potentially influencing the GBP/USD pair in the short term.

AUDUSD – AUD slips on stronger USD, awaits ISM Services PMI

The Australian Industry Group index came at -5.3 in February month when compared to -14.9. Manufacturing PMI data came at -7 from -12.6 in previous month. RBA Meeting minutes last day is not support well for Australian Dollar in the market.

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Australian Dollar (AUD) is experiencing a slight retreat on Wednesday, attributed partly to the depreciation of the US Dollar (USD), driven by downward pressure on US Treasury yields. This downward pressure is providing support to the AUD/USD pair. Additionally, the decline in the ASX 200 Index is adding to the downward pressure on the AUD.

In terms of economic indicators, the Australian Industry Group (AiG) Industry Index and AiG Manufacturing PMI both showed improvement in February. The AiG Industry Index rose to a reading of -5.3 from the previous -14.9, while the AiG Manufacturing PMI increased to -7 from the prior reading of -12.6. Furthermore, the Reserve Bank of Australia (RBA) March meeting minutes, as summarized by Westpac, indicated that the current cash rate level is deemed appropriate for the present circumstances, although this assessment may change in the future.

Conversely, the US Dollar Index (DXY) is facing challenges following dovish remarks from Federal Reserve (Fed) officials. Cleveland Fed President Loretta Mester suggested on Tuesday that rate cuts later this year are anticipated, while San Francisco Fed President Mary Daly expressed her view that three rate cuts in 2024 seem “reasonable,” subject to further evidence.

In the broader context, several economic indicators and developments are influencing market sentiment:

– The Caixin Manufacturing PMI for China came in at 51.1, surpassing expectations.

– China’s National Bureau of Statistics (NBS) reported a rise in the monthly NBS Manufacturing PMI and NBS Non-Manufacturing PMI.

– US President Joe Biden had a phone conversation with Chinese leader Xi Jinping, covering various bilateral, regional, and global topics.

– Treasury Secretary Janet Yellen is scheduled to visit China for meetings with Chinese officials and engagement with various stakeholders.

– In the US, the ISM Manufacturing PMI indicated a surprise expansion in March, reaching the highest level since September 2022, along with an increase in ISM Manufacturing Prices Paid.

These developments collectively contribute to the evolving market sentiment and are closely watched by investors for potential impacts on currency movements and broader economic trends.

NZDUSD – climbs steadily to 0.5975, reaching fresh daily peak amid slight USD weakness.

The NZDUSD is moving lower due to Strong US Domestic data printed in this week. US Economy performing well during higher rates prevailing in the market. NZ Economy is moving down after the higher rates. Rate cuts will see in next year after the inflation rate will come to RBNZ target as per RBNZ said in earlier meetings.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The USD Index (DXY), which measures the performance of the US Dollar against a basket of major currencies, has declined for the second consecutive day, moving away from its recent peak reached on February 14. This downward movement in the DXY is viewed as supportive for the NZD/USD pair. However, expectations of reduced rate cuts by the Federal Reserve (Fed) are likely to limit significant declines in the Greenback and restrain further upward movement in the currency pair.

Recent data releases indicate that the US manufacturing sector expanded in March for the first time since September 2022, while demand for labor remains strong. Additionally, comments from several influential members of the Federal Open Market Committee (FOMC) have cast doubt on the likelihood of the Fed implementing three interest rate cuts this year. Current market pricing suggests a total rate cut of 65 basis points (bps) for 2024, lower than the Fed’s projection of 75 bps.

The change in market expectations has led to a rise in the yield on the benchmark 10-year US government bond to a four-month high. This, coupled with a generally cautious sentiment in equity markets, may prompt some investors to seek refuge in the safe-haven US Dollar, thereby limiting the upside potential for the risk-sensitive New Zealand Dollar (NZD). As a result, traders may prefer to await strong confirmation of buying momentum before concluding that the NZD/USD pair has reached its bottom.

Market participants are eagerly awaiting the release of key US economic data, including the ADP report on private-sector employment and the ISM Services PMI. Additionally, speeches by FOMC members, notably Fed Chair Jerome Powell, will be closely monitored for insights into monetary policy. These factors, along with movements in US bond yields and overall market sentiment, will likely influence short-term trading dynamics in the NZD/USD pair.

CRUDE OIL – WTI attracts some buyers to nearly five-month high of $85.00, Middle East tensions rise

The Crude oil prices increasing day by day after the Middle east disruptions, Russia- Ukraine disruptions. US Oil reserves report shows 2.286 million barrels in week ending March 29, down from 9.337 million barrels in the previous week. OPEC+ meeting is scheduled today and we see the how much barrels per day reductions from meeting is expected.

Crude Oil price is moving in an Ascending channel and the market has reached the higher low area of the channel

The increase in WTI prices is driven by multiple factors, including geopolitical tensions in the Middle East and Russia-Ukraine. Recent events such as the Israeli airstrike on an Iranian embassy in Syria, ongoing attacks on Russian refineries in Ukraine, and Houthi assaults on shipping in the Red Sea contribute to fears of supply disruptions, pushing WTI prices higher.

Additionally, oil traders are closely monitoring the Joint OPEC/non-OPEC Ministerial Monitoring Committee (JMMC) meeting scheduled for Wednesday. Expectations are for the OPEC+ committee to extend voluntary production cuts into the second quarter, further supporting WTI prices.

Furthermore, data from the American Petroleum Institute (API) released on Tuesday showed a decrease in US crude oil inventories by 2.286 million barrels for the week ending March 29. This decline, following a significant increase in the previous week, also contributes to the positive sentiment surrounding WTI prices.

The softer US Dollar, amid speculation of potential rate cuts by the Federal Reserve, is another factor supporting WTI prices. Futures traders anticipate rate cuts to begin as early as the June meeting, with expectations of a three-quarters of a percentage point cut by the end of the year. A weaker US Dollar makes dollar-denominated oil cheaper for holders of other currencies, boosting oil demand and prices.

However, market participants are attentive to Fedspeak on Wednesday, with Fed officials including Bowman, Goolsbee, Barr, Kugler, and Powell scheduled to speak. Any hawkish comments from these officials could strengthen the US Dollar and potentially limit the upside for WTI prices.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/