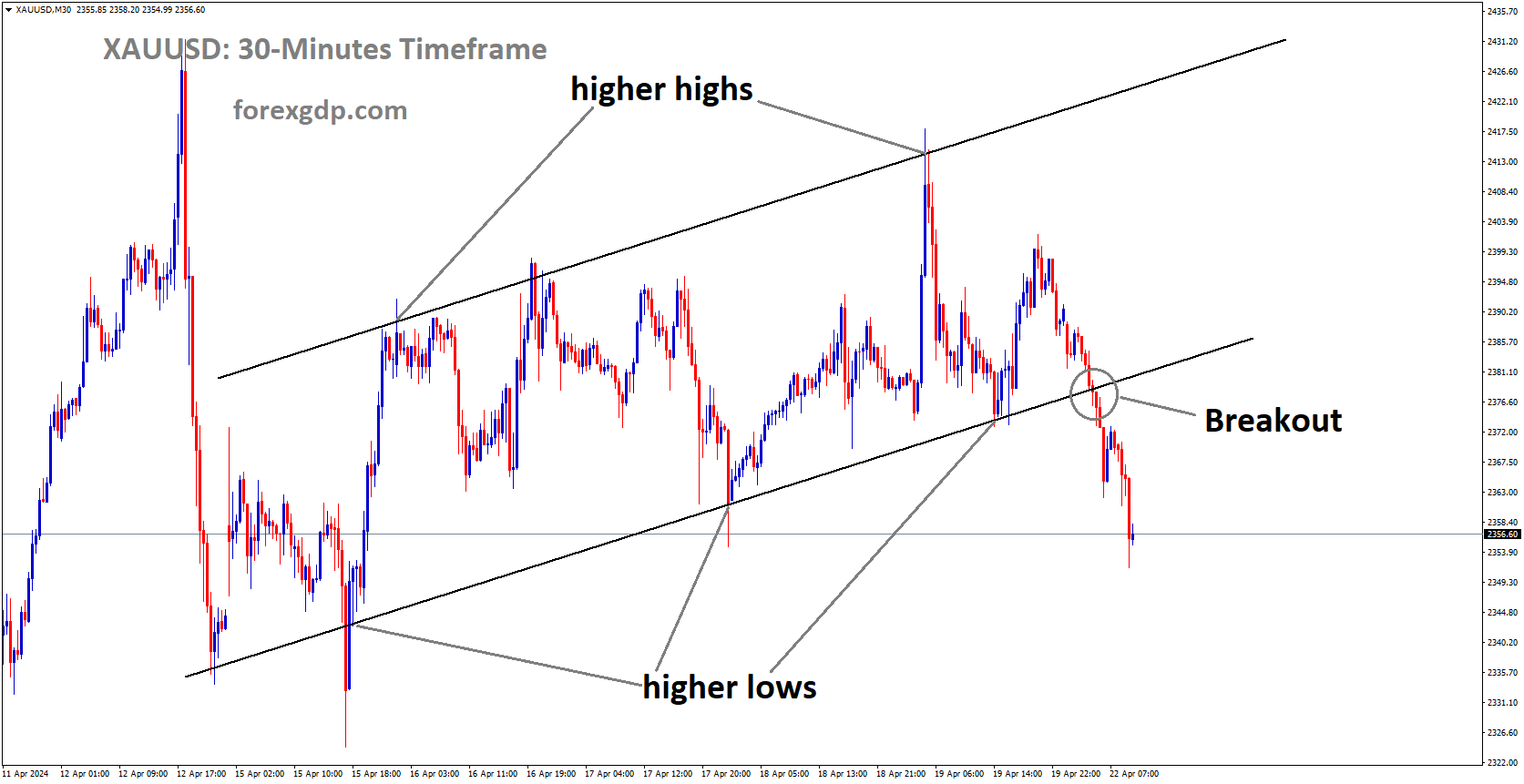

XAUUSD has broken Ascending channel in downside

GOLD – Gold Price Dips Amid Iran-Israel Optimism and Fed Rate Expectations

Gold prices (XAU/USD) face downward pressure as the new week begins, sliding to a multi-day low ahead of the European session. Investor sentiment turns upbeat amidst hopes for a de-escalation in the Iran-Israel conflict, reflected in the positive tone across equity markets. Additionally, the US Dollar’s strength, driven by hawkish Federal Reserve (Fed) expectations, prompts a flow away from the safe-haven precious metal.

Despite these pressures, speculations of forthcoming interest rate cuts by major central banks in response to worsening global economic conditions provide some support for gold. This, coupled with caution ahead of key economic releases including flash global PMIs, the Advance Q1 GDP report, and the Personal Consumption Expenditures (PCE) Price Index, tempers the downside potential for XAU/USD.

Iran’s signal of non-retaliation against the Israeli missile strike on Friday alleviates fears of further Middle East tensions, dampening demand for safe-haven assets like gold. Meanwhile, investors push back expectations of the Fed’s first rate cut to September and reduce bets on the total number of rate cuts in 2024, bolstering US bond yields and the Dollar.

Chicago Fed President Austan Goolsbee’s remarks on stalled US inflation progress reinforce the cautious stance on policy adjustments. Elevated US bond yields act as a tailwind for the Dollar, intensifying pressure on gold. Moreover, concerns about slowing global economic growth support expectations for synchronized interest rate cuts by major central banks, potentially lending further support to XAU/USD.

Traders remain watchful for upcoming economic data releases, which could provide fresh cues for gold’s direction amidst the interplay of geopolitical tensions, central bank policies, and global economic dynamics.

EURUSD: Distinct Perspectives on ECB and Fed Policies and Trends

EUR/USD pair displays a modest uptick as the US Dollar experiences a slight decline, reflecting the prevailing sentiment among several European Central Bank (ECB) policymakers in favor of maintaining higher interest rates for an extended period. Meanwhile, remarks from Fed’s Goolsbee regarding the stagnation in inflation progress and the appropriateness of the current restrictive policy of the Federal Reserve add nuance to the market dynamics.

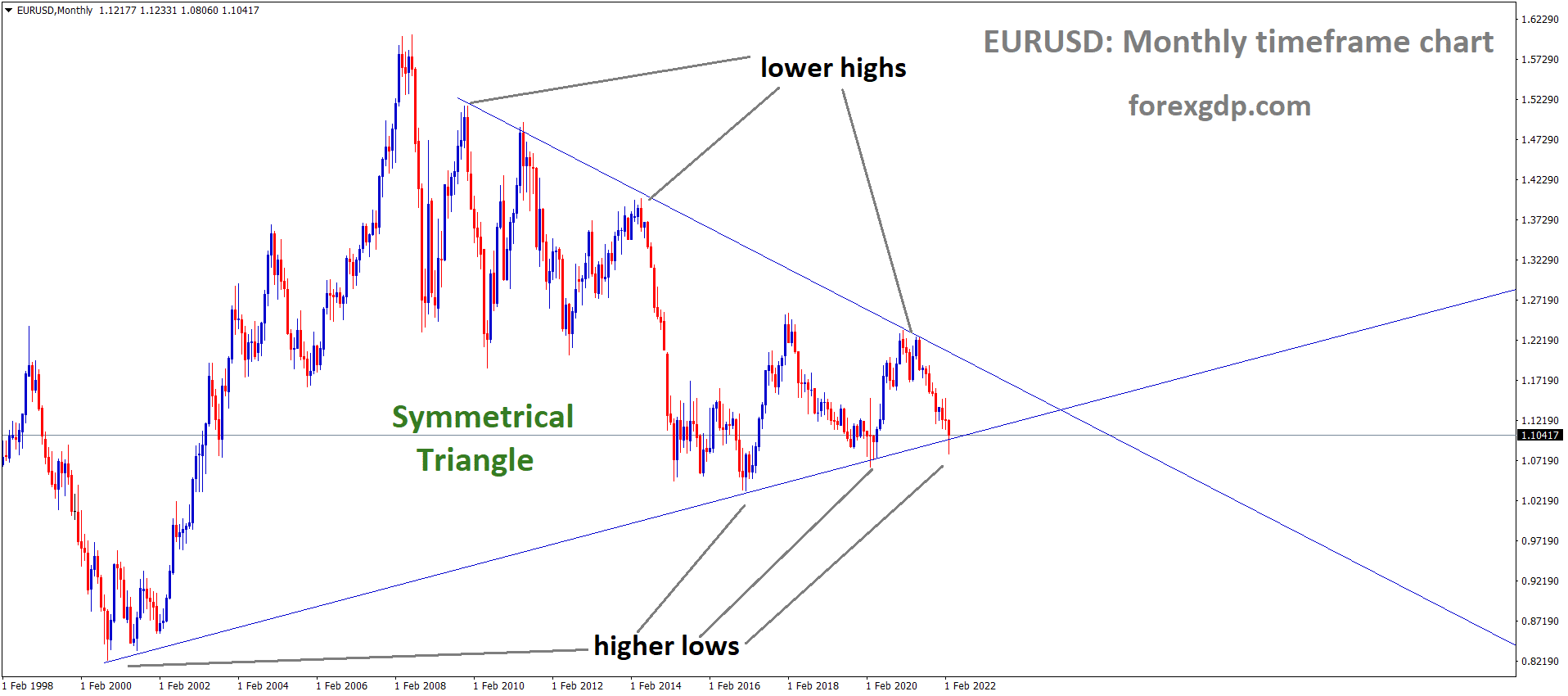

EURUSD is moving in Descending Triangle and market has fallen from the lower high area of the pattern

In the early hours of the Asian trading session on Monday, the EUR/USD pair maintains its strength. However, the potential for further gains is tempered by the anticipation of a more hawkish stance from the Federal Reserve, as indicated by recent statements from Fed officials. This anticipation could act as a limiting factor on the pair’s upward trajectory.

Market participants are closely monitoring upcoming economic data releases, particularly the preliminary Eurozone HCOB PMI for April scheduled for Tuesday, and the final reading of the US March Personal Consumption Expenditures Price Index (PCE) slated for Friday. These data points are expected to provide insights into the economic health of both regions, potentially influencing currency movements.

Looking ahead, the ECB’s upcoming June meeting is anticipated to maintain interest rates at current levels. However, there is a growing sentiment within the ECB that if significant economic developments do not materialize, an interest rate cut may be imminent. ECB officials, including François Villeroy de Galhau and Joachim Nagel, have expressed concerns about the potential adverse effects of prolonged high interest rates on the Eurozone economy. Nevertheless, caution is advised by some ECB members, such as Madis Muller and Robert Holzmann, who emphasize the need for prudence and highlight geopolitical tensions as a critical factor to consider in policy decisions.

Conversely, the US Dollar may find support from the hawkish stance of the Federal Reserve, particularly in light of ongoing geopolitical tensions in the Middle East. Fed’s Goolsbee’s acknowledgment of stalled inflation progress underscores the Fed’s commitment to its current policy stance. Atlanta Fed President Raphael Bostic’s assertion that rate cuts are unlikely until the year’s end further reinforces the market’s perception of the Fed’s cautious approach.

In summary, the interplay between central bank policies, economic data releases, and geopolitical developments continues to shape the dynamics of the EUR/USD pair, with investors closely monitoring each factor for potential implications on currency movements.

USDJPY: JPY Struggles Against USD Amid BoJ Caution and Fed Speculation

During Monday’s Asian session, the Japanese Yen (JPY) continued to struggle against the US Dollar (USD), hovering near multi-decade lows. The cautious stance of the Bank of Japan (BoJ) regarding further policy tightening, coupled with expectations of delayed interest rate cuts by the Federal Reserve (Fed), has widened the US-Japan rate differential. This, alongside optimism that tensions between Iran and Israel will not escalate further, has diminished the JPY’s safe-haven appeal.

USDJPY is moving in box pattern and market has reached resistance area of the pattern

Despite these pressures, BoJ Governor Kazuo Ueda’s recent hawkish comments and warnings from Japanese Finance Minister Shunichi Suzuki against excessive currency market movements have prevented more significant declines in the JPY. Traders are exercising caution and opting to wait on the sidelines ahead of the pivotal BoJ policy decision scheduled for Friday. Additionally, market focus will be on crucial US macroeconomic releases, including the Advance Q1 GDP on Thursday and the Personal Consumption Expenditures (PCE) Price Index on Friday, which will likely shape the near-term trajectory of the USD/JPY pair.

Friday’s data revealed a sharper-than-expected easing in Japan’s consumer inflation for March, casting uncertainty on the BoJ’s potential rate hikes and weighing on the JPY. Furthermore, Iran’s indication of no plans for retaliation against Israel’s limited-scale missile strike has bolstered investor risk appetite, further denting the JPY’s safe-haven status.

Governor Ueda’s suggestion of potential rate hikes in response to significant Yen declines to boost inflation has provided some support for the domestic currency. Minister Suzuki’s warnings to speculators against excessive JPY depreciation reinforce the government’s readiness to intervene in currency markets if necessary.

Looking at Fed funds futures, the market anticipates a less aggressive interest rate cut of around 40 basis points, or fewer than two cuts, starting in September, given persistent US inflation. This outlook suggests that the substantial rate differential between the US and Japan will persist, acting as a headwind for the JPY and offering support to the USD/JPY pair ahead of the critical BoJ policy decision.

Market expectations lean towards no policy changes following the BoJ’s historic decision last month to end its negative rate policy and Yield Curve Control program. As such, focus will likely be on the quarterly outlook report.

The upcoming US data releases, particularly the Advance Q1 GDP and the PCE Price Index, are expected to influence USD dynamics in the coming days.

USD/CAD finds itself navigating through a complex landscape marked by contrasting forces. The weakening US Dollar, despite the backdrop of elevated US Treasury yields, poses a significant challenge for the currency pair. Concurrently, the Canadian Dollar grapples with downward pressure stemming from a recent decline in WTI crude oil prices, a crucial factor given Canada’s status as a major oil exporter.

USDCAD is retesting the broken higher high area

This struggle is evident as USD/CAD experiences a prolonged decline over four consecutive trading sessions, with its value hovering around a certain level during Asian trading hours on Monday. The subdued performance of the US Dollar, juxtaposed with the backdrop of rising Treasury yields, exacerbates this downward trend. However, hints of a potential shift towards a more hawkish stance from Federal Reserve officials could potentially mitigate the extent of this decline.

Meanwhile, the Canadian Dollar faces resistance due to the aforementioned dip in crude oil prices. Given Canada’s reliance on oil exports, any fluctuations in oil prices can significantly impact the currency’s strength. The decline in WTI prices further underscores the challenges facing the Canadian Dollar’s upward momentum.

Adding to the mix, reports dismissing rumors of a Middle Eastern drone attack contribute to a gradual alleviation of risk aversion. This reduction in geopolitical tensions, albeit temporary, adds additional pressure on the USD/CAD pair.

Furthermore, softening inflation trends in Canada accentuate the divergent monetary policy outlook between the Bank of Canada and the US Federal Reserve. While Canada contemplates potential rate cuts amidst sluggish inflation and growth, the US appears to be on a different trajectory.

Federal Reserve officials, including Chicago Fed President Austan Goolsbee, acknowledge a stall in inflation progress, affirming the appropriateness of the current restrictive monetary policy. Similarly, Atlanta Fed President Raphael Bostic echoes this sentiment, suggesting a cautious approach towards interest rate adjustments until year-end.

In summary, USD/CAD faces a multitude of challenges and influences, from the performance of the US Dollar and Canadian Dollar to fluctuations in oil prices and geopolitical developments. These factors collectively shape the dynamics of the currency pair, influencing its trajectory in the global foreign exchange market.

USDCHF – Fed’s Rate Outlook and SNB Stability Focus

USDCHF Greenback Strengthens on Fed’s Rate Cut Outlook, SNB Emphasizes Stability. At the onset of Monday’s early Asian session, the USD/CHF pair maintains a positive stance, with its value near 0.9115. This upward movement is propelled by nuanced shifts in monetary policy sentiments from the central banks of both the United States and Switzerland.

USDCHF is moving in Ascending channel and market has rebounded from the higher low area of the channel

In the United States, there has been a notable adjustment in market expectations regarding the Federal Reserve’s approach to interest rates. This adjustment comes in response to persistent inflationary pressures, which have prompted many Fed officials to advocate for a more cautious stance on rate cuts. The emerging consensus suggests a willingness among policymakers to extend the timeline for any potential rate adjustments, buoying the strength of the US Dollar against the Swiss Franc.

Chicago Federal Reserve President Austan Goolsbee recently hinted at a delayed timeline for rate cuts, citing a slowdown in the pace of inflationary progress. Despite witnessing a significant decrease from its peak during the pandemic era, inflation in the US continues to hover above the Fed’s target range. Similarly, Atlanta Fed President Raphael Bostic echoed sentiments of prudence, signaling that rate cuts are unlikely until the latter part of the year. These statements contribute to the prevailing narrative of an extended period of elevated interest rates in the US, thereby reinforcing the Greenback’s position.

Meanwhile, in Switzerland, the Swiss National Bank (SNB) underscores the importance of maintaining monetary policy focus on price stability. SNB Chairman Thomas Jordan emphasized this commitment, highlighting the need to navigate economic challenges while ensuring inflation remains within acceptable bounds. However, amidst such efforts, concerns persist regarding geopolitical tensions, particularly in the Middle East. Escalating tensions, especially between Israel and Iran, have the potential to elevate demand for safe-haven assets like the Swiss Franc, thereby exerting a limiting influence on the USD/CHF pair’s upward trajectory.

Looking ahead, market participants eagerly anticipate key economic indicators, including the preliminary US Gross Domestic Product Annualized for the first quarter and the Personal Consumption Expenditures Price Index. These indicators are poised to provide further insights into the evolving dynamics of both currencies. Against the backdrop of shifting central bank policies, inflationary trends, and geopolitical developments, the USD/CHF pair navigates a landscape characterized by complexity and uncertainty.

GBPUSD: Geopolitical Shifts and Fed Speculation Impact Markets

GBP/USD pair’s movements provided a comprehensive snapshot of market dynamics. Despite initial interest from investors seeking to leverage a weakened USD, the pair struggled to sustain significant upward momentum.

GBPUSD has broken box pattern in downside

A pivotal factor influencing market sentiment was the easing of geopolitical tensions, notably in the Middle East. Iran’s announcement of no plans for retaliation against Israel’s limited-scale missile strike alleviated concerns, fostering a boost in market confidence. Consequently, safe-haven assets like the US dollar witnessed reduced demand as investors shifted away from risk aversion.

Shifting expectations surrounding the US Federal Reserve’s monetary policy stance were equally impactful. Earlier speculation hinted at imminent rate cuts, but sentiment shifted as expectations were deferred, possibly towards September. Additionally, there was a notable reduction in the anticipated number of rate cuts for the year. This more hawkish outlook for Fed policy bolstered higher US Treasury bond yields, providing support for the USD against the GBP.

Despite the relative weakness of the USD, the GBP faced obstacles in achieving substantial gains. Speculation surrounding potential aggressive policy easing measures by the Bank of England acted as a restraining factor, curbing the GBP’s upward trajectory.

In terms of economic data, the day saw no significant releases from both the UK and the US. Consequently, spot prices were primarily influenced by broader USD dynamics. Attention swiftly turned to upcoming key data releases later in the week, including the Advance Q1 GDP report and the Personal Consumption Expenditures (PCE) Price Index from the US. Additionally, market participants awaited the flash PMI prints from both the UK and the US for insights into the future direction of the GBP/USD pair.

AUDUSD – Geopolitical Shifts and Central Bank Sentiment Impact

AUD/USD experienced a reversal of fortunes, breaking its two-day losing streak amidst indications of easing tensions in the Middle East. An Iranian official’s suggestion of no immediate retaliation against Israeli airstrikes boosted market confidence, propelling the Australian Dollar (AUD) higher.

AUDUSD has broken box pattern in downside

However, challenges loom for the AUD, particularly with the Reserve Bank of Australia (RBA) maintaining a cautious stance amidst moderating domestic inflation and ongoing labor market tightness. This could potentially pave the way for rate cuts before year-end, injecting uncertainty into the currency’s outlook.

In contrast, the US Dollar (USD) may find support despite initial pressure, buoyed by a rise in US Treasury yields and hints of a hawkish shift in Federal Reserve (Fed) rhetoric.

Other notable developments include the People’s Bank of China’s decision to hold its Loan Prime Rates (LPR) and China’s imposition of tariffs on US goods, which could impact the Australian market given its strong economic ties with China.

Over the weekend, the AUD continued to strengthen amidst relatively calm geopolitical conditions, with US Secretary of State Antony Blinken urging restraint following reports of Iranian missile strikes, further bolstering market sentiment towards the AUD.

On the monetary policy front, statements from Chicago Fed President Austan Goolsbee and Atlanta Fed President Raphael Bostic underscored a cautious approach, expressing concerns over inflation progress and a commitment to maintaining interest rates unchanged until year-end.

Looking ahead, traders will closely monitor forthcoming Purchasing Managers Index (PMI) data from both Australia and the US, as well as key economic releases such as the Australian Consumer Price Index (CPI) and the US Gross Domestic Product Annualized report. These data releases are anticipated to influence market dynamics and provide fresh insights into currency movements.

AUD/JPY made notable gains in the latest trading sessions, breaking free from a recent downtrend as geopolitical tensions remained relatively subdued over the weekend. The currency pair’s upward movement was particularly significant given the absence of any major developments on the geopolitical front, providing investors with a sense of relief and prompting a shift towards riskier assets.

AUDJPY is moving in Descending channel

US Secretary of State Antony Blinken played a crucial role in stabilizing market sentiment by calling for calm amidst concerns over potential retaliation from Iran. Blinken’s reassurance followed statements from Iranian officials indicating that there were no immediate plans for retaliatory action, particularly in response to reported Israeli missile strikes. This diplomatic effort aimed at de-escalating tensions helped ease investor concerns, contributing to the positive momentum in the AUD/JPY pair.

Meanwhile, the Japanese Yen faced its own set of challenges as Bank of Japan (BoJ) Governor Kazuo Ueda emphasized the need to maintain loose monetary policies. Speaking at a seminar hosted by the Peterson Institute for International Economics, Ueda underscored the importance of sustaining accommodative measures due to persistently low inflation levels. He pointed out that underlying inflation remained below the BoJ’s 2% target, while long-term inflation expectations hovered around 1.5%. Ueda’s remarks signaled a commitment to continued monetary stimulus, which exerted downward pressure on the Yen.

The Australian Dollar (AUD) saw support from a buoyant domestic equities market, with the ASX 200 Index posting gains for the second consecutive session. The rally was fueled by a surge in metal prices, including Iron Ore, Copper, and Gold, reflecting improved investor confidence. This positive sentiment was further bolstered by a reduction in geopolitical tensions in the Middle East, which alleviated concerns and spurred risk-taking behavior among traders.

In China, the decision by the People’s Bank to maintain its Loan Prime Rates at 3.45% had implications for the Australian market due to the close economic relationship between the two countries. Additionally, China’s imposition of a new tariff on US goods, specifically targeting imports of propionic acid with a duty of 43.5%, added another layer of complexity to global trade dynamics.

In Japan, the National Consumer Price Index (CPI), excluding fresh food but including fuel costs, showed signs of moderation, expanding by 2.6% year-over-year in February. While this figure remained above the BoJ’s target, it represented a slowdown from the previous month’s four-month high of 2.8%, primarily driven by modest increases in food prices. However, the weakness of the Yen and elevated commodity prices continued to exert upward pressure on inflation.

")

Looking ahead, market participants will closely monitor upcoming economic data releases, including Purchasing Managers Index (PMI) and Consumer Price Index (CPI) reports from Australia. These indicators will provide insights into the health of the economy and could influence trading activity in the AUD/JPY pair, shaping market sentiment in the days ahead.

NZDUSD – Strengthens Amidst Positive Sentiment

NZD/USD maintains a positive stance as the early Asian session unfolds on Monday, benefiting from a weaker US Dollar (USD). Several factors contribute to the pair’s upward movement, shaping market sentiment.

A prevailing risk-on sentiment in the market has fueled demand for riskier assets like the New Zealand Dollar (NZD). Additionally, there is a modest retreat of the USD, providing further support to the NZD’s upward trajectory.

NZDUSD is moving in Descending channel and market has reached lower low area of the channel

Traders are closely monitoring forthcoming inflation data, particularly following the Reserve Bank of New Zealand’s (RBNZ) recent inflation figures. While inflation continues to decline, it remains within the RBNZ’s target range of 1 to 3%. Speculation arises that the RBNZ may consider a rate cut from the November meeting, potentially providing support to the NZD.

Moreover, recent tensions in the Middle East have seen a de-escalation, with both Israel and Iran downplaying the possibility of further conflicts following Israel’s reportedly minor strike on Iran. This development has contributed to an improved market sentiment, lifting riskier assets like the NZD.

Conversely, remarks from Chicago Federal Reserve (Fed) President Austan Goolsbee on Friday indicate a potentially longer timeline for interest rate cuts. Goolsbee notes stalled progress on inflation, with inflation levels remaining persistently above the Fed’s target despite a decline from its pandemic-era peak of 9.1%. This narrative of sustained higher US rates may strengthen the Greenback, presenting a challenge for the NZD/USD pair.

Additionally, on Monday, China’s Ministry of Commerce implemented new tariffs on US imports, imposing a 43.5% tax specifically on imports of propionic acid from the US. While this move reignites trade tensions between the US and China, the NZD/USD pair continues to maintain its upward momentum.

XTIUSD – WTI Oil Prices React to Geopolitical Developments and US Sanctions Dynamics

West Texas Intermediate (WTI) oil prices exhibit a downward trend, closely mirroring their monthly low, amidst a confluence of factors shaping the global oil market.

XTIUSD is moving in Ascending channel and market has reached higher low area of the channel

A pivotal contributor to this decline is the relaxation of geopolitical tensions in the Middle East. Reports indicating a reduction in hostilities between Israel and Iran following Israel’s targeted strike assuage concerns over potential disruptions to oil supply chains in the region. This easing of tensions alleviates market anxieties and contributes to the bearish sentiment surrounding oil prices.

Additionally, the recent passage of new sanctions by the US House targeting Iran’s oil sector introduces a new dimension of uncertainty. These sanctions, slated to be incorporated into a foreign aid package, prompt speculation regarding their potential ramifications on global oil supply dynamics. While the sanctions aim to curb Iran’s crude oil exports, the extent of their impact hinges on various factors, including the scope of the sanctions and the responses of other key oil-producing nations.

Moreover, the expansion of secondary sanctions to encompass transactions involving Chinese financial institutions and sanctioned Iranian banks adds further complexity to the oil market landscape. The potential disruption of financial flows related to petroleum and oil-derived products underscores the intricacies involved in assessing oil price movements.

On the demand side, market sentiment is influenced by expectations surrounding US monetary policy. The Federal Reserve’s hawkish stance, driven by concerns about persistent inflation, hints at the likelihood of prolonged periods of elevated interest rates. This scenario has the potential to bolster the US dollar, rendering oil more expensive for countries utilizing alternative currencies and potentially curbing global demand.

Of particular significance are the hawkish pronouncements from Federal Reserve officials, such as Chicago Fed President Austan Goolsbee and Atlanta Fed President Raphael Bostic. Their affirmations of a tighter monetary policy stance align with market expectations and contribute to the prevailing downward pressure on crude oil prices.

In summary, WTI oil prices navigate through a complex interplay of geopolitical developments, US sanctions dynamics, and monetary policy expectations. As market participants seek to discern the implications of these multifaceted factors, vigilance and thorough analysis remain paramount for understanding and forecasting oil price movements in the foreseeable future.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!